Boliden: A Northern European High-Quality Base Metals Mining Company

Summary

- Boliden stock price has retraced slightly over the last few months due to some operational challenges and weaker commodity prices.

- So, the valuation has come down some for Boliden, but it is still relatively close to the historical average.

- Over the long term, Boliden has done an excellent job operationally, which is also reflected in the stock price performance.

- I do much more than just articles at Off The Beaten Path: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

igormakarov/iStock via Getty Images

Investment Thesis

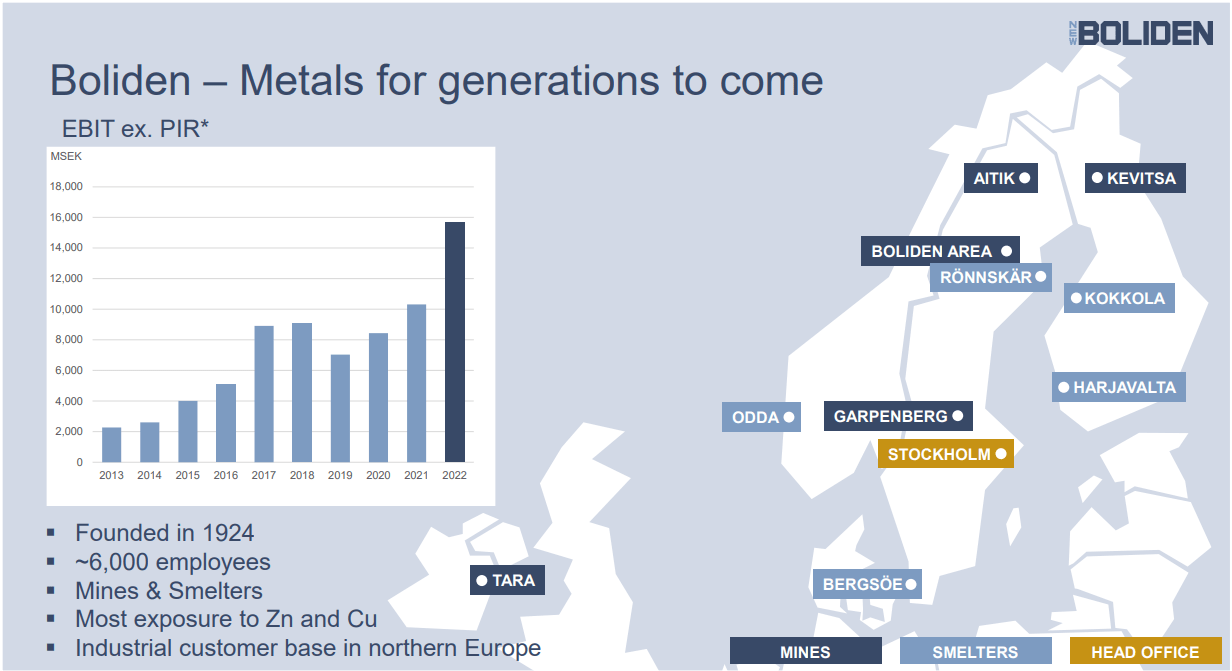

Boliden (OTCPK:BDNNY) is a Northern European mining company, which is primarily exposed to copper and zinc, but mines several other metals as well. The company has its head office and primarily listing in Sweden. The reporting currency is consequently Swedish Kronor ("SEK")

