Whitecap Resources: Strong Free Cash Flow In Q2 Despite Wildfire Curtailments

Summary

- Whitecap saw a slightly lower production of 147,166 boe/d in Q2-23, due to the wildfires in Canada, operations has since returned to full production.

- The company did still report solid cash flows, with C$415M in funds flow and C$197M in free cash flow.

- The net debt is currently C$61M above the target, which is likely to be reached in Q3-23, at which time 75% of cashflows will be distributed to shareholders.

- This idea was discussed in more depth with members of my private investing community, Off The Beaten Path. Learn More »

Sergei Dubrovskii

Investment Thesis

Whitecap (OTCPK:SPGYF) (TSX:WCP:CA) yesterday after the close released its Q2 result, and the company will host a conference call later today. This article covers my main takeaways on the Q2-23 result and some general views on the company. I have covered Whitecap a few times over the last year here on Seeking Alpha and those articles can be found here.

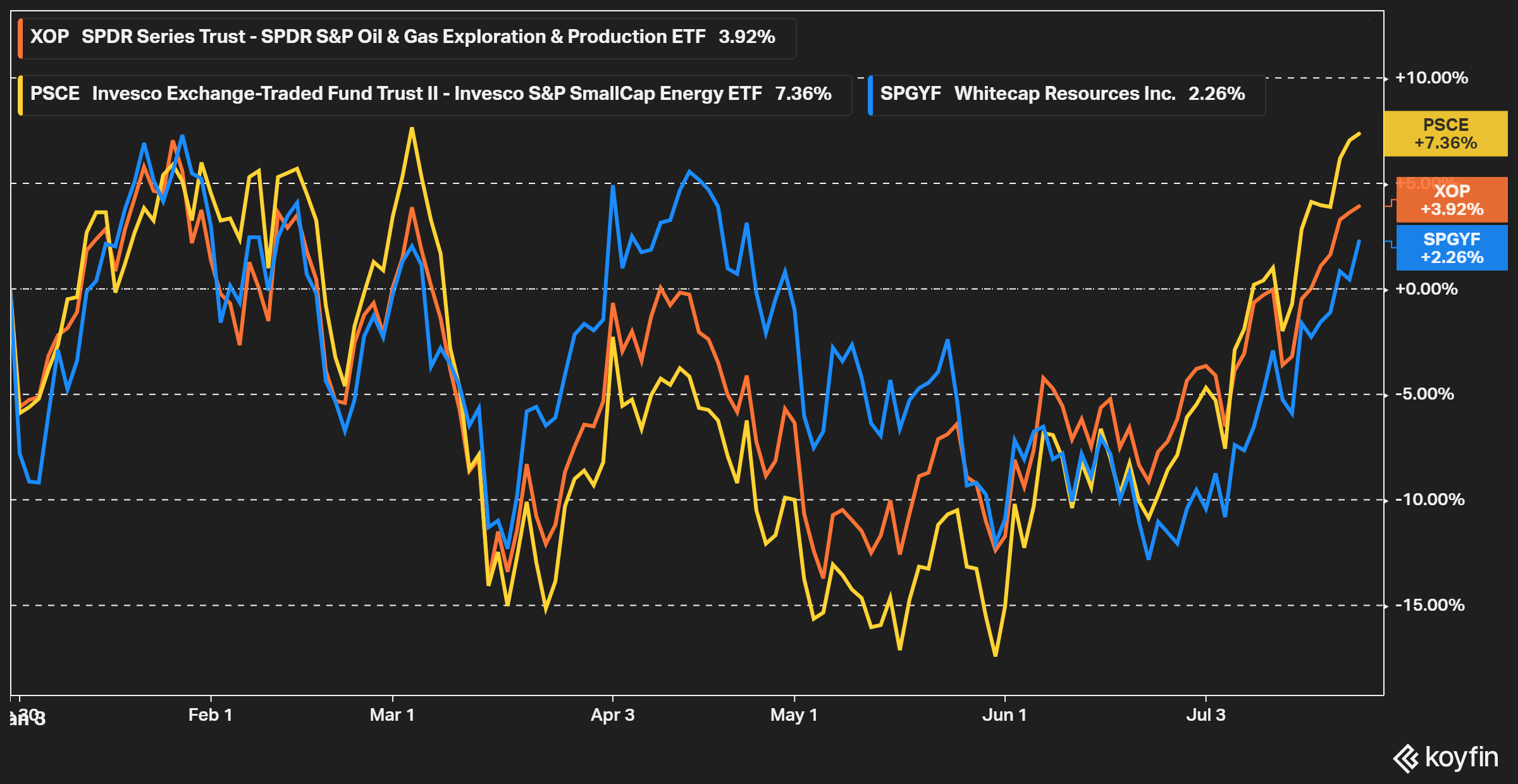

The stock price of Whitecap is up 16% in U.S. Dollars over the last year, but it has been relatively weak in 2023, with a marginally positive return of 2% YTD, slightly underperforming some industry ETFs.

