Textainer Group Holdings: A Brilliant Management Driving Value For Shareholders

Summary

- Textainer Group Holdings Limited has seen a 157% increase in its stock value over the past five years, with a 48.45% increase in the past year due to strong management and strategic industry approach.

- Despite a challenging macroeconomic environment and falling demand, the company has maintained a high utilization rate of 98.8% and reduced interest expenses through deleveraging and strategic implementation.

- The company’s total shareholder return over the past three years is 425%, significantly higher than the sector’s return, and it has also returned capital to shareholders through share buybacks.

Fahroni

Investment Thesis

Textainer Group Holdings Limited (NYSE:TGH) holds and manages intermodal containers as its main business. Additionally, the organization is establishing a container resale business. The value of its stock has increased by almost 157% during the past five years. Despite the uncertainty and volatility in the business environment, the company has maintained its trajectory, as seen by a 48.45% increase in share price over the past year. Good management that is in tune with its industry and can swiftly respond to shifting conditions is to credit for these achievements.

Given the company’s strategic approach to the dynamic industry, I am confident it will overcome the current turbulence victorious. Further, the industry is entering the peak season, where I expect the company’s upward trajectory momentum to gain heat. As a result, I am bullish on this stock.

Company Overview

Through its subsidiaries, Textainer Group Holdings Limited acquires, manages, leases, and sells intermodal containers across the world. Its business is divided into three divisions: ownership, management, and resale of shipping containers.

The company’s container inventory features both general-purpose and specialist dry freight and refrigerated containers, as well as tank, 45', pallet-wide, and other specialty containers. It also helps both associated and unaffiliated container investors with management, purchase, and disposal services for their containers. Along with selling containers from its own fleet, the company also buys, leases, and resells containers from shipping companies, container brokers, and other sellers.

It manages a fleet of about 2.7 million containers, which is comparable to 4.4 million twenty-foot containers. The company’s main customers include shipping corporations, freight brokers, and the United States government.

Excellent Management: Adapting To The Volatile Environment

Large container ships are increasingly being used to transport both finished and intermediate commodities around the world, and this trend provides valuable insight into the state of the consumer market and the demand for manufactured goods. As the world’s container market adjusts to rates returning to pre-pandemic levels following the boom years of 2020 and 2021, it will face a number of challenges for the remainder of this year. As macroeconomic headwinds persist, liner businesses will face increasing difficulty deploying capacity in a market where demand is falling.

TGH management has taken a cautious but very strategic approach to weathering the storm as the industry shifts to adapt to weakening demand in a time when the macro environment is quite challenging. To begin with, the company has resulted to mute new container production and investment and instead resulted in higher utilization of their existing assets. In my view, this has helped the company save a lot of cash which would be otherwise deployed in new production amid cooling demand.

Secondly, given the cooling demand, the company leveraged its longstanding customer relationships to proactively renew the maturing leases. In my view, this move helped the company maintain the demand for its products as well as ensure steady cash flow in its business. To underscore this approach’s significance, Q1 lease rental income was $195 billion despite two fewer billing days in the quarter. It continues to display consistency, a monument to its utilization rate’s stability, which stands at an incredible 98.8%.

Olivier Ghesquiere,” Q1 lease rental income was $195 billion in spite of two fewer billing days in the quarter and continues to demonstrate stability a testament to the resilience of our utilization rate, which stands at an exceptional 98.8%. This in-turn can be attributed to the successful proactive renewal of maturing leases. Thanks to our strong, longstanding customer relationships. We continue to expect utilization to remain elevated for the duration of this year.”

Lastly, to cope with the rising interest rates challenge, the company mitigated increasing interest expenses through deleveraging and strategically implementing a long-term hedging strategy. As a result of these approaches, the company’s Q1’23 interest expenses of $42M reduced by $1M from Q4’22 expense.

Michael Chan,” Q1 interest expense of $42 million, decreased by 1 million from Q4 due to deleveraging and two fewer days. Average debt outstanding during Q1 reduced by $182 million from Q4.”

Peak Season Is Here: A Reason To Be Optimistic

Although some challenges affect this industry, the management is aware that the first quarter of the year is often a slow time. The term “peak shipping season” describes the year when the most cargo is being transported. Motor carriers are working harder than normal to get freight to their destinations on time as shippers struggle to meet demand and control inventory levels while completing a surge in orders.

The peak shipping season for intermodal logistics has traditionally been from June to December. While June may appear too early, many shippers are scrambling to get their goods through West Coast ports by June 30th, and rail is a common mode of transit for West Coast imports. According to the Alameda Corridor Transportation Authority, the number of products imported and subsequently loaded into intermodal equipment through Los Angeles and Long Beach ports has increased by 25% since 2006.