Figure 1 - Source: Boliden Q1-23 Presentation

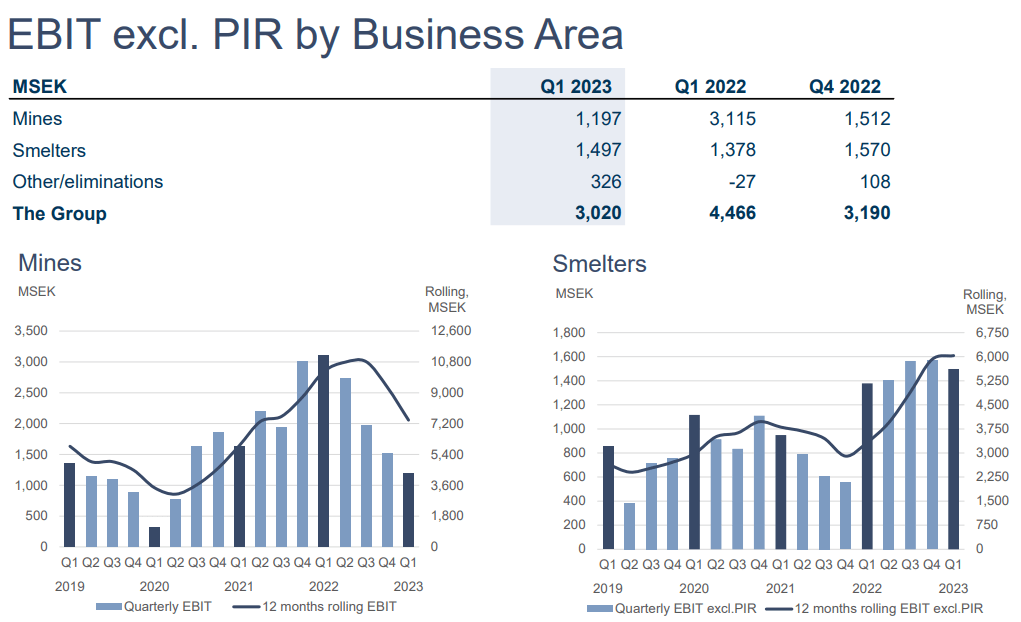

During the last quarter, more than 50% of EBIT came from the smelters, which is an important segment for Boliden, even if the mines normally contribute more than the smelters to EBIT.

