The REIT has a national presence in Canada, with a focus on the Maritime Provinces and Ontario.

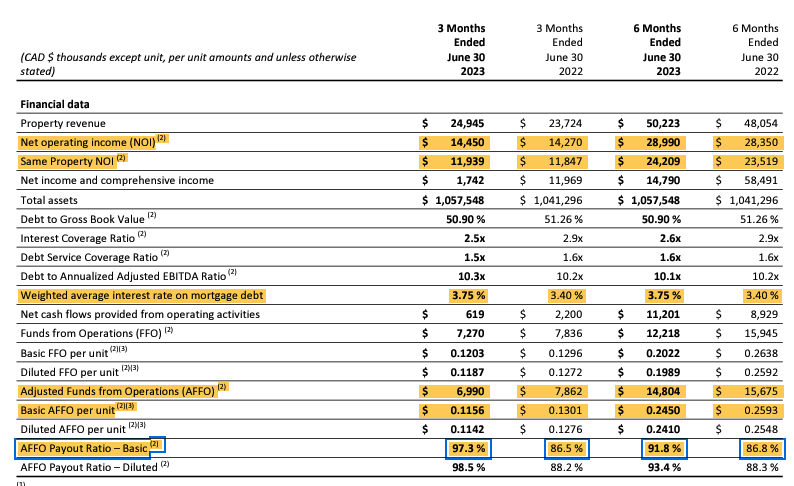

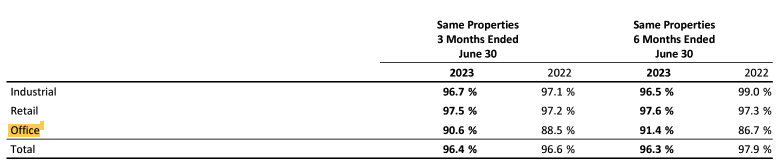

Q2 2023 results showed flat NOI and decreasing AFFO, but the decrease in occupancy was due to a temporary vacancy that has since been re-leased.

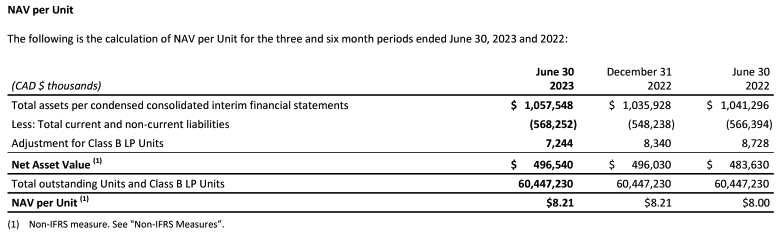

The REIT trades at a 45% discount to NAV and has an 8.26% yield.

1933bkk

Introduction

You may recall that I began covering Pro REIT (TSX:PRV.UN:CA) in May 2023 and made the following conclusion:

The REIT certainly looks attractive at a 26% discount to NAV and has a higher than average yield at 7.45%. The REIT should see strong cash flows over the next year (possibly the next two) purely from lease rollover as acquisition activity reaches its climax. As an investor I wouldn't expect these cash flows to get shared, with the higher than average leverage ratio I expect the bulk of these cash flows to go towards debt repayment to keep their interest expenses at bay. With a recession looming, rising rental rates may not be able to outpace interest rate increases forever. The payout ratio is pretty high at 86% of AFFO as well.

That slower growth profile is still very attractive at the current valuation in my view. I mark this as a buy.

