U.S. Wide-Moat Stocks On Sale - The July 2023 Heat Map

Summary

- Our 3-step process focuses on wide-moat stocks (as per Morningstar’s rating).

- We are only interested in those targets that are attractively valued in historical comparison.

- We share the heat map of the most investable candidates that may be worth your time for further analysis.

ValeryEgorov

Step One: Wide-moat stocks with 5-star and 4-star ratings

Historical evidence says that while quality alone is a poor indicator of outperformance, when combined with a decent valuation filter, Morningstar's moat rating proves to be more than useful. Based on the available data, stocks with a wide-moat rating that also fit into the 4- or 5-star category deserve to be the subject of further analysis. See the detailed explanation and the underlying evidence of our first step in this article.

We focus on those companies that are covered by a Morningstar analyst as assigning a wide-moat rating without thorough analysis is a questionable practice in our opinion. As of July 5, there were 145 U.S. wide-moat stocks meeting our criteria (unchanged compared to last month, as Morningstar initiated coverage of Copart (CPRT) and Kenvue (KVUE) which both received a wide-moat badge, while Western Union (WU) got downgraded to a narrow-moat rating, and analysts dropped the coverage of John Wiley & Sons (WLY)).

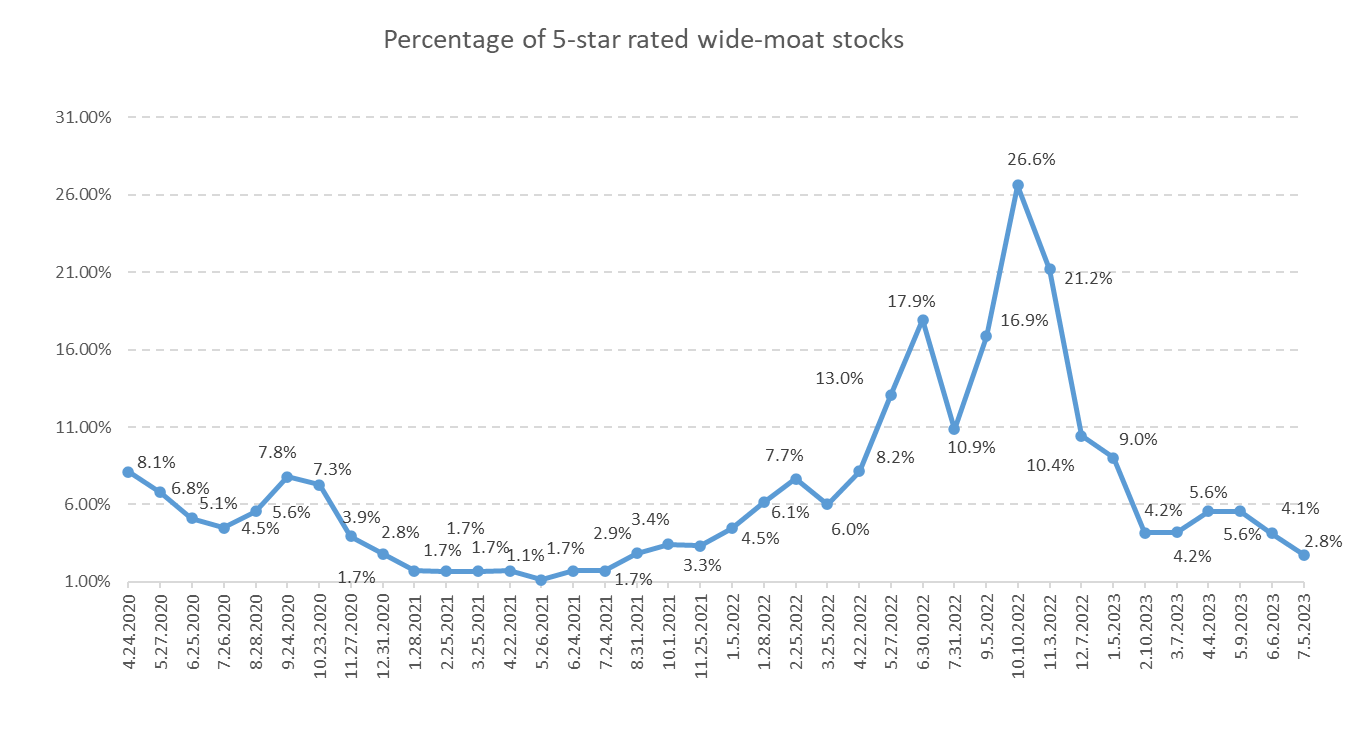

Only 2.8% (4 stocks) of this wide-moat group earned a 5-star (most attractive) valuation rating. Here are they:

