Commvault Looks To Be Resilient To Macro Slowdown

Summary

- Commvault provides cloud and on-premises data protection software and related services.

- The firm has produced low total revenue growth, but improving operating income and strong free cash flow as it transitions to a cloud-first approach.

- CVLT is generating ARR growth for its Metallic system and appears resilient to macro slowdown fears due to the mission-critical nature of its products.

- My outlook is a Buy at around $72 per share.

- Looking for more investing ideas like this one? Get them exclusively at IPO Edge. Learn More »

Orhan Turan

A Quick Take On Commvault Systems

Commvault Systems (NASDAQ:CVLT) provides various on-premises and cloud data storage and recovery technologies.

I previously wrote about Commvault with a Hold outlook.

The firm’s strong cash flow generation, expected stock buybacks and continued progress toward a cloud-first approach for mission-critical functions should help mitigate the potential effects of macro slowdown risks on its stock.

My outlook on CVLT in the near term is a Buy at around $72 per share.

Commvault Overview

Tinton, New Jersey-based Commvault was founded to provide organizations with various data protection, backup, and recovery solutions.

The firm is headed by Chief Executive Officer, Sanjay Mirchandani, who was previously CEO of Puppet and SVP Asia Pacific Japan for VMware.

The company’s primary offerings include:

Backup & recovery

Disaster recovery

File storage optimization

Data governance

eDiscovery & compliance

Managed services

Security

The firm acquires customers via its direct and inside sales and marketing teams, as well as through partner referrals.

CVLT counts more than 100,000 customers and 7,000 ecosystem partners worldwide.

