Okta Preview: Revenue Revisions Awaited

Summary

- Okta's Fiscal Q2 2024: While I'm bullish, caution arises as Okta's stock has dropped 50% in 2023 and could be transitioning into a ''show-me'' story.

- Customer Adoption Curve: A significant indicator of business viability, a +15% increase in total customers YoY would signal thriving performance amid a demand for value-driven software.

- Okta's valuation has expanded despite slowing growth, with the challenge of maintaining investor confidence resting on sustained revenue re-acceleration.

- Looking for a helping hand in the market? Members of Deep Value Returns get exclusive ideas and guidance to navigate any climate. Learn More »

MF3d/E+ via Getty Images

Investment Thesis

Okta (NASDAQ:OKTA) is heading into its Fiscal Q2 2024 at the end of August. While I remain bullish on Okta's prospects, I'm becoming increasingly wary that Okta is starting to become a "show-me" story.

Here I describe some of the pluses and minuses of this investment.

Heading Into Fiscal Q2 2024, What to Think About

Okta specializes in identity and access management solutions. Okta provides cloud-based services to help businesses securely manage user identities and access to various applications, delivering enhancing security and user experience.

Okta's Single Sign-On ("SSO") product allows users to access multiple applications and services with just one set of login credentials, streamlining the authentication process and enhancing security.

As we head into Okta's fiscal Q2 earnings on 30th August, the one consideration that I believe will carry its earnings results will be an uptick in its current remaining performance obligations ("cRPO") and the pace that Okta will add new customers. Allow me to explain both.

As followers of my work will know, I've made this argument on previous occasions, and I'll reiterate my point now, the customer adoption curve is in my opinion the single best indicator of the health of a business.

If we see when Okta reports its fiscal Q2 2024 results that its customer adoption curve has accelerated once again, this will be a positive indicator that the business is still thriving. The figure that I'm looking out towards is a +15% increase in total customers y/y.

Additionally, I have seen several recent earnings reports confirming this point of view. To illustrate, there's still a lot of customer appetite for software companies that provide enterprises with a clear value proposition, in Okta's case a comprehensive identity and access management platform that enables organizations to securely connect their users and manage applications. But customers are demanding more value than they were in the past two years.

Simply put, IT departments are requiring clear and high ROIs, before embracing "yet another" productivity software platform. To this end, we've seen companies mention on numerous occasions during the current earnings season that IT departments are embracing a wave of software consolidation and providing added scrutiny to the software adoption process. To put it simply, the time of easy money has gone and if a company isn't seeing clear value, they are rethinking whether they truly need that software or whether an alternative option will suffice?

Next, we'll discuss Okta's cRPO.

Okta's Guidance Needs to be Upwards Revised

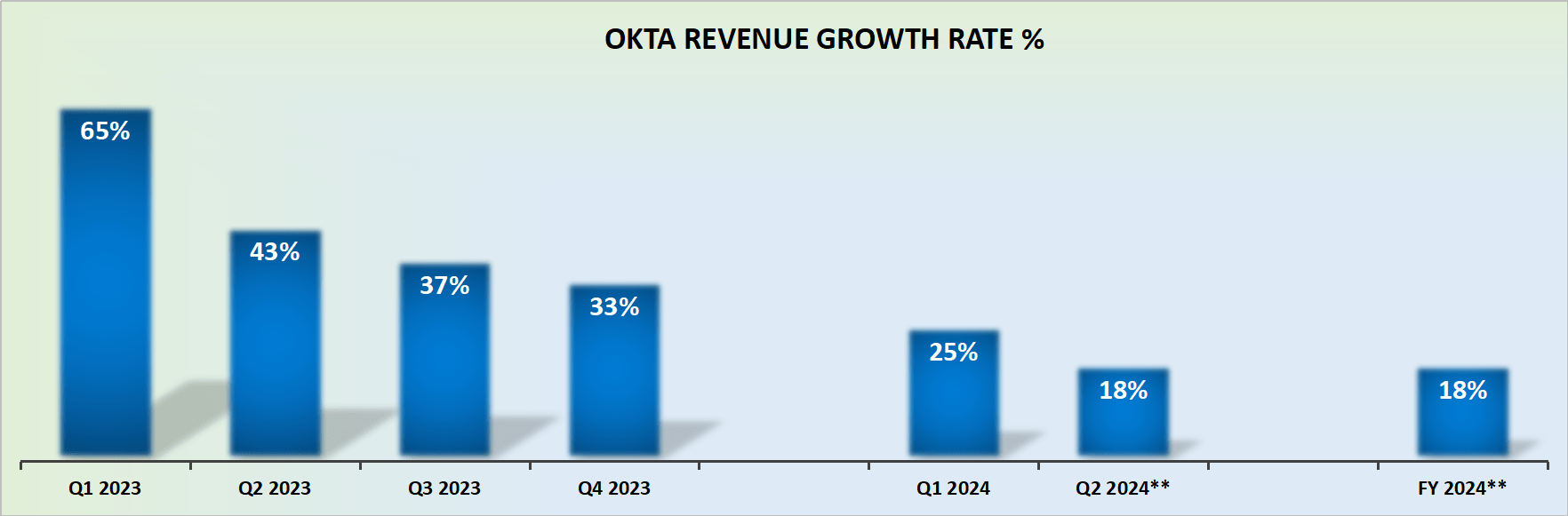

OKTA revenue growth rates

In fiscal Q1 2024, that is last quarter, we saw Okta's cRPO decelerate from 25% in fiscal Q4 2023 down to 20% for Q1 2024.

