PTF: Technology Dashboard For July

Summary

- Technology is the most overvalued sector regarding my metrics.

- Semiconductors and electronic equipment have the less concerning value and quality scores among subsectors.

- PTF: a technology ETF for swing traders.

- 8 stocks cheaper than their peers in July.

- Quantitative Risk & Value members get exclusive access to our real-world portfolio. See all our investments here »

SweetBunFactory

This monthly article series shows a dashboard with aggregate industry metrics in technology and communication services. It may also serve as a top-down analysis of sector ETFs like Vanguard Information Technology Index ETF (VGT), Technology Select Sector SPDR ETF (XLK) and iShares U.S. Technology ETF (IYW), whose largest holdings are used to calculate these metrics. This month’s article will focus on Invesco DWA Technology Momentum ETF (NASDAQ:PTF).

Shortcut

The next two paragraphs in italic describe the dashboard methodology. They are necessary for new readers to understand the metrics. If you are used to this series or if you are short of time, you can skip them and go to the charts.

Base Metrics

I calculate the median value of five fundamental ratios for each industry: Earnings Yield ("EY"), Sales Yield ("SY"), Free Cash Flow Yield ("FY"), Return on Equity ("ROE"), Gross Margin ("GM"). The reference universe includes large companies in the U.S. stock market. The five base metrics are calculated on trailing 12 months. For all of them, higher is better. EY, SY and FY are medians of the inverse of Price/Earnings, Price/Sales and Price/Free Cash Flow. They are better for statistical studies than price-to-something ratios, which are unusable or non available when the "something" is close to zero or negative (for example, companies with negative earnings). I also look at two momentum metrics for each group: the median monthly return (RetM) and the median annual return (RetY).

I prefer medians to averages because a median splits a set in a good half and a bad half. A capital-weighted average is skewed by extreme values and the largest companies. My metrics are designed for stock-picking rather than index investing.

Value and Quality Scores

I calculate historical baselines for all metrics. They are noted respectively EYh, SYh, FYh, ROEh, GMh, and they are calculated as the averages on a look-back period of 11 years. For example, the value of EYh for hardware in the table below is the 11-year average of the median Earnings Yield in hardware companies.

The Value Score ("VS") is defined as the average difference in % between the three valuation ratios (EY, SY, FY) and their baselines (EYh, SYh, FYh). The same way, the Quality Score ("QS") is the average difference between the two quality ratios (ROE, GM) and their baselines (ROEh, GMh).

The scores are in percentage points. VS may be interpreted as the percentage of undervaluation or overvaluation relative to the baseline (positive is good, negative is bad). This interpretation must be taken with caution: the baseline is an arbitrary reference, not a supposed fair value. The formula assumes that the three valuation metrics are of equal importance.

Current Data

The next table shows the metrics and scores as of last week's closing. Columns stand for all the data named and defined above.

VS | QS | EY | SY | FY | ROE | GM | EYh | SYh | FYh | ROEh | GMh | RetM | RetY | |

Hardware | 2.73 | -42.22 | 0.0408 | 1.1795 | 0.0264 | 2.11 | 35.00 | 0.0354 | 0.9612 | 0.0376 | 6.74 | 41.51 | 6.15% | 32.91% |

Comm. Equip. | -24.17 | 9.06 | 0.0289 | 0.2671 | 0.0147 | 19.60 | 60.13 | 0.0311 | 0.2749 | 0.0393 | 15.95 | 63.17 | -0.23% | 6.55% |

Electronic Equip. | -9.78 | 5.19 | 0.0456 | 0.6104 | 0.0322 | 17.17 | 28.33 | 0.0414 | 0.7767 | 0.0393 | 13.10 | 35.70 | 1.70% | 26.32% |

Software | -30.14 | -6.95 | 0.0198 | 0.1109 | 0.0234 | 16.16 | 81.79 | 0.0259 | 0.1659 | 0.0353 | 17.78 | 85.89 | 3.08% | 11.17% |