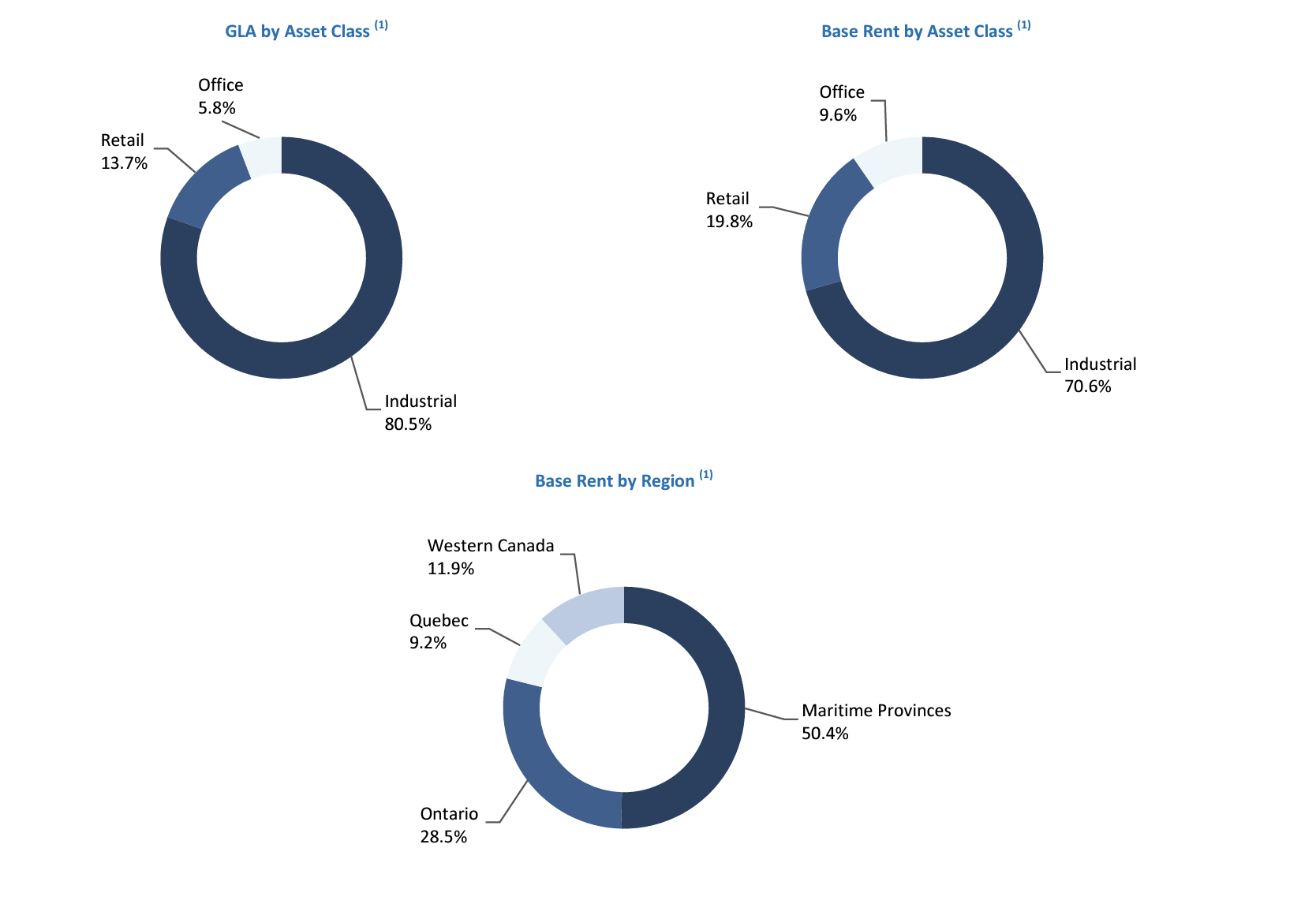

As you may recall this is a REIT with a national presence in Canada although their properties are largely concentrated in the Maritime Provinces with 50% of assets and Ontario with 28%. The REIT is also considered diversified but has made efforts to part ways with their office properties which today's market regards as toxic waste and has reallocated their capital to much more beloved industrial assets. The REIT now has 71% of assets in the industrial space. The majority of the properties in the portfolio are high-quality properties, located in prime locations along major traffic arteries benefitting from high visibility and convenient access.

