TG Therapeutics: Too Early To Talk About Blockbuster Briumvi Sales

Summary

- TG Therapeutics' newly-launched multiple sclerosis therapy has been generating a lot of hype among analysts.

- Many are predicting sales to have grown exponentially - from ~$8bn in Q123 - when next quarter's earnings are announced.

- TGTX share price has been climbing as a result - up >100% this year.

- In reality, however, Briumvi faces some tough challenges in its market, against incumbents such as Roche and Novartis and their comparable drugs.

- I find it hard to board the hype train and doubt that TG Therapeutics' >$3.5bn market cap valuation is justified at this time.

- Looking for a portfolio of ideas like this one? Members of Haggerston BioHealth get exclusive access to our subscriber-only portfolios. Learn More »

frantic00/iStock via Getty Images

Investment Overview - Why I'm Not Boarding BRIUMVI Hype Train

TG Therapeutics (NASDAQ:TGTX) shares have been on the rise today after analysts told the market they expected outperformance when Q223 earnings are released in August, with TG's only commercial asset Briumvi, indicated for relapsed Multiple Sclerosis, beginning to justify blockbuster revenue expectations.

Management has provided no guidance, and I'm not so sure the revenue numbers, when they arrive, will support TG's $3.8bn market cap valuation.

TG Therapeutics - A Brief History - Summarizing Rise and Fall of Ukoniq

If backing biotech roller coaster rides is among your favored investment strategy then TG Therapeutics is doubtless on your watchlist.

I last covered the company more than three years ago when shares traded $18, and the Morrisville, N.C.,-based company was pushing for two major drug approvals - the anti-CD20 monoclonal antibody Ublituximab, and PI3K Inhibitor Umbralisib.

Ublituximab was being advanced to treat multiple sclerosis, and Umbralisib was up for approval in Marginal Zone Lymphoma ("MZL") and Follicular Lymphoma ("FL"). Meanwhile, the two drugs together - popularly referred to as "U2" - had delivered some strong data in Chronic Lymphocytic Leukemia ("CLL"), extending progression free survival by a statistically significant amount vs. standard of care - Roche's (OTCQX:RHHBY) Gazyva plus chlorambucil - and causing its pivotal study to be halted early. An approval for the combo in CLL looked more likely than not.

In February 2021, the FDA granted Umbralisib accelerated approval in relapsed or refractory MZL and FL under the brand name Ukoniq, and TG Therapeutics also submitted its Biologics License Application ("BLA") for U2 in patients with CLL/small lymphocytic lymphoma ("SLL").

At this point, TG Therapeutics stock was riding high, trading >$50 per share, but then in November 2021 the FDA informed the company that it planned to, according to TG's 2022 10K submission (annual report):

host an Oncologic Drug Advisory Committee (ODAC) meeting in connection with its review of the pending BLA/sNDA and to discuss the benefit risk of UKONIQ in its approved indications.

Notes in the 10K conclude the story as follows:

While the FDA identified a number of concerns, the FDA’s desire to host an ODAC appeared to stem from an early ad hoc analysis of overall survival ("OS") from the UNITY-CLL trial.

On April 15, 2022, based on newly updated OS data from the UNITY-CLL study, which showed a negative survival benefit, we decided to withdraw the pending BLA/sNDA for U2 to treat CLL/SLL.

On April 15, 2022, we also announced the voluntary withdrawal of UKONIQ from sale for its approved indications. Our decision to withdraw UKONIQ from sale was primarily based on the withdrawal of the BLA and sNDA for U2 in CLL. On June 1, 2022, the FDA withdrew its approval of UKONIQ.

The FDA had identified a possible elevated risk of death in patients using Ukoniq from earlier studies, and a drug that promised much is now fully withdrawn from the market, having generated <$10m in revenues. TG's share price sunk to a value of $4 by June last year - down 92%.

Ublituximab / Briumvi To The Rescue

Meanwhile, amid the furore over Ukoniq, TG continued to develop ublituximab, and in December last year TG announced that:

The FDA granted approval of ublituximab, now referred to as BRIUMVI, for the treatment of RMS, to include clinically isolated syndrome, relapsing-remitting disease, and active secondary progressive disease, in adults. (source - Q123 10Q submission)

The news triggered a bull run on TG stock that peaked in May, when the stock price touched a high of $35. Briumvi is, according to a TG presentation, "the first and only anti-CD20 monoclonal antibody that can be administered in a one-hour infusion twice a year, following the starting dose."

