Is General Electric Stock A Wise Choice Amid Air Traffic Recovery?

Summary

- On July 25, General Electric, the mastodon of the industrial sector, released its financial results for the second quarter of 2023.

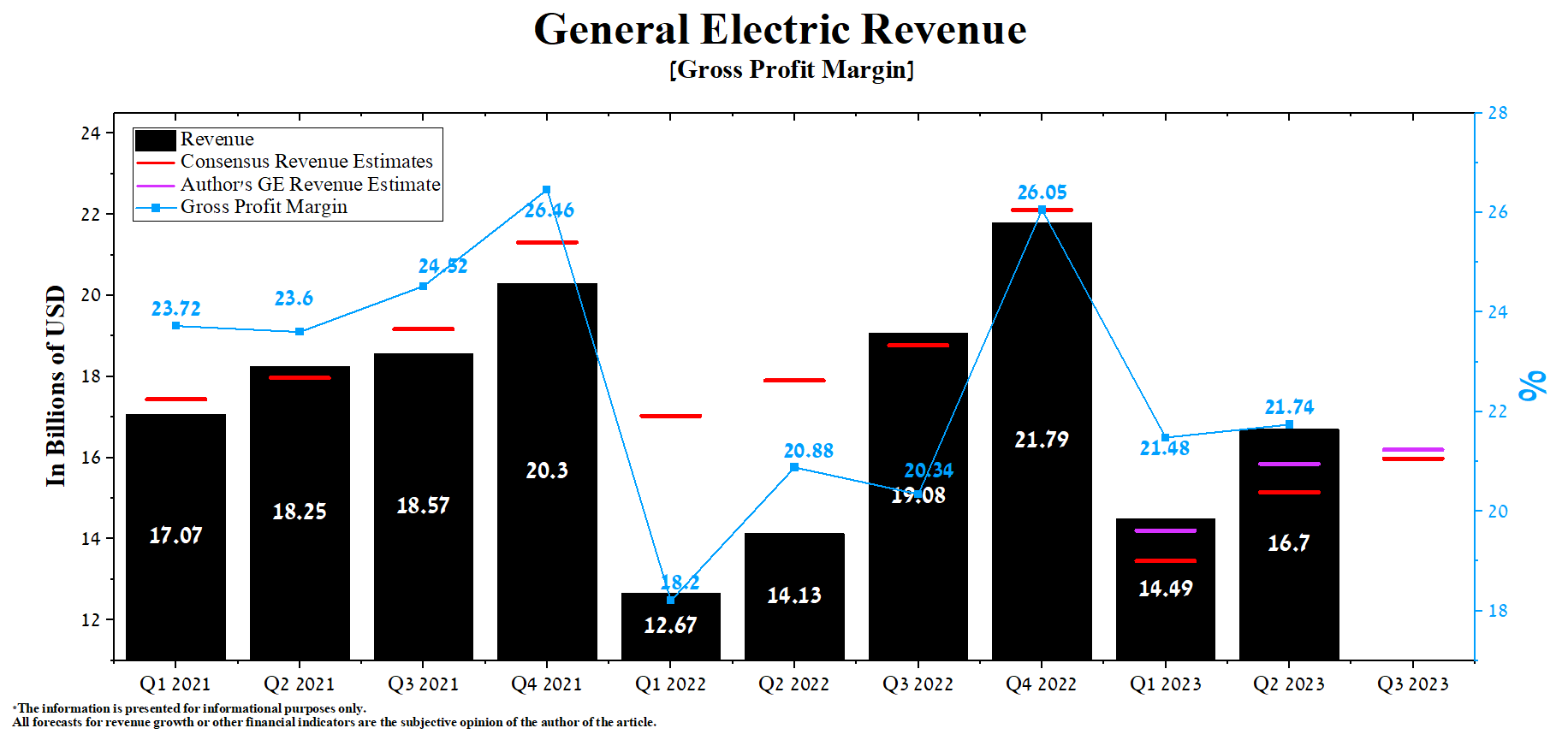

- General Electric's revenue for the second quarter of 2023 was $16.7 billion, up 15.3% from the previous quarter and 18.2% from the second quarter of 2022.

