NIO Is Not The Next Tesla (Rating Downgrade)

Summary

- NIO faces challenges in the near and intermediate term due to a sluggish Chinese economy, rising costs, lower margins, increased competition, and Tesla's dominance.

- NIO's Q2 earnings missed consensus estimates, with a decrease in revenue, deliveries, and vehicle sales, and a significant net loss.

- Tesla's lower prices and economies of scale advantage make it difficult for NIO to effectively compete, raising concerns about NIO's long-term profitability.

Drew Angerer/Getty Images News

NIO Inc. (NYSE:NIO) is an exciting pure EV company out of China. I've been bullish on NIO due to its innovative vehicles, growth prospects, and future profitability potential. Moreover, due to its higher-end EV market position, production capacity, and other factors, I've often said that NIO is the closest pure EV competitor that Tesla (TSLA) has.

However, despite NIO's considerable long-term growth and profitability potential, the company may face challenges in the near and intermediate term. NIO's problems could persist for several reasons, including a sluggish Chinese economy, rising costs, lower margins, increased competition, and other variables. Nevertheless, a primary concern for NIO is Tesla. Tesla has illustrated that it can drop vehicle prices while maintaining high profitability, taking market share from NIO and other EV manufacturers.

Unfortunately for NIO, it cannot drop prices low enough to effectively compete with Tesla because of Tesla's economies of scale advantage and other factors. Therefore, NIO could continue struggling as we move forward. Moreover, NIO's recent earnings announcement showed the company missing top and bottom-line consensus estimates, putting the company's outlook into question. Additionally, NIO's margins continue deteriorating, and uncertainty surrounds its stock. Due to the increased transparency, NIO's risk/reward ratio has fallen, and I'm taking down my buy rating on its stock, transitioning to a hold instead.

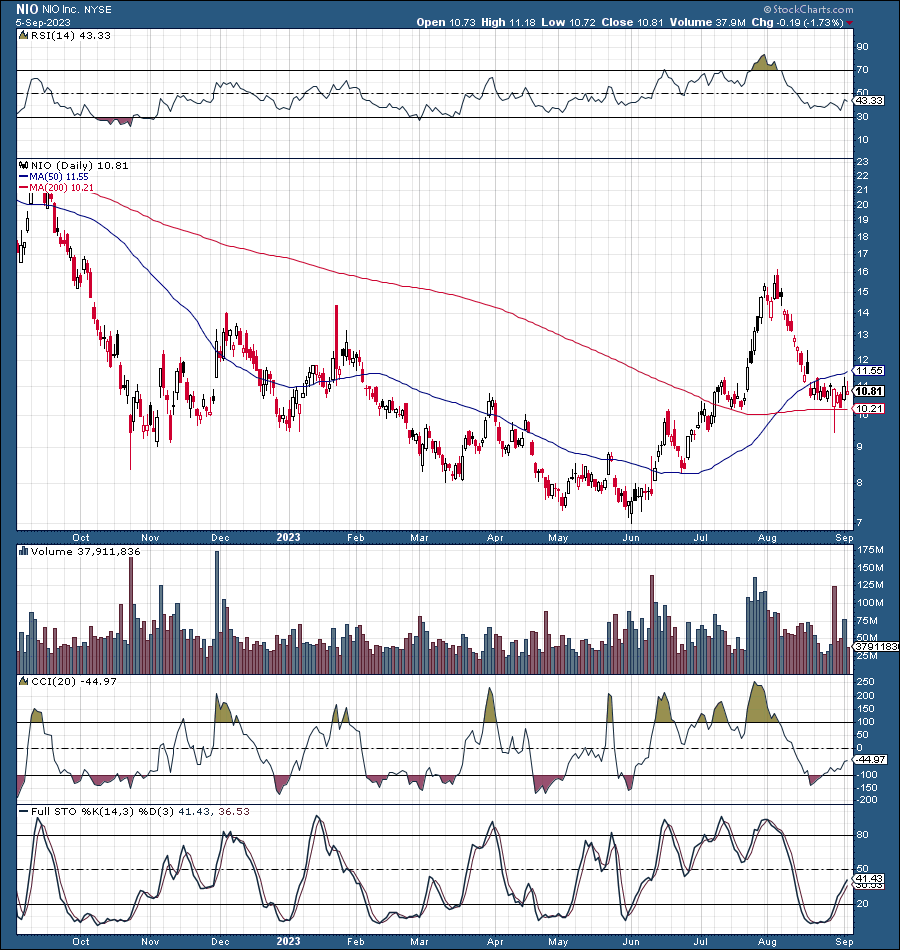

Technically - Could Rally In The Near Term

NIO (StockCharts.com)

I won't deny it. Technically, NIO's chart appears bullish in the near term here. The stock likely put in a long-term bottom around the $7 level, staging a robust rally to around $16 before dropping back to the $10 range. We recently witnessed the 50-day MA move above the 200-day MA, a bullish technical signal. We also see a possible basing platform around the $10 support, implying we may see a rally in the near term. Nevertheless, this stock remains highly uncertain for the long term despite the near-term positives.

