Wallenius Wilhelmsen: China Internally Suffers, But Not Exports

Summary

- Wallenius Wilhelmsen is benefiting from the return to normal in car exports and trade in vehicles after the COVID-19 pandemic.

- Chinese exports being decimated by COVID-zero policies last year is a positive factor for global trade volumes as they recover and reopen.

- Despite potential credit crunch and falling demand, the margin of safety in car sales volumes and pent-up demand should keep trade volumes relatively stable.

- Moreover, the shift to longer routes due to foreign exchange considerations that are likely to endure should provide downside protection on charter rates.

- Looking for a helping hand in the market? Members of The Value Lab get exclusive ideas and guidance to navigate any climate. Learn More »

AvigatorPhotographer

Wallenius Wilhelmsen (OTCPK:WAWIF)(OTCPK:WILWY) is a RoRo shipping company primarily that has been benefiting from the return to normal in car exports and trade in vehicles that was depressed during COVID-19. There are more tailwinds, namely the fact that Chinese exports were decimated by COVID-zero policies last year. China is an issue in terms of global demand, but not in global supply, and the trade volumes are what matters. Also, with the data on car volumes, we can say with some confidence that there is a margin of safety that should keep car demand pretty flat even if there are some larger credit and demand hits in the economy.

Q2 Data

Let's start with high level data.

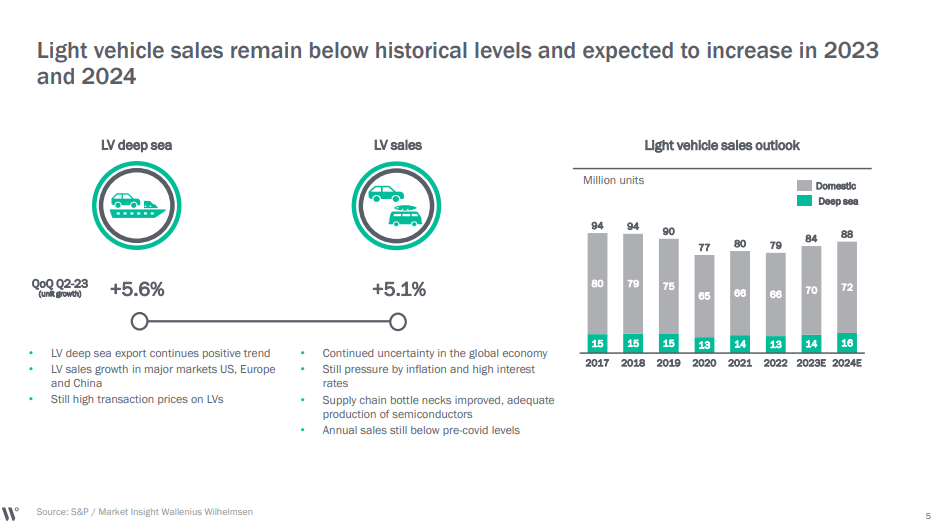

Light Vehicle Volumes (Q2 2023 Pres)

Light vehicle sales are pretty low, around 11% below pre-COVID levels, giving us a pretty good indication of what is happening in terms of excess demand since pre-COVID. 11% is a large margin of safety to assure pretty constant trade volumes even if the automotive markets are hit by a credit crunch and falling demand at some point in the next 12 months.

While volumes are important, there are other factors at play as far as RoRo economics go. Light vehicle sales growth means that the ships are more heavily laden, so there is growth in terms of charter revenue, but the revenue per storage unit is less now due to the generally weaker demand for goods and more availability of shipping.

