Buffett Says Buy Tangible Assets, 2 Great Picks For A Rich Retirement

Summary

- Berkshire Hathaway has a substantial stake in American utilities and infrastructure companies.

- This industry offers income stability for retirees as they experience inelastic demand through economic cycles.

- Two +7% yields for your retirement with income safety and sustainability.

- Looking for a portfolio of ideas like this one? Members of High Dividend Opportunities get exclusive access to our subscriber-only portfolios. Learn More »

Eric Francis

Co-authored with “Hidden Opportunities."

Warren Buffett is a buyer of assets that produce reliable profits through the noise that surrounds the financial markets. This goes with all his investments like Coca-Cola (KO), American Express (AXP), or Occidental Petroleum (OXY). The company should have a tangible moat, it must be able to raise prices without losing market share, and the demand for its goods and services must be strong through economic cycles.

"Our goal in both forms of ownership is to make meaningful investments in businesses with both long-lasting favorable economic characteristics and trustworthy managers. Please note particularly that we own publicly-traded stocks based on our expectations about their long-term business performance, not because we view them as vehicles for adroit purchases and sales. Charlie and I are not stock-pickers; we are business-pickers" – Warren Buffett, 2023 Berkshire Hathaway Shareholder Letter.

While stock prices move based on the emotions, perceptions, and sentiments of Mr. Market, business fundamentals don’t. However, looking at industry fundamentals, the utility industry is doing very well and successfully growing its asset base while raising prices to consumers.

Berkshire Hathaway Energy is one of the largest electric utilities in the country with 5.2 million customers and is the second largest owner of renewable energy assets and a significant investor in liquefied natural gas facilities. Most importantly, it is a conglomerate of tangible assets, churning usable cash for Berkshire Hathaway (BRK.B).

"Each company [MidAmerican Energy and BNSF] has earning power that even under terrible economic conditions will far exceed its interest requirements." – Warren Buffett.

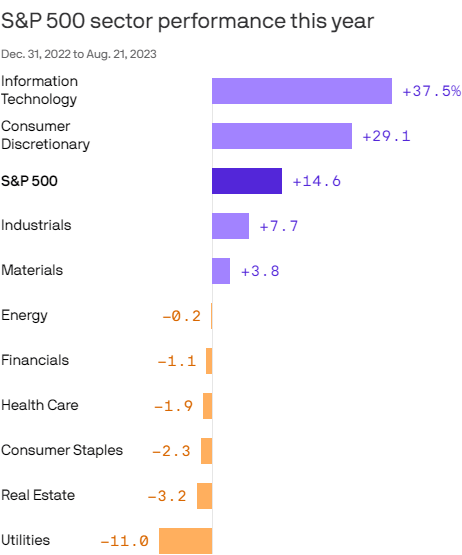

The Utility sector is currently out of favor among investors due to higher rates and uncertainty over the Fed’s economic actions. Investors have shunned this historically stable dividend-friendly sector due to the availability of risk-free alternatives for income, making it the most underperforming S&P sector YTD. Source.

FactSet

Let's examine two deeply discounted picks that pay big dividends through the profit prowess of the utility/energy infrastructure sector. Let’s dive in!

Pick #1: UTG - Yield 8.7%

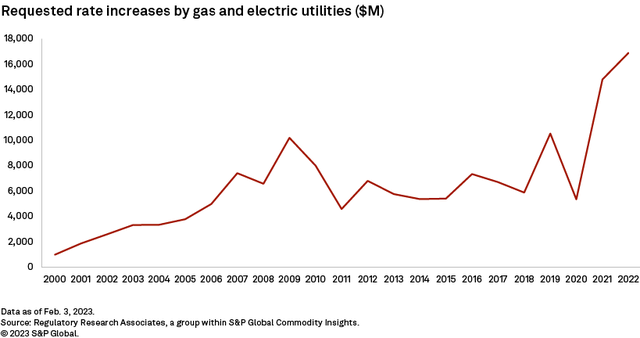

For utility companies, there is a terminology called “rate base”, which refers to the total value of its regulated assets. This is used to determine the rates the company can charge its customers for the services provided and serves as a fundamental component in cost recovery and profitability for this industry.

