Block: Time To Be Aggressive Before Others Jump In

Summary

- Block stock has outperformed the S&P 500 since my update in May, despite initial negative sentiment due to a short attack by Hindenburg Research.

- The company is making encouraging progress in moving upmarket. Its adjusted EBITDA is estimated to grow at a CAGR of over 35% from FY22-25.

- SQ is priced at a premium against its peers, indicating the need for CEO Jack Dorsey and his team to execute well.

- I assessed that dip buyers have returned to underpin the stock at key support levels, opening up further opportunities for momentum buyers to follow through.

- It's time to get more aggressive before the rest jump on the bandwagon.

- I do much more than just articles at Ultimate Growth Investing: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

Drew Angerer

Block, Inc. (NYSE:SQ) stock has outperformed the S&P 500 (SPX) since I upgraded SQ in late May, seeing an opportunity to get more constructive. SQ was initially hampered by negative sentiment relating to the short attack by Hindenburg Research.

However, SQ investors have shrugged off the attack, as they bought the dips in mid-May, bolstering its recent recovery. Despite that, I assessed that momentum buyers will not likely return until SQ regains its medium-term uptrend decisively. As such, I believe the opportunities to get on board SQ's nascent recovery remain intact as investors fret over its exposure to SMBs and lower-income consumers.

Moreover, the US economy has proven to be more resilient than economists had anticipated. I shared in a recent Invesco QQQ ETF (QQQ) article how the consensus view of economists about a recession had shifted to one where "no recession [is] coming after all."

With the market pricing in a more hawkish Fed, given the strength of the recent jobs numbers and the US economy, SQ's outperformance augurs well. It likely suggests that market operators could have priced in the worst at its lows in October 2022.

Block management updated in a recent conference and reminded investors that it's making progress in moving upmarket. Despite that, "regulatory constraints as a financial institution limit Block's ability to act like an internet company." As such, it's critical for investors to assess Block's ability to outgrow its industry peers, given the growth premium baked into its valuation.

CFO Amrita Ahuja articulated that the company is attacking a $200B TAM, in which its opportunity is still nascent. Ahuja stressed that the company's penetration of less than 5% indicates that Block can continue to "take share over time."

I believe that's the crux of the company's thesis in a highly competitive financial technology space. With its legacy banking peers on schedule to launch FedNow in late July, the competitiveness against Block will likely intensify. The leading banks are fighting back with their massive resources and their stocks trade at much lower valuation multiples than SQ. As such, investors need to assess the dynamism in the competitive landscape on how Block's edge could be impacted.

Morningstar rated Block with a narrow economic moat, corroborating its strength in the SMB segment. In addition, investors are also reminded that the monetization opportunities in its consumer-facing Cash App "may be limited."

However, I gleaned that management thinks that the monetization opportunity within Cash App is still early, as it focuses on "product adoption and engagement within the ecosystem." As such, investors must assess the underlying growth in "product attachments and inflows per active over time."

Wall Street analysts' estimates suggest that Block's growth opportunities are still in the earlier stages. Analysts project the company could gain significant operating leverage over the next few years.

Accordingly, Block's adjusted EBITDA is estimated to increase at a CAGR of more than 35% from FY22-25. Seeking Alpha's Quant also rated SQ's growth metrics with an "A+" grade (the best possible).

Therefore, I believe it's important to assess SQ from a growth stock perspective on whether its valuation has reflected its potential bottom-line growth over the next three years.

SQ last traded at an FY25 EBITDA multiple of 16.5x, which is still above its peers' forward median of 10.7x (according to S&P Cap IQ data). As such, bears could argue that SQ's valuation has likely baked in a high level of optimism, suggesting that CEO Jack Dorsey and his team must execute impeccably to achieve its growth projections.

I believe SQ's growth premium remains its most significant risk in my thesis, and investors considering adding more positions must have a high conviction over the company's ability to gain share.

