Heritage Financial: I Understand Why Shares Haven't Recovered

Summary

- Heritage Financial Corporation has seen a decline in deposits and a volatile revenue and profit picture in recent years.

- The bank has been successful in growing its loan book and managing leverage, but its high uninsured deposit exposure is a concern.

- The company is trading at a discount to its book value and has a low price to earnings multiple, making it an interesting but not bullish investment prospect.

- Looking for a helping hand in the market? Members of Crude Value Insights get exclusive ideas and guidance to navigate any climate. Learn More »

Fly View Productions/E+ via Getty Images

When it comes to the banking sector, there appears to be a large number of companies that offer attractive upside. This is largely because, after the banking crisis that occurred earlier this year, many of the institutions that took a beating have not regained the confidence of shareholders. For those willing to take the risk, this could result in some very nice upside.

But it's also important to keep in mind that quality does matter during this time. While any one company could go on to generate strong upside, value-oriented investors should only focus on the highest quality operators.

One bank that I was hoping would meet that bill happens to be Heritage Financial Corporation (NASDAQ:HFWA). But upon digging into its financial condition, I would argue that there are better prospects to be had at this time.

Mixed results

Originally founded in 1997, Heritage Financial is a pretty young bank. But its youth has not stopped it from growing rather quickly. By the end of its most recent completed fiscal year, the company had 50 branch offices spread throughout the state of Washington, as well as in parts of Oregon. But the company has not stopped there. In January of this year, it opened a 51st branch in Idaho, marking that branch as the first for the bank in that state. Through these locations, the bank offers clients a wide variety of services. Examples include deposit services, and the origination of loans like real estate construction loans, mortgages, and more. It even has a wealth management department that's dedicated to providing advisory services and other related services, to those clients who request them.

