Noble Corporation: Not Enough Upside

Summary

- Noble Corporation, an offshore drilling contractor, is benefiting from major industry tailwinds, and its share price has recently rallied.

- Noble has performed well and announced significant shareholder distributions including $400 million of share buybacks and a $1.2 per share dividend.

- However, given the current valuation, we prefer other names in the sector, and issue a Hold rating.

TebNad

We have so far published notes with a Buy rating on Seadrill (SDRL) and Valaris (VAL) highlighting the robust market fundamentals of offshore drilling contractors, upcoming earnings inflections, attractive valuations, and potential catalysts. We now present our thoughts on Noble Corporation (NYSE:NE).

Introduction to Noble Corporation

Noble Corporation is an offshore drilling contractor providing services to the oil and gas industry. Noble Drilling Corporation was spun off in 1985 from Noble Affiliates Inc., a Texas-based hydrocarbon exploration company. It is headquartered in London, with the main operational office in Sugar Land, Texas, and listed on NYSE.

Following a considerable downturn in the energy sector, which was accelerated by the Covid-19 pandemic, like many of its peers, Noble filed for bankruptcy in July 2020, eliminating all of the company’s $3.4 billion bond debt. In February 2021, Noble emerged from bankruptcy, with a new capital structure, a strong financial foundation, $600 million of liquidity, $400 million of debt, and a young high-spec fleet.