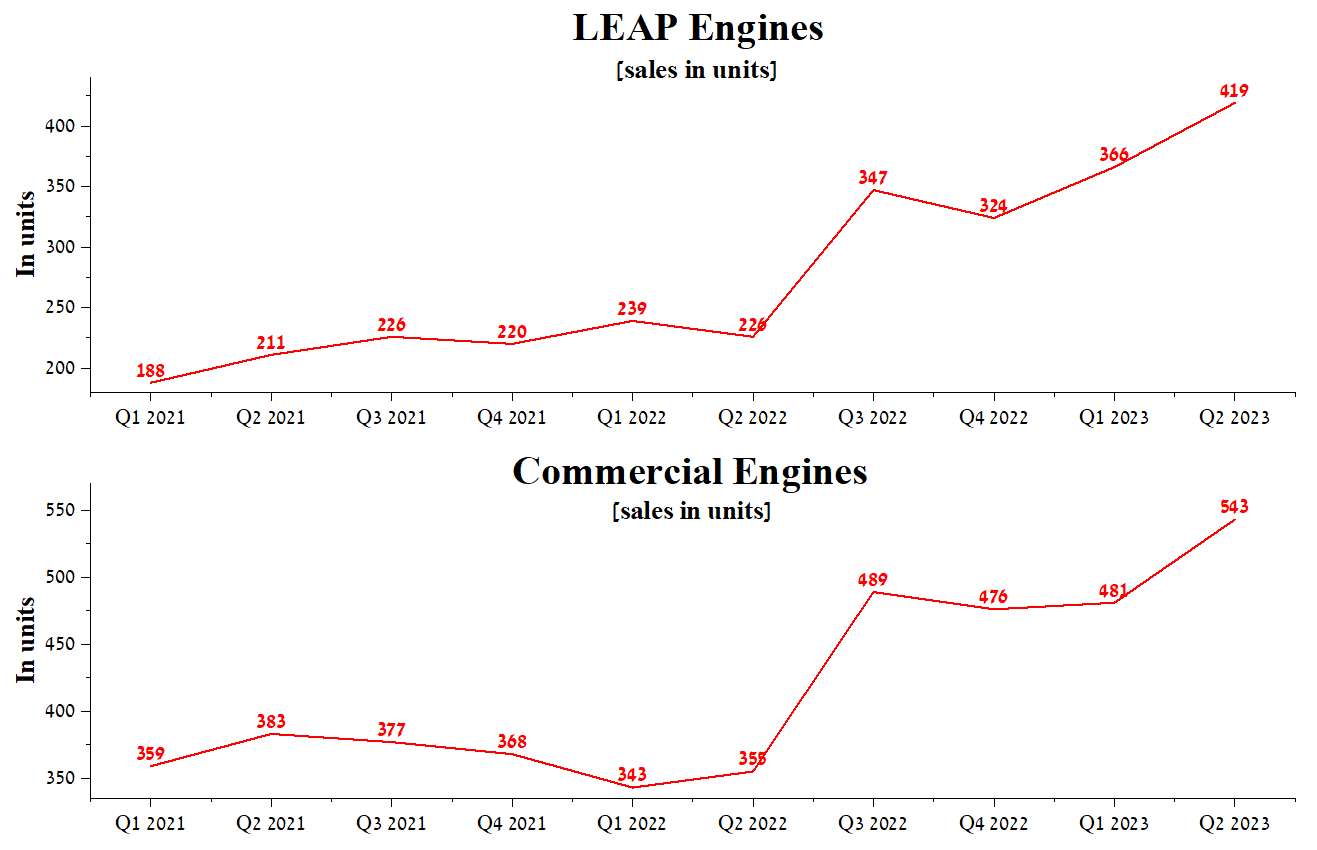

- The total sales of commercial engines amounted to 543 units in the second quarter of 2023, which is 53% more than in the previous year.

- At the end of the second quarter of 2023, General Electric's total debt was about $23.88 billion, down $14.15 billion from 2021, thanks to Larry Culp's efficient financial policies.

- We continue our analytics coverage of General Electric stock with a "hold" rating for the next 12 months.

RgStudio/iStock via Getty Images

Two weeks after the release of General Electric's (NYSE:GE) Q2 2023 financial report, which beat our expectations as well as analysts', news broke on August 1 that its aerospace division is one of the potential buyers of L3Harris Technologies' avionics business. Thanks to a sharp decrease in total debt and an improvement in the company's margins, Larry Culp is on the M&A trail ahead of the early-2024 spinoff of GE Vernova, which financial market participants favorably assessed.

