Job Gains: Easing Wage Pressures To Come?

Summary

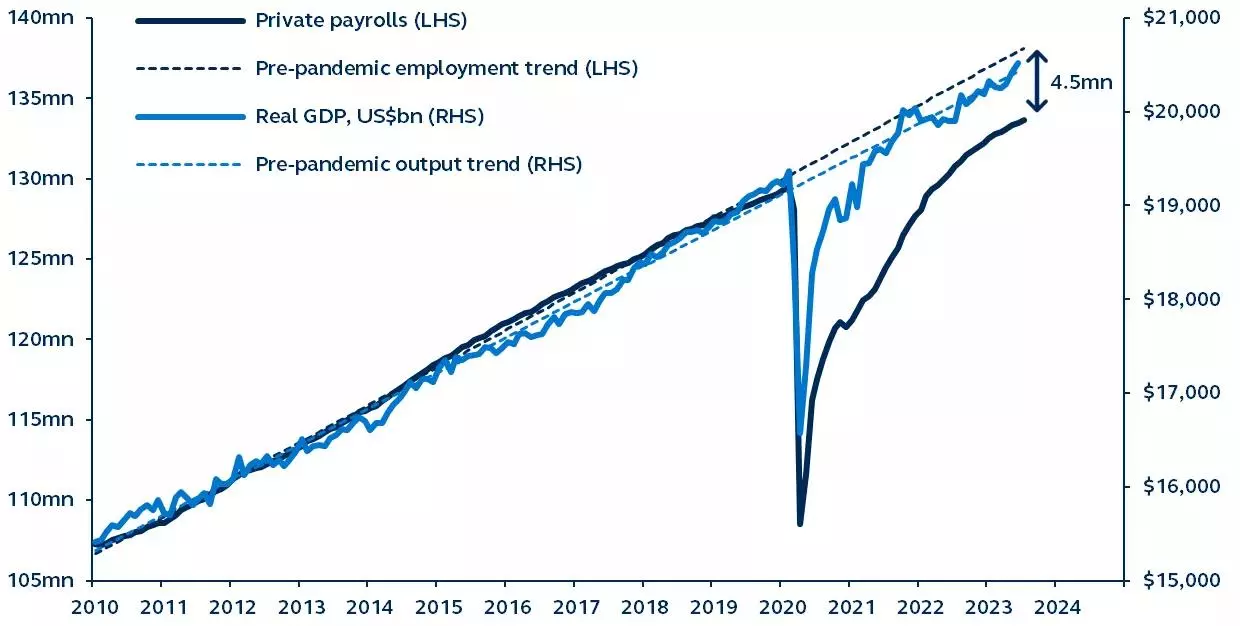

- Employment sits below its pre-pandemic trend and notably, has not recovered as fast as U.S. real GDP.

- Leisure & hospitality has been the biggest culprit, having had a late start on post-COVID reopening.

- As these predominantly low-wage jobs return, investors should expect structural downward pressure on wage inflation.

Ceri Breeze

Employment sits below its pre-pandemic trend and notably, has not recovered as fast as U.S. real GDP. Leisure & hospitality has been the biggest culprit, having had a late start on post-COVID reopening.

As these predominantly low-wage jobs return, investors should expect structural downward pressure on wage inflation - which would be welcome news for the Fed and bolsters the case for a prolonged pause in Fed rate hikes.

U.S. real GDP and private employment versus pre-pandemic trends

2010–present

Source: Bureau of Labor Statistics, Macroeconomic Advisers, Bloomberg, Principal Asset Management. Data as of July 31, 2023.

Despite the deep pandemic recession, real GDP recovered remarkably fast, and real economic output has now surpassed its pre-pandemic trend.

On the other hand, employment and the 22M jobs lost during the pandemic only returned to pre-pandemic levels last June and are still below trend.

From 2010-2020, the relationship between the level of real GDP and private employment was extraordinarily close. Today, however, employment gains have lagged, and the employment shortfall from the pre-pandemic trend suggests that 4.5M more private-sector workers are still needed. Sustainable economic growth will likely require further job gains.

Post-pandemic employment shortfalls have been largely concentrated:

- Manufacturing and Construction, two of the most cyclical sectors, remain about 800k jobs below trend.

- Healthcare services is short over 500k jobs, which likely reflects burn-out among pandemic front-line workers.

- Nearly 1.8M jobs have yet to return to Leisure & Hospitality, indicative of its delayed COVID reopening.

Recently, economy-wide job gains in the face of aggressive Federal Reserve policy rate hikes have confounded investors. Yet, persistent employment shortfalls suggest continued substantial payroll gains should be, in fact, expected.

With the strong likelihood that an outsized portion of job gains from here will come from lower-wage, labor-intensive sectors, wage inflation should continue to moderate while sustaining output growth - another case for a prolonged pause in Fed rate hikes.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

This article was written by