Author - SEC EDGAR Data

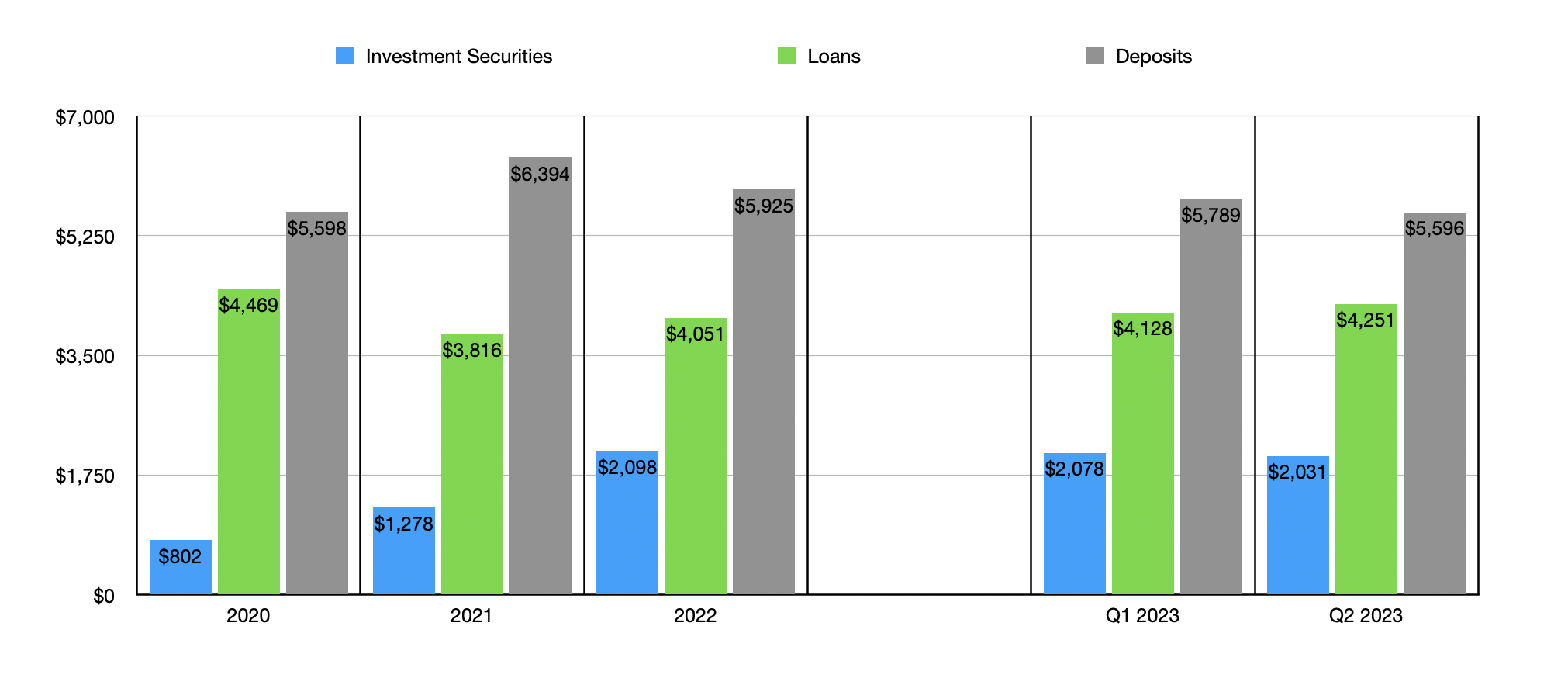

Even though it's not a dealbreaker on its own, one of the things that I look for most when considering an investment opportunity is a company that has consistently improving financial performance. I take this, as well as other indicators, as signs of quality management and a quality space that said companies trade in. Unfortunately, Heritage Financial just not exactly fit in this group. Consider, for starters, the overall trend that the institution has seen from a deposit perspective. After seeing deposits jump from $5.60 billion in 2020 to $6.39 billion in 2021, the bank then saw a consistent decline in deposits thereafter. By the end of 2022, deposits totaled $5.92 billion. They dropped further to $5.79 billion during the first quarter of 2023 before falling even more to just under $5.60 billion again at the end of the second quarter of this year.

