Arista Networks: Resilience And Future-Forward Strategy

Summary

- Arista Networks demonstrated impressive performance in Q2 2023, achieving an EPS of $1.58 with strong revenue and margins.

- The Company stands out in the enterprise sector with robust demand and steady growth in data center and campus domains.

- ANET's strategic positioning in generative AI applications presents growth potential and future opportunities.

da-kuk

Investment action

Based on my current outlook and analysis on Arista Networks (NYSE:ANET), I recommend a buy rating. In the second quarter, ANET demonstrated impressive performance, achieving an EPS of $1.58, propelled by robust revenue and strong gross and operating margins. Looking forward, ANET foresees a continued positive trajectory into H2 2023, expecting Q3 revenues in the range of $1.45 billion to $1.5 billion.

ANET stands out in the enterprise sector with robust demand and steady growth in the data center and campus domains. Their market share gains are attributed to the shift towards modern cloud models and a diversified portfolio. Their leadership in both data center and cloud switching, backed by outstanding software solutions, instills confidence in sustained revenue growth. Additionally, their foray into AI switching aligns well with the evolving AI landscape, presenting a promising prospect. ANET's proactive strategies and strong market presence set a promising foundation for their future growth and success.

Basic Information

ANET stands at the forefront of data-driven networking, seamlessly connecting clients to the cloud in modern data center and campus workspace settings. From the outset, ANET embarked on a path to distinguish its framework through two fundamental pillars: an unwavering commitment to top-tier quality and operational efficiency, all powered by ANET's cutting-edge networking operating system known as the Extensible Operating System [EOS]. This innovative system, in conjunction with a suite of network applications and Ethernet switching and routing platforms utilizing advanced merchant silicon, delivers an enhanced balance of cost-effectiveness and speed to market. The result is a robust cloud networking solution that excels in high performance, scalability, and availability, enabling streamlined network automation, enhanced visibility, and fortified security.

Over the last decade, ANET has achieved a remarkable growth rate, boasting a CAGR of approximately 28%. Furthermore, in terms of EBITDA margins, ANET has demonstrated substantial and consistent expansion. Specifically, the EBITDA margin stood at around 22% in 2013, but by 2022, it had surged impressively to reach a remarkable 43%.

According to ANET's investor presentation in February 2023, their presence in the high-speed data center switching market has been rapidly expanding over the past decade. In 2020, ANET held a mere 4.9% share in ports, but by 2022, this had surged to an impressive 22.6%. Conversely, CISCO's share decreased notably from 71.4% to 29.6% during the same period.

Review

Strong revenue and both gross and operating margins helped ANET achieve an EPS of $1.58 in the second quarter of 2023. The reported revenue for 2Q23 stood at $1.46 billion. Product revenue marked $1.26 billion, reflecting a notable 42% year-over-year increase, while services revenue amounted to $197 million, showing a respectable 19% year-over-year growth. The adjusted EBIT reached $607 million, showcasing a solid 41.6% margin. Overall, ANET's second quarter results were robust, and I anticipate this positive trend continuing into the second half of the year.

ANET outlined their 3Q23 guidance, anticipating revenues between $1.45 billion and $1.5 billion and aiming for adjusted EBIT margins of 41%. Additionally, ANET foresees sustainability of these margins in 4Q23 by reducing reliance on brokered parts and optimizing manufacturing output, while also pivoting towards fulfilling a greater volume of enterprise orders. Management has also increased its 2023 revenue growth projection to exceed 30% year-over-year, compared to the previous estimate of around 26%, and has also shared expectations for double-digit revenue growth in 2024. This optimistic guidance underscores management's confidence in the robustness of ANET's business model.

My confidence was bolstered by the fact that, in contrast to the cautious enterprise spending observed in other firms, ANET continues to see robust enterprise demand and steady growth in both the data center and campus domains. This tells me that ANET is, again, winning share which I attribute to the ongoing architectural shift in numerous enterprises towards a modern cloud operating model and the broadened portfolio of offerings. As ANET continues to win share, I expect the increasing contribution from enterprise vertical to lead to a sequential improvement in margins throughout 2023, complemented by a reduction in supply chain costs. A core part of my belief here is that I am positive about ANET's proactive approach to aligning with the evolving needs of enterprises and diversifying its offerings, which has positioned the company favorably in the market.