NIO's Missing Numbers - Puts Outlook in Question

NIO recently reported Q2 Non-GAAP EPADS of -$0.45, missing the four-cent consensus number. Moreover, it reported revenue of $1.21B, a $60M miss, and a 14.8% YoY decrease. Q2 deliveries came in at 23,520 vehicles, a 6.1% YoY decrease. Q2 vehicle sales came in at about $991M, representing a 25% YoY decline. Vehicle margin was only 6.2%, a staggering drop from the 16.7% in the same quarter last year.

NIO's Staggering $828 Million Loss

Additionally, NIO's gross margin crashed to just 1% from 13% in the same quarter last year. NIO's Q2 net loss widened to more than 6 billion Yuan, equating to a staggering quarterly loss of $828 million. Unfortunately, this massive loss isn't new for the company, as NIO's TTM loss is close to $3 billion. NIO produced about $6 billion in revenues during the same time frame. Thus, the $64,000 question is, when will NIO become profitable?

The answer is no time soon. Moreover, a capital raise could come shortly. Therefore, there's likely dilution in NIO's future, implying the stock could fall or stay range bound longer-term. Moreover, I wonder if NIO can effectively compete with Tesla in the long run.

NIO's Massive Tesla Problem

Tesla dominates China's higher-end EV segment. Tesla recorded more than 84,000 unit sales last month (August). This sales increase represents a 31% YoY surge for Tesla, bringing its YTD vehicles sold in China to about 625,000. NIO delivered 19,329 in August, bringing its YTD vehicle sales count to 94,352. However, management is guiding to sales of 15-17K in September. Therefore, we're seeing NIO's order book slowing down, and NIO needs many more sales (200-300K annually) to have a chance to be profitable. Tesla's position is so prominent in China that NIO may find it challenging to compete effectively in the long run.

What Would You Buy - Tesla or NIO?

NIO's popular ET5 sedan starts at about $46,100, and the price can climb into the $50-$60K range quickly once options are added. NIO's EC6 (Model Y competitor) starts at about $52,400, and the price can surge into the $60-$70K range with options. In contrast, the Model Y starts at only $41,000 in China and has (arguably) more advanced technologies and better engineering. Due to Tesla's remarkable ability to control prices, its mass-market vehicles are far more affordable than its prime competitor in China. Therefore, NIO's recent sales improvement may be temporary, and Tesla could continue taking NIO's market share as we advance. NIO can have a niche place in the EV market, but whether it can become mainstream and profitable remains to be seen. Therefore, I need more certainty as an investor here. Until then, I would rather own Tesla's stock instead.

NIO: Is It Worth The Risk?

NIO is an increased-risk investment because it is a Chinese company. However, NIO is even riskier because it's a highly unprofitable Chinese company. There is the added risk of unrelenting competition from Tesla and other profitable higher-end EV automakers. Moreover, some market participants have raised questions regarding NIO's accounting practices, pointing to a "Philidor" like entity (Wuhan Weineng) inflating NIO's revenues and profitability in recent years. Therefore, we have an additional risk of accounting irregularities with NIO. As an investor, why do I need to take such risks? To see NIO succeed? The company may grow in the long run, and its share price could go much higher in the coming years. Nevertheless, there is also an inflated risk of sideways price action and failure, which makes NIO a less attractive investment long-term. Therefore, I've reduced my buy rating to hold, recently selling my NIO shares following the troubling Q2 earnings announcement.

Are You Getting The Returns You Want?

- Invest alongside the Financial Prophet's All-Weather Portfolio (2022 17% return), and achieve optimal results in any market.

- Our Daily Prophet Report provides crucial information before the opening bell rings each morning.

- Implement our Covered Call Dividend Plan and earn an extra 40-60% on some of your investments.

All-Weather Portfolio vs. The S&P 500

Don't Wait! Unlock Your Own Financial Prophet!

Take advantage of the 2-week free trial and receive this limited-time 20% discount with your subscription. Sign up now, and start beating the market for less than $1 a day!

This article was written by

Hi, I'm Victor! It all goes back to looking at stock quotes in the old Wall St. Journal when I was a kid. What do these numbers mean, I thought? Fortunately, my uncle was a successful commodities trader on the NYMEX, and I got him to teach me how to invest. I bought my first actual stock in a company when I was 20, and the rest, as they say, is history. Over the years, some of my top investments include Apple, Tesla, Amazon, Netflix, Facebook, Google, Microsoft, Nike, JPMorgan, Bitcoin, and others.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I am long a diversified portfolio with hedges.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.