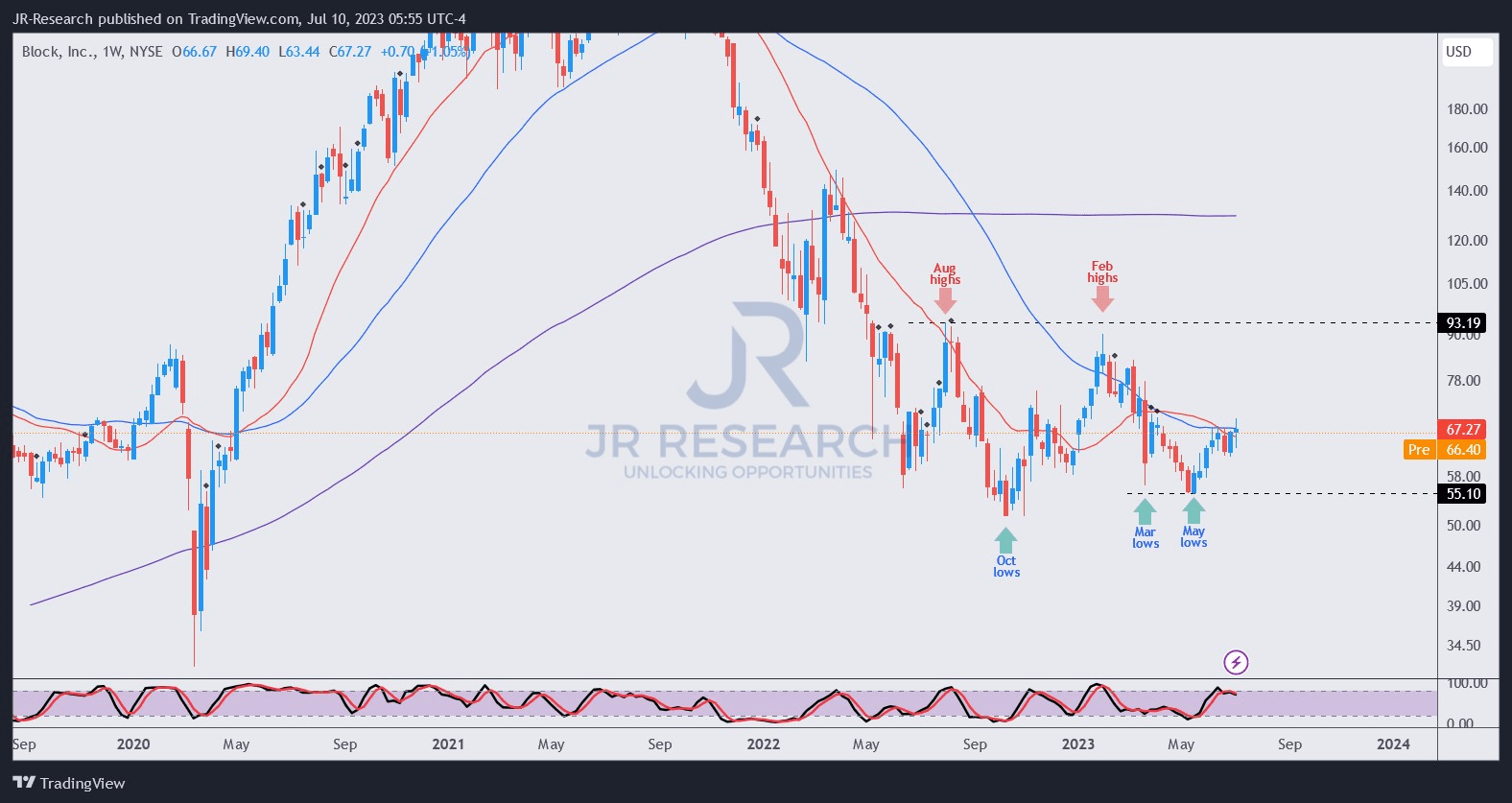

SQ price chart (weekly) (TradingView)

Note that SQ formed its lows in October 2022, and buyers defended it stoutly in March and May, refusing to allow sellers the opportunity to take out lower lows.

I assessed that SQ's recovery momentum indicates that dip buyers are increasingly confident, as seen in its buying sentiment in May. In addition, SQ could retake its medium-term uptrend bias, even though it's still too early to ascertain when that would occur.

Still, I gleaned that high-conviction investors who have confidence that SQ could recover further from its May lows should find the current levels appealing.

While a pullback should be expected with SQ's momentum in overbought levels, I'm more confident that SQ could see further upside from here as momentum investors could return to bolster its upward re-rating.

With that in mind, I believe it's time to turn even more constructive on SQ and not wait for these investors to arrive first so that we can get in earlier.

Rating: Strong Buy. (Revised from Buy).

Important note: Investors are reminded to do their own due diligence and not rely on the information provided as financial advice. The rating is also not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have additional commentary to improve our thesis? Spotted a critical gap in our thesis? Saw something important that we didn't? Agree or disagree? Comment below and let us know why, and help everyone in the community to learn better!

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA's bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!

This article was written by

Ultimate Growth Investing, led by founder JR Research, helps investors better understand a range of investment sectors with a focus on technology. JR specializes in growth investments, utilizing a price action-based approach backed by actionable fundamental analysis. With a powerful toolkit, JR also provides insights into market sentiments, generating actionable market-leading indicators. In addition to tech and growth, JR also offers general stock analysis across a wide range of sectors and industries, with short- to medium-term stock analysis that includes a combination of long and short setups. Join the community today to improve your investment strategy and start experiencing the quality of our service.

Seeking Alpha features JR Research as one of its Top Analysts to Follow for the Technology, Software, and the Internet category, as well as for the Growth and GARP categories.

JR Research was featured as one of Seeking Alpha's leading contributors in 2022.

About JR: He was previously an Executive Director with a global financial services corporation and led company-wide, award-winning wealth management teams consistently ranked among the best in the company. He graduated with an Economics Degree from Asia's top-ranked National University of Singapore (NUS). NUS is also ranked among the top ten universities globally. I currently hold the rank of Major as a Commissioned Officer (Reservist) with the Singapore Armed Forces.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of SQ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (1)