NIO Delivers: Remains A Strong Buy Long-Term

Summary

- NIO's stock may have finally found a bottom, surging by about 60% off the $7 ultra-low achieved six weeks ago.

- However, despite NIO's considerable run-up, its stock remains dirt cheap.

- NIO's stock trades at about two times this year's revenue estimates and just 1.2 times 2024's projected sales.

- NIO should become increasingly profitable as its revenues continue increasing, enabling its multiple to expand in the coming years.

- NIO's stock should go much higher long term, making NIO a top buy-and-hold candidate for the next 5-10 years.

- This idea was discussed in more depth with members of my private investing community, The Financial Prophet. Learn More »

Andy Feng

NIO Inc.'s (NYSE:NIO) stock has skyrocketed by about 60% in six weeks. The company's stock price rebounded strongly off the extreme low around $7 as its sales in China's pure EV market bounced back last month. NIO's MoM sales surged by 74% in June due to the easing of COVID-19 restrictions, the introduction of new Models, and other constructive variables. Moreover, NIO's sales should continue surging in the second half, likely doubling its first-half delivery numbers.

China's massive pure EV market should continue expanding, and NIO's sales should increase dramatically as the company looks to ramp up production to 500,000 or 600,000 annual sales. Moreover, NIO has plans to export more budget EVs as it expands its operations to other areas of the world. NIO's revenues could be around $8.5-9B this year, and its market cap is only around $18B (roughly two times sales). NIO's revenues could expand rapidly in the coming quarters, leading to better-than-expected profitability and a significantly higher stock price in the coming years.

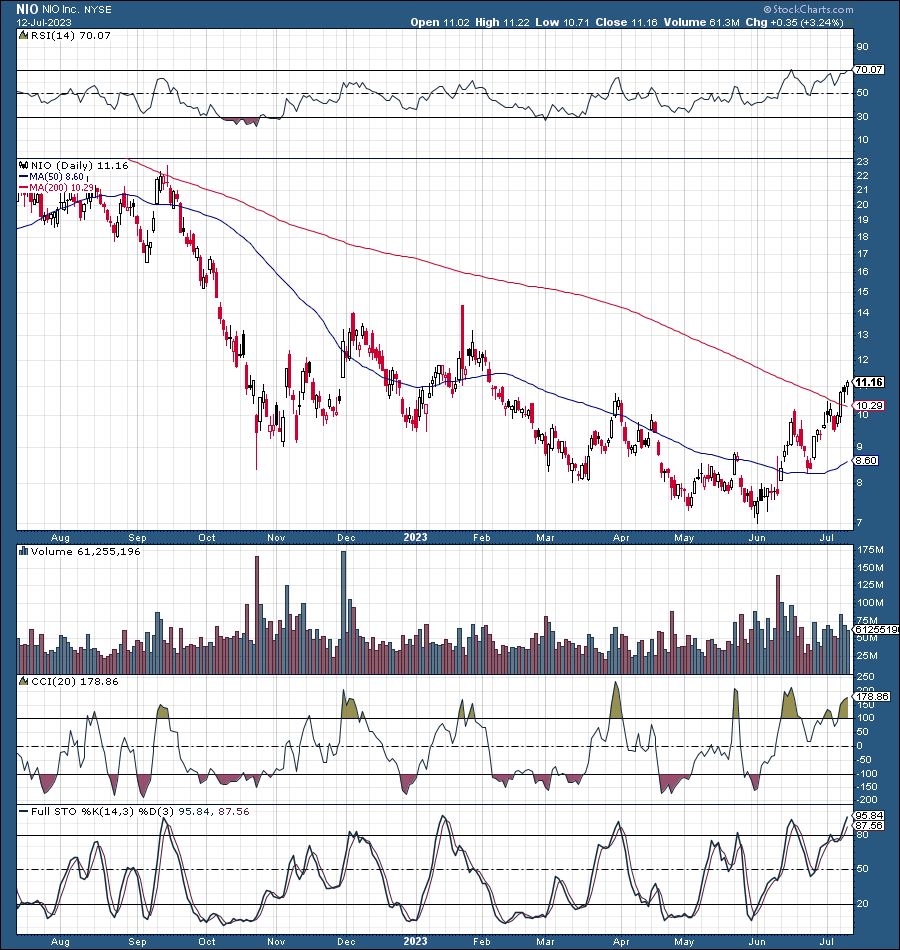

NIO's Technical Image Has Turned Bullish

NIO (StockCharts.com )

