Energy Transfer: Stay The Course And Load Up On Steep Pullbacks

Summary

- Energy Transfer LP unitholders have seen a remarkable revival in their fortunes as the company rallied significantly over the past few weeks.

- The recent acquisition of Crestwood is expected to expand Energy Transfer's market leadership and bolster its distributable cash flows.

- Energy Transfer's valuation remains attractive, and its solid distribution yield offers holders a defensive play in a leading midstream company.

- Despite that, I assessed that near-term caution is warranted, given its recent sharp recovery. Buying the next steep pullback could help improve risk/reward markedly.

- I do much more than just articles at Ultimate Growth Investing: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

pandemin

Leading midstream player Energy Transfer LP's (NYSE:ET) unitholders have recently enjoyed a remarkable revival in its fortunes as ET re-tested its January 2023 highs.

I updated holders in my previous article in July, upgrading ET to Strong Buy on the back of my bullish thesis on the sector. Given ET's attractive valuation to peers (assigned a "B" valuation grade by Seeking Alpha Quant), I have confidence Energy Transfer is well-positioned to benefit from the recovery. Bolstered by its industry-leading profitability (assigned "A-" profitability grade by Seeking Alpha Quant), value and income investors looking for a defensive energy play have likely added more exposure to ET.

As such, ET has significantly outperformed the S&P 500 (SP500) on a total return basis since my update. However, I also noted that its upward momentum has stalled as it re-tested its January 2023 highs, suggesting near-term caution is warranted.

Despite that, it underscores the market's confidence in its recent acquisition of Crestwood (CEQP), which is expected to expand its market leadership by gaining exposure into the Powder River basin. The $7.1B all-equity deal is expected to be "immediately accretive" to Energy Transfer's distributable cash flow, or DCF, upon closing. As such, Energy Transfer should maintain its ability to keep its adjusted EBITDA leverage ratio in the 4-4.5x range.

Crestwood's confidence in accepting the all-equity deal supports my thesis that ET is attractively valued. Accordingly, management updated holders it believes "in the potential for Energy Transfer's unit price to increase over time, driven by the execution of the business plan." The LP also accentuated the potential of upward re-rating in ET's valuation "toward a trading multiple of above 9x firm value to EBITDA, in line with peer groups."

Accordingly, ET last traded at a forward EBITDA of 7.8x, well below its 10Y average of 10.8x. Moreover, its attractive forward distribution yield of 9.3% offers unitholders a solid defensive profile against underlying market volatility. As such, while I expect some near-term downside, I also expect dip-buyers to return strongly to underpin its attractive valuations.

Analysts' estimates suggest Energy Transfer's DCF is expected to inflect back into growth in FY23, up 1.5%. It's sufficient to cover its distributions, supporting income investors looking for predictable income streams while leveraging Energy Transfer's 90% fee-based EBITDA composition. Analysts' estimates (ex-Crestwood) also suggest a re-acceleration in Energy Transfer's adjusted EBITDA growth for FY23, up 1.5% after last year's 0.4% uptick. It's slightly above the midpoint outlook of Energy Transfer's adjusted EBITDA guidance range of between $13.1B and $13.4B.

Therefore, I assessed that the market is likely pricing in a further growth uptick in Energy Transfer's underlying business as it looks to close its recent acquisition.