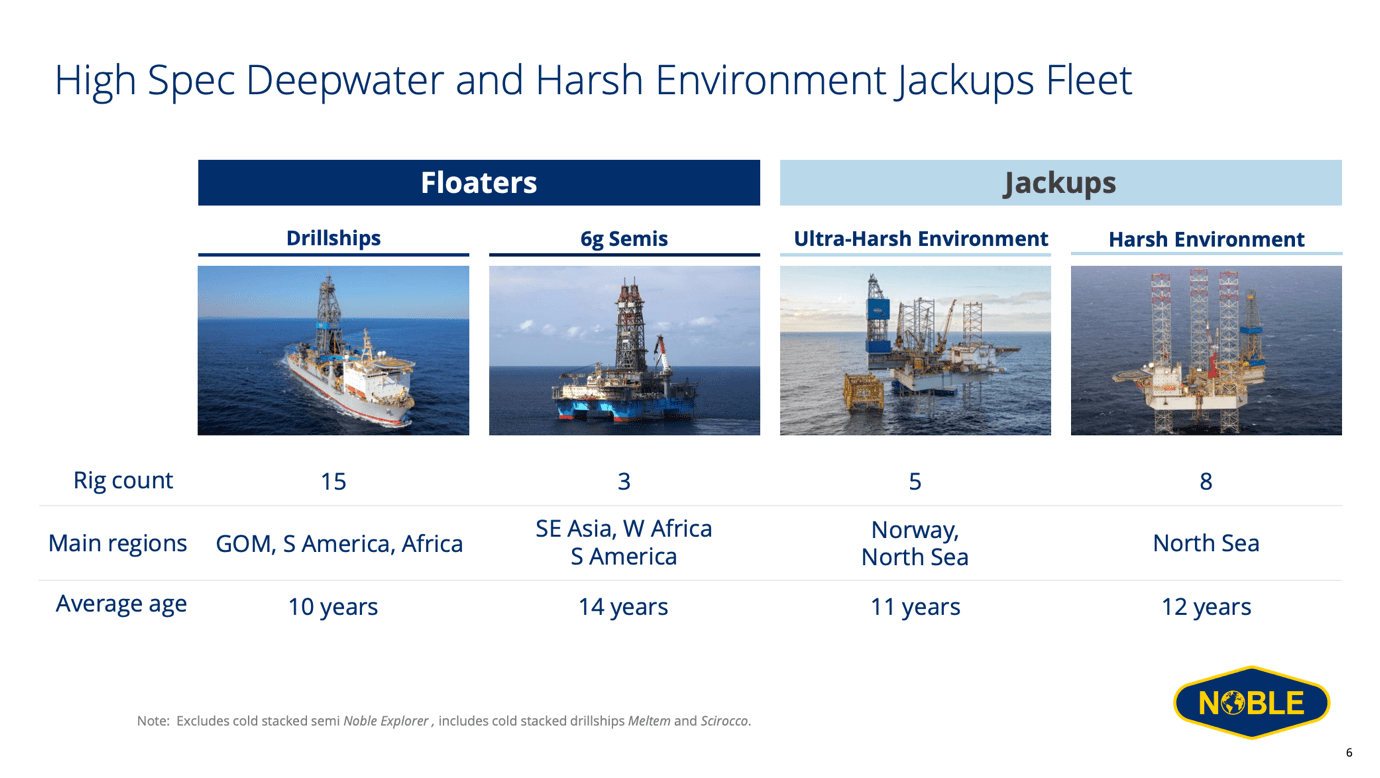

In the 2010s decade, Noble significantly upgraded its fleet, adding multiple high-specification assets and developing strategic alternatives for many existing older assets. Noble presently has a fleet of 31 rigs across Floaters and Jackups consisting of 15 Drillships with an average age of 10 years, 3 6th Generation Semisubmersibles with an average age of 14 years, 5 Ultra-Harsh Environment Jackups with an average age of 11 years, and 8 Harsh Environment Jackups with an average age of 12 years. Noble has scale in its key geographic regions, services key offshore basins, and has strong long-term customer relationships with oil majors and independents alike. We would like to point out Noble’s $4.6 billion backlog which offers significant earnings visibility.

Over the last 2 years, Noble has completed major M&A deals, acquiring Pacific Drilling in an all-stock transaction in March 2021, and merging with Maersk Drilling in October 2022 creating a leading player with one of the youngest and highest spec fleets in the industry. By Q4 2024, Noble expects to realize $125 million in annual synergies, out of which $60 million has already been realized. The synergies will be achieved through SG&A rationalization, operations optimizations, logistics and supply chain savings, and capex efficiencies.

Noble Corporation's Investor Presentation

Market Fundamentals

Market fundamentals have been thoroughly discussed in our note on Seadrill and expanded on our note on Valaris. We would highly recommend readers to have a look at our previous notes. However, we would like to stress a couple of points.

