Oppenheimer: An Overvalued Asset Manager With Net Loss In Q2, Downgraded To Hold

Summary

- Oppenheimer Holdings stock downgraded to Neutral / Hold since my Buy rating in late April. Today's rating agrees with analyst consensus on SA.

- Positives: capital strength, share price vs. moving average, book value vs. sector average.

- Headwinds: dividend yield uncompetitive, earnings net loss for Q2.

Georgijevic

Research Brief

In today's analysis, I will be covering Oppenheimer Holdings (NYSE:OPY), which is in the financials sector, and investment banking /brokerage subsector.

Since my last rating in late April where I rated it a buy, the share price climbed 3.14%. Incidentally, that was my very first research analysis for Seeking Alpha, and to mark a successful & continual 4 months on the platform I will be revisiting this stock today to see if my prior rating stands or not, for this often under-covered equity.

Oppenheimer - price since last rating (Seeking Alpha)

Since my last analysis, the company had its most recent quarterly earnings result on July 28th, and that will be the reference data used in some parts of today's analysis.

For readers less familiar with this company, some relevant points to mention from their quarterly earnings presentation are: trades on NYSE, market cap of $444MM, $41B in "AUM" and $113B in "AUA", 92 branches across US. It describes its business as providing financial services and advice to high net worth investors, individuals, businesses and institutions.

A key peer of this company is Piper Sandler (PIPR), and known competitors are Raymond James Financial (RJF) and Charles Schwab (SCHW).

Research Methodology

To determine a holistic rating for this stock of buy, sell, or hold, I split my research into the following 5 categories: dividends, valuation, share price, earnings growth, capital strength.

Each category has equal weight. If I recommend the stock in at least 4 of 5 categories, it gets a buy rating. 3 out of 5 will get a hold rating, and below that earns a sell rating.

This process is aimed to simplify things, focus on financial fundamentals, and to analyze an equity from multiple angles.

Dividends

In this category, I will discuss whether this stock should be recommended for dividend-income investors, by analyzing official dividend data from Seeking Alpha.

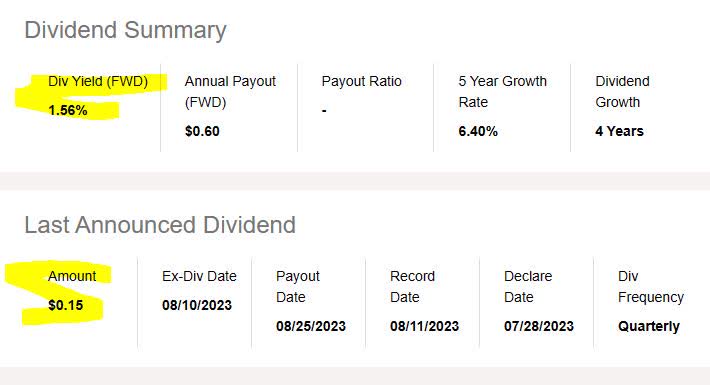

As of the writing of this article, the forward dividend yield is 1.56%, with a payout of $0.15 per share on a quarterly basis. No ex dates are coming up soon.

Oppenheimer - dividend yield (Seeking Alpha)

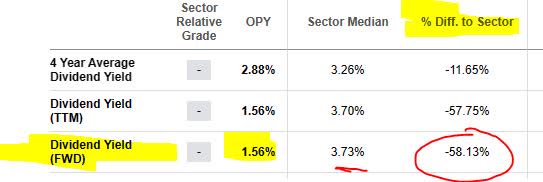

In comparing the yield vs the sector average, this stock is below the sector average by around 58%. I think that could be a moderate negative to think about for the dividend investor in terms of this stock vs the overall sector it is in, although yield is not the only component to dividends and should be considered along other factors as well.