Q2 2023 MD&A (Pro REIT)

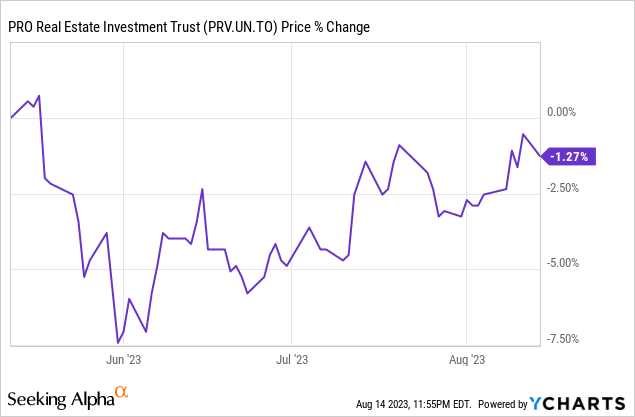

The REIT has largely been flat since I last covered it, but I will reassess based on the recent release of Q2 2023 results.

The key takeaways from the report were flat NOI and same property NOI growth, the increasing interest expense, the decreasing AFFO (AFFO per share) and the payout ratio.

Q2 2023 MD&A (Pro REIT)

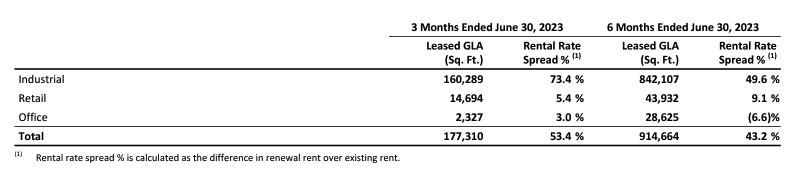

The flat NOI and decreasing AFFO is a bit perplexing as leasing spreads on their industrial properties were unfathomable at 73% in Q2 2023 versus Q2 2022 but management clarified that.

Q2 2023 MD&A (Pro REIT)

The decrease in occupancy in the industrial asset class for the three and six month periods ended June30,2023 is driven by a temporary vacancy of a 102,000 square foot property in Montreal, Quebec as of April 1, 2023. The property has been fully re-leased with occupancy starting in the third quarter of 2023. The overall increase in the Same Property NOI, adjusted to exclude the NOI of the temporary vacancy of one industrial property for the three and six month periods ended June 30, 2023, was $451,000 and $1,051,000 or 3.9% and 4.6% respectively.

The space was fully re-leased to two tenants in June 2023 with 10 year lease terms with an average rental rate spread of 55% over the previous tenants. Occupancy will commence in the third quarter of 2023. Management expects year-end profitability to exceed fiscal 2022 as a result of this leap. In addition the REIT had to payout $2 Million in one-time bonus pay to their previous CEO Gordon Lawlor who retired at the end of fiscal 2022 and had to pay $10 Million of the property tax owed for 2023 in Q2. These factors impacted the payout ratio which has never been particularly low but the 12% decline in AFFO in Q3 2023 vs. Q2 2022 pushed the quarterly payout ratio up to 99%. The payout ratio should normalize towards ~90% as the year progresses.

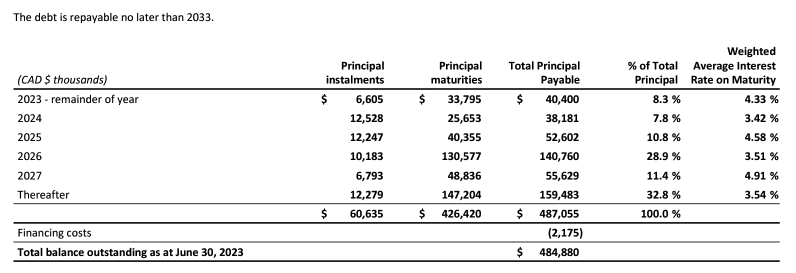

The REIT is not exactly the most conservatively financed at 10X annualized EBITDA (more on that later) but we can already see interest rates taking their toll with the weighted average interest rate on debt now at 3.75% versus 3.40% one year ago.