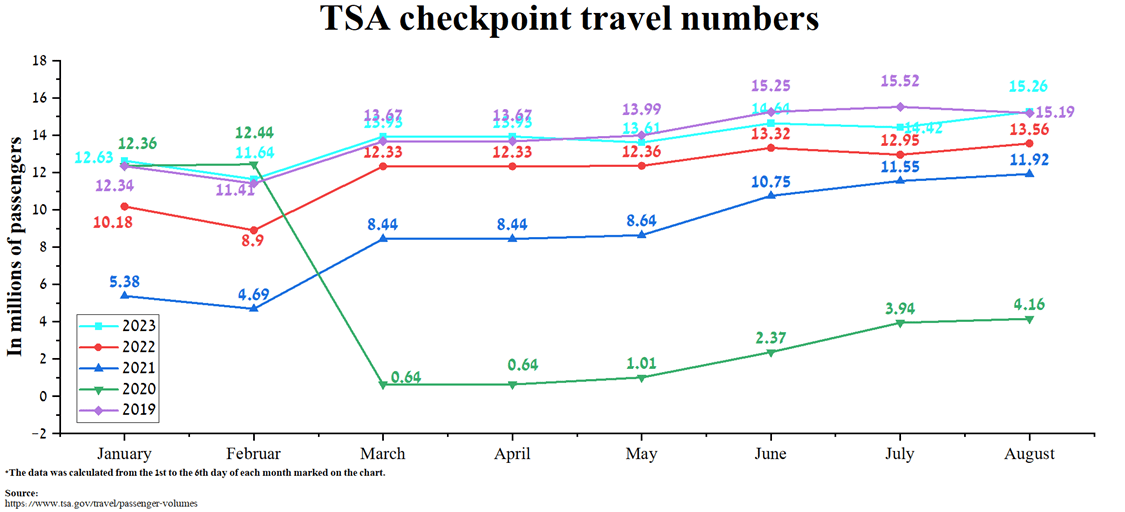

GE Aerospace is a gem in the company's structure in the post-COVID-19 era, thanks partly to increased demand for air travel. Data from the Transportation Security Administration show a record level of passenger traffic in recent years. Thus, in the first six days of August 2023, the number of passengers amounted to 15.26 million, an increase of 12.5% compared to the previous year.

On the other hand, due to rising crude oil and gasoline prices in the US, fears are growing that inflation problems may worsen. These unfavorable events are slowing the pace of the global economic recovery, which not only raises the level of investor fear for its future, but also leads to the suspension of the impulse movement in the price of GE shares.

N_Aisenstadt – TradingView

We continue our analytics coverage of General Electric with a "hold" rating for the next 12 months.

General Electric's Q2 2023 financial results and outlook for the second half of 2023

General Electric's revenue for the second quarter of 2023 was $16.7 billion, up 15.3% from the previous quarter and 18.2% from the second quarter of 2022.

Author's elaboration, based on Seeking Alpha

Both quarterly and year-on-year revenue growth was driven primarily by two of the company's divisions, GE Aerospace and GE Renewable Energy. GE Aerospace's revenue was $7.86 billion, up about $1.73 billion from the prior year, driven by growing demand for air travel. Favorable trends in the commercial aviation industry require carriers to expand their fleet, mainly consisting of Airbus and Boeing aircraft powered by both GE and LEAP engines. Thus, total sales of commercial engines amounted to 543 units in the second quarter of 2023, which is 53% more than in the previous year.

Author's elaboration, based on quarterly securities reports

In addition, the increase in air travel positively affects the shipment volumes of commercial spare parts relative to previous quarters and orders for after-market services of the company's engines. According to the Transportation Security Administration, the total number of passengers was 15.26 million in the first six days of August 2023, an increase of 12.5% on the previous year and exceeding the 2019 level.

Author's elaboration, based on TSA

According to Seeking Alpha, General Electric's Q3 2023 revenue is expected to be $15.24-$17.07 billion, up 5.5% from analysts' expectations for Q2 2023. At the same time, under our model, the company's total revenue will be slightly higher than the median value of this range and will amount to $16.2 billion.