NIO's stock likely finally bottomed around the $7-8 range, and a constructive inverse head and shoulders pattern has materialized since then. Now we're seeing bullish higher highs and higher lows forming, and the 50-day MA looks poised to move above the 200-day MA soon (a bullish long-term technical indicator). Moreover, we see improvements in the RSI, CCI, full stochastic, and other technical gauges. Momentum is improving for NIO, and the stock could continue moving higher from here.

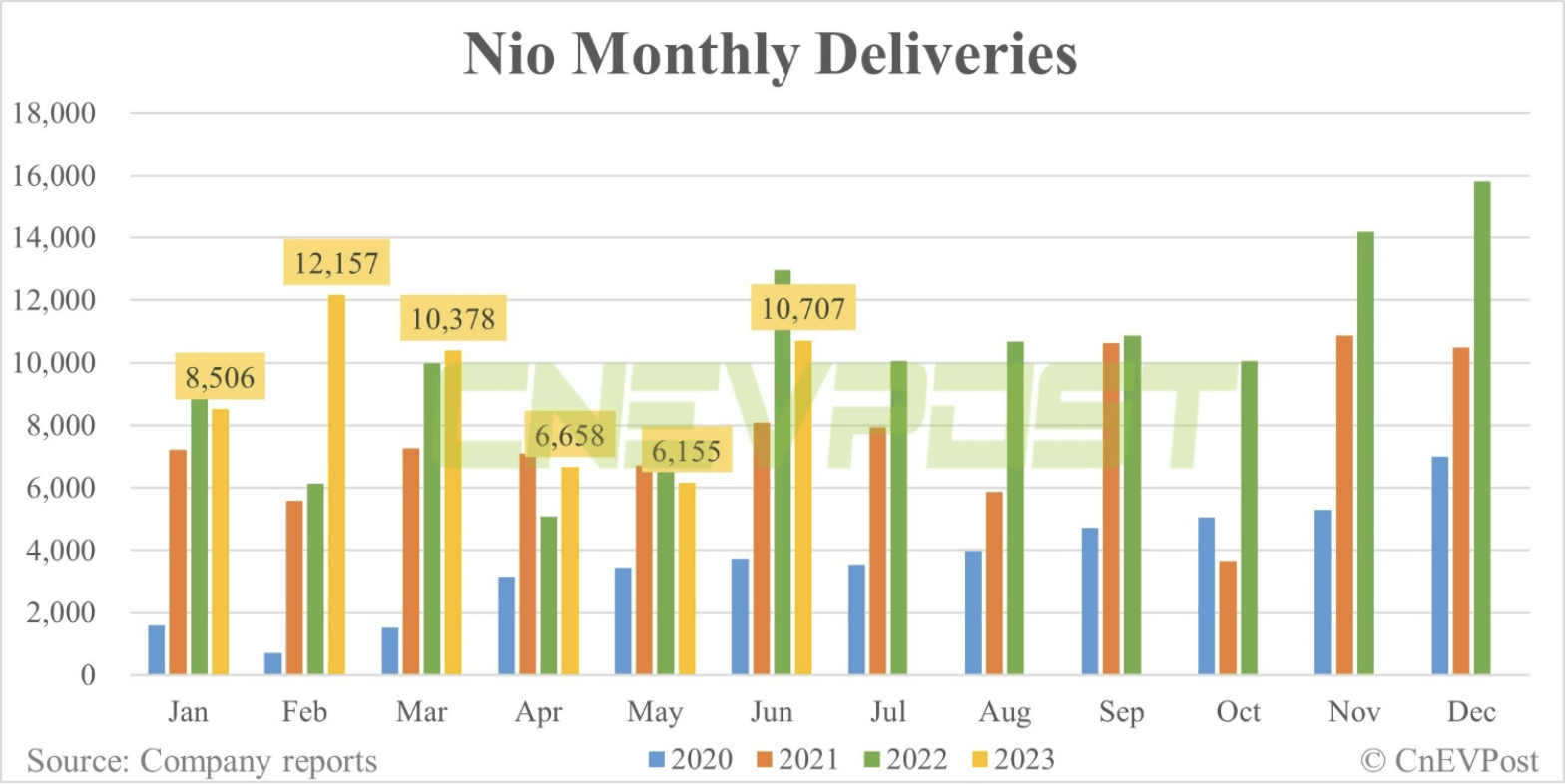

NIO Delivered More Than 54,000 Vehicles in H1

NIO delivered 54,561 vehicles in the first half of the year and should increase sales significantly in H2. NIO Q1 revenues came in at about $1.5B and should provide approximately $1.2-1.3B in sales for the second quarter. However, this quarter should be a significant low point for NIO as sales should increase to about $5.6B in the second half. That's a massive increase, and NIO's recent stock run-up illustrates that the market is behind the curve on NIO and could chase the stock higher as we advance.

NIO's H2 revenues of approximately $5.6B would be a staggering increase of around 100% from H1. Moreover, higher-end revenue estimates project NIO could deliver around $6.3B in revenues in this year's second half. Therefore, NIO's total 2023 revenues could come in around $9-10B (consensus estimate of $9.23B). NIO's market cap is only about $18B here, illustrating a relatively inexpensive two times this year's sales valuation in NIO's stock. Moreover, NIO could deliver revenues of about $15B next year, suggesting its stock is trading at about 1.2 forward sales here (dirt cheap).

Revenue Estimates - Excellent Growth Potential

NIO revenue estimates (SeekingAlpha.com)

The lifting of COVID-19 restrictions, production increases, and improved demand for new models should lead to substantial sales increases as NIO advances in future years. NIO's revenues could spike to around $20 billion or more in 2025, and its revenues should continue growing from there.