In its pivotal ULTIMATE I and ULTIMATE II studies, Briumvi demonstrated a 59% and 49% relative reduction in annualized relapse rate versus teriflunomide - an approved MS therapy marketed and sold by French pharma Sanofi (SNY), earning $1.96bn of revenues last year - and a 97% relative reduction in Gd+ T1 lesions. Importantly, the safety profile appears to be satisfactory - according to TG:

The overall rate of infections in MS patients treated with Briumvi was similar to patients who were treated with teriflunomide (55.8% vs 54.4%, respectively). Serious infections were 5% and 3% for BRIUMVI and teriflunomide, respectively

Assessing Briumvi's Market Opportunity

BRIUMVI is not the only anti-CD20 multiple sclerosis ("MS") therapy on the market - the two Swiss pharma giants Roche and Novartis (NVS) market and sell Ocrevus and Kesimpta respectively - these two drugs earned $6.7bn and $1.1bn in 2022.

Of the three commercial therapies, BRIUMVI is the least frequently dosed, with Kesimpta requiring injection once per month, and Ocrevus requiring two infusions in two weeks, followed by a once every six-month regime. Frankly, although TG lists this as a potentially significant difference, I would be more cautious - as far as treatment with Ocrevus goes, we are apparently talking about one extra treatment per annum, and in the case of Kesimpta, this therapy can be self-injected at home, which is arguably more convenient.

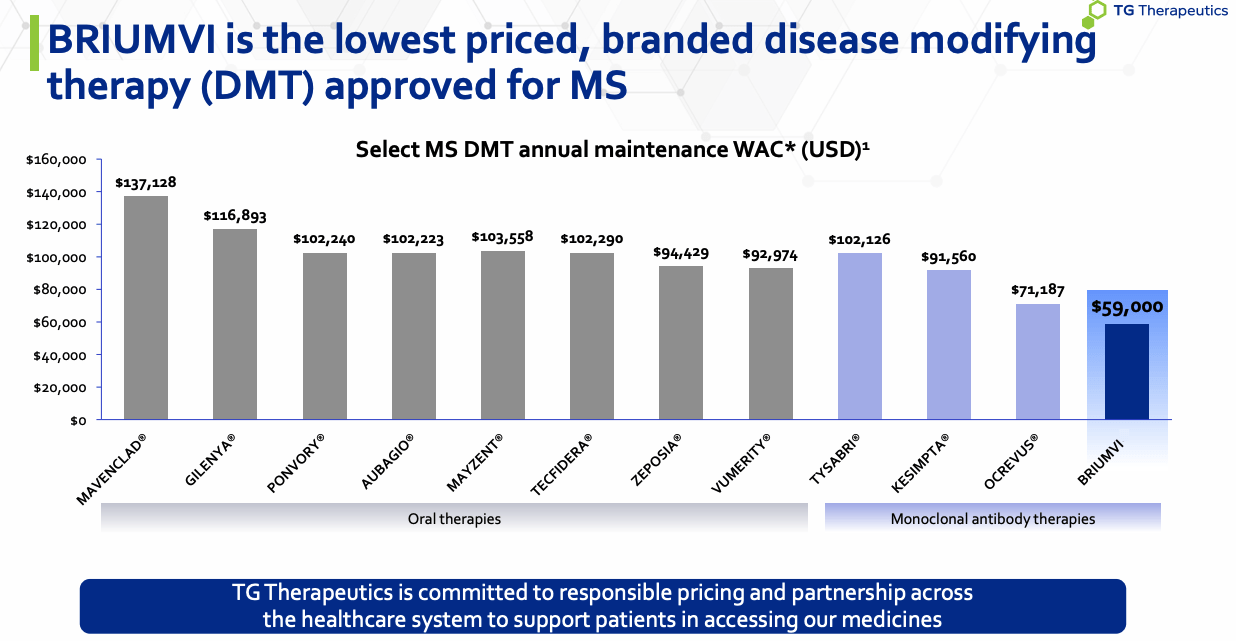

Nevertheless, Briumvi is, according to TG's approval day presentation, the cheapest disease modifying therapy ("DMT") on the market, with a price of $59k.

BRIUMVI pricing vs rivals (TG Therapeutics presentation)

Undercutting rivals on price would certainly be one way for TG to take market share away from entrenched rivals, although with that said, drug pricing is extremely complex and patients will not necessarily pay the prices quoted above to the drug manufacturers, given health insurers negotiate their own prices for drugs via pharmacy benefit managers.

TG says that it has hired sales agents to market and sell Briumvi that have worked at pharma giants like Novartis, Biogen (BIIB), which has an MS franchise driving >$6bn in revenues per annum, Bristol-Myers Squibb (BMY), which markets and sells Zeposia, another treatment option that is new to the market, and Roche and Novartis.

In some ways that's a good sign, but the corollary to that argument is that Roche, Novartis, Biogen, etc., are still the dominant incumbents in the MS market, and whatever TG's marketing budget may be, it's unlikely to be able to compete with these relative behemoths and their marketing budgets, and sales forces - or indeed their R&D budgets, dedicated to discovering better and safer drugs.