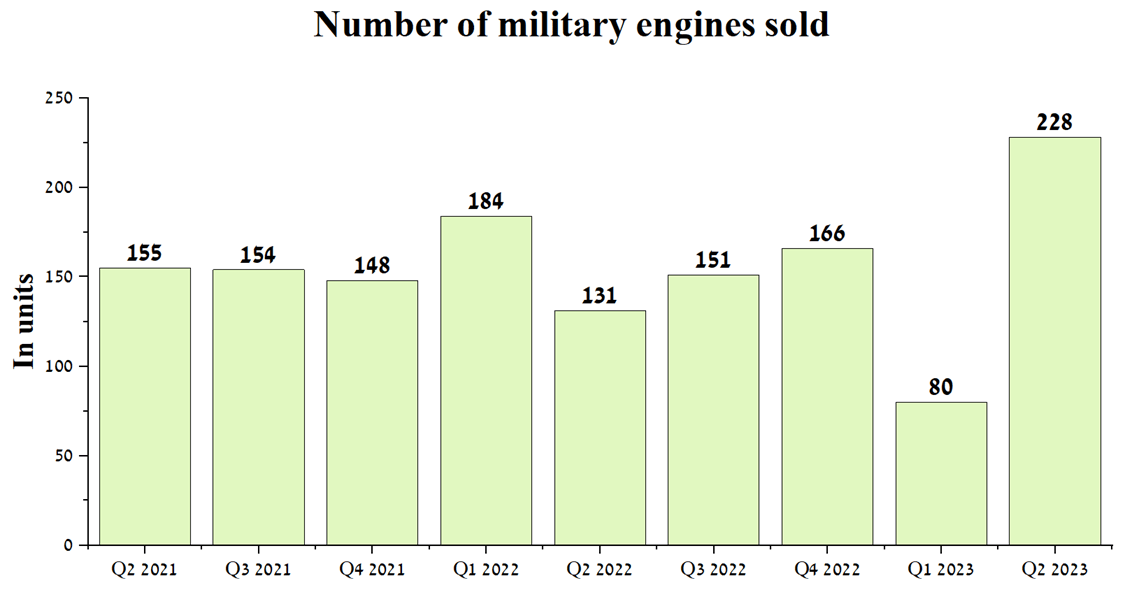

In addition to the growth in sales of the company's commercial aviation equipment, we expect military spending by NATO members and other countries to continue to be extremely high due to Russia's invasion of Ukraine. The war in Eastern Europe provoked an increase in the sale of military aircraft and helicopters powered by high-performance GE engines.

Thus, the number of engines delivered amounted to 228 units in the second quarter of 2023, an increase of 97 units compared to the previous year. This was mainly due to the resolution of logistical difficulties in delivering components for the T700 turboshaft engines used in various helicopters, including the Sikorsky UH-60 Black Hawk and the Boeing AH-64 Apache.

Author's elaboration, based on quarterly securities reports

Moreover, according to Reuters, at the end of June 2023, Germany announced its intention to purchase 60 Chinook helicopters worth up to 8 billion euros to replace its aging fleet of CH-53 helicopters.