Commvault Systems’ Market & Competition

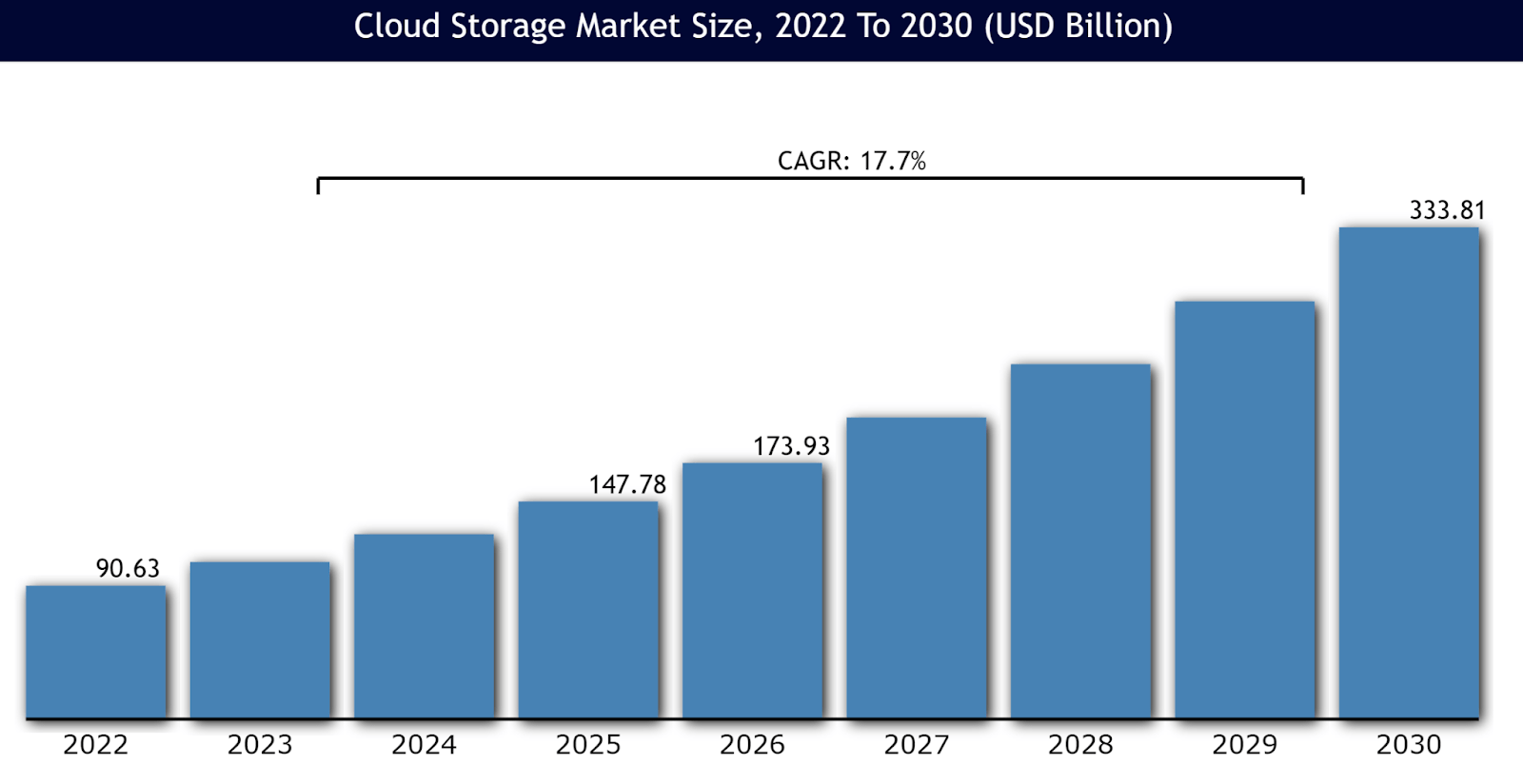

According to a 2023 market research report by Vantage Market Research, the global market for cloud storage services (as a proxy for data protection software and services) was an estimated $90.6 billion in 2022 and is forecast to reach $333.8 billion by 2030.

This represents a forecast CAGR of 17.7% from 2023 to 2030.

The main drivers for this expected growth are the growing demand for enterprises for ever larger amounts of data and a rising number of remote-located employees and contractors needing access to relevant data stores.

Also, a key challenge for the industry is to effectively defend against security threats and improve data privacy for corporate and personal data.

The chart below shows the historical and projected market growth for the cloud storage industry from 2022 to 2030.

Cloud Storage Market (Vantage Market Research)

Major competitive or other industry participants include:

Amazon

Alphabet

Microsoft

Dell EMC

IDrive

pCloud

Dropbox

Icedrive

NordLocker

Others

The company also provides on-premises storage solutions.