Figure 2 - Source: Boliden Q1-23 Presentation

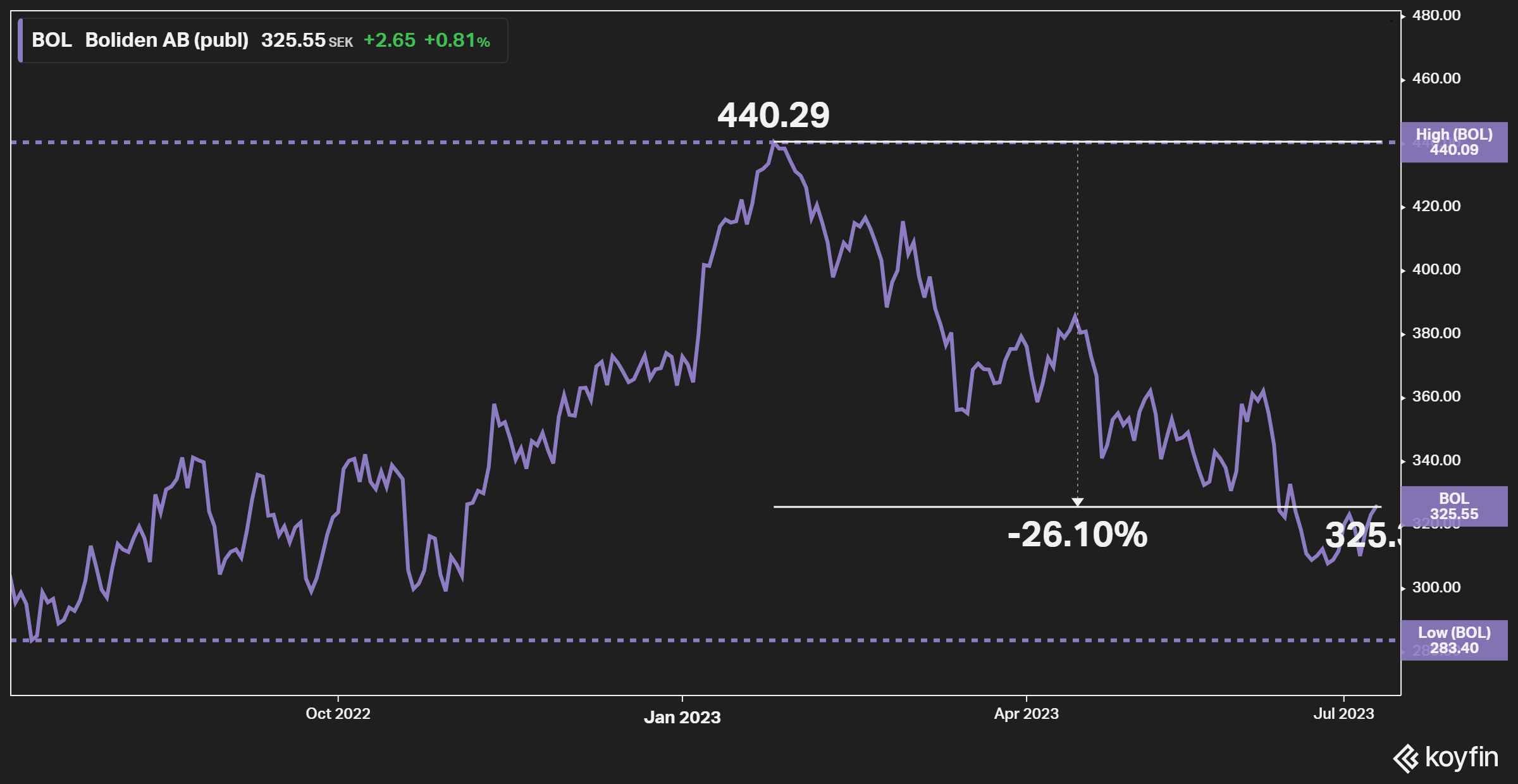

The stock price of Boliden has sold off 26% from the peak seen early in 2023 due to a combination of lower metal prices and some operational challenges, which I am not overly concerned about longer term. So, the attractiveness has in my view improved lately.