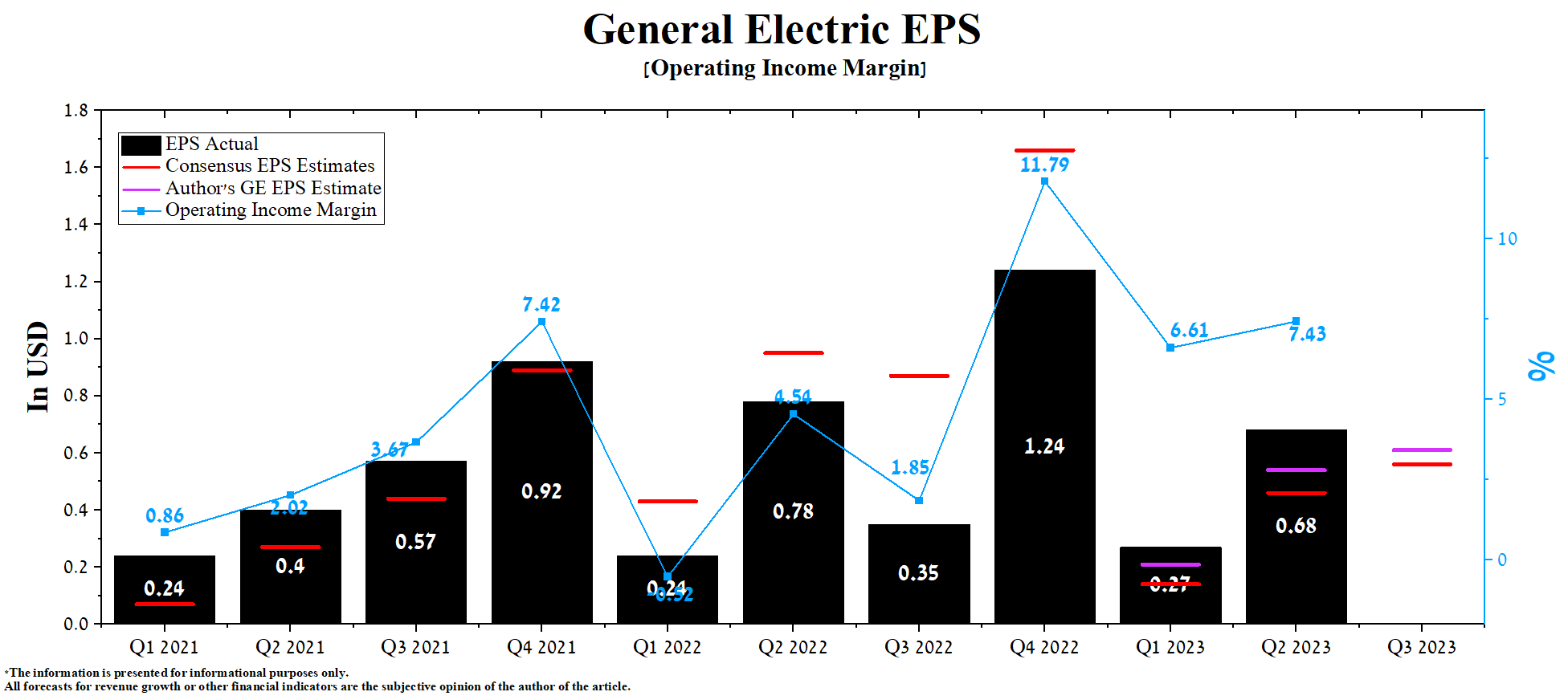

General Electric's Q2 Non-GAAP EPS was $0.68, up 151.9% from Q1 2023, and just as importantly, it has beaten analyst consensus estimates in six of the last ten quarters. Thanks to the improvement in the company's margins, its management raised the guidance for 2023 from $1.70-$2.00 to $2.10-$2.30.

So given the strength of GE Aerospace, and the improvement at GE Vernova, for the full year, we're now expecting revenue growth in the low double digit range up from high single digits. $2.10 to $2.30 of adjusted EPS, up from $1.70 to $2 and that includes 4.7 billion to 5.1 billion of operating profit. And finally, we now guide for a range of $4.1 billion to $4.6 billion for free cash flow up from $3.6 billion to $4.2 billion.

According to Seeking Alpha, General Electric's Q3 EPS is expected to be $0.56, up 21.7% from the consensus estimate for Q2 2023. While we believe this is slightly underestimated, our model puts GE's EPS at $0.61.

Meanwhile, General Electric's Non-GAAP P/E [TTM] of 45.17x is 160.35% higher than the sector average and 3.98% higher than the average over the past five years. On the other hand, P/E Non-GAAP [FWD] is 49.10x, which is one of the factors indicating that the company is overvalued in the current period of slowing down the recovery of the Chinese economy and rising energy prices.

