GitLab: Valuation Multiple Expected To Be A Headwind (Rating Downgrade)

Summary

- I recommend a hold for GTLB as the stock price has already reflected my price target and the current premium is excessive.

- GTLB has a competitive edge in the rapidly expanding DevOps market, with a single application that covers all stages of software development.

- Despite being a loss-making company, GTLB has a strong balance sheet with no debt and $930 million in cash.

Olemedia

Overview

My recommendation for GitLab (NASDAQ:GTLB) is a hold rating as the stock price has reflected my price target, and I expect the valuation to compress back to 9x forward revenue as the current premium is too much given the relative growth rates.

Note that I previously rated buy rating for GTLB due to its proven competitive advantage over its competitors by having a single application that comprises all the stages of software development, and that investing in it provides exposure to the strong secular trend.

Business

GTLB is a software development company that provides a DevOps platform for integrating software design, security, development, operations, IT, and business teams. This is a major shift in how businesses approach software architecture, development, and distribution.

Industry

According to Allied Market Research, the global DevOps market size was $6.78 billion in 2020 and is expected to reach $57.90 billion by 2030, recording a CAGR of 24.2% from 2021 to 2030.

I expect that the DevOps market will continue to expand as a result of rising interest in decreasing capital expenditures and operating expenses, as well as the need for continuous and rapid application delivery. The proliferation of applications operating in the ever-changing IT landscape also contributes to the market's expansion. Moreover, innovations in AI and its use in application development, as well as a high rate of adoption among SMEs, are anticipated to present lucrative opportunities for the expansion of the DevOps market.

Amazon, Broadcom, Dell, Google, IBM, Microsoft, and many others are just a few of the formidable companies operating in this space.

Investment highlights

Investor confidence should rise in light of the solid financial performance. As GTLB continues to implement its plan to use multiple LLMs to introduce generative AI into each of the 9 phases of the software development life cycle, I anticipate it will continue to expand its market share. Combined with the sequential stabilization of relative demand and the absence of any major changes in the competitive landscape, I think the recent performance has calmed investors' fears of further structural challenges. Along with churn being relatively stable, key qualitative metrics like net expansion rate continue to be extremely healthy at 128%. When the macro environment turns around and growth picks up, I think GTLB will be in a good position to benefit. As I mentioned before, I think there are levers for further gains in market share in the scaling of generative AI features and in monetizing the opportunity.