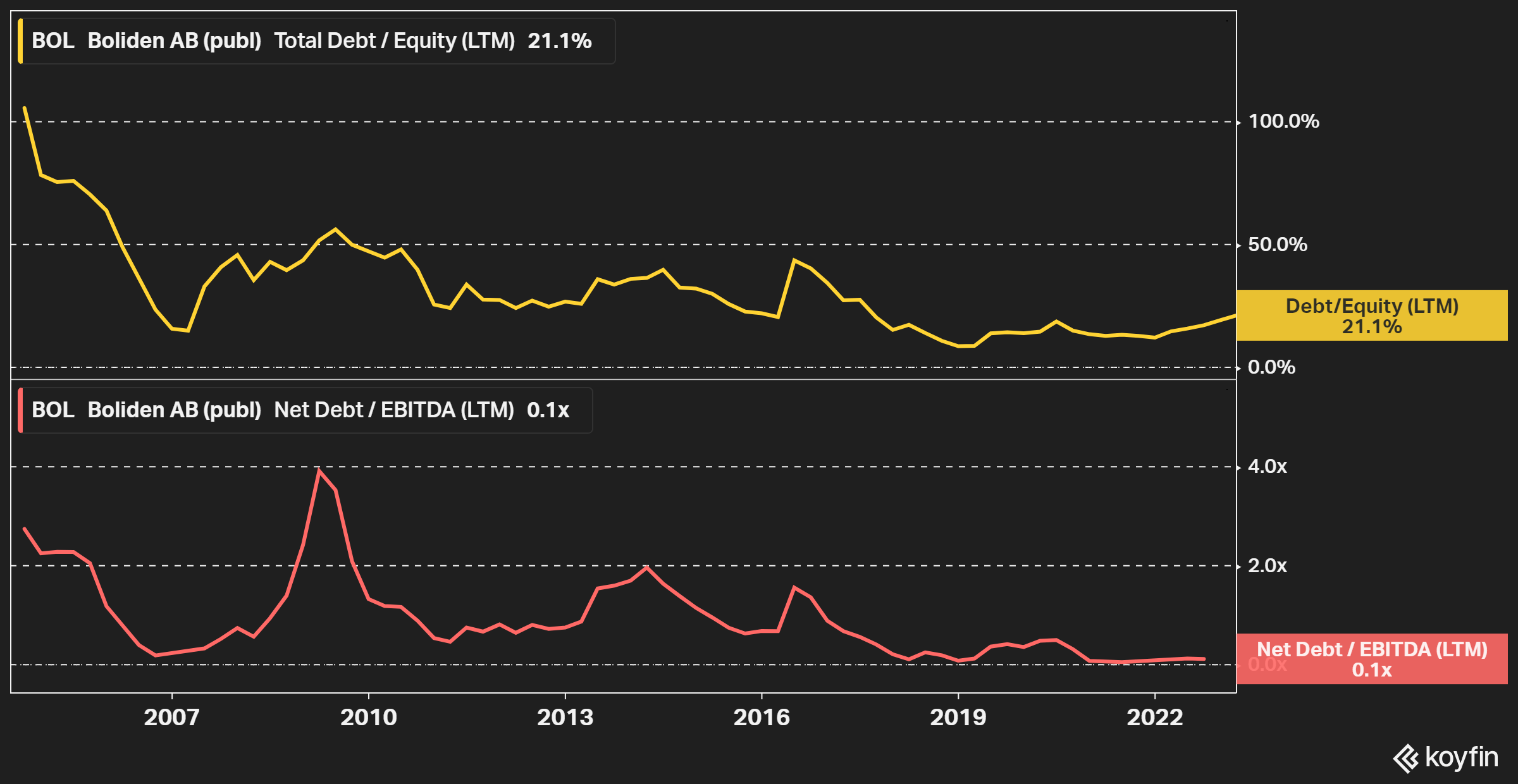

Figure 3 - Source: Koyfin

Consistent Performer

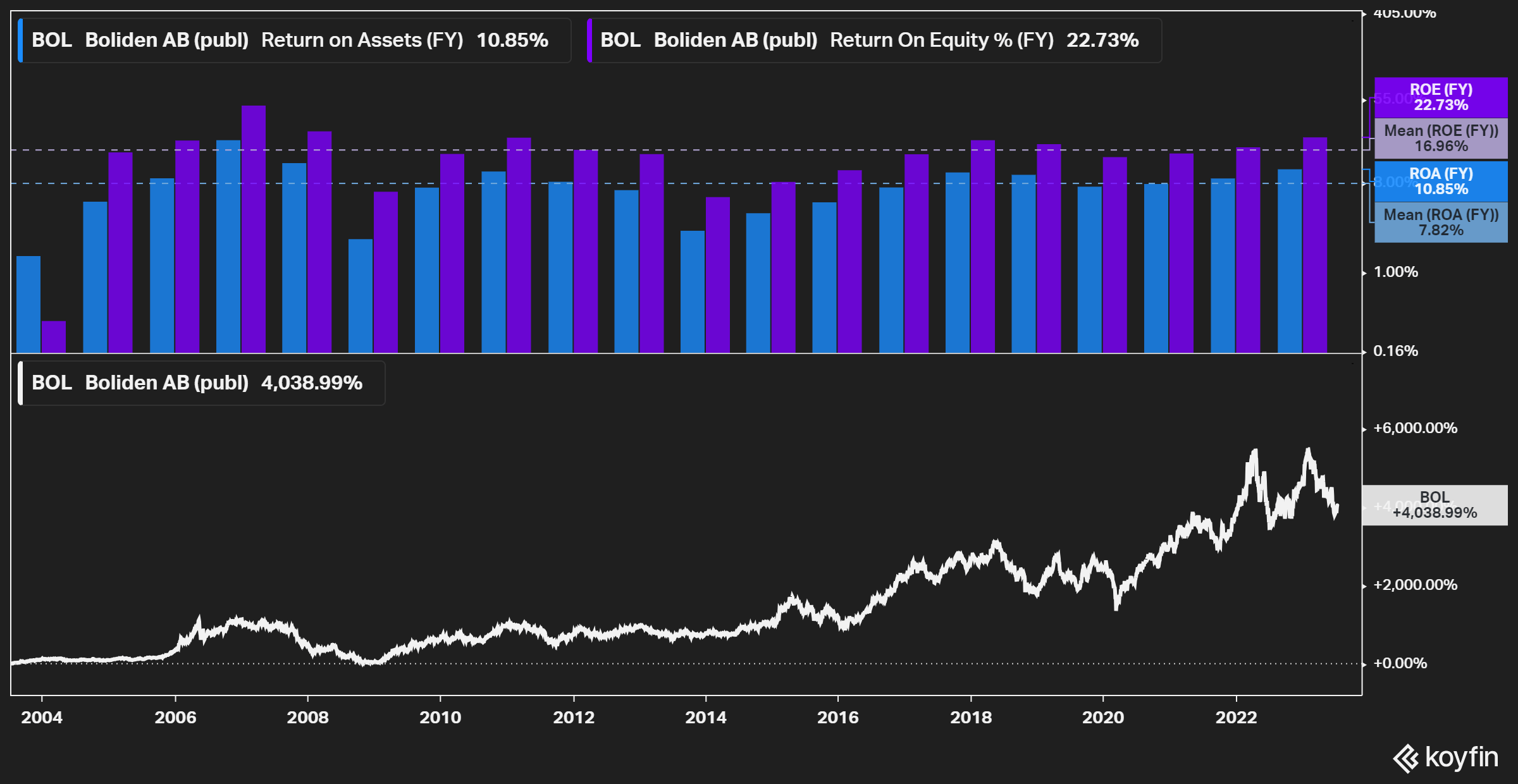

Over the last 20 years, Boliden has had a very impressive operating history, averaging a return on equity of 17%. That is even more impressive when we consider that the company has had relatively modest financial leverage during much of this period. The net debt in the most recent quarter is around zero and the debt-to-equity ratio is at 21%.

Over the last 20 years the stock price return has been extremely impressive as well, even if the starting point of the chart below was relatively close to a cycle low.

