Chatham Lodging Trust: The Preferred Shares Are Yielding 8.65%

Summary

- Chatham Lodging Trust is focusing on Extended Stay hotels.

- I expect a full-year AFFO of $1.15-1.20 per share.

- According to my calculations, an increase of the cost of debt to 8% would reduce the Chatham AFFO/share by less than $0.25.

- The dividend coverage ratio on the preferred shares is excellent, and I will likely initiate a position in the next few weeks.

- Looking for a helping hand in the market? Members of European Small-Cap Ideas get exclusive ideas and guidance to navigate any climate. Learn More »

kartouchken/iStock via Getty Images

Introduction

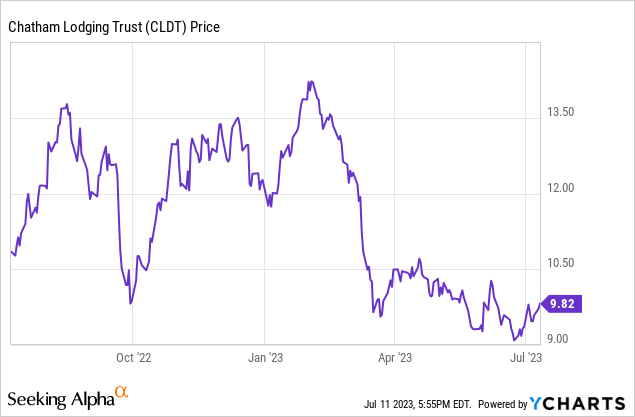

I have been keeping an eye on the preferred shares issued by some hotel real estate investment trusts ("REITs"). Although it is not my favorite sector to invest in, there are some interesting investment opportunities with a good risk/reward ratio out there. In this article, I wanted to have a closer look at Chatham Lodging Trust (NYSE:CLDT) before the REIT reports (expected pre-market August 2) on its Q2 results (the second and third quarter are usually the best quarters for this hotel REIT as travel numbers pick up in the summer months) to see if I should consider building a position in the common shares or the preferred shares.

Expect positive FFO and AFFO in Q1, and this should accelerate in the summer months