Oppenheimer - dividend yield vs sector (Seeking Alpha)

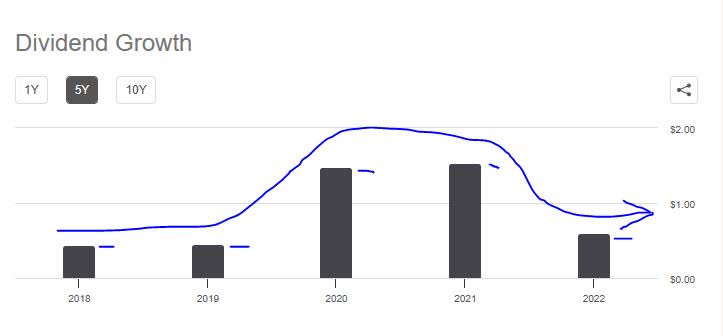

Important to mention, for example, in comparing the current dividend to the last 5 years, this company has been on a lopsided trend when it comes to dividend growth, with a negative growth more recently. I think this is also a modest negative for dividend investors as it points to a weakening of the capacity of this company to return capital back to shareholders, though not necessarily a guarantee of future dividends or lack thereof.

Oppenheimer - 5 year dividend growth (Seeking Alpha )

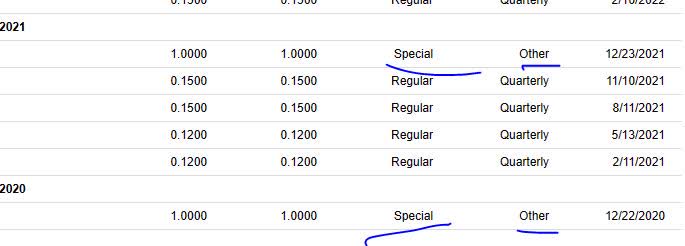

Relevant to this is that in 2020 and 2021 a "special" dividend was paid out along with regular quarterly dividends, which was a plus, however in 2022 and 2023 it was not.

Oppenheimer - special dividends (Seeking Alpha)

Based on the overall evidence found, I would not recommend this stock in the category of dividends. In the section on share price later on, however, I will show how annual dividend income can play a role in putting together my investment idea for this stock.

Valuation

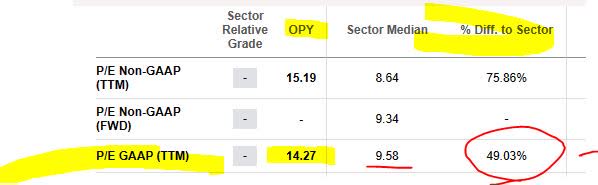

In this category, I will discuss whether this stock presents an attractive valuation for my readers. To analyze this, I will use today's valuation data from Seeking Alpha and specifically the trailing-twelve-month P/E ratio and also the TTM P/B ratio.

This stock's trailing P/E ratio is 14.27, which is 49% above the sector average that is hovering closer to 9.6x earnings. I am looking for a valuation in a range that is up to 30% below the average or in line with it and up to 5% above average. I am comfortable with a price up to 10x earnings.

In this case, in my opinion this stock is not reasonably valued on price-to-earnings but significantly overvalued. I don't see the justification when the sector is closer to 10x earnings. However, I welcome your comments on this valuation topic as always, to hear your perspective! My goal is to make this an interactive but productive discussion.

Oppenheimer - P/E ratio (Seeking Alpha)

This stock's trailing P/B ratio is 0.53, which is 49% below the sector average that is hovering around 1.6x book value. My benchmark is a valuation in a range that is up to 30% to 50% below the average or in line with it and up to 5% to 10% above the average. In this case, this stock is reasonably undervalued I think.

Oppenheimer - P/B ratio (Seeking Alpha)

This offsets the overvaluation on price to earnings, I think.

Since this stock is reasonably valued on one of the two ratios, I would therefore recommend it in the category of valuation, based on the evidence researched.

Share Price

In this category, I will decide if the current share price presents a value buying opportunity or not based on a pre-defined investing idea.