Commvault’s Recent Financial Trends

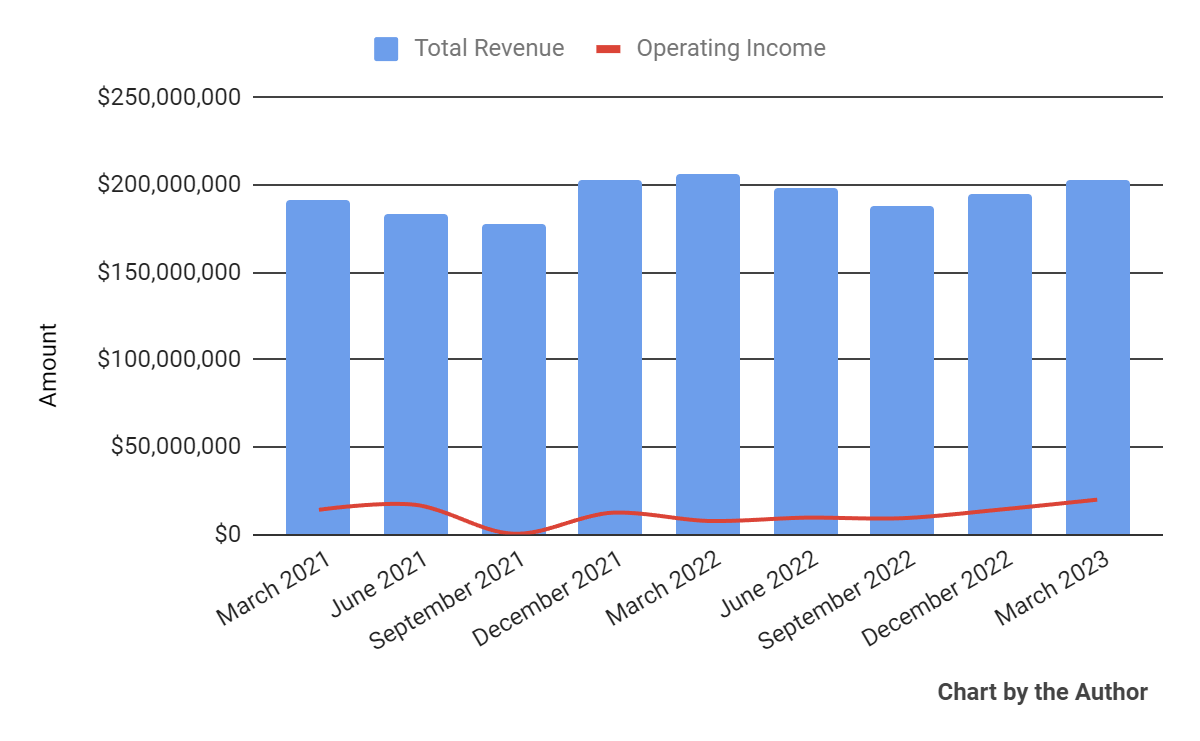

Total revenue by quarter has fallen slightly YoY; Operating income by quarter has increased more recently.

Total Revenue and Operating Income (Seeking Alpha)