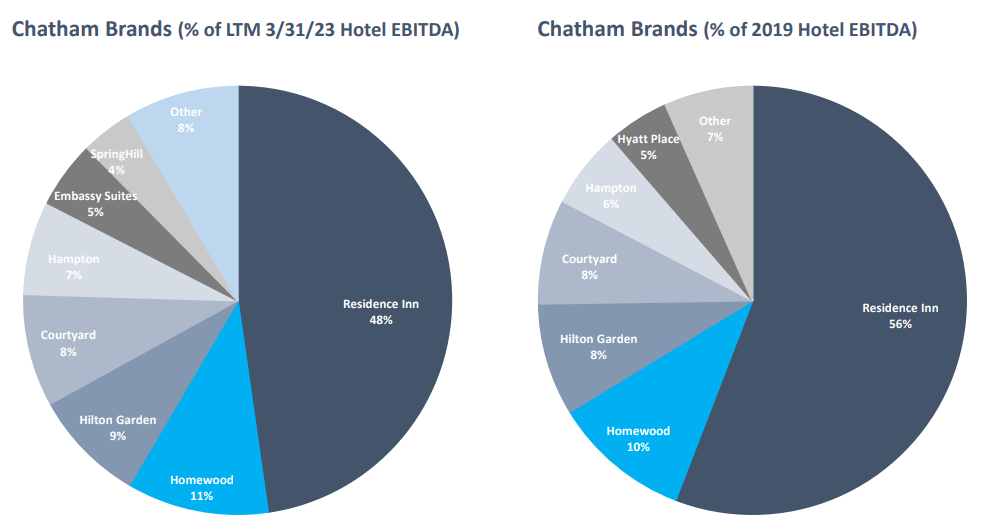

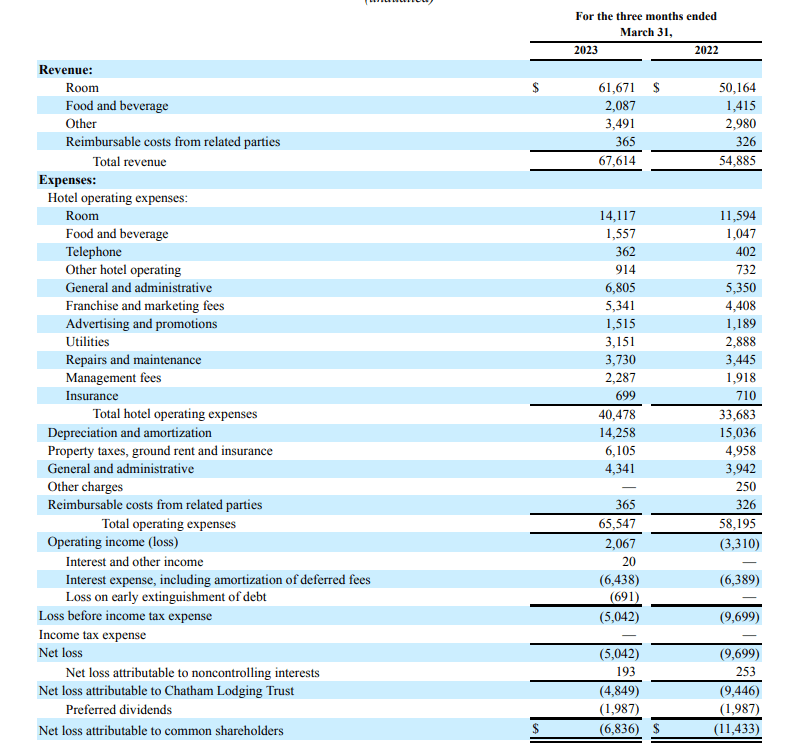

Before diving into the funds from operations ("FFO") and adjusted FFO ("AFFO") performance, I wanted to discuss the income statement first as it contains important pieces of information regarding the breakdown of operating expenses as well as the total interest expenses. The latter is obviously becoming a very important element in discussing the REIT sector these days, as most REITs are still going through the cycle of refinancings which is gradually increasing the average cost of debt. And Chatham had to deal with a slowdown in business-related travel demand, which reduced the demand for the extended stay facilities in its portfolio (which make up for almost 2/3 rd of the total EBITDA).

Chatham Investor Relations

In the first quarter of this year, Chatham reported a total room revenue of just under $62M, which is a 23% increase compared to the first quarter of 2022. Meanwhile, the total amount of room operating expenses increased by a similar percentage, but in absolute dollar amounts the total net room revenue increased from $38.5M to $47.5M, and this was one of the main reasons why Chatham’s first quarter was actually pretty good.

Chatham Investor Relations

And as you can see in the image above, the total interest expenses remained relatively flat. That’s a good achievement, but let’s also not forget Chatham reduced its gross debt level throughout 2022, as it used the proceeds from asset sales to reduce the debt, which obviously helps to keep the interest expenses in check. Additionally, three expensive mortgage loans were repaid with the proceeds from a new term loan earlier this year. I will discuss the impact of increasing interest rates later in this article, as I first would like to discuss the FFO and AFFO performance.

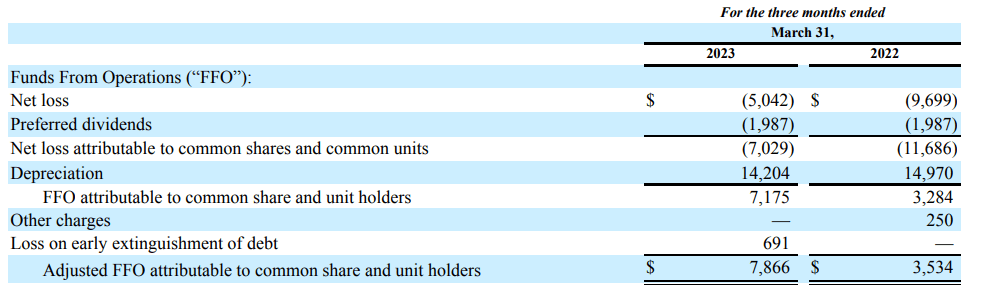

Chatham’s FFO and AFFO calculations are very basic. As you can see below, there are hardly any adjustments, and in the first quarter of the current financial year, Chatham’s FFO and AFFO came in at $7.2M and $7.9M, respectively.

Chatham Investor Relations

Based on the current share count of 50.2M shares and units (which includes the non-controlling interests), the FFO and AFFO per share came in at $0.14 and $0.16, respectively. That’s low for a $10 stock, but keep in mind the seasonality is very important here. Just to explain how important: in Q2 and Q3 last year, the total AFFO was approximately $46M and almost 80% of the full-year AFFO was generated during Q1 and Q2. Based on last year’s performance, I think it is safe to say the AFFO/share will likely exceed $1.15 during 2023 and has a shot at exceeding $1.20.

