Consolidated Water: Hidden Gem But Fully Valued Right Now

Summary

- Consolidated Water is a water solutions company that has seen impressive stock growth in recent months.

- The company recently increased its dividend for the first time since 2018, indicating confidence in its future prospects.

- CWCO's strong Q2 results and recent analyst upgrade have contributed to its uptrend, and it is trading at a reasonable standalone valuation.

- I suggest waiting for a pullback before initiating a position for the long term.

BlackJack3D

"Watching paint dry" is often used to describe a boring activity. In the usually exciting world of investing, the equivalent might as well be "investing in utilities". But boring can also be effective, as proven by companies like Southern Company (SO) with its decades-long dividend growth history. While electric and trash utility companies have their stalwarts in the world of investing with the likes of Southern Company and Waste Management, Inc. (WM), it feels like Water companies do not get their dues, just like Water, despite arguably being the most precious commodity.

Until I started working on this article, I could name only two Water Utilities companies, American Water Works Company, Inc. (AWK) and The York Water Company (YORW). As a follower of dividend-paying stocks, this surprised me a little because according to Seeking Alpha data, all but one of the 12 companies listed under the Water Utilities industry pay a dividend, including the focus of this article, Consolidated Water Co. Ltd. (NASDAQ:CWCO).

About Consolidated Water

As the name suggests, Consolidated Water is a Water Solutions company that deals with seawater desalination plants and water distribution systems. In the company's own words, Consolidated Water is "an international water solutions company, supplying potable water, treating water for reuse, and manufacturing and providing water-related products and services to customers in the Cayman Islands, The Bahamas, the United States, and the British Virgin Islands."

As the company proudly mentions on its website, Consolidated Water has been operating for the last 50 years and became a publicly listed entity in 1995. The company reported diluted EPS of 54 cents per share on $94 million in revenue in 2022. The stock has been on an uptrend recently as it is up:

- 52% in the last month

- 92% in the last 6 months

- 103% YTD

As impressive as that sounds, in the last 10 years, the stock is up just 130%, meaning at the beginning of 2023, the stock was more or less at the same price it was trading at 10 years ago. Is the recent uptrend here to stay, potentially taking the stock to new highs or is the stock destined to be stuck in a long-term range like it did between 2008 and 2023 before breaking the $20 barrier? No one has a crystal ball, but I am presenting a few reasons below as to why I believe the stock's breakout is likely to last at least in the short to medium term. Let us get into the details.

CWCO Stock Chart (Seekingalpha.com)

Dividend Increase

The safest dividend is the one that has just been raised. Consolidated Water recently increased its dividend for the first time since 2018 as Seeking Alpha has reported here. Clearly, this is not your classic dividend growth company/stock and that brings up the question, why this increase now? Can the company afford it? Let's find out.

- Total shares outstanding: 15.74 million

- New quarterly dividend per share: 9.5 cents

- Quarterly Free Cash Flow [FCF] needed on average to cover dividends: $1.49 million (that is, 15.74 million shares times 9.5 cents/share).

- CWCO's average quarterly FCF over the last 5 years: $2.473 million

- Payout ratio using 5-year average quarterly FCF: 60% (that is, $1.49 million divided by $2.473)

- Payout ratio using forward EPS of $1.48: 25% (that is, 38 cents per share in annual dividend divided by forward EPS of $1.48)

That likely answers why the company raised its dividend. The company can afford it and is likely seeing a bright future for itself as described below.

Strong Q2 and Recent Analyst Upgrade

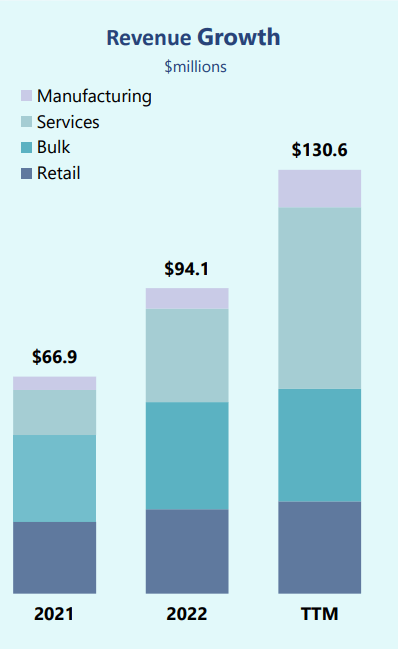

The company recently landed an analyst upgrade as well after its Q2 results exceeded expectations. EPS beat by more than 100% while revenue of $44 million beat by nearly 45%. Keep in mind the company's 2022 FY revenue was $94 million and it nearly reported 50% of that in one quarter. No wonder the stock has been on an uptrend since, especially when you consider that revenue has basically doubled since 2021.