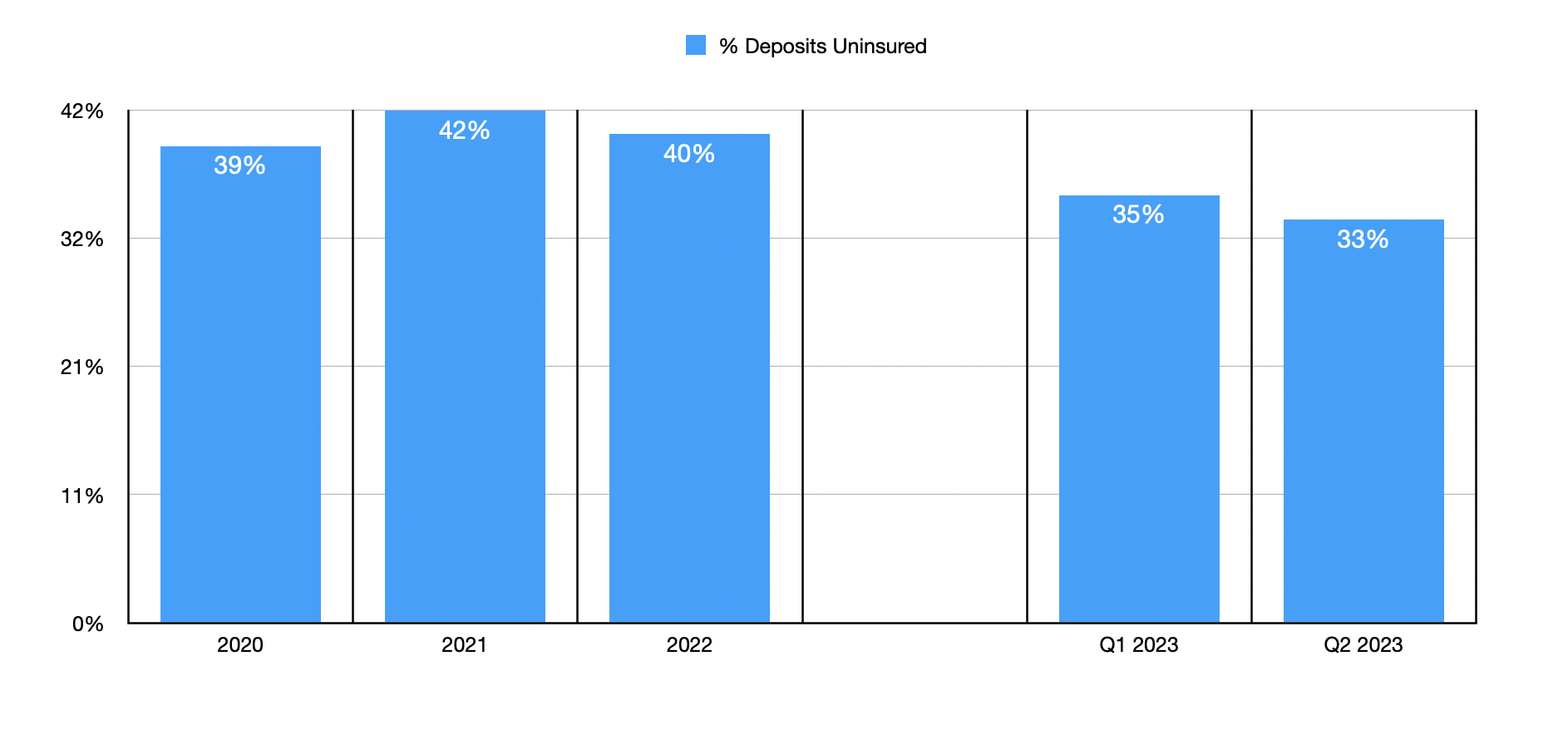

Some of this decline is almost certainly attributable to changes in depositor sentiment. Many financial institutions have seen deposits decline over the past couple of years because, as interest rates have risen, depositors have looked elsewhere for more attractive returns for their capital. But also, earlier this year, we had the banking crisis that also spooked a number of market participants. More likely than not, much of the decline seen since the end of last year can be chalked up to the effects of the banking crisis. I say this because, from 2021 to 2022, the company's exposure to uninsured deposits only budged slightly, dipping from 42% to 40%. But by the end of the most recent quarter, it had fallen to 33%. Fears of financial collapse and the very real possibility at the time that those with uninsured deposits could lose out on most or all of their money, led to significant drawdowns at certain financial institutions. It seems to me as though Heritage Financial was no exception.

Author - SEC EDGAR Data

Even though deposits have been on the decline, loans have been increasing. At the end of 2021, Heritage Financial had $3.82 billion worth of loans on its books. Today, that number is $4.25 billion. Over that same window of time, the value of investment securities also grew, jumping from $1.28 billion to $2.03 billion. Management has achieved this while keeping debt in check. This is not to say that there has not been any debt though. At the end of 2022, the bank had $21.5 million in debt. Today, that number is $471.6 million.

Heritage Financials

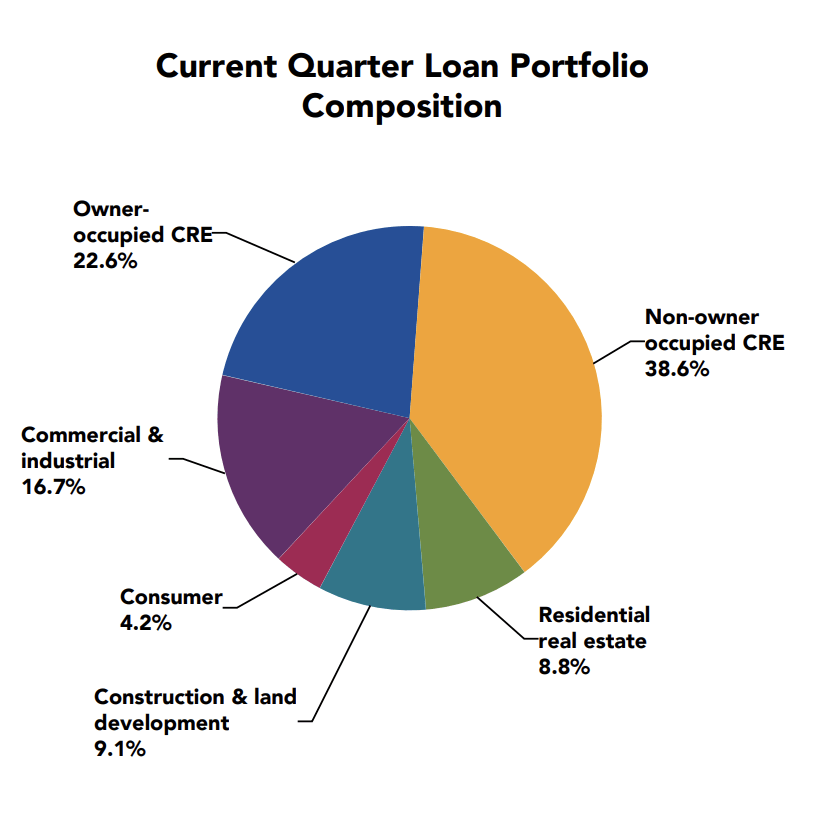

Touching on the loans for another minute, it should be mentioned that the greatest exposure for the bank involves residential real estate. About $1.64 billion, or 38.6%, of all loans fall under this category. The next largest exposure comes from owner occupied commercial real estate at $959 million, or 22.6% of all loans. This is followed up by $708 million, or 16.7%, that involves commercial and industrial assets. For those worried about exposure to office properties, management did reveal that 22% of all commercial real estate loans, by value, have been granted with office properties as collateral. Although this may sound like a lot, it translates to approximately 13.5% of all loans. Frankly, this is a bit higher than I would normally like to see. But it's not necessarily bad either.