Figure 4 - Source: Koyfin

Figure 5 - Source: Koyfin

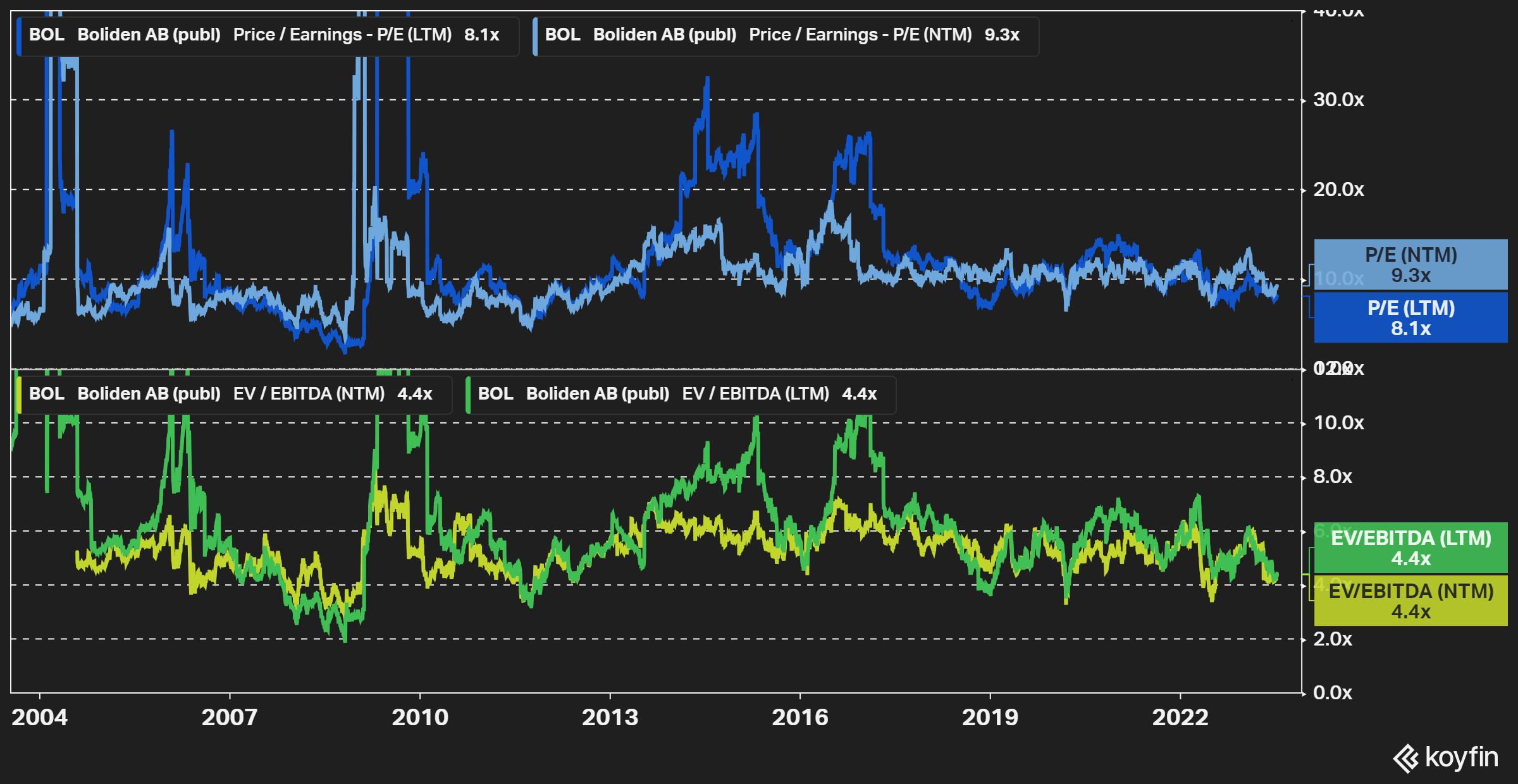

Boliden does frequently trade with a Price/Earnings ratio around 10 and the EV/EBITDA has often been in the 4-6 range. We can see in the chart below that the valuation looks to be slightly below the long-term averages, even if the stock price is far from depressed at this level.

Figure 6 - Source: Koyfin

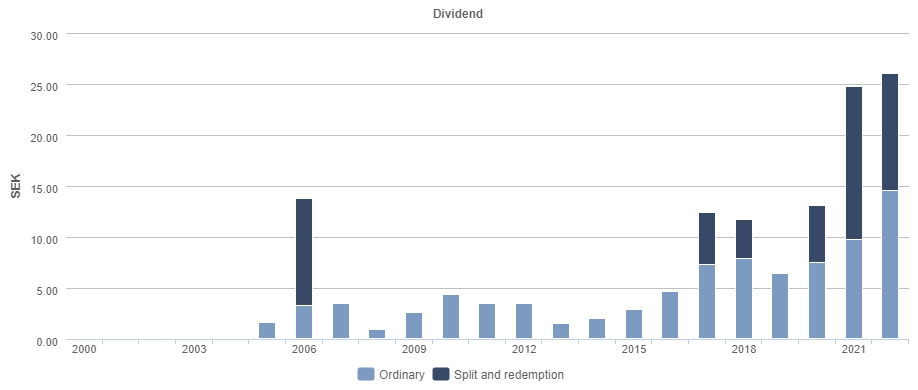

The company's policy is to return 33% of net profits in dividends. but the capital distributions have been significantly higher than that lately. Boliden, apart from the regular dividend, does rely on split and automatic redemption shares for cash distributions.

For those not familiar with this approach, you effectively have one regular share get split into one new regular share + one redemption share which will automatically be converted to cash after a few weeks. However, the redemption shares will trade very close to the redemption value for a short listing-period, which allows investors that pay higher taxes on Swedish dividends compared to capital gains to sell the redemption shares in the market.

Figure 7 - Source: Boliden.com

Competitive Advantages

Some might be concerned about investing in heavy European industries, which the mines and smelters certainly are, given the lack of energy security for Europe. However, all of Europe is not equally exposed to energy security problems and higher electricity prices.

You can see in figure 1 at the top where Boliden has its operations. The northern part of Sweden and Norway frequently have very low electricity prices compared to continental Europe, due to being scarcely populated, and primarily relying on hydro to generate electricity. Lately Finland has seen very low electricity prices as well, following the launch of the latest nuclear reactor, Olkiluoto 3.