Revenue Growth (ir.cwco.com)

Valuation and SA Quant Ratings

Despite the 100% YTD, CWCO stock is trading at a reasonable forward multiple of 18. However, when you factor in the expected earnings growth rate of 8%/yr, the valuation appears just a little rich given the industry we are talking about here. This is confirmed by Seeking Alpha's valuation scale that ranks CWCO's valuation as "F" while the competitors are either rated C or D.

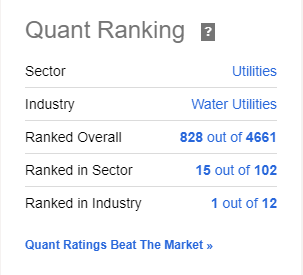

Overall though, Seeking Alpha's quant ratings have ranked CWCO stock as #1 in its industry as the stock's profitability, growth and momentum tilt things in its favor.

CWCO Quant (Seekingalpha.com)

A Precious But Wasted Commodity

- The best thing Consolidated Water has got going in its favor is that it deals with a precious commodity that is supposed to be readily available but is scarce (from global perspective) and yet is being wasted. According to the Environment Protection Agency [EPA]:

- The average American family uses 300 gallons of water every day

- The average American family wastes up to 180 gallons of water each week

- The wastage can be cut drastically by following simple steps like running dishwasher only when it is full but this has not been followed at large by the general population. This means it is ingrained in people's day-to-day habits to waste water, as sad as that sounds.

- Increased infrastructure spending is another catalyst for the stock in the medium term as covered in this Seeking Alpha article.