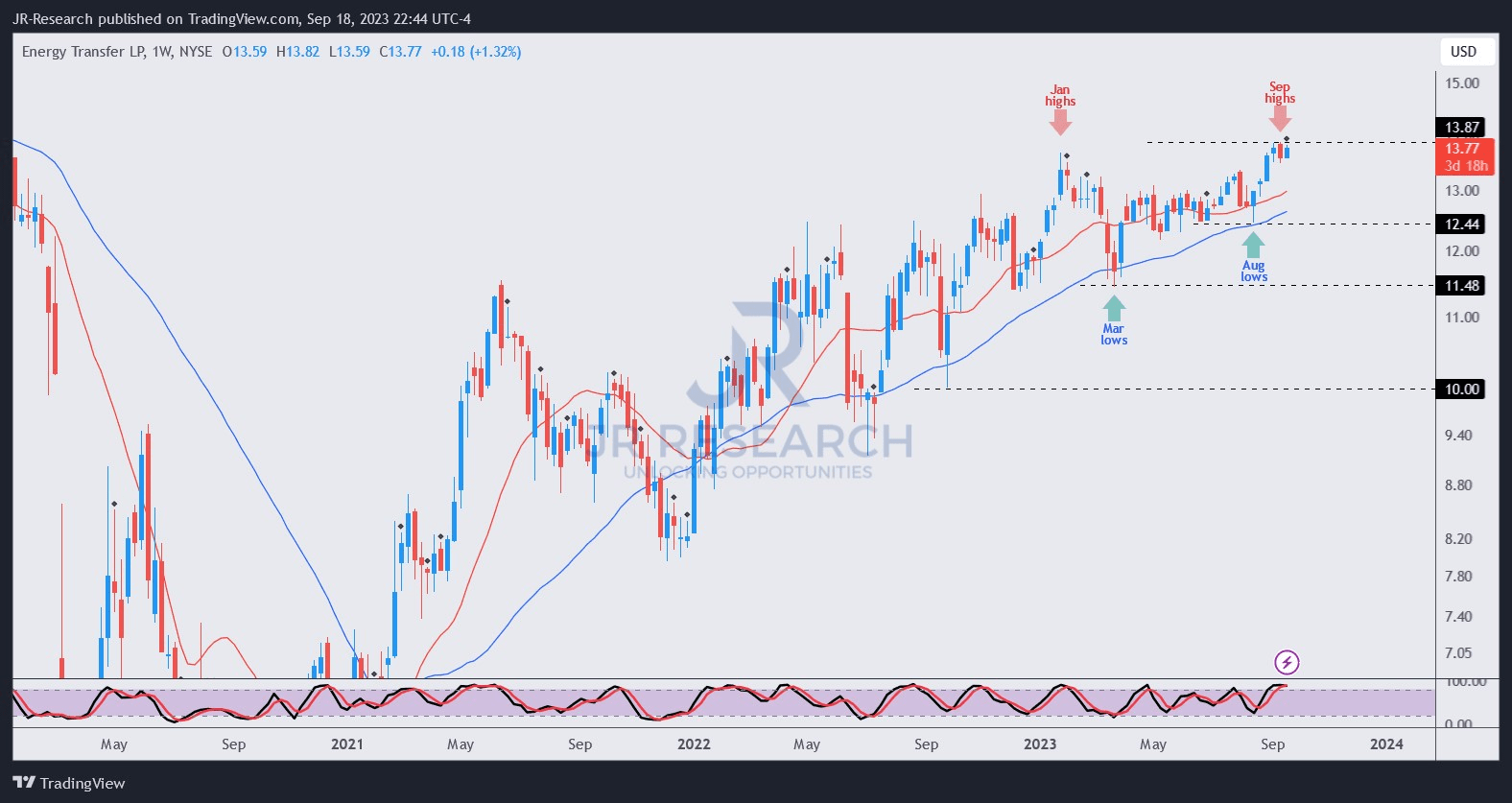

ET price chart (weekly) (TradingView)

Notwithstanding Energy Transfer's fee-based adjusted EBITDA predictability, ET's price action remains relatively volatile. As seen above, ET experienced sharp upswings/downswings over the past year. Hence, I assessed that investors looking for a more attractive risk/reward proposition consider buying more aggressively when ET falls closer to its critical moving average support levels (blue line).

With ET's upward momentum seemingly stalling as it re-tested its January 2023 highs, I gleaned near-term caution is apt. As such, I move back to the sidelines at the current levels as we assess another opportunity to move back into ET at more attractive support zones.

Rating: Downgraded to Neutral.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn't? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA's bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!

This article was written by

Ultimate Growth Investing, led by founder JR Wang of JR Research, helps investors better understand a range of investment sectors with a focus on technology. JR specializes in growth investments, utilizing a price action-based approach backed by actionable fundamental analysis. With a powerful toolkit, JR also provides insights into market sentiments, generating actionable market-leading indicators. In addition to tech and growth, JR also offers general stock analysis across a wide range of sectors and industries, with short- to medium-term stock analysis that includes a combination of long and short setups. Join the community today to improve your investment strategy and start experiencing the quality of our service.

Seeking Alpha features JR Research as one of its Top Analysts to Follow for the Technology, Software, and the Internet category, as well as for the Growth and GARP categories.

JR Research was featured as one of Seeking Alpha's leading contributors in 2022.

About JR: He was previously an Executive Director with a global financial services corporation and led company-wide, award-winning wealth management teams consistently ranked among the best in the company. He graduated with an Economics Degree from Asia's top-ranked National University of Singapore (NUS). NUS is also ranked among the top ten universities globally. I currently hold the rank of Major as a Commissioned Officer (Reservist) with the Singapore Armed Forces.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (4)

When my CEQP holdings become ET holdings my only concern will be the reaffirmation that today's Kelcy Warren is no longer the Kelcy Warren of the past.

Elliot Miller