As ANET continues to see robust enterprise demand and steady growth in both the data center, ANET's prime position in data center switching positioned them well to capture the growth. ANET's dominance in cloud switching is anchored in its exceptional platform, featuring a top-tier EOS and distinct software solutions. In addition to excelling in the cloud sector, ANET's emphasis on superior, adaptable software has conferred a competitive edge in enterprise data centers and campus installations. As a result, ANET is consistently increasing its market share. I have confidence that its dominance in data center switching will allow them to growth in the foreseeable future as the ride on the robust enterprise demand and steady growth in both the data center.

In recent times, the emergence of generative AI, exemplified by ChatGPT, has begun to exert a significant influence on Data Centers and Network Infrastructures. This is primarily due to the growing necessity for instantaneous, low-latency processing of extensive Language Model databases (LLMs) to deliver responsive on-the-fly solutions, which is presenting new challenges. Consequently, the existing data and communication infrastructures are compelled to undergo extensive transformations and expansions to cater to the evolving demands of AI technology.

The generative AI sector is poised to become a $1.3 trillion market by the year 2032. To secure a substantial market share from the generative AI demand, ANET is actively engaged in rigorous testing of its AI switching portfolio. The company's strategic plans involve commencing initial deployments in infrastructure pilot projects by 2024, followed by a gradual scaling-up to larger clusters. The ultimate objective is the establishment of a comprehensive and fully operational production deployment by 2025 and beyond. As a result, ANET is strategically positioned to capitalize on the growing demand for generative AI services and solutions.

Valuation

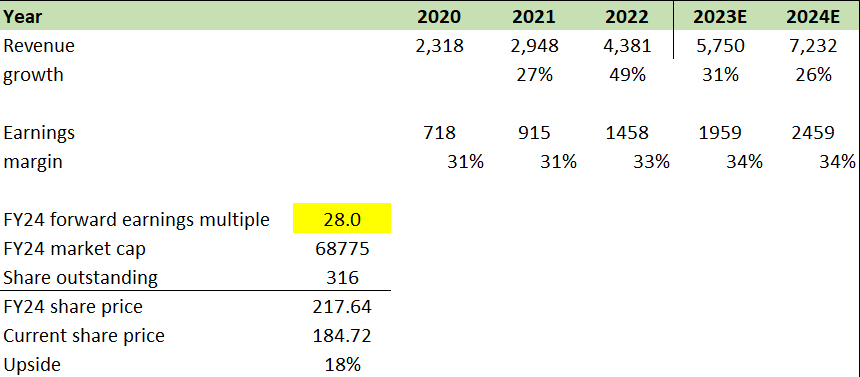

I believe ANET can grow at 26% because of its strong historical financial performance, which grew at a CAGR of 28%. Notably, in the second quarter, ANET displayed notable financial strength, showcasing a year-over-year revenue growth of 42% and maintaining strong margins at 41.6%. The margin is expected to persist into the latter half of 2023.

The ongoing enterprise shift to a modern cloud operating model and ANET's expanded portfolio of offerings continue to fuel the enterprise sector's demand, which is still very strong and characterized by consistent growth.

ANET's strategic positioning is noteworthy, especially in relation to generative AI applications. The ongoing development of its switching portfolio tailored for AI demonstrates ANET's proactive approach in this regard and is poised to capture growth due to the anticipated growth potential.

At present, ANET trades at a forward PE ratio of 28x, which is higher than its peers such as Cisco and Extreme Networks, which trade at a median P/E of 14x. ANET's premium valuation can be attributed to its superior EBITDA margin of 36.84% in comparison to the peer median of 7.77% and its lower leverage ratio (Debt-to-equity ratio of 0.88% as opposed to the peer' median of 28.30%).

Considering ANET's robust financial performance and my optimistic outlook on its future revenue growth driven by robust enterprise demand, AI initiatives, and its prime position in data center switching, my target share price is $217 (18% upside). Therefore, I recommend a buy rating for ANET.

Author's work

Risk and final thoughts

A rapid adoption of disaggregated software solutions by datacenter clients could present a challenge for ANET. ANET is known for providing top-tier switching technology by seamlessly integrating hardware and software. However, if customers unexpectedly rapidly transition towards in-house software and standardized hardware, it could pose a competitive threat to ANET.

Overall, ANET exhibits impressive financial strength and a forward-looking strategy that positions it favorably in the market. Strong Q2 2023 performance, with robust revenue and high margins, underscores its resilience. ANET's consistent growth, especially in data center switching, highlights its market dominance. The company's proactive approach in diversifying its offerings and embracing generative AI applications aligns well with evolving industry trends, ensuring future growth opportunities. With a target share price of $217, representing an 18% upside, I recommend a buy rating.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.