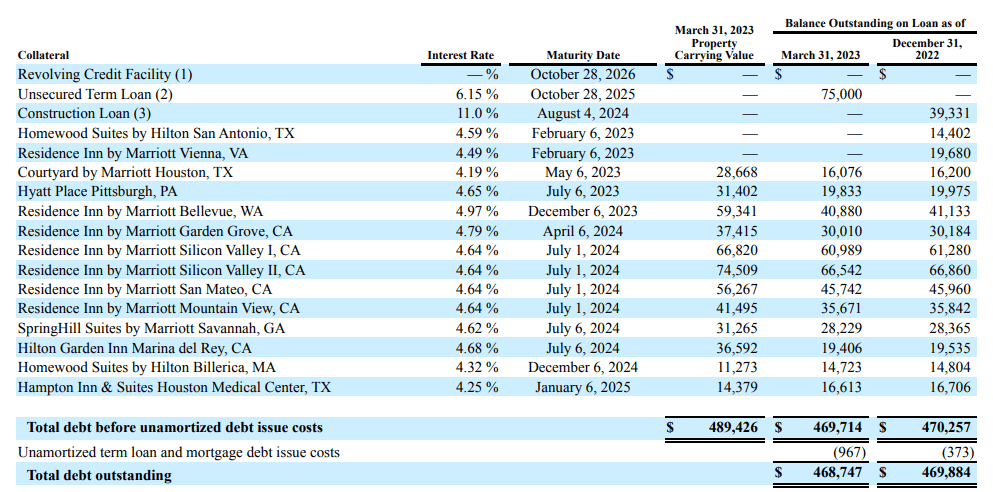

Going back to the interest expenses. The majority of the debt on the balance sheet is fixed rate debt, as you can see below. The average cost of debt is just under 5%, which is manageable.

Chatham Investor Relations

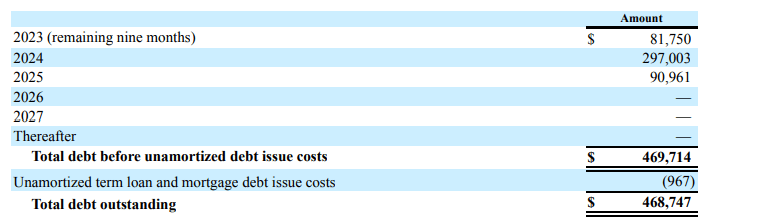

The main issue, as you can see above, is that virtually all mortgage debt expires within the next 24 months. Which means that mainly 2024 could potentially result in a shock to the total interest expenses.

Chatham Investor Relations

Applying a 200 bp increase in the interest expenses across the board means that between now and the end of 2024, Chatham will see its annual interest expenses increase by approximately $7.5M per year. Fortunately this is less than $2M per quarter which essentially means the AFFO/share will be hit to the tune of $0.15 per share per year. Not great, but also not a total disaster. And even if – in a bearish scenario – the total cost of debt would increase to 8% across the board, the AFFO/share would increase by "just" $0.24. Not great for the common shareholders but it does not impact the thesis for the preferred shareholders.

The details of the preferred shares

Chatham Lodging Trust only has one series of preferred shares outstanding, the Series A cumulative preferred shares (NYSE:CLDT.PA). I like the cumulative feature, as it means the REIT will have to cover all unpaid preferred dividends before making any payments on the common units. And perhaps also important: although Chatham suspended making distributions on its common units (until it reinstated a quarterly dividend of $0.07 per share), it continued to make the preferred dividend payments.

The Series A preferred shares have a fixed annual preferred dividend of $1.65625 per share, which is payable in four equal quarterly installments of $0.414 per share. Based on the current share price of $19.14/share (the closing price as of Tuesday), the preferred dividend yield is currently 8.65%. The preferred shares can only be called from June 2026 on.

As there are only 4.8M preferred shares outstanding, the quarterly preferred dividend payment is just under $2M. If Chatham’s AFFO in 2023 would come in flat versus last year (I am expecting a small increase), the total pre-dividend AFFO would be approximately $68M of which less than $8M would be needed to cover the preferred dividends. Or in other words, the REIT needs to spend less than 15% of its full-year AFFO to cover the preferred dividends.

This means the dividend coverage ratio is excellent but it’s obviously also important to have a look at the balance sheet as well.