Why Did Q2 Sales Drop Off?

China's economy struggled with increased COVID-19 restrictions and a slowdown in its domestic economy in the second quarter. Moreover, Tesla's price cuts likely negatively impacted NIO's Q2 sales. Nevertheless, NIO's sales bounced back swiftly in June. Thus, the company's slowdown in sales should be transitory, and with the introduction of NIO's newest vehicles, we should see a robust rebound in the second half.

NIO's updated lineup includes the recently launched completely overhauled second-gen versions of its ES6 and ES8 SUVs. Also, NIO recently launched its ET5 sedan to compete with the Tesla Model 3. NIO's flagship ET7 sedan, aimed to compete with Tesla's Model S, went on sale last year. Additionally, NIO has several other SUV and crossover options that match up well with Tesla's Model X/Y vehicles. Therefore, NIO has an extensive lineup of excellent pure electric cars, and its sales could surge as we advance.

What Makes NIO Unique

Despite the presence of other major EV makers in China, NIO remains unique. BYD (OTCPK:BYDDF) is a significant auto player in China, but it is not a pure EV play. Moreover, many BYD vehicles are aimed at the lower/cheaper end of the market and may not directly compete with NIO. XPeng (XPEV) is an exciting company, but it focuses on several specific vehicles aimed at the simpler/cheaper end of the market. Tesla is the closest competitor to NIO in quality, luxury, performance, capabilities, range, and price. Moreover, if we look closely at NIO's updated lineup, it has cars that closely resemble and can adequately compete with Tesla's S/3/X/Y lineup of vehicles.

NIO Has the Home Field Advantage in China

I like Tesla, and the company has done an excellent job expanding operations in China. Tesla has massive sales in China (Nearly 78K vehicles in May). However, China has insatiable EV demand and has the most significant car market on earth (especially for EVs). Therefore, China is big enough for several key players, including Tesla, NIO, and others.