Semiconductors | -14.05 | 13.40 | 0.0451 | 0.1876 | 0.0269 | 31.10 | 60.58 | 0.0452 | 0.2376 | 0.0340 | 24.00 | 62.32 | 1.64% | 38.26% |

IT Services | -32.57 | 6.98 | 0.0280 | 0.1880 | 0.0221 | 29.37 | 56.61 | 0.0376 | 0.3176 | 0.0322 | 26.41 | 55.08 | 2.30% | 11.88% |

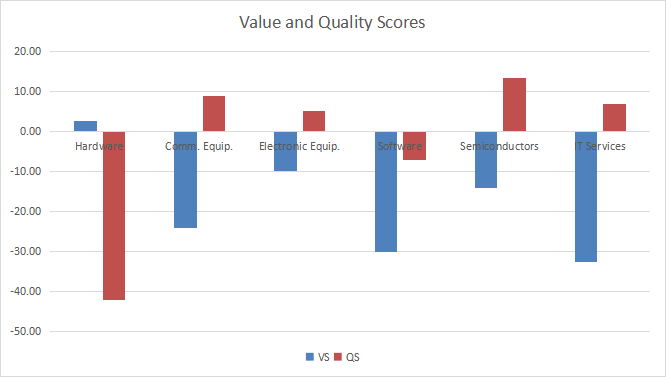

Value And Quality Chart

The next chart plots the Value and Quality Scores by industries (higher is better).

Value and quality in technology (Chart: author; data: Portfolio123)

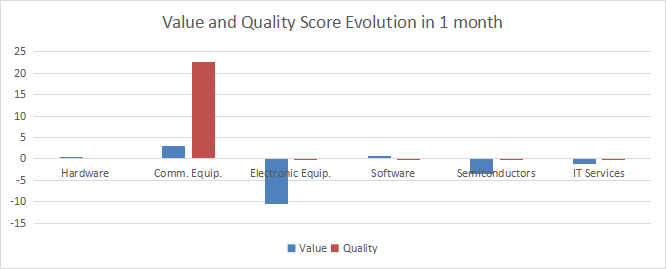

Evolution Since Last Month

Quality has improved in communication equipment and valuation has deteriorated in electronic equipment.

Score variations (Chart: author; data: Portfolio123)

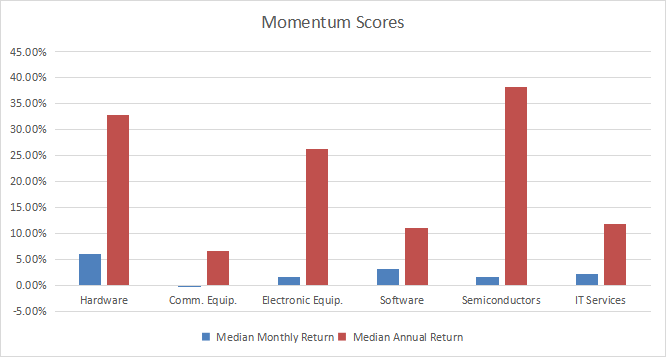

Momentum

The next chart plots momentum scores based on median returns.

Momentum in technology (Chart: author; data: Portfolio123)

Interpretation

As reported in my S&P 500 monthly dashboard, technology is the most overvalued sector. Electronic equipment and semiconductors are overvalued by less than 15% relative to 11-year averages, and good quality scores may partly justify it. Hardware is close to its historical baseline in value, but its quality score is far in negative territory. Software and IT services are the most overvalued tech industries.

Focus on PTF

The Invesco DWA Technology Momentum ETF (PTF) started investing operations on 10/12/2006 and tracks the Dorsey Wright Technology Technical Leaders Index. It has 36 holdings and a net expense ratio of 0.60%. Capital-weighted sector ETFs like VGT and XLK have much cheaper management fees (0.10%). The underlying index selects and weighs constituents using a score based on price relative strength, and it is rebalanced quarterly. The aggregate weight of the five largest holdings is capped at 25%.

The fund is mostly invested in two industries: software and semiconductors (55% and 24% of asset value, respectively). The portfolio is quite concentrated: the top 10 holdings, listed below with fundamental ratios, weigh 42.4% in aggregate.