Author - SEC EDGAR Data

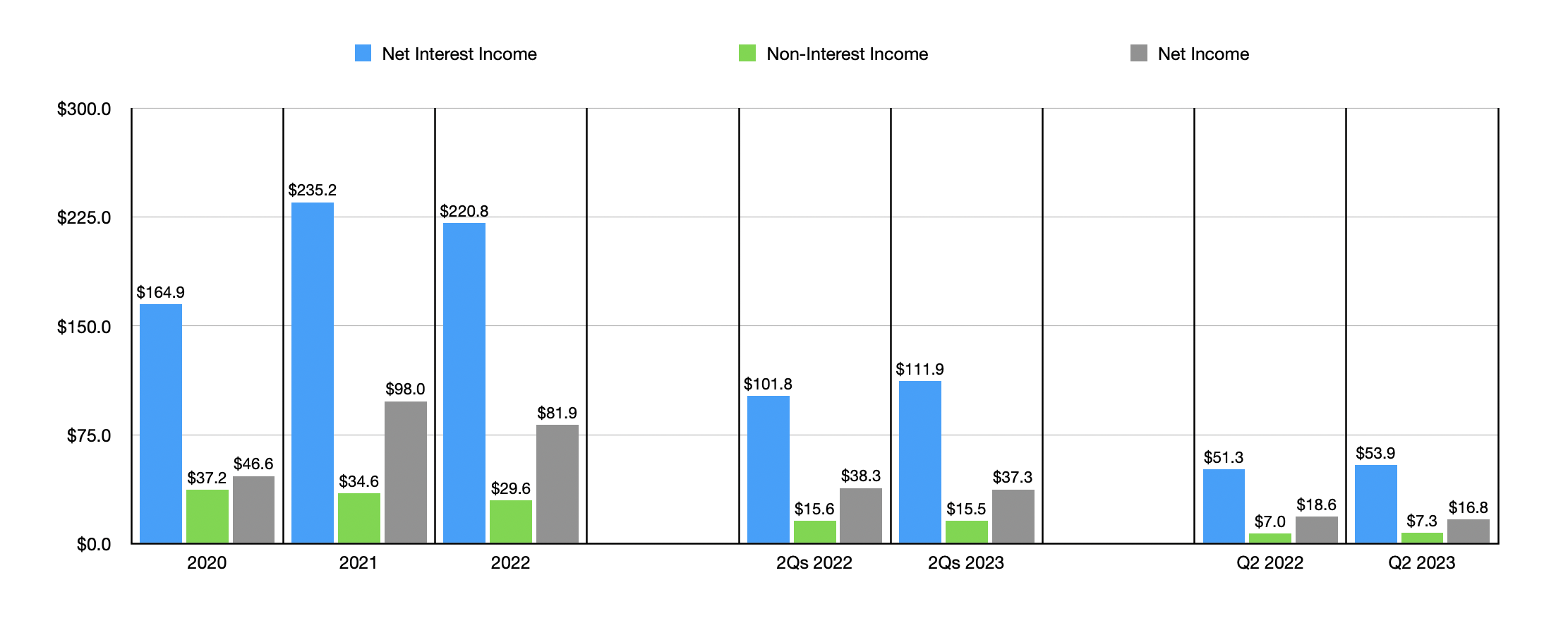

Lumpy deposit values have also resulted in rather lumpy revenue and profits in recent years. Net interest income, for instance, went from $164.9 million in 2020 to $235.2 million in 2021. But then, in 2022, it came in at $220.8 million. So far this year, net interest income is higher than it was last year, rising from $101.8 million to $111.9 million. When it comes to non-interest income and net income, there has also been some volatility from year to year. Nothing extreme, but also not the kind of consistency that I would prefer to see.