NIO sales monthly (cnevpost.com)

In comparison, NIO only delivered 6,155 vehicles in May (only 8% of Tesla sales). Yet, the company's sales bounced back sharply to more than 10.7K in June, roughly a 74% MoM increase. With NIO's new models and second-generation updates available, we should see its sales rise substantially in the second half of this year.

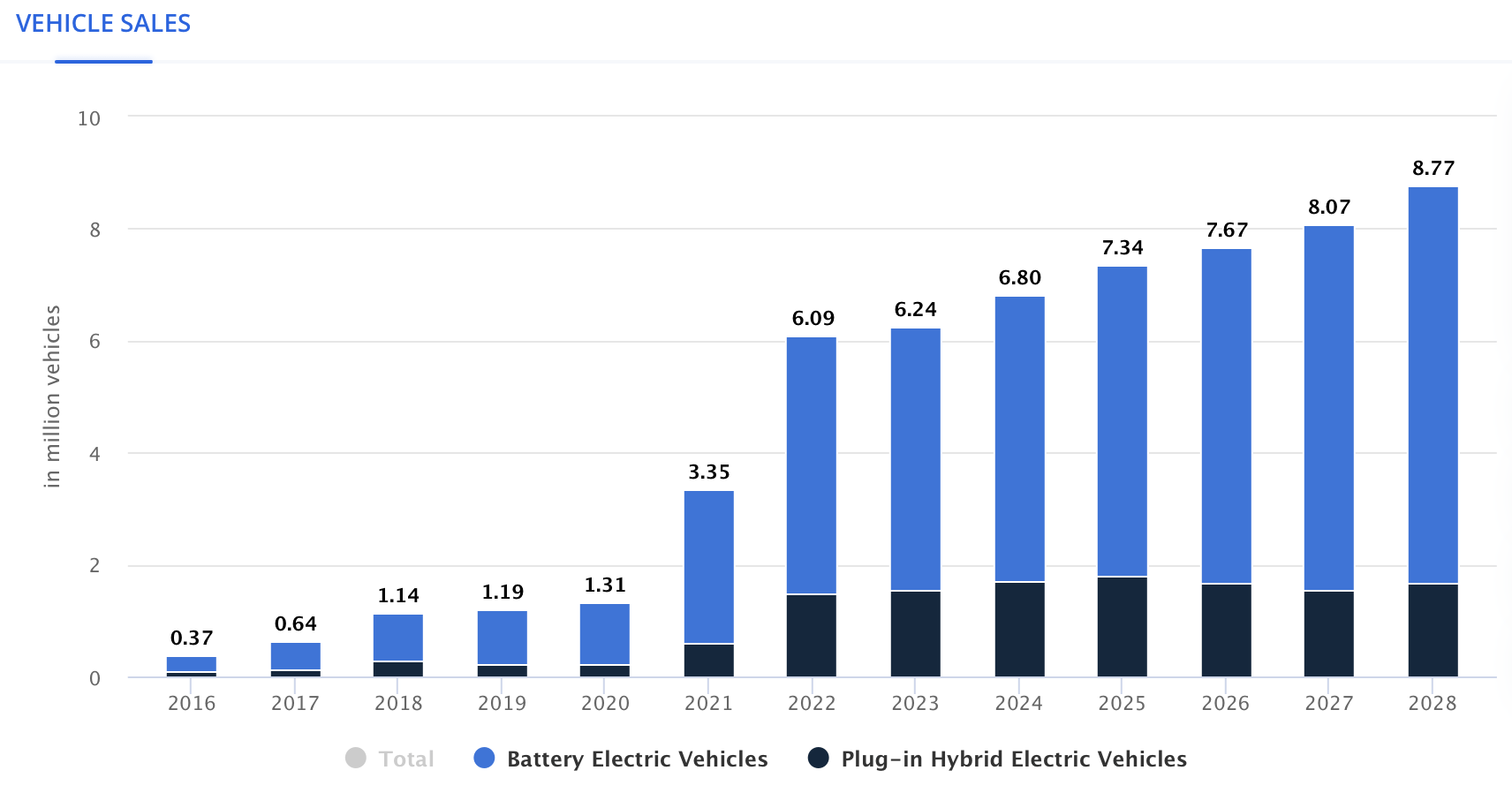

China's Staggering EV Demand

China EV growth (Statista.com)

Pure EV sales are exploding, especially in China. We see about 4.6 million pure EV sales in 2022, which could rise to around 7 million pure EV sales by 2028. NIO only delivered about 54K vehicles in the first half and could deliver about 100K in H2. Therefore, NIO's 2023 deliveries could account for only about 3.2% of China's total pure EV sales. However, NIO can produce 500-600K cars annually from its two plants (F1 and F2 NeoPark).