Company Name | Ticker |

Comcast Corp. Class A | |

Compass Minerals International, Inc. | |

International Flavors & Fragrances Inc. | |

U.S. Bancorp |

We believe that the percentage of 5-star-rated wide-moat stocks is a good indicator of market sentiment. When this percentage is high, even the best companies are on sale. When the percentage is extremely low, market conditions may warrant caution. (Please note that this is not an indicator for market timing!)

Data from Morningstar. Dataset after 12/2022 only contains U.S. stocks.

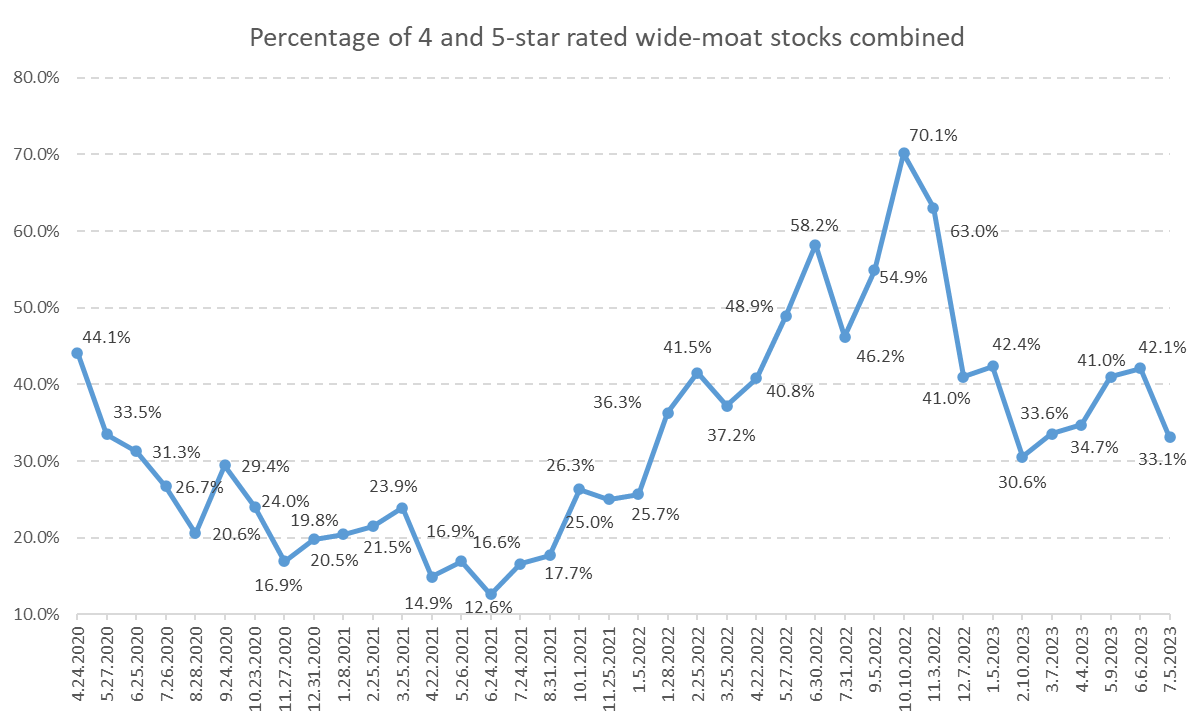

As these best-of-breed companies may be worth a closer look even when they are just slightly cheaper than their fair value but are not in the bargain bin, we also list the 4-star-rated wide-moat stocks as of July 5:

Company Name | Ticker |

Equifax Inc. | |

TransUnion | |

Wells Fargo & Co. | |

Polaris Inc. | |

Zimmer Biomet Holdings, Inc. | |

Teradyne, Inc. | |

The Walt Disney Co. | |

Tyler Technologies, Inc. | |

Veeva Systems Inc. Class A | |

Berkshire Hathaway Inc. Class B | |

Alphabet Inc. Class A | |

Bank of America Corp. | |

Masco Corp. | |

Ecolab Inc. | |

Kellogg Co. | |

Charles Schwab Corp. | |

Intercontinental Exchange, Inc. | |

Etsy, Inc. | |

Bank of New York Mellon Corp. | |

Emerson Electric | |

Domino's Pizza, Inc. | |

Roper Technologies, Inc. | |

Harley-Davidson, Inc. | |

Gilead Sciences, Inc. | |

Altria Group, Inc. | |

Corteva, Inc. | |

Pfizer Inc. | |

Biogen | |

Intuit Inc. | |

BlackRock, Inc. | |

Nike, Inc. Class B | |

CME Group Inc. Class A | |

The Estee Lauder Companies Inc. Class A | |

Cheniere Energy Partners, L.P. | |

Autodesk, Inc. | |

Tradeweb Markets Inc. | |

Northern Trust | |

Thermo Fisher | |

Amgen Inc. | |

General Dynamics | |

Campbell Soup Co. | |

MarketAxess Holdings Inc. | |

Agilent Technologies, Inc. | |

Waters Corp. |

All in all, we have 48 firms that pass our very first criteria.

Data from Morningstar. Dataset after 12/2022 only contains U.S. stocks.

Step Two: Historical Valuation in the EVA Framework

We believe that the most widely used valuation multiples are terribly flawed. See this article on why we consider the Future Growth Reliance metric the best-of-breed sentiment indicator that addresses accounting distortions, thus gives us a true picture of which wide-moat companies seem attractively valued in historical terms. We want to buy our top-quality targets when the baked-in expectations are low, since that is when surprising on the upside has the highest probability. As investment is a game of probabilities, all we can do is stack the odds in our favor as much as possible.

19 of the 48 stocks survived this second step. Here's the list:

Company Name | Ticker |

Agilent Technologies, Inc. | |

Amgen Inc. | |

Autodesk, Inc. | |

Bank of America Corp. | |

Cheniere Energy Partners, L.P. | |

CME Group Inc. Class A | |

Comcast Corp. Class A | |

Corteva, Inc. | |

Etsy, Inc. | |

Harley-Davidson, Inc. | |

MarketAxess Holdings Inc. | |

Northern Trust | |

Pfizer Inc. | |

Polaris Inc. | |

Charles Schwab Corp. | |

Tradeweb Markets Inc. | |

U.S. Bancorp | |

Veeva Systems Inc. Class A | |

Wells Fargo & Co. |

We are rather strict when it comes to historical valuation. There are stocks that unquestionably fail both our short- and long-term tests. There are some targets, however, that may look attractively valued if you only focus on the short-term (like the last 5 years), but the longer you zoom out, the more you lose your appetite. It comes down to personal preference where you draw the line. For us, only those stocks are allowed to appear on the heat map in our third step that seem attractively valued in both a short-term and long-term context. (We go back as far as 20 years, calculate averages and medians on different time frames, and let our algorithm do the ruthless work.)