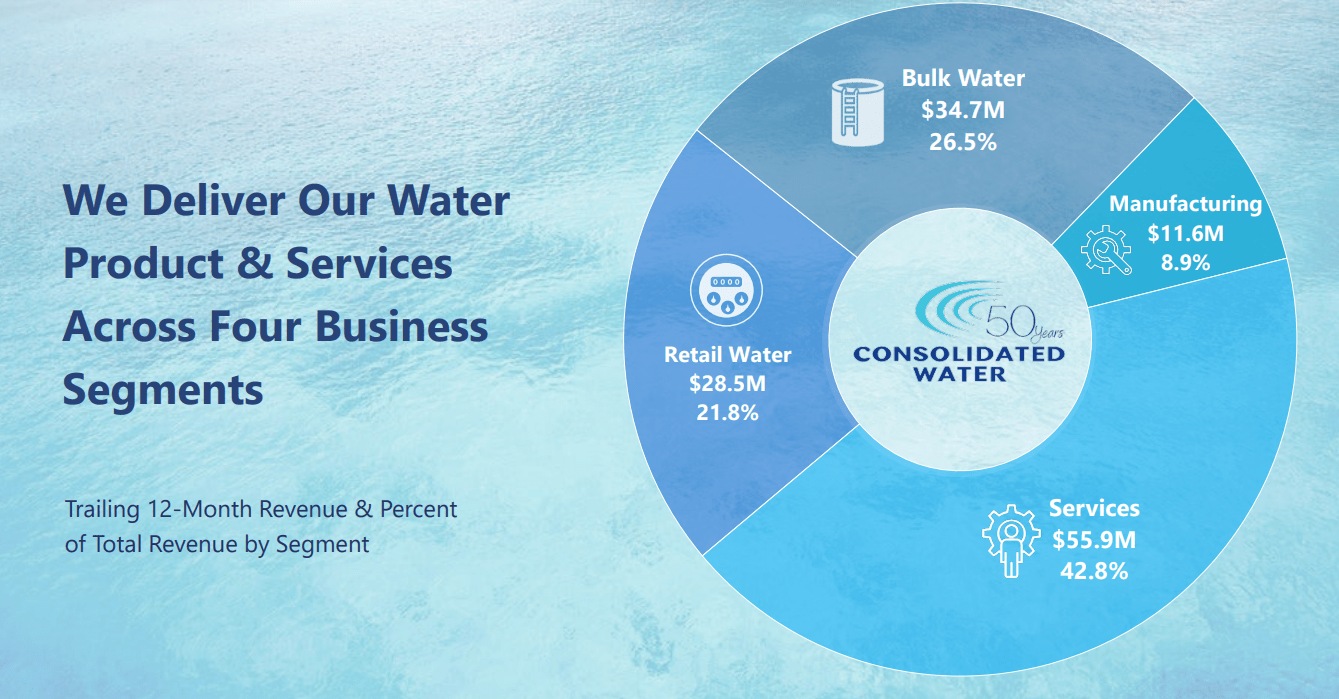

- Consolidated Water's revenue is split fairly well across its 4 business segments. Services is the largest at nearly 43% but the other three segments are providing their worth as well.

Revenue Split (ir.cwco.com)

Risks and Conclusion

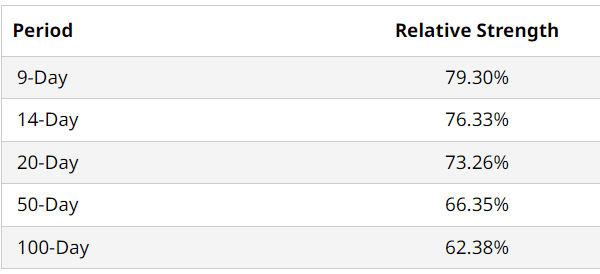

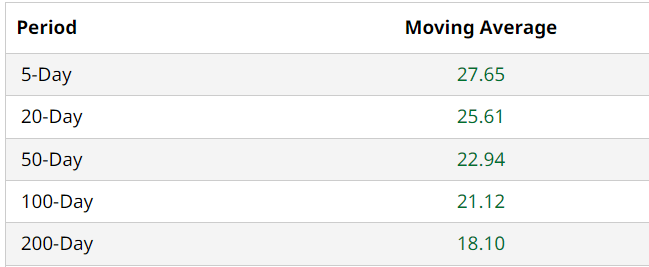

The medium-term risk to the stock is its run-up in the last few months, which has almost pushed the stock into overbought territory. While momentum is great, sometimes stocks tend to go up too far, too fast with no stops in between. CWCO's 200-day moving average is nearly 40% below the current trading price and that means the stock may take a while to find support should things turn south.

CWCO RSI (barchart.com) CWCO Moving Avgs (barchart.com)

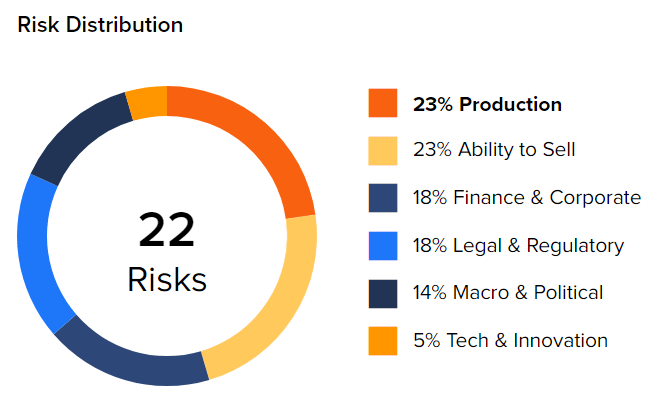

From a longer-term perspective, CWCO is still one of the smallest players in the market and is likely to run into production and scale issues than larger companies. Geopolitical risks apply to the entire industry given the nature of the business but are more applicable to CWCO given its smaller size and reach.

CWCO Risks (tipranks.com)

Overall, while I expect the stock's recent strong price action to continue for a little while, I rate the stock a Hold for now given its recent run-up but encourage investors to keep an eye out for pullbacks. When you consider the 40% gap predicted between global water supply and demand by 2030, Consolidated Water's long-term market opportunity stands out.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.