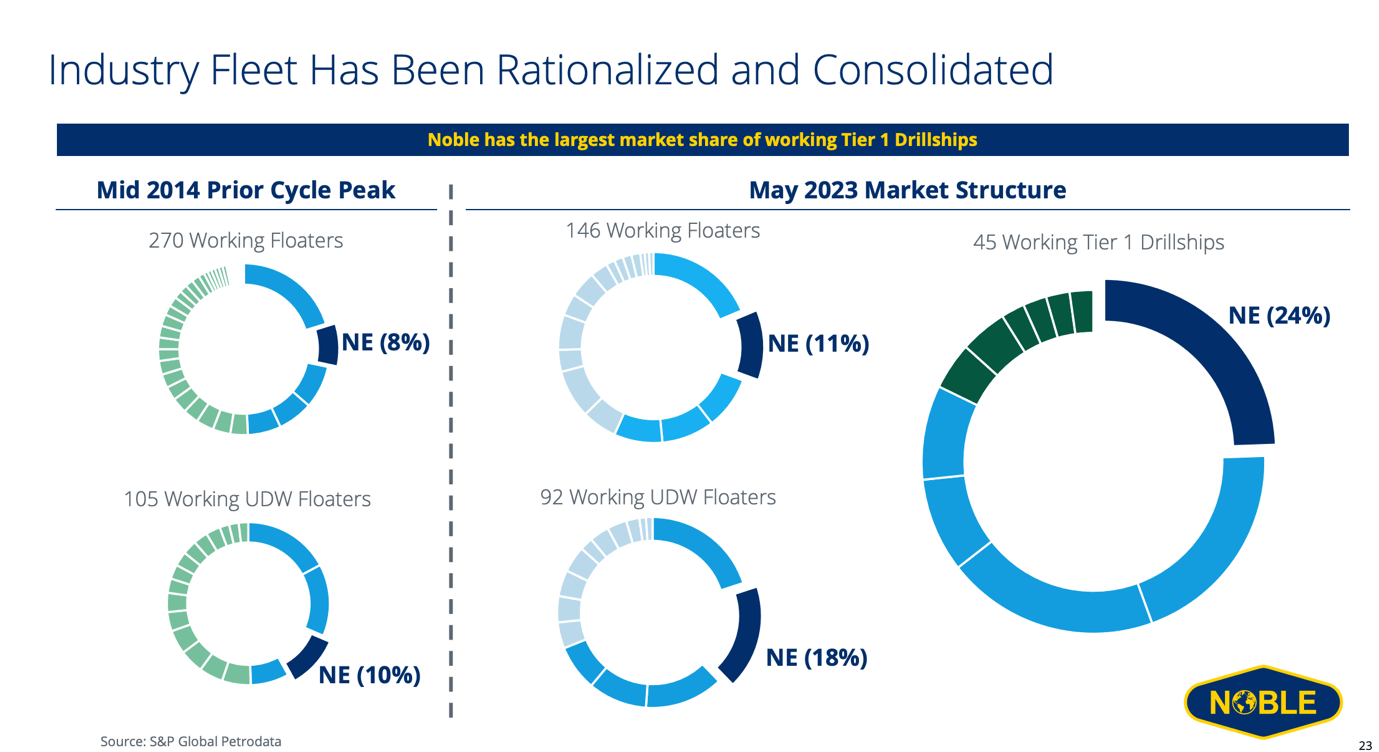

Offshore is emerging from a decade of underinvestment and is forecasted to ramp significantly. Ultra-deep water has advantaged breakeven cost and emissions profiles, and this is favorable for Noble particularly. After a prolonged downcycle the industry fleet has been rationalized and consolidated, and now Noble has the largest market share, ca. 24% of working Tier-1 Drillships.

Noble Corporation's Investor Presentation

Investment Case and Valuation

As was the case with Seadrill and Valaris, our investment case on Noble does not solely rely on what seems to be the beginning of a multi-year upcycle and expectations of further day-rate increases, as Noble is quite appealing even at current day-rates. Unlike most other drillers, Noble has not missed out too much on the daytime improvements and maintains a high utilization rate. Moreover, it leads the sector in terms of capital returns with $400 million of share buybacks.

We forecast $800 million of EBITDA in FY2023. The company has guided to an EBITDA range of $725 million to $825 million, while the sell-side consensus is around $850 million. With a market capitalization of $7.0 billion, a net debt position of $334 million, and an enterprise value of ca. $7.3 billion, Valaris is trading at c.9x EBITDA. We forecast $1.2 billion of EBITDA in 2024 and $1.8 billion in 2025. Valaris is respectively trading at 6x EBITDA’24e and 4x EBITDA’25e. Our forecasts reflect the latest contract awarded to Noble, most notably the extension with ExxonMobil in Guyana for its 7G Drillships, the 650 days rig-sharing agreement in Malaysia, the Petronas contract in Suriname, etc.

We value Noble at 5x EBITDA 2025, arriving at an EV of $9 billion in 2025. We discount this back to the present at a cost of capital of 10% (based on a 3.8% Risk-Free Rate, 1.1 Beta – Damodaran estimate for oil and gas services and equipment, and 5.9% Equity Risk Premium) and get an enterprise value of $7.8 billion, a market capitalization of $7.5 billion and a share price of $55 / share, or 8% upside. Valuing the company at 6x EBITDA’25e and discounting back would imply 28% upside or a share price of $65 / share. We believe other names in the off-shore drilling sector, such as Valaris and Seadrill, are more currently attractive and offer more upside for investors.

Capital Returns

Noble aims to return at least 50% of free cash flow to shareholders. Noble has been able to benefit earlier than most peers from the rise in dayrates, and this has also been reflected in terms of capital returns with $400 million of buybacks announced in November 2022, and the initiation of a quarterly dividend of $0.30, payable on September 14, 2023, to shareholders of record at the close of business on August 17, 2023. On an annualized basis this represents a dividend of $1.20 and a dividend yield of 2.3%.

Risks

Risks include but are not limited to a decline in crude oil prices, an increase in newbuilds leading to excess supply and deterioration of market fundamentals, inability to realize synergies from the Maersk Drilling merger, value destructive M&A resulting in an increase in net leverage, technological improvements in shale, changes in drilling technology and customer demand for upgraded technology, accidents, and weather events.

Investment Verdict: Hold

Noble shares have risen by 40% just over the last month, 64% year-to-date and 350% since IPO reflecting the excellent outlook for the sector and the company. However, we believe that at these share price levels, there is little upside left, and we prefer other names in the sector, hence we issue a Hold rating on Noble Corporation shares.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.