Nevertheless, TG's stock price has been climbing primarily on analyst bullish expectations for the drug - today, for example, Cantor's forecast for a Q223 earnings beat has sent shares climbing by 12%, while Jefferies has initiated coverage on TG with a buy rating, suggesting Briumvi sales could top $1bn by 2027, conferring "blockbuster" status on the drug, and setting a target price of $40 per share.

There's a caveat here, however, in my view. In Q123, admittedly only a couple of months post launch, TG reported Briumvi revenues of $7.8m, adding that it had registered:

Over 400 Briumvi prescriptions in the first partial quarter from 165+ healthcare providers at 125+ centers

According to TG, >100k MS patients in the US are currently on an anti-CD20 therapy, so that means that TG has captured 0.4% of the market in the first couple of months since launch. If TG earns its list price of $59k from all 400 patients, it will earn $23.6m. Clearly, that is not nearly enough to justify the hype, so how many prescriptions and patients would be enough?

To get to $1bn of revenues - assuming TG offers no rebates and gets every cent of the $59k list price, the number of patients would have to rise to ~20k, by my calculation, or a 20% market share. Is a 20% market share versus Roche and Novartis realistic?

These are entrenched incumbents, and although Briumvi does offer some advantages in terms of efficacy, dosing, and price, they appear to be quite marginal. Should Novartis and Roche be worried about a company with no prior commercial experience taking their market share away from them? I would be doubtful that they are.

It may be noteworthy that TG has so far declined to provide any 2023 guidance. On the Q123 earnings call, one analyst suggested that a figure of $65 - $70m would be achievable, based on between 2k - 25k patients using Briumvi by year-end. TG Chief Commercial Officer Adam Waldman declined to take the bait, however, commenting:

Yes, I think it's still too early. We're still early in this launch. I think we'd like another quarter of time to give you guidance on that.

Perhaps the guidance will arrive when Q223 earnings are announced, which is expected to happen around Aug. 9. It would not take much to outperform Q1, but to fulfill analysts' expectations of blockbuster sales by 2027, Briumvi is going to have to start showing some exponential growth very soon.

Concluding Thoughts - TGTX Faces A Tough Challenge In An Admittedly Large Market, With A Solid Therapeutic Option - But Current Valuation Feel Excessive

TG Therapeutics stock is +113% year to date, and the company's current market cap is $3.83bn. In Q123, revenues were $7.8m, operating loss was $(37m), and cash and equivalents were $140m. Accumulated deficit stood at $1.57bn.

These do not feel like figures that support a $3.8bn market cap valuation to me. Yes, Briumvi likely has good growth potential, but if we take a rule of thumb that commercial stage pharmaceutical companies typically trade at ~5x sales, even if Briumvi is set for blockbuster sales - which is a massive assumption to make at present - the upside potential may be capped at ~30%. It also should be noted that the P/S ratio of 5x usually only works when companies are profitable, and TG is far from profitable at this stage, and will likely have to invest hundreds of millions of dollars into marketing Briumvi if it wants to grab market share from Ocrevus and Kesimpta.

Meanwhile, the MS market is fluid with most big pharma concerns interested in the space given the rewards on offer. The anti-CD20 market may be worth ~$8bn at present based on sales of Ocrevus / Kesimpta, so a 15% share of it may help Briumvi achieve the coveted blockbuster status, but at the present time it seems far too optimistic for analysts to be discussing that kind of figure. BMY's Zeposia may soon prove it can challenge for standard of care, for example, while Biogen's BTK inhibitor Orelabrutinib is another potential challenger for "best in class" status a few years from now.

TG does not have much else in its pipeline, other than two Phase 1 stage assets, and its only other commercialized drug was withdrawn from the market due to safety concerns after earning <$10m of revenues.

In summary, while some analysts may be boarding the hype train where Briumvi and TG are concerned, I find it too hard to make the case for a $3.8bn valuation based on a single asset that earned <$8bn last quarter, and for which management is providing no guidance. Q223 earnings may justify some of the hype, but I'd be inclined to wonder if it also could check TG's shares progress somewhat and hand the company a reality check.

If you like what you have just read and want to receive at least 4 exclusive stock tips every week focused on Pharma, Biotech and Healthcare, then join me at my marketplace channel, Haggerston BioHealth. Invest alongside the model portfolio or simply access the investment bank-grade financial models and research. I hope to see you there.

This article was written by

I write about Biotech, Pharma and Healthcare stocks and share investment tips. Find me at my marketplace channel, Haggerston BioHealth - model portfolio + 4 exclusive stock tips every week. I'm on twitter @edmundingham

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BMY either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.