Thanks to the push for cleaner energy and increasing the safety and reliability of the grid, it has been a record year for requested rate increases by U.S. utility firms. Over $3 billion in rate increase requests have been filed through February 2023, positioning this sector to have a terrific year. Source.

S&P Global

Rate base increases add to the long-term value of the company’s assets, serve as an effective inflation hedge, and provide improved stability to the income stream for investors.

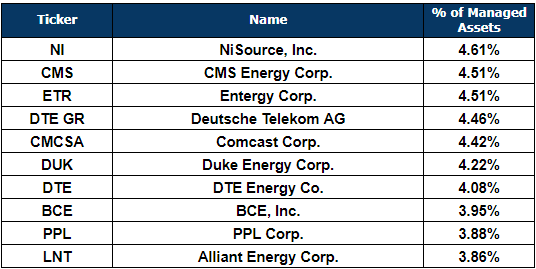

We like the attractively discounted valuation of this asset-rich and inelastic industry and seek diversified exposure with big yields. Reaves Utility Income Trust (UTG) is a CEF (Closed-End Fund) that has a track record of providing both since its inception in 2004. UTG is actively managed and holds 44 companies at this time, primarily U.S. and Canadian utility and telecom companies.

Author's Calculations

Looking at UTG’s top holdings, we see names of regulated utility firms that have requested/received approvals for massive rate base hikes. Such rate increases position the firms well for sustained dividend growth and asset enhancement over the long term, directly benefiting shareholders.

This CEF pays $0.19/share every month, an 8.7% annualized yield at current prices. UTG’s active management helps it capture low prices from undervalued yet fundamentally strong names. Markets rarely move in one direction, and the CEF’s active balancing allows for the realization of healthy gains, which can sustainably fuel our distributions over the long term.

In its semi-annual report, UTG reported $146.9 million (almost $1.97/share) in unrealized gains as of April 2023. Being a CEF, UTG must eventually realize and distribute these gains. In addition to this, UTG collects $1.30/share annually from dividends, which is sustainably recurring from its portfolio holdings. The sum is adequate to support UTG’s annual distribution for ~1.5 years, making its current yield sustainable.

Pick #2: AM - Yield 7.7%

Antero Midstream Corporation (AM) is a midstream energy company with a wide network of gathering pipelines, compression facilities, processing and fractionation plants, and water handling systems in the Appalachian Basin – the Marcellus and Utica Shales. Substantially all of AM’s revenues are derived by providing midstream services to Antero Resources (AR), which also happens to be a significant shareholder, establishing a symbiotic relationship between the two entities.

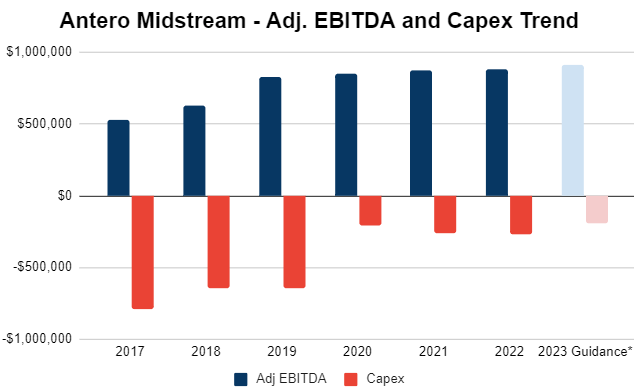

The biggest benefit of midstream companies is the insensitivity of their operations to commodity prices through their steady fee-based revenues. Despite natural gas trading at record low prices, AM reported a 10% YoY increase in Adj. EBITDA during Q2 2023. Along with this, the company achieved a 31% YoY decrease in operating expenses.

Author's Calculations

Growing EBITDA and declining capital expenditure is a sight for sore eyes in this inflation-ridden high interest rate economy that is staring down fearfully into the recession barrel. AM’s profitability is rising, with the company generating $139 million of FCF (Free Cash Flow) before dividends and $31 million FCF after dividends. AM currently pays $0.225/quarter, a 7.7% qualified annualized yield. With growing FCF after dividend payments, the next raise is getting closer.