Given that Okta's revenue growth rates at the time were up 25% y/y, which is higher than its cRPO figure, this would lead one to conclude that Okta recognized revenues at a pace that is not consistent, and was higher, than the amount of bookings it has received.

There's nothing wrong with this. But it could mean that Okta will in the coming quarters see its revenue growth rates decelerating into the mid-teens, unless Okta's cRPO figure or its customer bookings figure increased.

Consequently, this is my contention, for now, I have a buy rating on this stock. But Okta needs to find a way to reaccelerate and grow its cRPO, otherwise, this would inform me (and the investment community) that this is no longer a rapidly growing company. And it would affect its valuation, which we'll discuss next.

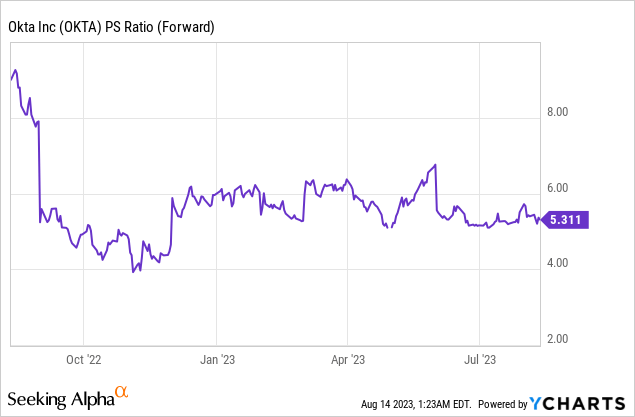

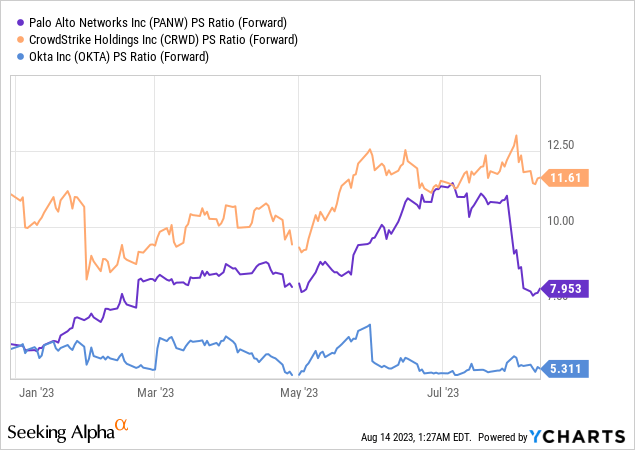

Okta's Valuation - Still Priced as a Growth Stock

Okta's valuation got crushed in the bear market, but since the October lows its multiple has expanded slightly from 4x to 5x. And it has kept this expansion, even while its revenue growth rates have clearly continued to slow down. Why?

Because investors continue to believe that Okta has what it takes to reaccelerate its revenue growth rates. However, investors will only continue to hold that vision for so long. After a while, Okta will become a "show-me" story.

And indeed, the argument could be made that Okta is already a "show-me" story, given that, unlike many other SaaS businesses which have re-rated higher in the past few months, Okta's valuation has remained relatively static since the start of 2023.

Accordingly, by the time Okta reports its fiscal Q2 2024 results, it will be halfway through its fiscal year. Meaning that if Okta does not upwards revise its full-year 2024 revenue guidance, this will put a lot of pressure on the multiple that investors will be willing to pay for Okta.

After all, Okta would be assuredly on the deceleration path, and its underlying profitability would become increasingly in focus. And I'm not convinced that paying more than 50x next year's EPS is all that attractive, for a business with revenue growth rates below 25% CAGR.

The Bottom Line

Heading into Okta's Fiscal Q2 2024 earnings, I maintain a bullish outlook but am growing cautious as the stock's performance has been under pressure.

As I analyze the pluses and minuses of this investment, I'm focusing on the customer adoption curve and the pace of new customer additions, with a keen eye on a potential +15% increase in total customers y/y.

The recent trend in software consolidation and heightened scrutiny in IT departments demand clear value propositions, posing a challenge for Okta to reaccelerate and grow its remaining performance obligations (cRPO).

While Okta's valuation has slightly expanded, its continued ability to reaccelerate revenue growth will be crucial to maintaining investor confidence.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.

This article was written by

Our Investment Group is focused on value investing as part of the Great Energy Transition. For example, did you know that AI uses thousands of megawatt hours for even small computing tasks? Join our Investment Group and invest in stocks that participate in this future growth trend.

I provide regular updates to our stock picks. Plus we hold a weekly webinar and a hand-holding service for new and experienced investors. Further, Deep Value Returns has an active, vibrant, and kind community. Join our lively community!

We are focused on the confluence of the Decarbonization of energy, Digitalization with AI, and Deglobalization.

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

DEEP VALUE RETURNS: The only Investment Group with real performance. I provide a hand-holding service. Plus regular stock updates.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.