Step Three: The Heat Map of the most investable wide-moat stocks

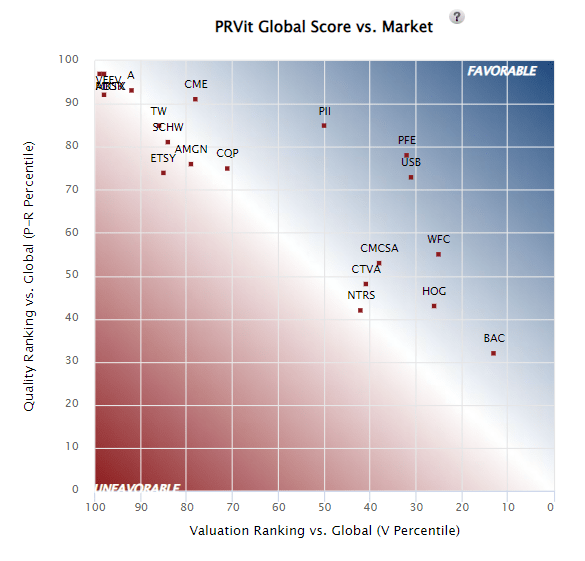

Seeing the stocks of our shortlist on a heat map with a quality and valuation axis is something that can prove very useful when we need to make a decision on which candidates to analyze thoroughly. As explained in our previous article, we use the PRVit (Performance-Risk-Valuation investment technology) model of the EVA Dimensions team.

All in all, PRVit is a multifactor quantitative stock selection model based on EVA-centric measures of Performance, Risk, and Valuation. It first estimates the fundamental value of a company based on its risk-adjusted EVA performance (shown on the vertical axis) and then compares it to its actual valuation (shown on the horizontal axis). All factors in this model were chosen heuristically based on common sense, and not by data mining, yet strong and statistically significant backtests prove the soundness of the PRVit approach both in the U.S. and globally. (See the details here).

Here is the heat map as of July 5:

Institutional Shareholder Services Inc.

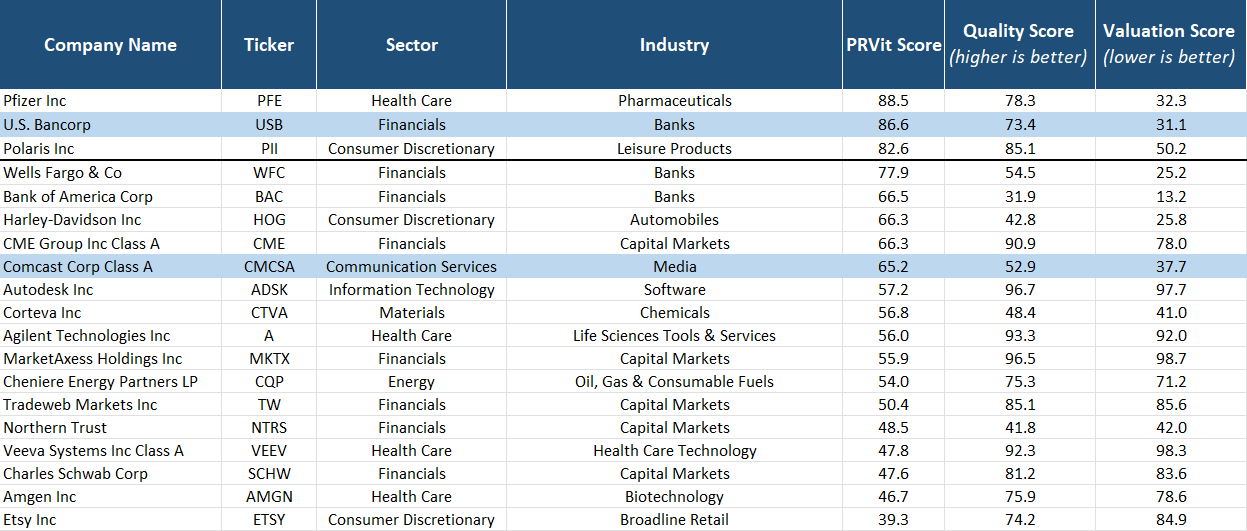

We also present the results in a table format to make your decision easier.

Institutional Shareholder Services Inc., Morningstar

(Stocks highlighted in light blue are Morningstar's 5-star-rated U.S. wide-moat names that survived the second step of our process.)

In PRVit, the factors are grouped into three categories: Performance, Risk, and Valuation. Each company has a composite 0-100 score in each category, where higher is better for Performance and lower is better for Risk and Valuation. We believe that stocks in the upper quintile of the PRVit ranking (with a PRVit score above 80) are worth a closer look.

We plan to run this three-step process on a monthly basis and publish the shortlist of targets it produces. If you don't want to miss any of these pieces, please scroll up and click "Follow".

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DIS, GOOGL, DPZ, BLK either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.