Figure 1 - Source: Koyfin

Part of the reason for the weakness is likely related to the wildfires in Canada during Q2, which forced Whitecap and several other Canadian oil & natural gas producers in the region to curtail production for a while.

However, the overall impact on the annual production appears to be relatively small. Whitecap has revised the annual production guidance down from 161,000 boe/d to now 158,000 boe/d, which is only a 2% decrease. The production in Q4-23 is still expected to be around 170,000 boe/d, so there doesn't appear to be any impact on the near-term growth.

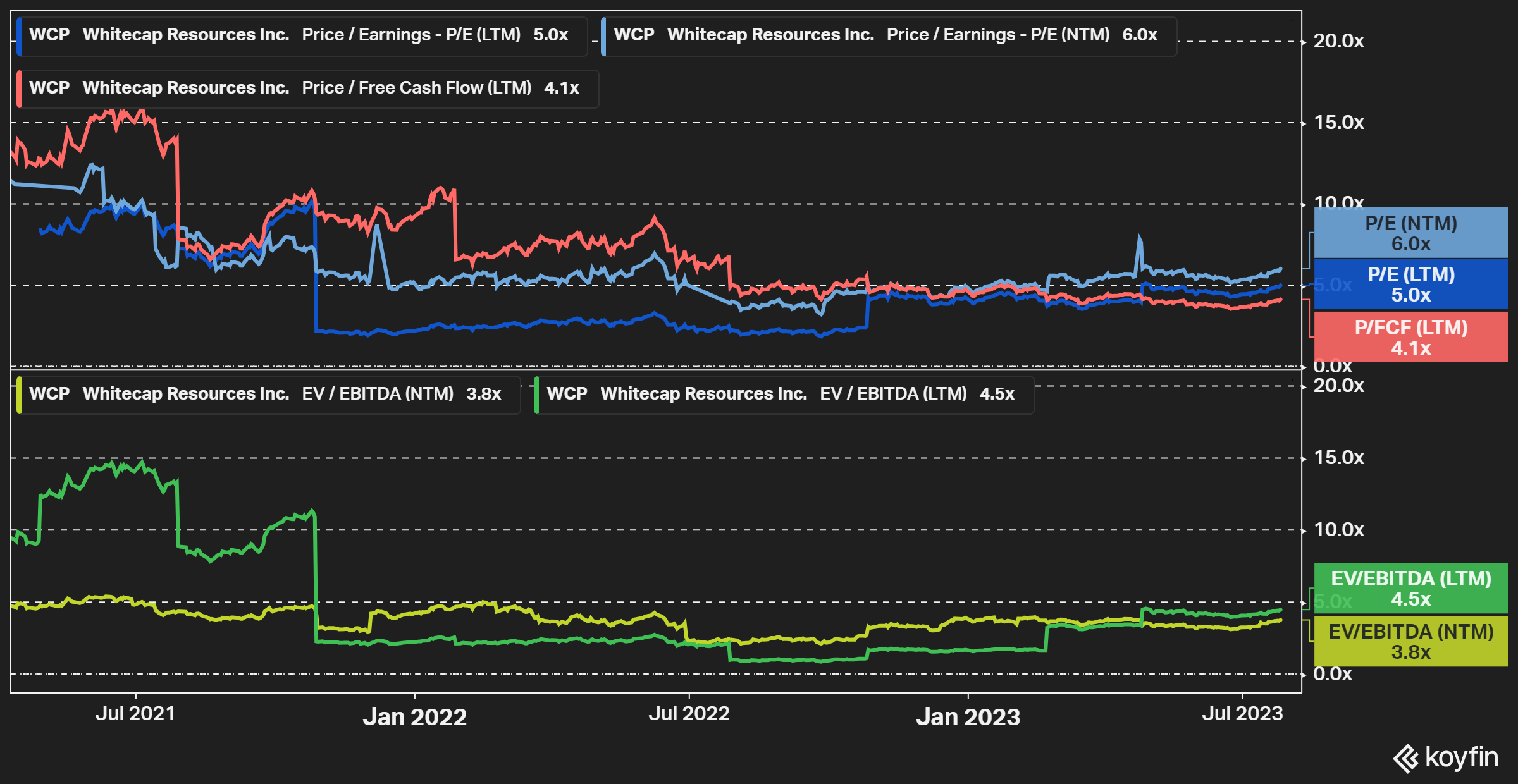

Figure 2 - Source: Koyfin

Whitecap continues to trade with very attractive valuation multiples, whether we look at historical or forward-looking numbers, and the company has much of its revenue coming from liquids even if a decent part of production comes from natural gas. The weaker natural gas prices have likely had some impact on Whitecap's YTD performance as well.