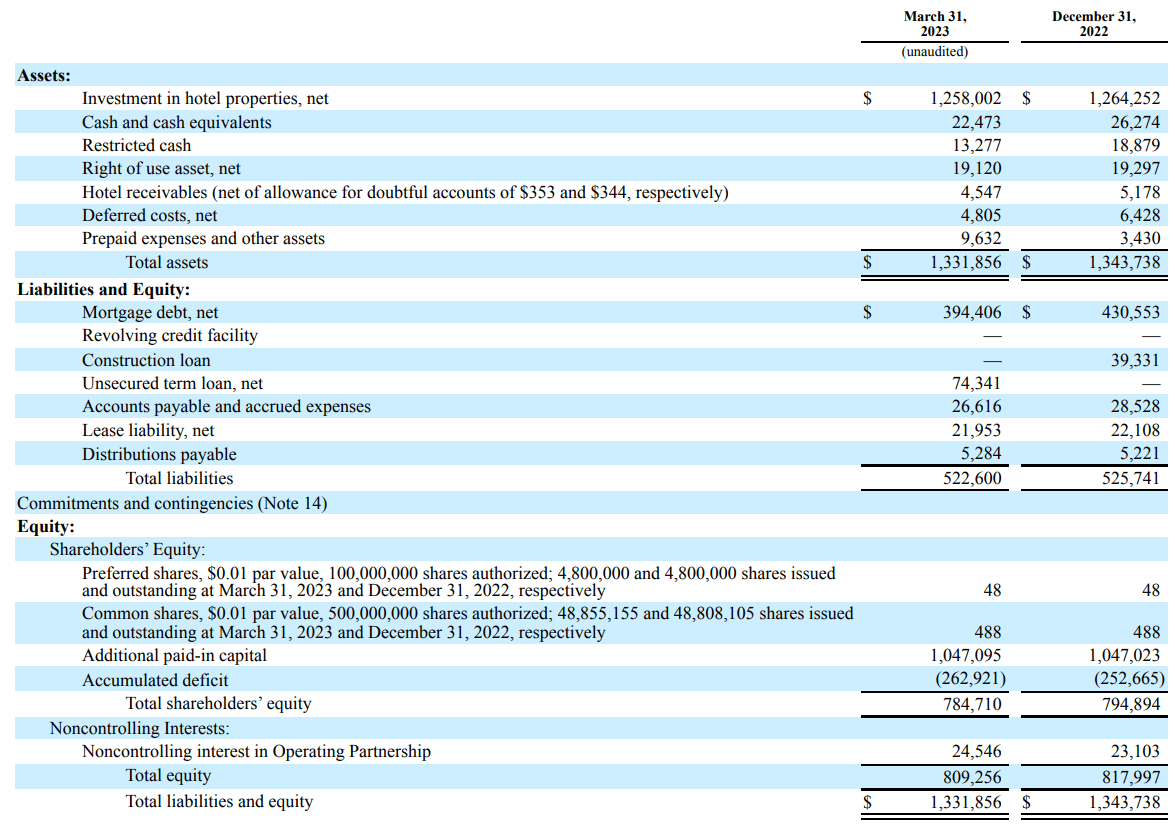

Chatham Investor Relations

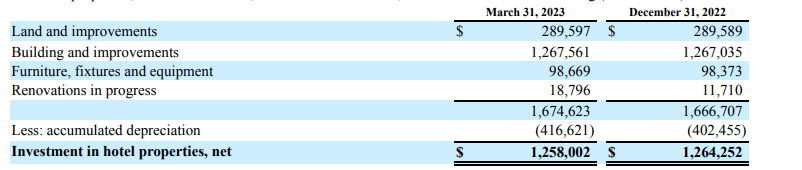

The net debt on the balance sheet is just $450M, which represents just 36% of the book value of the assets. That’s very reasonable, especially if you know the book value already includes in excess of $400M in accumulated depreciation (see below).

Chatham Investor Relations

Even if we would just use the book value of the REIT, there’s about $785M in equity, of which exactly $120M was raised through the sale of the preferred shares. This means there is a very comfortable cushion of in excess of $660M in equity ranked junior to the preferred shares. Or, in other words, if all hotel assets would be sold at 50% of the book value, the REIT would still generate enough cash to make the preferred shareholders whole.

Investment thesis

And this makes Chatham Lodging an interesting "duo-pick." The common shares appear to be attractive enough to warrant a long position. Keeping all other elements stable, even an average cost of debt increase to 8% across the board (which I don’t think is going to happen) would still result in an AFFO of close to $1/share. And as the dividend yield is pretty low on the Chatham Lodging Trust common shares (just under 3%), the 8.65% yielding preferred shares may be more appealing to income-focused investors.

I will be looking to add the Chatham Lodging Trust preferred shares to my portfolio, as I think the risk/reward ratio is pretty good.

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I may initiate a long position in Chatham's preferred shares, but very likely not within the next 72 hours.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (2)