Author - SEC EDGAR Data

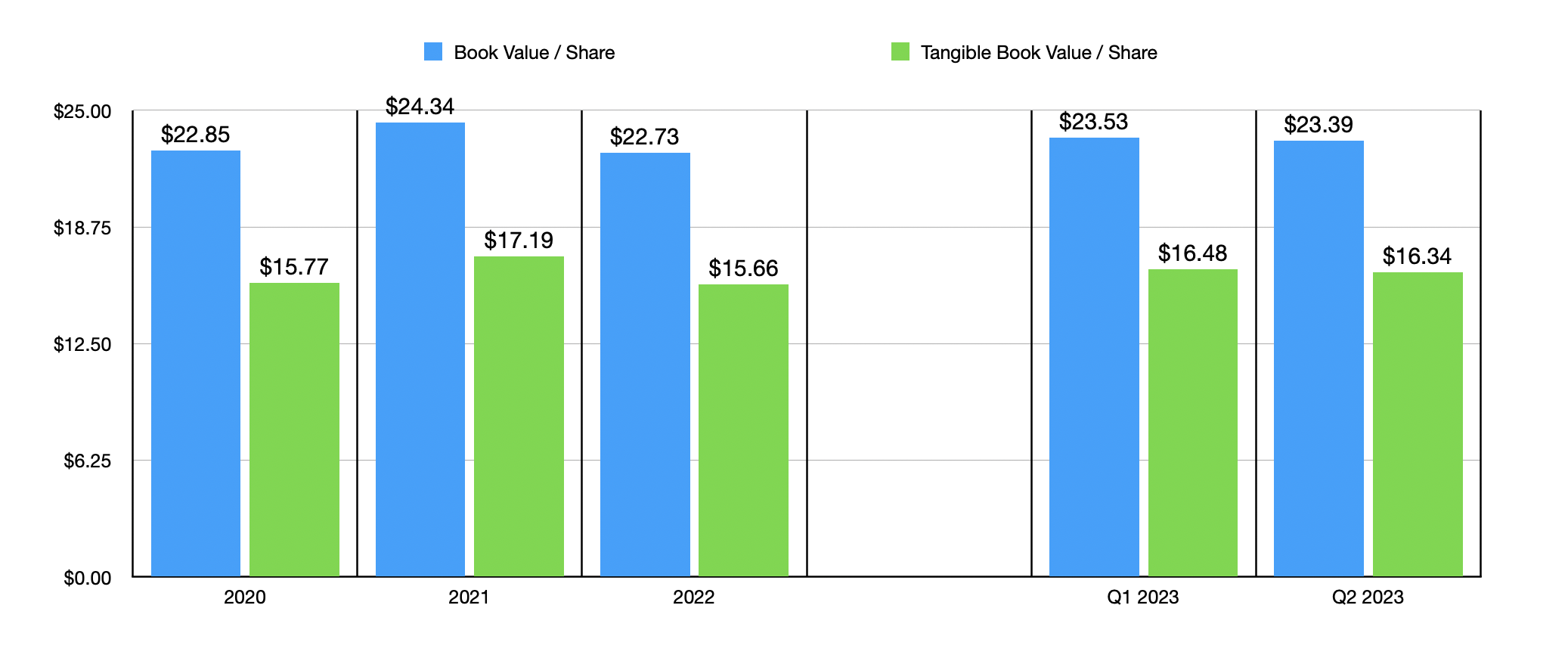

In terms of valuing the company, there are two different methods that we can use. The first would be to compare its stock price to its book value per share. As of the end of the most recent quarter, the company had a book value per share of $23.39. This was up from the $22.73 per share reported at the end of 2022. Tangible book value per share, meanwhile, has grown from $15.66 to $16.34 over that same window of time. With shares at $16.91, the company is trading at a premium over its tangible book value of only 3.5% and at a discount to its book value of 27.7%. That's quite appealing. The other way to look at the picture is through the lens of the price to earnings multiple. Using results from 2022, Heritage Financial is trading at a multiple of 7.3. While this is not the lowest that I have seen, it is definitely on the cheap side.

Takeaway

At this time, I find Heritage Financial to be an interesting company. However, I'm not ready to come out as bullish regarding it just yet. On the positive side, we have a low trading multiple, using both the price to earnings approach and the price to book value approach. Management has been successful in growing the company's loan book and leverage has remained in check. On top of this, uninsured deposit values, while higher than I would like, have been on the decline for the past few quarters. At the same time, the mix revenue and profit picture, the aforementioned high uninsured deposit exposure, and the continued drop in deposits, all makes me feel as though this is not a prime prospect to consider. Because of these factors, I've decided to rate the company a ‘hold’ for now.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!

This article was written by

Daniel is an avid and active professional investor. He runs Crude Value Insights, a value-oriented newsletter aimed at analyzing the cash flows and assessing the value of companies in the oil and gas space. His primary focus is on finding businesses that are trading at a significant discount to their intrinsic value by employing a combination of Benjamin Graham's investment philosophy and a contrarian approach to the market and the securities therein.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.