Author's elaboration, based on Seeking Alpha

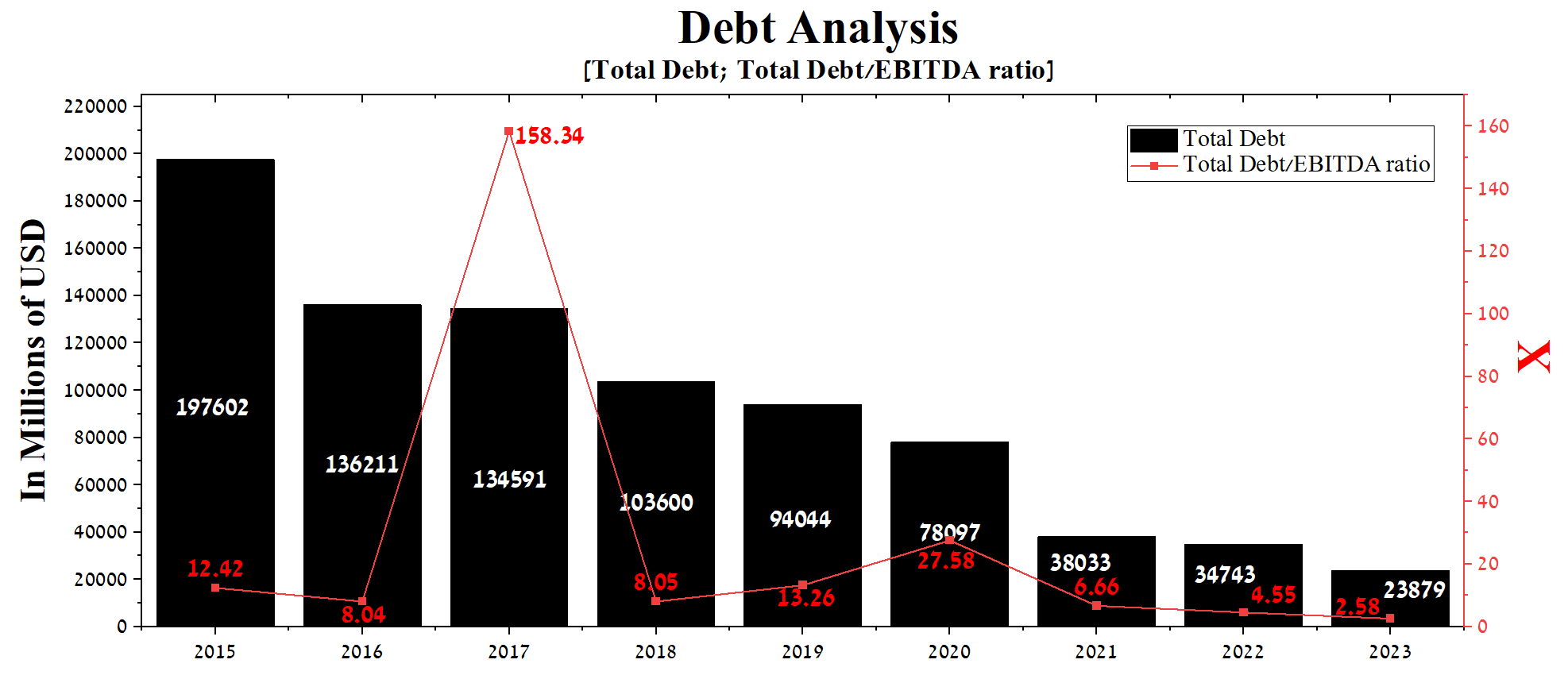

At the end of the second quarter of 2023, General Electric's total debt was about $23.88 billion, down $14.15 billion from 2021, thanks to Larry Culp's efficient financial policies. Moreover, thanks to the growth in EBITDA in recent years, the total debt/EBITDA ratio has dropped from 6.66x to a record low of 2.58x for GE. As a result, we expect Moody's, Standard and Poor's Global Ratings, and Fitch Ratings to upgrade the company's credit ratings, allowing it to obtain debt financing on more favorable terms.

Author's elaboration, based on Seeking Alpha

With General Electric's total debt/EBITDA ratio down below 3x, growing cash flow, and GE Aerospace's revenue, we don't expect the company to have any difficulty redeeming its senior notes maturing between 2025 and 2037.

Risks

In our assessment, there are two main risks to consider that could affect both General Electric's financial position and its share price.

