Astria Therapeutics: Most Likely Too Little, Too Late

Summary

- Astria Therapeutics is developing STAR-0215, a monoclonal antibody inhibitor, for the treatment of hereditary angioedema (HAE), with promising initial findings and ongoing clinical trials.

- The company reported a Q1 2023 operating loss of $13.5 million and a net loss of $11.2 million, but holds $213.3 million in cash, cash equivalents, and short-term investments, sufficient to operate until 2025.

- Despite Astria's promise, the saturated HAE market, emerging gene therapies, and STAR-0215's potential minor edge over current treatments, my recommendation is "Sell".

Bobex-73

Introduction

Astria Therapeutics (NASDAQ:ATXS) is a biopharmaceutical firm focusing on novel therapies for rare allergic and immunological diseases. Their key product, STAR-0215—a monoclonal antibody—is currently being developed as a long-term treatment for hereditary angioedema (HAE), a severe condition. Initial data suggest its potential effectiveness. Astria is advancing STAR-0215's development through ongoing clinical trials, targeting the unmet needs of HAE patients globally.

The following article provides a brief overview of Astria's prospects in HAE.

Q1 2023 Earnings

Let's first take a look at the firm's most recent quarterly earnings. As of March 2023, Astria held $213.3 million in cash, cash equivalents, and short-term investments, sufficient to operate until 2025. The company's net cash usage in operating activities was $13.3 million for Q1 2023. Research and development expenses decreased to $8.0 million due to major expenses for STAR-0215 in Q1 2022, but they are projected to rise in 2023. General and administrative expenses were $5.5 million. Astria reported a Q1 2023 operating loss of $13.5 million and a net loss of $11.2 million, or $0.40 per share. These losses were smaller than those of Q1 2022.

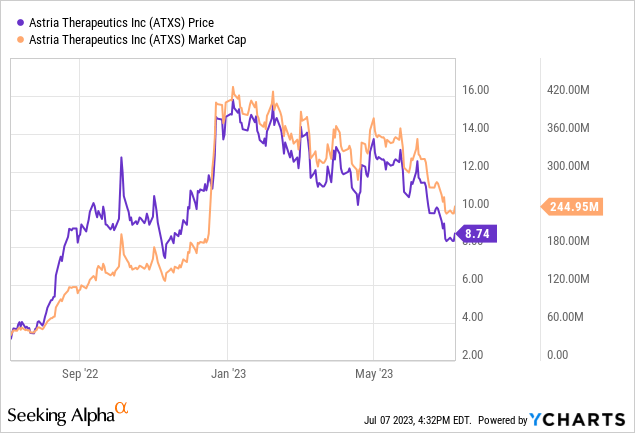

Astria, boasting a market capitalization of $244 million, classifies as a microcap company. Investors should be particularly cautious of the dilution risk inherent to such microcap firms. Even though Astria expects its current cash reserves to sustain the company until 2025, it is uncommon for biotechnology companies to delay fundraising until they've almost depleted their funds. As Astria continues to push its STAR-0215 through clinical trials, it's reasonable for investors to anticipate escalating operating costs. The need to cover these expenses may motivate the company to raise more funds, which is generally not left until the last moment. To illustrate this point, a hypothetical public offering raising merely $48 million could result in a dilution of its shares by around 20%. Therefore, it is crucial for investors to remain vigilant of the potential for additional capital raises and the associated dilution risk.

Evaluating STAR-0215: Potential and Challenges in the HAE Treatment Landscape

STAR-0215, a humanized monoclonal antibody tailored to combat Hereditary Angioedema, targets plasma kallikrein. It has been engineered via hybridoma screening and antibody optimization, resulting in high selectivity, a long plasma half-life, and minimized manufacturing concerns. The treatment entered clinical trials in 2022 and showed promising early results, with minor, self-resolving side effects. Impressively, STAR-0215 demonstrated a sustained presence in the body with a half-life of "up to 117 days", indicating the possibility of long-term attack prevention and less frequent dosing. Following a successful Phase 1a trial, it advanced to the Phase 1b/2 ALPHA-STAR trial in 2023. Preliminary results highlight its potential as a durable treatment for HAE that could enhance patient outcomes. Per Astria, preclinical data also suggest that STAR-0215's potent kallikrein inhibition and prolonged action period could provide superior preventative therapy for HAE patients. The company expects "initial proof-of-concept data" in mid-2024.