The higher cost Tara mine in Ireland was recently put on care and maintenance, due to combination of factors, but I would exclude that from any projections going forward. The southern part of Sweden has seen higher electricity prices lately, likely due to the closure of some nuclear reactors a few years back. While it looks like the new Swedish government is taking steps to address the energy security, it will likely take some time before that is completely rectified.

Having said all that, Boliden has also been very strategic and has hedged much of its electricity consumption at very attractive prices. So, rather than viewing the energy problems for Europe as a concern, I would actually view the locations of Boliden's operations and the electricity hedges as a competitive advantage for the company.

The aim during the next two years is for around 80 percent of electrical power consumption to be secured through long-term contracts. Today, around 60 percent of electricity consumption is hedged up to 2035 at a fixed price of around EUR 35/MWh, including estimated adjustments for consumer price index. /Boliden 2022 Annual Report

Part of the reason for Boliden's success is the optimization work the company has been doing over the years. This relates to the use of fossil fuels, where much of operations have been electrified, which might be a very important aspect if the European Union were to turn to some kind of carbon taxes over time. The optimization is also related to the usage of energy in general and the use of labor, which is no doubt an important component in countries with relatively high costs and high taxes.

Figure 8 - Source: Boliden Q1-23 Presentation

Concluding Thoughts

Lately Boliden has had more production disruptions than we have seen historically. Rönnskär, for example, had a fire which destroyed some assets at the smelter and has curtailed production, even if part of the operation has now been restarted. I don't think the recent problems will impact Boliden's long-term value proposition substantially.

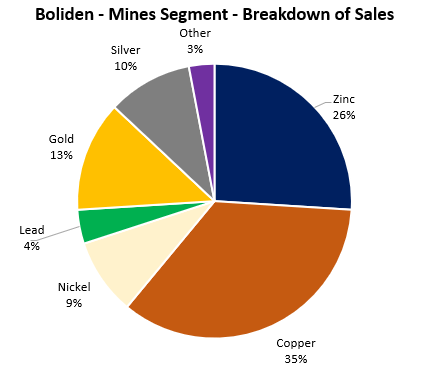

There is a lot to like about Boliden, but it is important to remember that the company operates in a cyclical business. Where you can see the sales by metals during 2022 for the mines segment below.

Figure 9 - Source: Data from Boliden Annual Report 2022

The 23% of sales in the mines segment coming from gold and silver are likely somewhat countercyclical compared to the rest of the business and the earnings from the smelters are at least slightly less volatile. However, given the large exposure to base metals, Boliden is relatively exposed to a potential economic downturn in Europe.

Boliden is an attractive company, where the stock will remain on my watchlist rather than in the portfolio as the attractive quality characteristics and slightly lower price are not sufficient to offset my slight concerns about the European economy in general.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you like this article and is interested in more frequent analysis of my holding companies, real-time notifications on portfolio changes, together with macro and industry analysis. I would encourage you to have a look at my investing group, Off The Beaten Path.

I primarily invest in turnarounds in natural resource industries, where I have a typical holding period of 1-3 years. Focusing on value offers good downside protection and can still provide great upside participation.

This article was written by

I enjoy my anonymity, which I think is underappreciated in today's world, where I write under the name Bang For The Buck. I hold a BSc and MSc in Financial Economics and I have extensive experience with the investment management industry. I am the CEO of a small investment company. I primarily focus on turnaround stories, with attractive valuations, in cyclical industries.

Presently, I am very focused on the precious metals industry due to current monetary and fiscal policies. I am also invested in the uranium and oil & gas industries, due to underinvestments together with very attractive valuations.

I publish regular articles on Seeking Alpha and offer an investing group service called Off The Beaten Path where subscribers receives real-time updates on the portfolio, in-depth portfolio reports, and frequent updates on holdings companies. As the name suggest, I primarily invest in industries and companies that are underappreciated, which I have found provides more attractive returns.

I am always happy to respond to comments and questions in my articles during the first few days. More in-depth and ongoing discussions are had inside Off The Beaten Path.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.