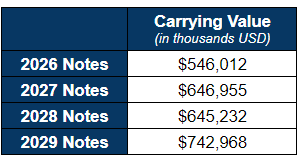

AM is aggressively paying down debt per its original commitment to shareholders. During 1H 2023, the company reduced its long-term debt by $56 million and brought its leverage down to 3.5x (from 3.7x). AM has senior unsecured notes maturing from 2026 onward, which gives them adequate flexibility with their near-term cash flows.

Author’s Calculations

Management has reiterated their expectation to reduce debt to 3.0x adj. EBITDA by 2024, which increases the likelihood of dividend increases in the near term.

AM's earnings are on an upward trajectory, complemented by a strategic reduction in both capital and interest expenses. This can be attributed to the prudent management navigating the broader dynamics of the energy sector during its darkest days. As a result of these actions, the previously noted 7.4% yield has not only gained in stability but also reaffirmed its strong potential for sustained long-term income expansion.

Conclusion

Warren Buffett has Berkshire Hathaway Energy as a dedicated platform to hold and invest in utility and other asset-rich infrastructure companies. This conglomerate contributes 10% of revenues and earnings at Berkshire and is projected to contribute in the mid-teens percentage in five years.

Berkshire Hathaway does not pay dividends to its shareholders, but the mega-cap corporation directly collects the profits of its energy conglomerate. Since I seek income from my investments (much like what Berkshire achieves from its portfolio), I choose to invest in different ways, yet learning and adopting Mr. Buffett’s investment techniques.

UTG and AM present attractively priced securities with up to 8.7% yields. With such picks, you can enjoy the benefits of inflation resistance, inelastic demand, and strong pricing power of the utility/midstream industry, akin to Berkshire's winning formula.

If you want full access to our Model Portfolio and our current Top Picks, join us at High Dividend Opportunities for a 2-week free trial.

We are the largest income investor and retiree community on Seeking Alpha with +6000 members actively working together to make amazing retirements happen. With over 45 picks and a +9% overall yield, you can supercharge your retirement portfolio right away.

We are offering a limited-time sale for 28% off your first year. Get started!

Start Your 2-Week Free Trial Today!

This article was written by

I am a former Investment and Commercial Banker with over 35 years of experience in the field. I have been advising both individuals and institutional clients on high-yield investment strategies since 1991. I am the lead analyst at High Dividend Opportunities, the #1 service on Seeking Alpha for 6 years running.

Our unique Income Method fuels our portfolio and generates yields of +9% alongside steady capital gains. We have generated 16% average annual returns for our 7,500+ members, so they see their portfolios grow even while living off of their income! Join us for a 2-week free trial and get access to our model portfolio targeting 9-10% overall yield. Our motto is: No one needs to invest alone!

In addition to being a former Certified Public Accountant ("CPA") from the State of Arizona (License # 8693-E), I hold a BS Degree from Indiana University, Bloomington, and a Masters degree from Thunderbird School of Global Management (Arizona). I currently serve as a CEO of Aiko Capital Ltd, an investment research company incorporated in the UK. My Research and Articles have been featured on Forbes, Yahoo Finance, TheStreet, Investing.com, ETFdailynews, NASDAQ.Com, FXEmpire, and of course, on Seeking Alpha. Follow me on this page to get alerts whenever I publish new articles.

The service is supported by a large team of seasoned income authors who specialize in all sub-sectors of the high-yield space to bring you the best available opportunities. By having 6 experts on your side, each of whom invest in our own recommendations, you can count on the best advice. (We wouldn't follow it ourselves if we didn't truly believe it!)

In addition to myself, our experts include:

3) Philip Mause

4) PendragonY

We cover all aspects and sectors in the high yield space including dividend stocks, CEFs, baby bonds, preferreds, REITs, and more! To learn more about “High Dividend Opportunities” and see if you qualify for a free trial, please check out our landing page:

High Dividend Opportunities ('HDO') is a service by Aiko Capital Ltd, a limited company - All rights are reserved.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of UTG, AM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Treading Softly, Beyond Saving, PendragonY, and Hidden Opportunities all are supporting contributors for High Dividend Opportunities. Any recommendation posted in this article is not indefinite. We closely monitor all of our positions. We issue Buy and Sell alerts on our recommendations, which are exclusive to our members.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (3)