AMC Entertainment: Adam Aron, We Have A Problem

Summary

- AMC remains a risky investment, due to its lack of sustainable profitability and reliance on share dilution/ retail investors.

- The latter has triggered much volatility, thanks to the reverse stock split and the authority approval to increase the overall number of Class A shares to 550M.

- On the one hand, things have somewhat improved in FQ2'23, with AMC's prospects likely to lift moving forward as H2'23 brings forth a promising blockbuster line up.

- On the other hand, we concur with the management's disclaimer that the AMC investment thesis comes with the risk of losing all or a substantial portion of the investment.

imaginima

The AMC Investment Thesis Remains Shaky

We previously covered AMC Entertainment Holdings (NYSE:AMC) in July 2023, discussing its meme stock status, thanks to its over reliance on retail investors and share dilution during the heights of the pandemic.

Since it had remained largely unprofitable, the company had naturally proposed another round of capital raise, with the subsequent APE court battle triggering further uncertainty in its short-term prospects.

Then again, while AMC has underperformed post-reopening, it appears that things may be quickly reversing soon.

This is thanks to the solid performance of the early summer movies in Q2'23, namely Comcast's (CMCSA) The Super Mario Bros. Movie, Disney's (DIS) Guardians of the Galaxy Vol. 3, and The Little Mermaid.

As a result of the blockbuster line up, AMC has been able to report an exemplary FQ2'23 earnings call, with revenues of $1.34B (+41.2% QoQ/ +15.6% YoY) and gross margins of 19.7% (+11.9% points QoQ/ +5.1 YoY).

The improvement is drastic indeed, nearing the pre-pandemic FY2019 margins of 16.8% (-2 points YoY). Thanks to its cost optimizations, the theatre company is also able to report positive operating margins of 6.3% (+17.7 points QoQ/ +7.7 YoY).

Then again, much of the positive developments have been negated by AMC's growing annualized interest expense of $372M (+1.5% QoQ/ +15.5% YoY) in the latest quarter, thanks to the elevated long-term debts of $4.79B (-1.4% QoQ/ -10.4% YoY).

The growing interest expense is mostly attributed to the Term Loan due 2026 with a variable interest rate of 8.218% as of June 2023 (+0.534 points QoQ/ +4.019 YoY).

AMC investors must also note that $505.6M of its debts will be due in 2023, with another $5M due in 2024 and $98.3M in 2025, triggering further headwinds to its liquidity worsened by the elevated interest rate environment.

Its near-term prospects remain highly uncertain as well, with its cash/ equivalents deteriorating to $435.3M (-12.1% QoQ/ -54.9% YoY) in the latest quarter and Free Cash Flow generation still negative at -$299.3M YTD (+35.5% YoY).

Therefore, it is unsurprising that once the reverse stock split is completed, the AMC management has decided to raise more capital by selling 40M shares.

This may potentially yield up to $545.6M in additional liquidity, based on the stock price of $13.64 on September 05, 2023, or $344.8M based on $8.62 on September 06, 2023.

Then again, the sum is barely enough to make any difference to its current debt balance, especially due to the massive pessimism embedded in its stock prices.

At the time of writing, AMC has drastically lost -81% of its value since the FQ2'23 earnings call in early August 2023. If the stock continues to retrace, the company may have a reduced chance of raising any meaningful capital, further jeopardizing its near-term survival.

On the other hand, depending on the timing and volume of its capital raise, the management has also obtained approval to increase its total number of Class A shares to 550M, with a forward balance of 351.62M after the 40M is exercised.

Based on its share price of $8.62 at the time of writing, we may see AMC raise another $3.03B in liquidity, effectively wiping out most of its debts and potentially improving its profitability as interest expenses moderate.

As a result, strong handed investors may want to maintain their positions for a little longer, since we do not see a point in realizing massive losses now, since the highly speculative reversal may potentially take any "bankruptcy risks off the table."

So, Is AMC Stock A Buy, Sell, or Hold?