What Has Been There For Investors?

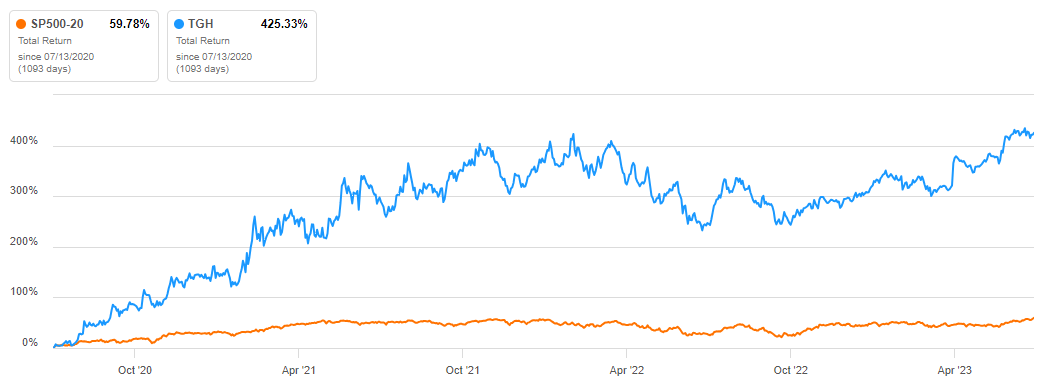

Current shareholders have a lot to be happy with regarding their investment in the company. Increasing price returns, higher total returns, and share repurchases are just some of the ways the corporation has rewarded its investors.

In terms of price return, the company has a three-year price return of 396.5%, which is pretty attractive, in my opinion. The company’s robust fundamentals have been the driving force behind its recent expansion, as evidenced by its 89% annualized EPS growth over the past three years. Let’s talk about the total shareholder return [TSR]. The TSR is a type of investment return that factors in the value of cash dividends and any discounted capital raise or spin-offs.

TGH’s TSR during the past three years is 425%, which is higher than the return on investment from its stock price. I attribute the discrepancy to the dividend payments. It is even more appealing to note that it exceeds the sector’s total return by a margin of about 366%

Seeking Alpha

In my opinion, this elevates the company’s standing in the eyes of investors looking for strong returns in the industrial sector. In addition to these pleasing returns. The company has also returned capital to shareholders through share buybacks, with 1.3m common shares repurchased in the MRQ. In my view, it demonstrates the management’s commitment to its shareholders.

Valuation

Based on relative valuation metrics, TGH is trading at an attractive value. With a PE ratio of 6.70x, about 66% lower than the industry median, and a PB ratio of 1x, about 62% lower than the industry medians, it is apparent this company is trading at a significant discount relative to the industry medians. Additionally, using an EPS-based DCF model with a forward EPS of 4.87, a discounting rate of 10.8%, and a growth rate of 5%, I estimate the company’s fair value to be about $49.24 with an upside potential of about 24%, further ascertaining that the company is undervalued.

Both the one-year momentum of 48.45% and the three-month momentum of 23.66% are considerably greater than the respective industry medians of 15.17% and 8.04%, suggesting that the company’s upward trajectory has not yet slowed. So, to take advantage of the company’s current momentum throughout this peak season and beyond, I recommend it to potential investors at a discount.

Risks

Just like any other investment, investing in TGH has its share of risks, as discussed below.

- Physical Asset Risk: TGH owns and leases out a large fleet of containers. The value of these assets can decline significantly over time due to wear and tear, accidents, or obsolescence. Maintenance and repair costs can also impact the profitability of the company.

- Currency Risk: Textainer operates internationally and earns revenues in multiple currencies. Fluctuations in exchange rates can impact the company’s revenues, costs, and profitability. Currency devaluations or sudden changes in exchange rates can lead to financial losses.

- Regulatory and Legal Risks: The company operates in various jurisdictions and is subject to compliance with local laws, tax regulations, and other legal requirements. Failure to comply with these regulations can result in fines, penalties, and reputational damage.

Conclusion

As a result of the company’s responsiveness to market uncertainty and the solid returns it provides to its shareholders, TGH is a solid investment. In light of the impending busy season, I recommend that investors buy low in order to benefit from the company’s upward trajectory both now and in the future; at the same time, they should keep a close check on the challenging business climate, which could threaten their investment.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This article was researched and written by January Mbuvi of Fade The Market.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.