GE Renewable Energy continues to be a loss-making division of the company

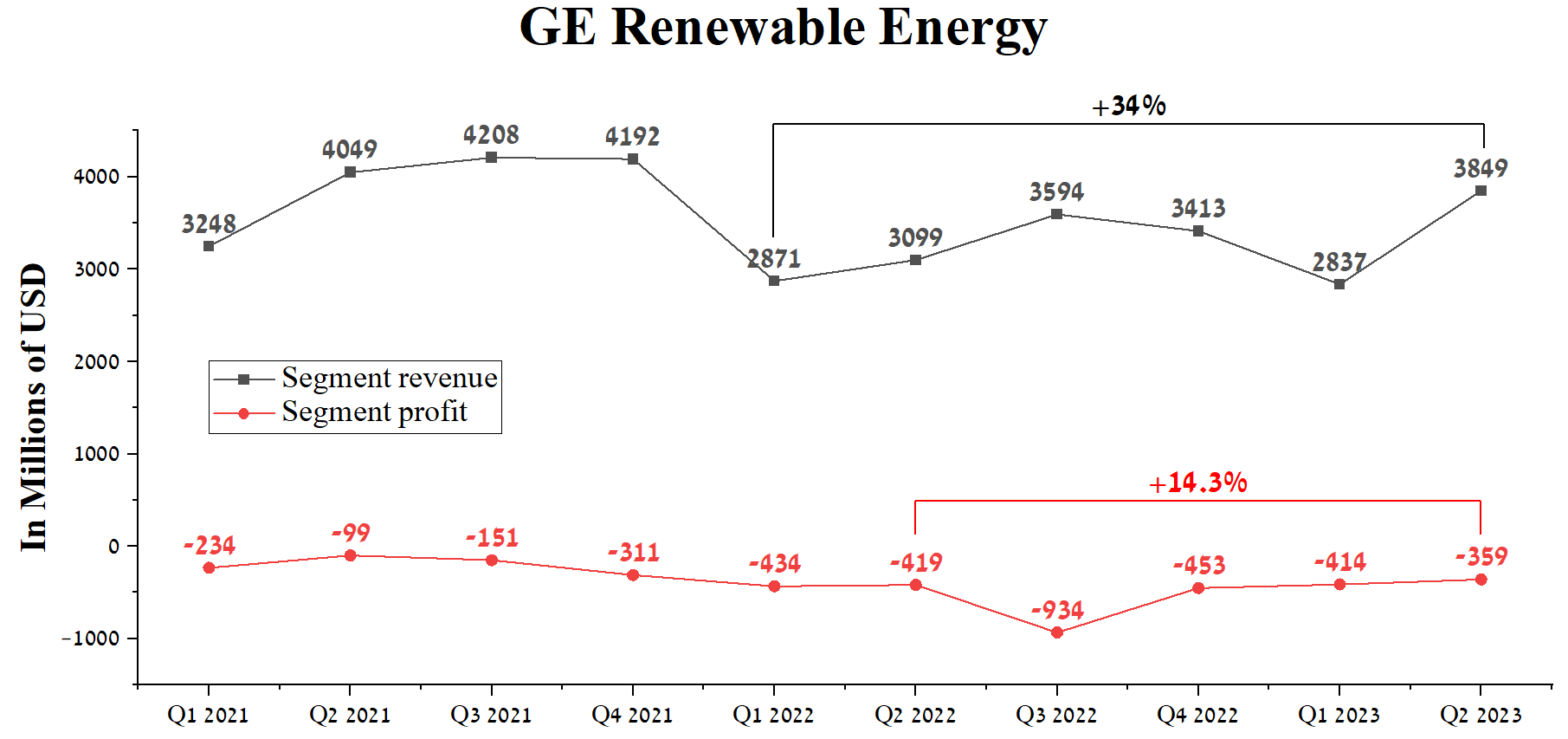

The Renewable Energy segment's revenue was $3.85 billion in Q2 2023, up 34% year-over-year, driven by higher wind turbine deliveries and prices. Despite such a sharp increase in equipment sales in this segment, its losses amounted to $359 million, down only $55 million from the previous year. We believe that GE Renewable Energy will remain unprofitable despite the identified defects in Siemens Energy's wind turbines. Consequently, this may adversely affect the valuation of this unit in anticipation of its spin-off from the parent company.