Therefore, NIO should do fine in scaling production to capture about a 10% market share. Annual sales of around 500,000-600,000 NIO vehicles should provide approximately $24-28B in revenues for NIO. Moreover, as demand increases to meet production capacity, NIO can increase production by opening another production facility and expanding its global network outside its homeland.

Furthermore, NIO has plans to build a new factory for "budget EVs" to transport to Europe and other areas. Therefore, NIO has substantial growth ahead and could achieve $24-28B in revenues around 2025 - 2026, enabling its stock price to move much higher from current levels.

Where NIO's stock price could be moving forward:

| Year | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 |

| Revenue | $10B | $15B | $20B | $26B | $33B | $40B |

| Revenue growth | 40% | 50% | 33% | 30% | 25% | 22% |

| Forward P/S ratio | 1.2 | 2.5 | 3.3 | 3.5 | 3.4 | 3.3 |

| Market cap | $18B | $50B | $86B | $116B | $136B | $160B |

| Stock price | $11 | $31 | $53 | $72 | $84 | $99 |

Source: The Financial Prophet

The Bottom Line: NIO to Go Higher Long Term

NIO should become increasingly profitable as revenues increase. Economies of scale should lead to improved production costs, enabling the company's multiple to expand in the coming years. NIO currently trades at a remarkably low 1.2 times forward sales estimates. Once NIO demonstrates it can ramp up production considerably without exhausting demand for its vehicles, its forward P/S multiple should expand to the 2.5-4 range or higher. As NIO's revenues increase, its multiple should expand. Therefore, NIO's stock price should go much higher in future years, making it a strong buy-and-hold candidate for the next 5-10 years.

NIO: Risks Exist

Despite my bullish outlook for NIO, it remains an elevated risk/reward investment. The most apparent risk factor is that NIO is a Chinese company. China may continue being an economic and geopolitical adversary to the U.S., dampening near and intermediate-term sentiment for Chinese stocks. Moreover, the primary reason why NIO trades at such a low P/S multiple is that it's a Chinese stock. If the "Chinese uncertainty" fades, we should see many quality Chinese stocks return to more compelling valuations. However, for now, NIO faces increased risk due to geopolitical tensions, competition, price cuts from EV giant Tesla, possible production and demand problems, and other variables. Please consider these and other risk factors before committing capital to an investment in NIO.

Are You Getting The Returns You Want?

- Invest alongside the Financial Prophet's All-Weather Portfolio (2022 17% return), and achieve optimal results in any market.

- Our Daily Prophet Report provides crucial information before the opening bell rings each morning.

- Implement our Covered Call Dividend Plan and earn an extra 40-60% on some of your investments.

All-Weather Portfolio vs. The S&P 500

Don't Wait! Unlock Your Own Financial Prophet!

Take advantage of the 2-week free trial and receive this limited-time 20% discount with your subscription. Sign up now, and start beating the market for less than $1 a day!

This article was written by

Hi, I'm Victor! It all goes back to looking at stock quotes in the old Wall St. Journal when I was a kid. What do these numbers mean, I thought? Fortunately, my uncle was a successful commodities trader on the NYMEX, and I got him to teach me how to invest. I bought my first actual stock in a company when I was 20, and the rest, as they say, is history. Over the years, some of my top investments include Apple, Tesla, Amazon, Netflix, Facebook, Google, Microsoft, Nike, JPMorgan, Bitcoin, and others.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of NIO, TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I am long a diversified portfolio with hedges.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.