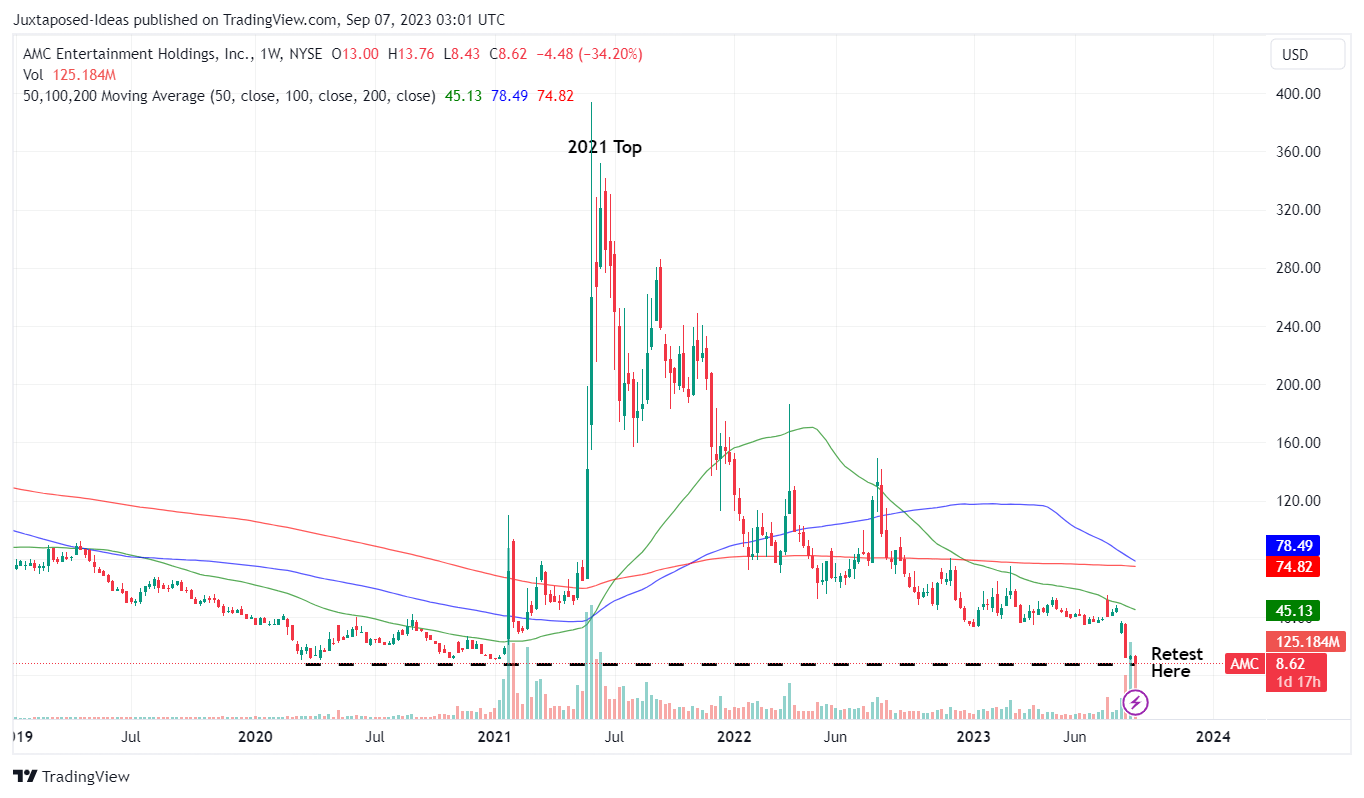

AMC 5Y Stock Price

Trading View

For now, the AMC stock has already plunged by -76% since our previous article, reaching the previous critical support levels during the hyper-pandemic period in 2020, in-line with our hypothesis.

While it remains to be seen if these support levels may hold, we are cautiously optimistic that the theatre company may report excellent H2'23 top and bottom lines.

This is attributed to Paramount's (PARA) Mission: Impossible – Dead Reckoning Part One, Warner Bros. Discovery's (WBD) Barbie, CMCSA's Oppenheimer in Q3'23, and Taylor Swift's Eras live tour in Q4'23.

With the APE legal overhang also cleared, we believe that AMC's prospects may look somewhat brighter ahead, for so long that it is able to maintain sufficient cash flow over the next few quarters.

However, investors must also note that if the stock's critical support level is breached, there is no telling how low the floor may be, attributed to the elevated short interest of 9.90% at the time of writing.

As a result of the potential volatility and capital losses, it is unsurprising that we concur with the management's disclaimer in the recent FQ2'23 10Q, resulting in our Hold (Neutral) rating on the AMC stock:

We believe that the recent volatility and our current market prices reflect market and trading dynamics unrelated to our underlying business, or macro or industry fundamentals, and we do not know how long these dynamics will last.

Under the circumstances, we caution you against investing in our Common Stock and AMC Preferred Equity Units, unless you are prepared to incur the risk of losing all or a substantial portion of your investment. (Seeking Alpha)

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The analysis is provided exclusively for informational purposes and should not be considered professional investment advice. Before investing, please conduct personal in-depth research and utmost due diligence, as there are many risks associated with the trade, including capital loss.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (7)

Damned for shareholders in either case even if good for the company