On June 1, 2023, the REIT closed on a new mortgage to refinance six industrial properties located in Winnipeg, Manitoba for $20.5 Million. The rate on the new mortgage was fixed at 5.07% with a term of seven years. Proceeds of the refinancing were used to repay approximately $16,600 of mortgages maturing in July 2023, $53 in yield maintenance fees and the balance used for general business and working capital purposes. On June 29, 2023, the REIT received a $10 Million three year term loan at rate of 6.79%. Approximately $3 Million of the proceeds was used to partially repay the credit facility on June 29, 2023 with another $5 Million partial repayment on July 7, 2023. The staggered repayment was a result of a July 2023 maturity date of the borrowings under the bankers' acceptance facility. The remaining balance was used for general business and working capital purposes.

On May 26, 2023 the REIT issued $35 Million in unsecured subordinated debentures bearing 8.00% interest per annum payable semi-annually and maturing in June 2028.

Source: Q2 2023 MD&A

The issuance of subordinated debt at 8% is most interesting as that was preferable to what they would have been paying to draw funds on their LOC. The weighted average rate on debt expiring in 2023 is 4.33%. The saving grace is the debt maturities are well staggered with a weighted average term of ~5 years and only 27% of debt matures in the next three fiscal years. Not the most ideal debt profile but far less concerning that other REITs I follow such as Artis REIT (AX.UN:CA) and H&R REIT (HR.UN:CA) whose leverage is at comparable levels but with weighted average terms of less than three years.

Q2 2023 MD&A (Pro REIT)

The REIT has managed to reposition itself nicely in getting away from office assets. In June 2023 the REIT entered an agreement to sell two non-core office properties totalling 60,000 sq. ft. for gross proceeds of $9 Million which will repay $5.7 Million in related mortgage debt expiring in 2023 with the rest to be used for working capital purposes. One of the properties had an expiring lease and a tenant who did not plan to renew.

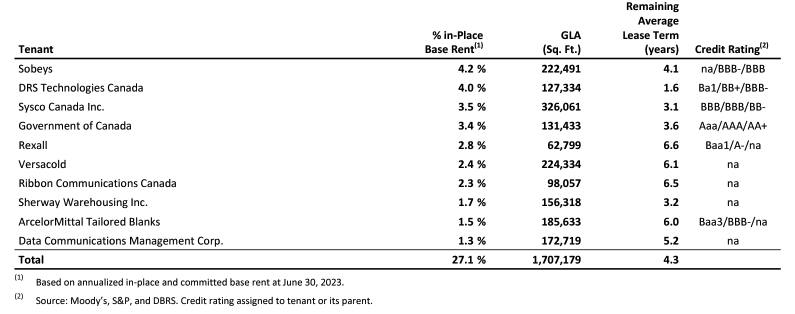

The office portfolio is not that bad however, and would potentially be the envy of many pure-plays as occupancy was at ~91% at Q2 2023 and actually increased from its levels in 2022. The REIT even managed to re-lease 15,730 sq. ft. in vacant space between a couple different properties with terms of up to 5-10 years. The weighted average lease term is ~4 years and lessees are largely government and investment grade tenants.

Q2 2023 MD&A (Pro REIT)

Q2 2023 MD&A (Pro REIT)

Valuation

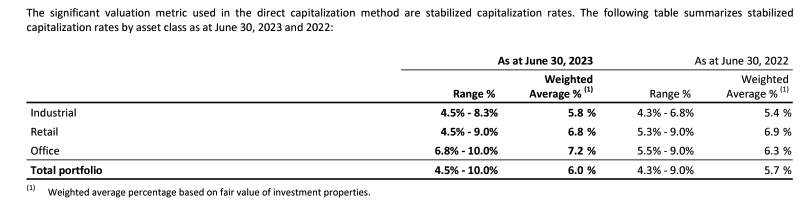

Despite rising interest rates management has largely left their NAV estimate unchanged over the past year. I feel this estimate is reasonable. There is a wide range in cap rates that are used to value properties but even 5% is high for light industrial properties which is what the REIT mostly holds. Although the REIT has properties throughout the maritime provinces the new supply has badly lagged absorption in Halifax. The current vacancy rate in Halifax is currently less than 2%. Cap rates between 7-10% is more than fair for any office properties and 5-9% is more than fair national branded retail outlets that are the main retail tenants of the REIT.