Author's elaboration, based on quarterly securities reports

China's economic recovery has slowed sharply

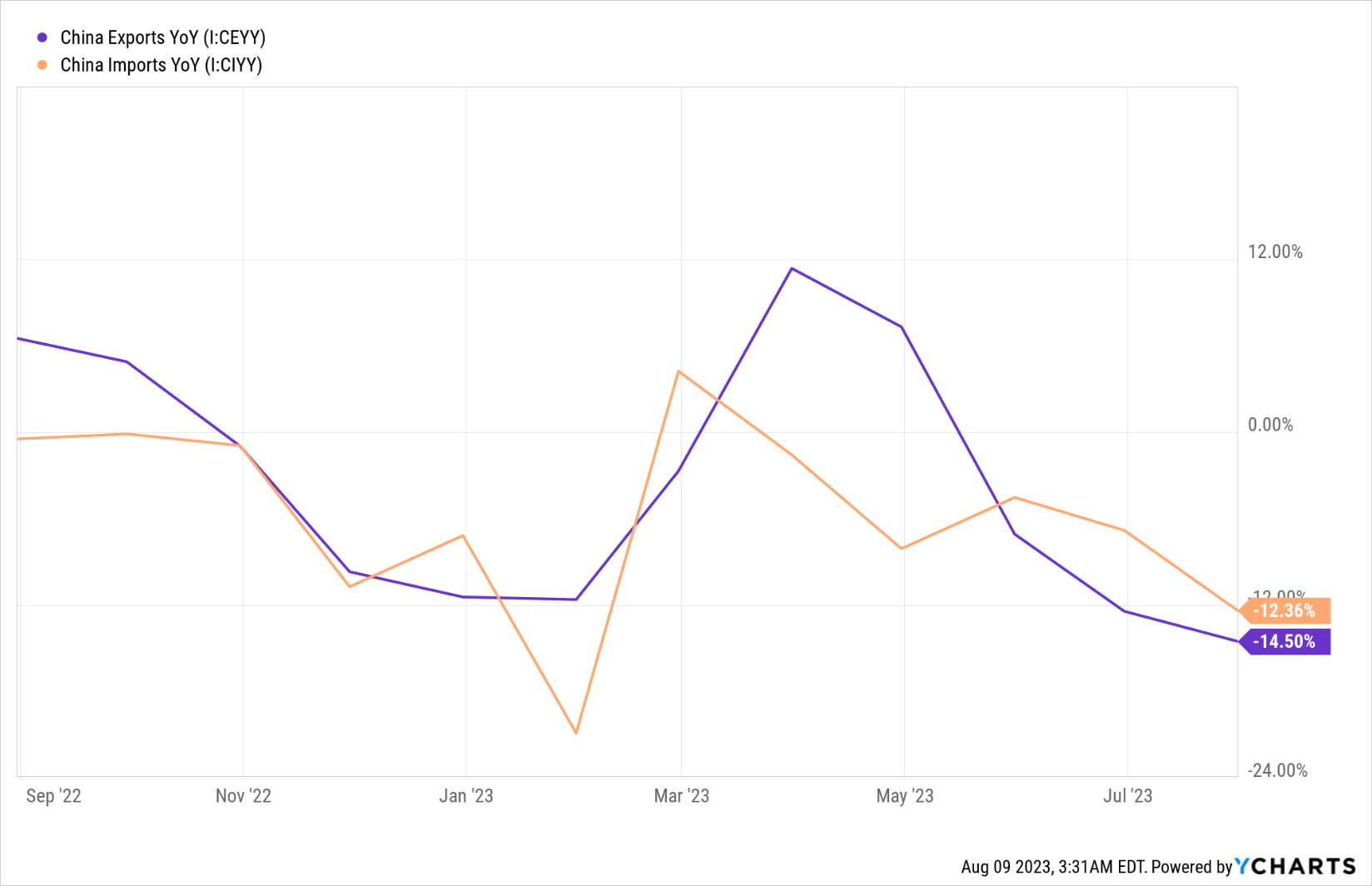

China's imports and exports in July 2023 fell by double-digit percentages from the previous year. Moreover, the pace of their decline turned out to be significantly higher than expected, threatening the prospects for recovery of the second-largest economy in the world. Moreover, published data on construction and manufacturing activity heighten fears that China's economic activity could slow further in the second half of 2023.

YCharts

As a result, this could lead to a slowdown in the aviation fleet expansion rate by local carriers and also negatively affect the level of passenger traffic, ultimately slowing down the growth of GE's revenue.

Conclusion

On July 25, General Electric, the mastodon of the industrial sector, released its financial results for the second quarter of 2023. The company's revenue and net income not only beat analysts' expectations but demonstrated that demand for its products and services is growing faster than Wall Street expected.

At the same time, the revenues of the three segments for the three months ended June 30, 2023, showed mixed dynamics. On the one hand, sales of the Aerospace and Renewable Energy segments are growing at double-digit percentages yearly, while GE Power's revenue is down 1.2%.

Given the growth in margins of all three GE segments and Siemens Energy's problems with their wind turbines, we are raising our previous level at which the risk/reward profile would be attractive. We plan to buy General Electric shares at the price level of $92-$93.5.

However, at this point in time, we will continue our analytics coverage of General Electric with a "hold" rating for the next 12 months.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This article may not take into account all the risks and catalysts for the stocks described in it. Any part of this analytical article is provided for informational purposes only, and does not constitute an individual investment recommendation, investment idea, advice, offer to buy or sell securities, or other financial instruments. The completeness and accuracy of the information in the analytical article are not guaranteed. If any fundamental criteria or events change in the future, I do not assume any obligation to update this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (1)