For clarity, proof-of-concept data typically comprises early indications validating the potential effectiveness or feasibility of a novel drug or treatment. In the realm of drug development, this often refers to initial findings from early-phase clinical trials (usually Phase 1 or 2), showcasing the drug's intended effect in humans. Importantly, this proof of concept generally stems from data collected in individuals with the specific disease or condition the treatment aims to address. This evidence serves as a crucial milestone, implying the treatment operates as initially hypothesized by researchers, and justifies further, more comprehensive clinical trials.

While STAR-0215 holds promise, its current improvements over existing HAE treatments seem to be primarily administrative, considering its developmental status. Existing HAE therapies, both reactive and preventive, present certain challenges regarding dosing frequency, side effects, and effectiveness. Nevertheless, these treatments, whether injected or taken orally, have demonstrated their efficacy. The less frequent dosing proposed for STAR-0215 is a potential advantage, but it still has to demonstrate safety and effectiveness that match or surpass current therapies before it can secure market approval. There is market interest in STAR-0215, but its actual impact on improving the quality of life for HAE patients is yet to be determined. Given the ongoing demand for long-lasting preventative therapies, the continued development and evaluation of STAR-0215 are paramount.

My Analysis & Recommendation

In conclusion, Astria Therapeutics has embarked on a notable journey with its monoclonal antibody, STAR-0215, targeting hereditary angioedema. The company's financial standing seems stable with sufficient funding to continue operations until 2025. Astria's commitment to their mission, progress with clinical trials, and the potential of STAR-0215 to offer long-term preventative therapy for HAE patients are commendable.

However, as an investor, I'm not entirely convinced about the company's long-term prospects. The HAE market is quite saturated and the advantages that STAR-0215 proposes—mainly less frequent dosing—are arguably marginal when compared to existing therapies. While less frequent dosing could potentially improve patients' lives, the drug's overall safety and efficacy will need to align with or surpass the currently approved treatments, which is yet to be seen.

Moreover, the landscape of HAE treatment is changing with the development of one-and-done gene therapies, a game-changer in treating genetic disorders like HAE. These advancements could significantly impact the future of HAE treatment and the market position of therapies like STAR-0215. Given Astria's current development stage, there's a risk of them being late to the game.

Hence, despite Astria's potential, the existing market saturation, coupled with the emergence of gene therapies and STAR-0215's possible marginal improvement over existing treatments, prompts me to recommend a "Sell" for Astria. That said, Astria's progress should be monitored closely. The landscape of biotech investment is continually evolving, and while Astria may not seem appealing today, the future could hold different opportunities.

Risks to Thesis

When the facts change, I change my mind.

While my bearish stance on Astria Therapeutics currently seems justified, it's crucial to acknowledge potential risks to this perspective.

Firstly, there's the inherent unpredictability of biopharmaceutical research and development. The science could break either way. STAR-0215 may outperform expectations in future trials, proving to be significantly more effective or safer than current therapies. This could boost its market appeal, potentially turning it into a game-changer in the treatment of HAE.

Secondly, while gene therapies are indeed promising, their practical application still faces many hurdles, including high costs, delivery challenges, and long-term safety concerns. If these issues are not resolved expediently, or if gene therapies for HAE prove less effective than anticipated, STAR-0215 and similar therapies may continue to dominate the market.

Another consideration is that while the HAE market appears saturated, it could potentially expand. This could happen if awareness and diagnosis rates improve, or if existing treatments prove inadequate for a significant number of patients, opening up more room for novel therapies like STAR-0215.

Finally, there's the possibility of Astria pivoting or expanding its focus to other rare and niche allergic and immunological diseases. If the company can leverage its technology and expertise to develop successful therapies for other conditions, it could enhance its market position and profitability, which would significantly impact the valuation.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This article is intended to provide informational content only and should not be construed as personalized investment advice with regard to "Buy/Sell/Hold/Short/Long" recommendations. Any predictions made in this article regarding clinical, regulatory, and market outcomes are the author's opinions and are based on probabilities, not certainties. While the information provided aims to be factual, errors may occur, and readers should verify the information for themselves. Investing in biotech is highly volatile, risky, and speculative, so readers should conduct their own research and consider their financial situation before making any investment decisions. The author cannot be held responsible for any financial losses resulting from reliance on the information presented in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.