Financial highlights

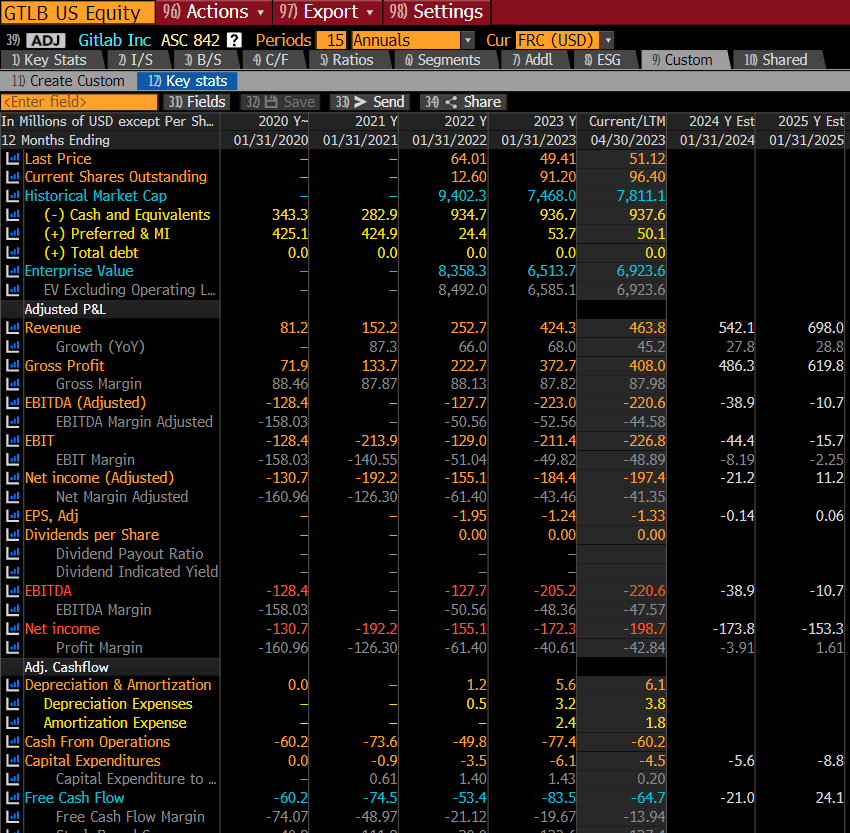

Bloomberg

In my opinion, revenue growth is the key metric that investors are watching for GTLB, as evidenced by the increase in share price following 1Q24 results. Revenue increased by 45% in the first quarter, exceeding expectations. GTLB's revenue should continue to grow rapidly, as the industry as a whole is expanding rapidly. Given GTLB's strong competitive advantage, I believe it can outperform the industry in terms of growth.

GTLB is a loss-making company today, but given its high gross margin profile of 80++%, I anticipate a very attractive long-term margin profile. However, it is not the focus today because the company is still growing at a rate of more than 40%.

GTLB's balance sheet is still solid, with no debt and $930 million in cash. Based on the LTM burn rate (EBITDA), this cash position can easily last GTLB for four years before any capital raising corporate actions are required.

Valuation

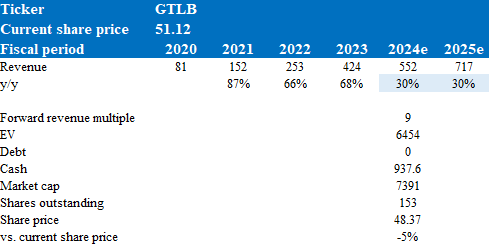

Author's valuation model

GTLB is valued at $48 in FY24, a -5% decline, making the stock fairly valued today, according to my model. This target price is based on my 30% growth forecast over the next two years, which is slightly lower than historical levels because the macroeconomy is not the same as in the past. However, growth should continue to outpace the industry.

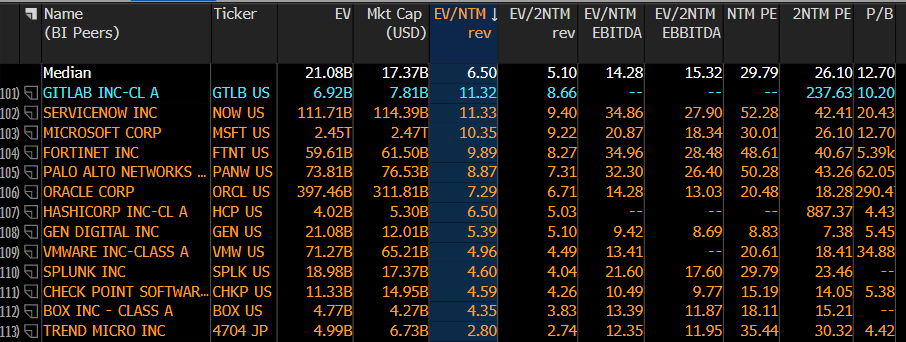

GTLB is now trading at 11x forward revenue, which I believe is excessive when compared to peers. As I believe a modest premium is justified, I valued it at 9x forward revenue.

Bloomberg

Bloomberg

Risk

GTLB's growth and prosperity are predicated on the company's skill in transforming trial users into paying customers by offering them more of what they already use. GTLB's success hinges on the rate at which its customers buy additional products and services; if these efforts are unsuccessful, the company will struggle.

Conclusion

In conclusion, my recommendation for GTLB is a hold rating due to the expected valuation multiple compression. While GTLB has a competitive advantage in the DevOps market and benefits from the industry's rapid expansion, the current premium on its stock price is excessive. Based on my valuation model, GTLB is fairly valued at $48, with a target price reflecting modest growth.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.