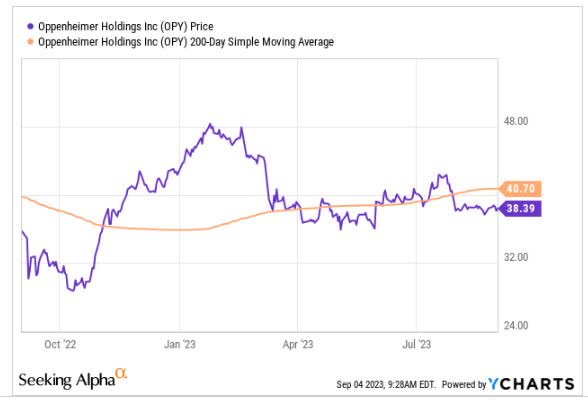

First, I pulled the most recent YChart as of this article writing. It shows a share price of $38.39 and compares it to its 200-day simple moving average “SMA” of $40.70, tracked over the last year. *Note: this chart below is not real-time so please be aware of the day/time in the chart, as market prices can fluctuate widely during a trading day.

Oppenheimer - price chart (yCharts)

To simulate my investing idea: I buy 10 shares at current share price, hold 1 year to earn a full year of dividend income, then sell in Aug. 2024 to achieve capital gains. A goal of +10% return on capital is my target.

At the same time, I established a risk tolerance to anticipate capital loss as well, so a negative -10% return is also tested. The following spreadsheet describes this idea:

Oppenheimer - investing idea (author analysis)

In the above test, the first sell price is +10% above the current 200-day SMA, and the 2nd price is -10% below the current SMA.

The first scenario exceeded my goal for return on capital as it achieves an 18.18% return after a year, and the 2nd sell scenario stayed within my risk tolerance for negative return since it actually achieved a negative return of -3.02%. Note that the potential capital loss is offset by the dividend income.

Because the two trading simulations met my profit goal and remained within risk tolerance, I would recommend the current share price as a buying opportunity, considering it priced just right.

This investing idea, however, may not fit all investors' portfolio goals or risk tolerance, and should only be considered an oversimplified way to think about this stock as a long-term investment and in terms of potential gains as well as potential losses that could occur.

Also, though I don't get into tax topics here, note that two potential tax events could occur in the above scenario: capital gains and dividend income.

Earnings Growth

In this category, I will analyze the earnings growth trend for this company over the last year, using data from the income statement on Seeking Alpha as well as the most recent company quarterly earnings release, presentation and commentary.

First, we can see that the current rate environment of the last year has favored this firm, with net interest income showing YoY gains, which I think is one positive sign.

Oppenheimer - net interest income YoY (Seeking Alpha)

Also another positive, is the YoY revenue growth as well, and a general upward trend in revenue since the same quarter a year prior.

Oppenheimer - revenue YoY growth (Seeking Alpha)

Unfortunately, I cannot be so positive when it comes to this firm's bottom line, with net income showing a further YoY drop into loss territory. In fact, this is the first firm I have covered this year that has shown a negative in quarterly earnings.

Oppenheimer - net income YoY growth (Seeking Alpha)

When trying to make sense of what could have caused this loss, I turned to the earnings commentary from CEO Albert Lowenthal, who stated:

The Company’s overall results were adversely impacted by the accrual of a significant legal reserve related to a previously disclosed matter. We believe that this reserve will permit us to cover anticipated costs related to the matter, even though the reserve created a net loss for the quarter.

Further to that, the earnings per share also experienced a YoY drop, showing yet another loss just like in the prior year quarter. This is more disappointment for this firm that has been otherwise strong on top-line revenue.

Oppenheimer - EPS YoY growth (Oppenheimer)

With that said, based on the data I would not recommend this stock on the category of earnings growth, and will wait for Q3 and Q4 results to see if the trend reverses in their favor.