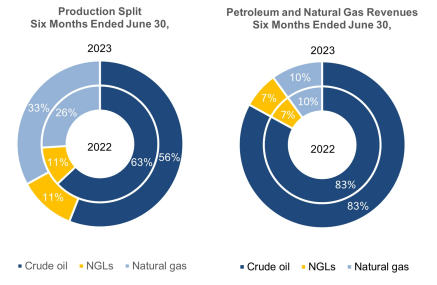

Figure 3 - Source: Whitecap Q2-23 MDA

I continue to believe Whitecap is one of the more compelling investments in the industry, where the company is expected to confirm a dividend increase to C$0.73 per year later this quarter. That translates to a dividend yield of 7.0% using the latest share price, with monthly distributions.

Q2-23 Result

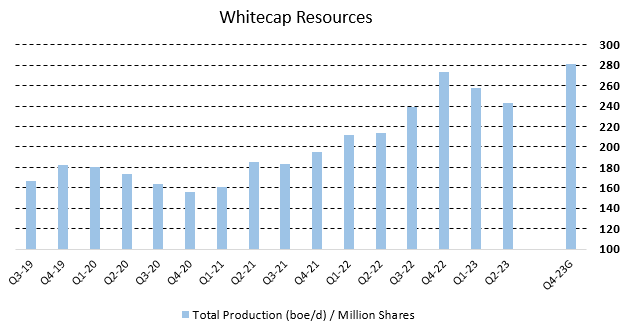

Production in the quarter was 147,166 boe/d, which is below the full year guidance and a decline compared to Q1-23. This was as mentioned earlier, primarily related to the wildfires during the quarter. If we include the Q4-23 production guidance and look at production per shares outstanding, we are still looking at a very constructive chart of production per share over time, even if Whitecap will need to deliver operationally in H2-23 to confirm this growth trend.

Figure 4 - Source: Whitecap Quarterly Results

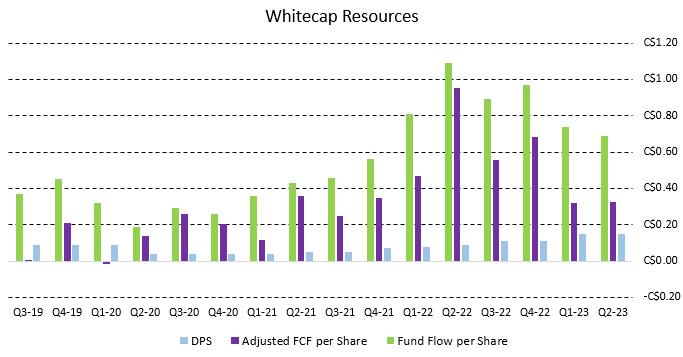

Whitecap did in the most recent quarter report C$415M in funds flow and C$197M in free cash flow, which comes to C$0.69 funds flow per share and C$0.33 free cash flow per share. While the company has seen a decline in cash flows over the last year due to lower commodity prices, the numbers are still respectable, and likely to improve going forward with a higher production volume. The dividend remains well covered.

Figure 5 - Source: Whitecap Quarterly Results

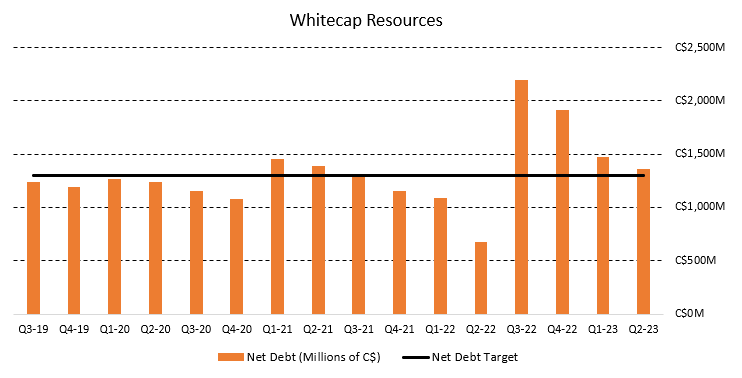

The net debt was at the end of Q2-23 at C$1,361M, very close to the C$1.3B net debt target. So, the company should not need many more months to reach this target. At which point we are looking at a higher base dividend and 75% of free cash flow to be distributed to shareholders via dividends & buybacks. With that said, the reassessment from the Canadian Revenues Agency could possible cause this increase to be delayed by a couple of months if Whitecap is required to pay 50% of reassessed taxes, interest, and penalties later in Q3.