Ticker | Name | Weight% | EPS growth %TTM | P/E TTM | P/E fwd | Yield% |

Apple, Inc. | 6.00 | -4.33 | 32.40 | 31.82 | 0.50 | |

Super Micro Computer, Inc. | 5.82 | 208.71 | 27.84 | 26.65 | 0 | |

Marathon Digital Holdings, Inc. | 4.85 | -316.72 | N/A | 144.48 | 0 | |

Cadence Design Systems, Inc. | 4.48 | 16.62 | 77.09 | 47.87 | 0 | |

Axcelis Technologies, Inc. | 4.07 | 55.90 | 31.74 | 27.55 | 0 | |

NVIDIA Corp. | 3.97 | -48.36 | 236.31 | 57.97 | 0.04 | |

Rambus, Inc. | 3.57 | 217.32 | 125.52 | 34.96 | 0 | |

Fortinet, Inc. | 3.24 | 58.32 | 65.08 | 53.91 | 0 | |

Synopsys, Inc. | 3.22 | -7.78 | 76.59 | 41.90 | 0 | |

AppLovin Corp. | 3.18 | -16.34 | N/A | 86.04 | 0 |

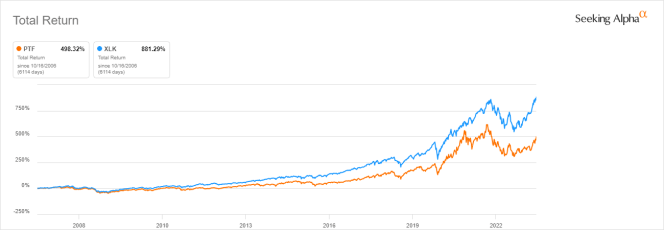

The next chart shows that performance since inception is underwhelming. PTF has lagged XLK by over 3% in annualized return.

PTF vs XLK since October 2006 (Seeking Alpha)

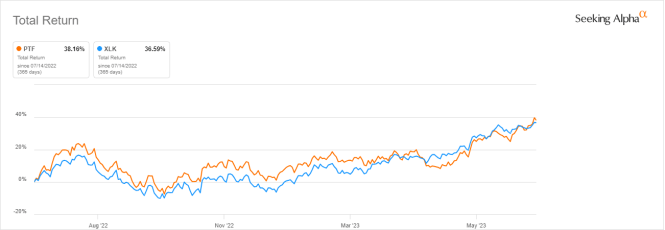

Nonetheless, the two funds are almost on par in the last 12 months (see next chart).

PTF vs. XLK, last 12 months (Seeking Alpha)

My opinion is that PTF is more valuable as a swing-trading instrument than as a long-term investment.

Dashboard List

I use the first table to calculate value and quality scores. It may also be used in a stock-picking process to check how companies stand among their peers. For example, the EY column tells us that a hardware company with an Earnings Yield above 0.0408 (or price/earnings below 24.51) is in the better half of the industry regarding this metric. A Dashboard List is sent every month to Quantitative Risk & Value subscribers with the most profitable companies standing in the better half among their peers regarding the three valuation metrics at the same time. The list below was sent to subscribers several weeks ago based on data available at this time.

Belden, Inc. | |

Jabil, Inc. | |

Veeco Instruments, Inc. | |

Diodes, Inc. | |

NXP Semiconductors NV | |

Progress Software Corp. | |

Gen Digital Inc. | |

InterDigital, Inc. |

It is a rotational list with a statistical bias toward excess returns on the long-term, not the result of an analysis of each stock.

Quantitative Risk & Value (QRV) features data-driven strategies in stocks and closed-end funds outperforming their benchmarks since inception. Get started with a two-week free trial now.

This article was written by

Step up your investing experience: try Quantitative Risk & Value for free now (limited offer).

I am an individual investor and an IT professional, not a finance professional. My writings are data analysis and opinions, not investment advice. They may contain inaccurate information, despite all the effort I put in them. Readers are responsible for all consequences of using information included in my work, and are encouraged to do their own research from various sources.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CDNS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.