Capital Strength

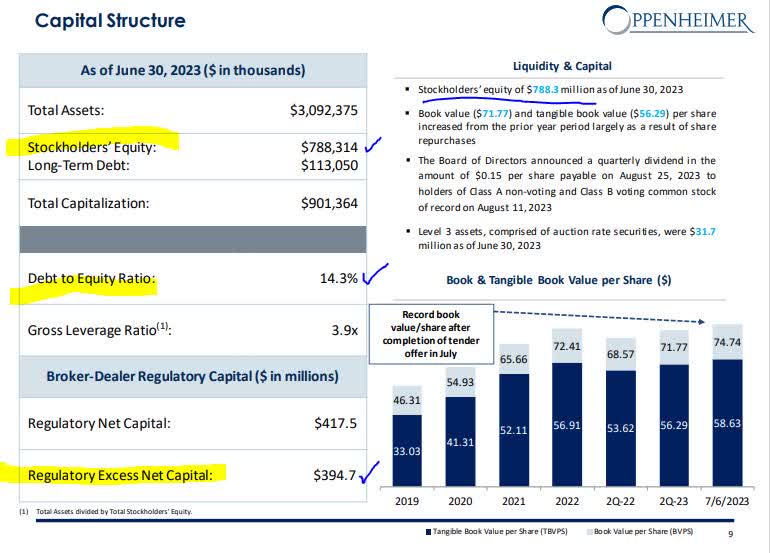

As this is a re-rating from April, I will keep this section brief and focus on key metrics the company has provided from their Q2 results, shown below.

Key items to mention here are that equity is positive, to the tune of $788MM. Also, the debt-to-equity is 14.3%, which I think is very attractive. The firm continues to allocate capital to dividend payouts, always a good sign, and it has regulatory excess net capital of $395MM, also a positive.

Oppenheimer - capital strength (company Q2 results)

So although they missed the mark on earnings, I continue to consider this firm one I recommend on the basis of its capital strength and I expect a similar outlook for Q3 and Q4 a well.

Rating Score

Based on passing 3 of my 5 rating categories above, this stock earned a hold/neutral rating today, which is a modest downgrade from my buy rating in late April. This rating is in line with the consensus from analysts. Currently, it appears the SA quant system is not covering this stock.

Oppenheimer - ratings consensus (Seeking Alpha)

Risk to my Outlook

My neutral outlook on this stock could be impacted by an upside risk by bullish investors & analysts who are more focused on this firm's growth in assets under management & administration rather than some of the other metrics I highlighted. This could open the door to a bullish tailwind after Q3 results especially if the firm beats on analyst estimates.

Consider the following point from their Q2 presentation:

Assets under administration and under management were both at higher levels at June 30, 2023 when compared with the same period last year, benefiting from market appreciation and positive net asset flows.

However, my opinion is that such bullishness will be offset by other analysts & investors who agree with me that the stock appears overvalued and the dividend yield is not competitive especially compared to some other financial sector stocks. Hence, I will remain modestly cautious and stick to my hold rating.

Analysis Summary

To wrap up today's analysis, let's go over the key points discussed:

This stock received a hold rating today, downgrading my buy rating from April. I am agreeing with the analyst consensus on this one.

Positive points: valuation on book value, capital strength, share price vs moving average.

Headwinds: dividends vs sector, earnings YoY growth.

A potential upside risk to my neutral outlook has been addressed.

Concluding Thoughts and Downside Risk:

I continue to keep Oppenheimer on my watchlist as I continue to like the business model of essentially making money from managing money for others.

At the same time, I think the potential downside risk readers should be cognizant of is that this firm has several key competitors for that capital to look after, and is not the only shop on the street. If the AUM/AUA levels were to start decreasing in the next few quarters, that would be of concern and may cause bearishness on this stock.

One major peer, Raymond James, has seen a healthy influx of assets to manage.

According to an August article on Raymond James by Seeking Alpha,

Financial assets under management of $204.6B in July, up 2% from June and up 6% from a year ago.

Client assets under administration of $1,313.5B rose 3% from the prior month and gained 10% year-over-year.

Also in August, according to portal Investment News, Raymond James also " welcomes $250MM AUM Edward Jones team"

So, my neutral sentiment on this stock remains.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.