Q2 2023 MD&A (Pro REIT)

Q2 2023 MD&A (Pro REIT)

Colliers (Q1 Industrial Report Halifax)

Risks

Despite the impressive growth in NAV since 2020, a large part of their success has been the strength of the industrial market in Canada.

The industrial sales market declined 37% from Q2 2022 and 64% from a record high Q1 2023, but remains a bright spot in the CRE investment market. Despite obvious pressure from rising rates, industrial leasing volume remains very strong, with a national availability rate hovering near one percent. The combination of record high population growth with land constraints in most major markets continues to mean industrial demand far outstrips supply. Industrial rent growth has partly been driven by a changing ownership profile as well: foreign investors have aggressively raised rents in previously flat markets, Quebec most notably.

The question for industrial is the long-term fortune of e-commerce and fulfilment centres; after the tremendous growth during lockdowns, the market for e-commerce has flattened considerably, as consumer spending has shifted from good to services, travel, and entertainment.

Canada Capital Markets Snapshot Q2 2023 (Colliers)

Although the REIT would not be immune to a decline in e-commerce their industrial assets tend to be more "light industrial" rather than production and storage of consumer goods. For example, larger tenants include Versacold and Sherway Warehousing that are more in food production and storage.

The REIT is not the most conservatively financed at 10X net debt/EBITDA. This is not unusual for industrial REITs as most have been pushing the boundaries as their asset values keep skyrocketing. Management has indicated that industrial properties in Halifax and Ontario/Quebec that they have renewed over the past year have been renewed for 3-5 and 5-10 year lease terms respectively with annual rent step-ups of at least 3%. So even though interest expense may increase $2-3 Million annually over the next couple years it will be offset by an industrial portfolio that currently generates $70 Million in rental revenue that can increase revenue by $2-3 Million and that's before renewals.

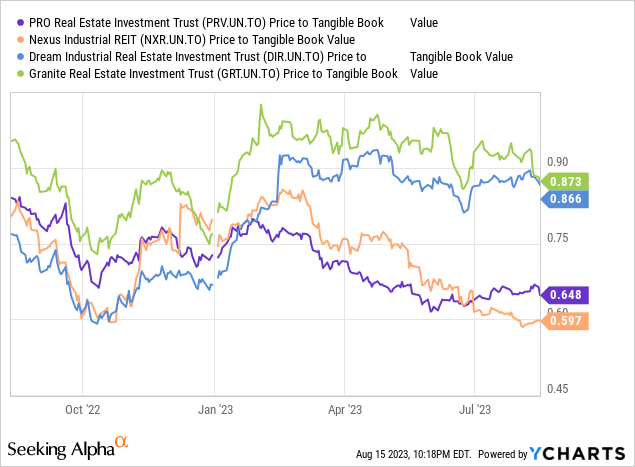

Despite the high leverage it will be hard to do poorly on this REIT at a 45% discount to NAV. The REIT is among the cheapest among its peers and has been among the most successful at growing NAV in the past 3 years. Despite its high leverage, I believe its asset base is strong enough to offset higher interest expense and therefore I think the current 8.26% dividend yield is fairly safe.

I am always on the lookout for businesses that have a strong cash generating ability and a strong enough competitive advantage that I can be sure they will be around for the next decade, and at a price where I can be as sure as possible that I can achieve at least 15 percent annualized returns, or else companies whose price is deeply discounted from their asset base as long as its highly marketable. Im not one to shy away from takeover targets, provided the target still has a strong business that I would be okay with owning it even if the takeover did not go through. Since I began investing on my own 3 years ago I have achieved an annualized time weighted return of about 16 percent, and plan to continue to beat that hurdle as I learn more.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of PRV.UN:CA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments

Disagree with this article? Submit your own. To report a factual error in this article, . Your feedback matters to us!

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.