Figure 6 - Source: Whitecap Quarterly Results

The costs have been well contained in the quarter, where most costs were relatively flat compared to both last quarter and the same quarter last year. There were a couple of exceptions, royalties are down substantially compared to this quarter last year, due to lower commodity prices. This quarter, Whitecap also had a small hedging gain, while there was a rather significant hedging loss in Q2 last year.

The very healthy operating netback of C$34/boe illustrates the low operating costs for Whitecap.

Figure 7 - Source: Whitecap Quarterly Results

Valuation & Conclusion

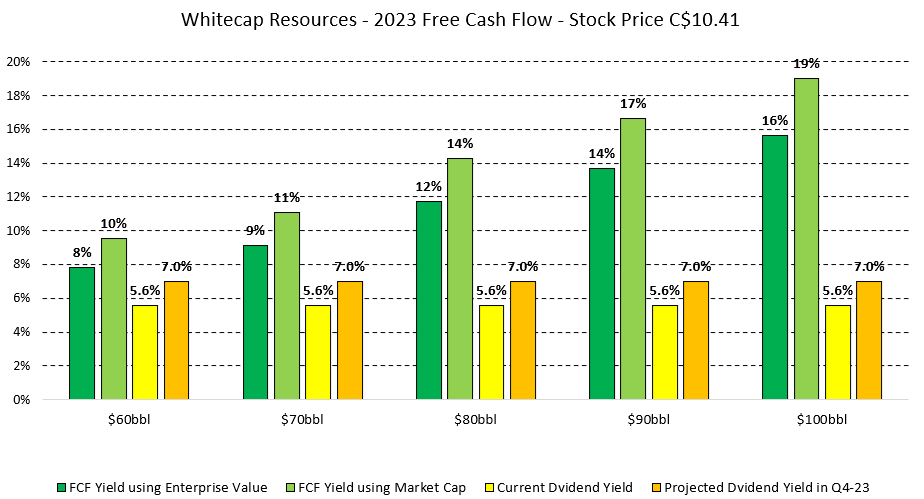

The below chart illustrates the company's free cash flow estimates for 2023 in a few different WTI price scenarios for the rest of the year. Where the company is currently trading with a free cash flow yield of around 12-14%, depending on whether we look at the market cap or enterprise value. The relatively secure dividend at lower commodity prices is another very positive feature of Whitecap.

Figure 8 - Source: Company's FCF Estimates for 2023

The valuation for 2024 is likely to be even better as well, primarily due to a couple of factors.

- The Q4-23 production guidance is 7.6% above the annual guidance of 2023. So, if that production or possibly slightly higher continues into 2024, it has the potential to boost cash flows significantly compared to 2023.

- The company is also expected to buy back shares and deleverage further during the back half of 2023, which will in 2024 mean a lower number in the denominator for the free cash flow yield.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you like this article and are interested in more frequent analysis of my holding companies, real-time notifications on portfolio changes, together with macro and industry analysis. I would encourage you to have a look at my investing group, Off The Beaten Path.

I primarily invest in turnarounds in natural resource industries, where I have a typical holding period of 1-3 years. Focusing on value offers good downside protection and can still provide great upside participation.

This article was written by

I enjoy my anonymity, which I think is underappreciated in today's world, where I write under the name Bang For The Buck. I hold a BSc and MSc in Financial Economics and I have extensive experience with the investment management industry. I am the CEO of a small investment company. I primarily focus on turnaround stories, with attractive valuations, in cyclical industries.

Presently, I am very focused on the precious metals industry due to current monetary and fiscal policies. I am also invested in the uranium and oil & gas industries, due to underinvestments together with very attractive valuations.

I publish regular articles on Seeking Alpha and offer an investing group service called Off The Beaten Path where subscribers receives real-time updates on the portfolio, in-depth portfolio reports, and frequent updates on holdings companies. As the name suggest, I primarily invest in industries and companies that are underappreciated, which I have found provides more attractive returns.

I am always happy to respond to comments and questions in my articles during the first few days. More in-depth and ongoing discussions are had inside Off The Beaten Path.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of WCP:CA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.