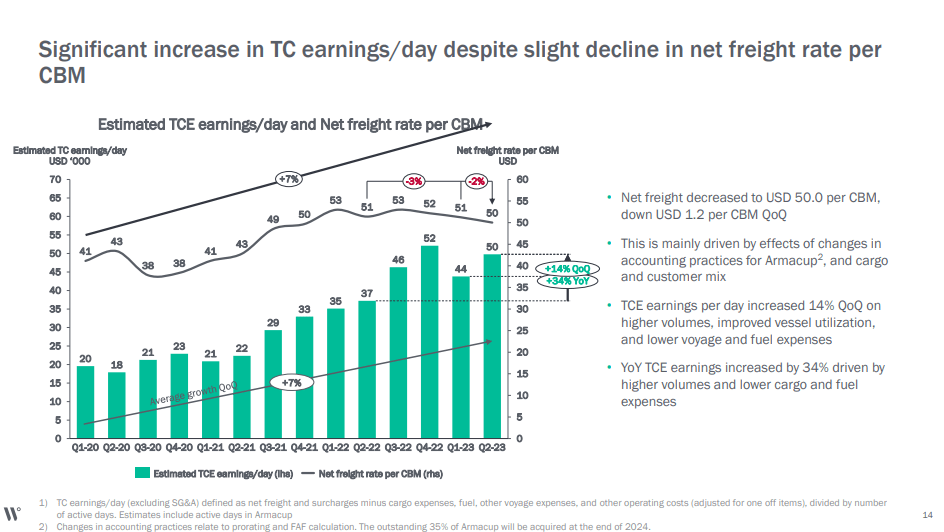

Dailies (Q2 2023 Pres)

There is some sequential pressure on daily earnings compared to Q4 2022, showing that there is cooling going on in RoRo shipping demand, but the YoY figures look good. Ultimately, the sharp uptrend in exports from Asia, and shift in demand to more distant manufacturers in Japan, Korea and elsewhere where currencies have depreciated more, is a general positive force in terms of keeping up charter rates and volumes - volumes of both cars and heavy machinery since both get transported by RoRo. In particular, on the volume side, the end of COVID-zero in China is important, since a lot of automotive parts were creating bottlenecks there when shutdowns were happening in 2022.

Shipping services is almost 90% of the EBITDA, and ultimately the commodity deflation easing fuel costs, and the general scope to control costs while revenues rise and charters become more valuable, has allowed for RoRo EBITDA growth.

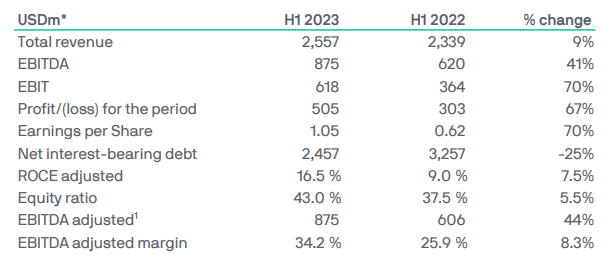

IS (Q2 2023 Pres)

Bottom Line

The release of capacity from COVID-zero comes at a good time in terms of the development of BEV, where BEV exports from China are rising and filling up RoRo vehicles. Longer routes, namely from places like Japan to the US and Europe, make RoRo ships less available as they're occupied for longer, meaning higher charter rates. This is being driven by Far East Asian depreciation, which is going to be an enduring phenomenon. In terms of volumes, while promotional activity on the buyside in the case of demand contraction will leak into lower prices in charters for Wilhelmsen, the volumes themselves should remain rather flattish thanks to the margin of safety in the car sales volumes being substantially below pre-COVID levels still and the presence of pent-up demand as a potential way to get through a recession relatively unscathed despite being a consumer durable.

This is a strange economic cycle. RoRo, and a lot of business related to cars in general, will be safer than it usually is in a downcycle despite pressure from the credit side. The PE multiple is around 4x for this stock. That's very low. About 7% of EBITDA is being bolstered by logistics activity around the Ukraine war, being paid for by NATO activity. While the earnings direction is going to be more ambiguous for these cyclical although high quality businesses, the 4x PE is definitely compelling enough value to consider the stock. Although we still place higher value on predictability and recession resistance, especially because you can find it for almost as cheap if you know where to look.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you thought our angle on this company was interesting, you may want to check out our idea room, The Value Lab. We focus on long-only value ideas of interest to us, where we try to find international mispriced equities and target a portfolio yield of about 4%. We've done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our gang could help broaden your horizons and give some inspiration. Give our no-strings-attached free trial a try to see if it's for you.

This article was written by

Formerly Bocconi's Valkyrie Trading Society, seeks to provide a consistent and honest voice through this blog and our Marketplace Service, the Value Lab, with a focus on high conviction and obscure developed market ideas.

DISCLOSURE: All of our articles and communications, including on the Value Lab, are only opinions and should not be treated as investment advice. We are not investment advisors. Consult an investment professional and take care to do your own due diligence.

DISCLOSURE: Some of Valkyrie's former and/or current members also have contributed individually or through shared accounts on Seeking Alpha. Currently: Guney Kaya contributes on his own now, and members have contributed on Mare Evidence Lab.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.