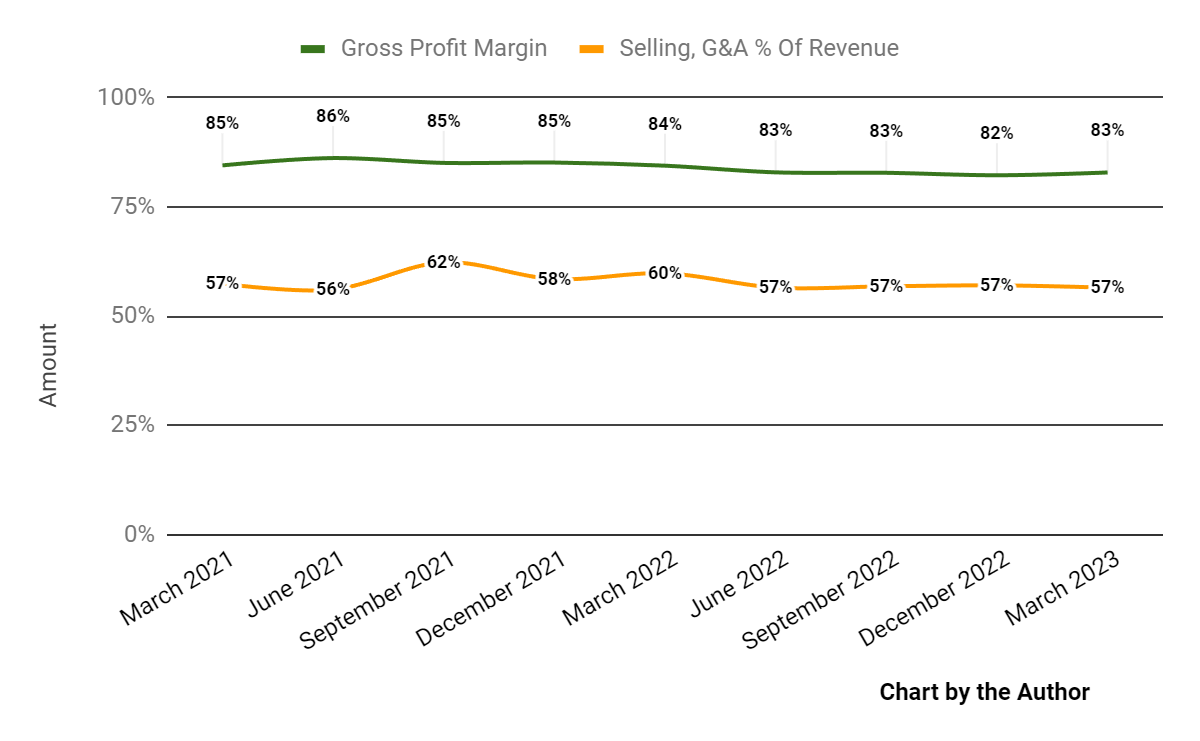

Gross profit margin by quarter has trended lower in recent quarters; Selling, G&A expenses as a percentage of total revenue by quarter have also trended lower YoY.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

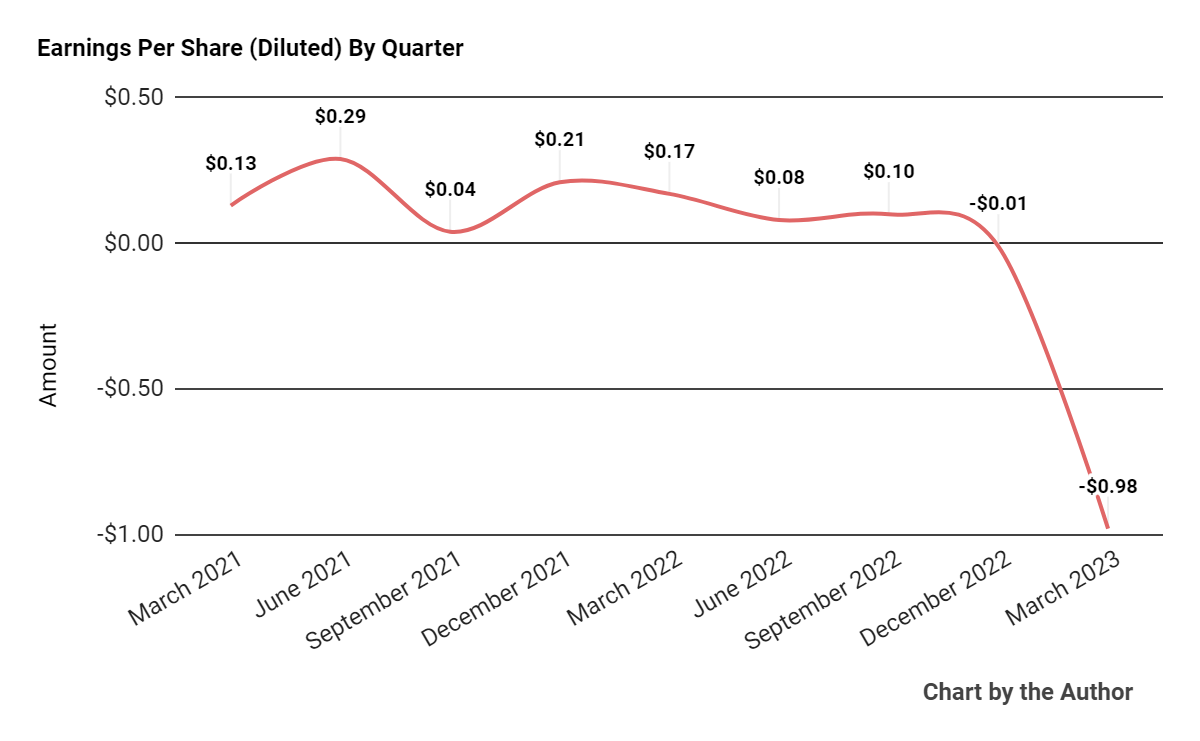

Earnings per share (Diluted) have worsened recently.

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

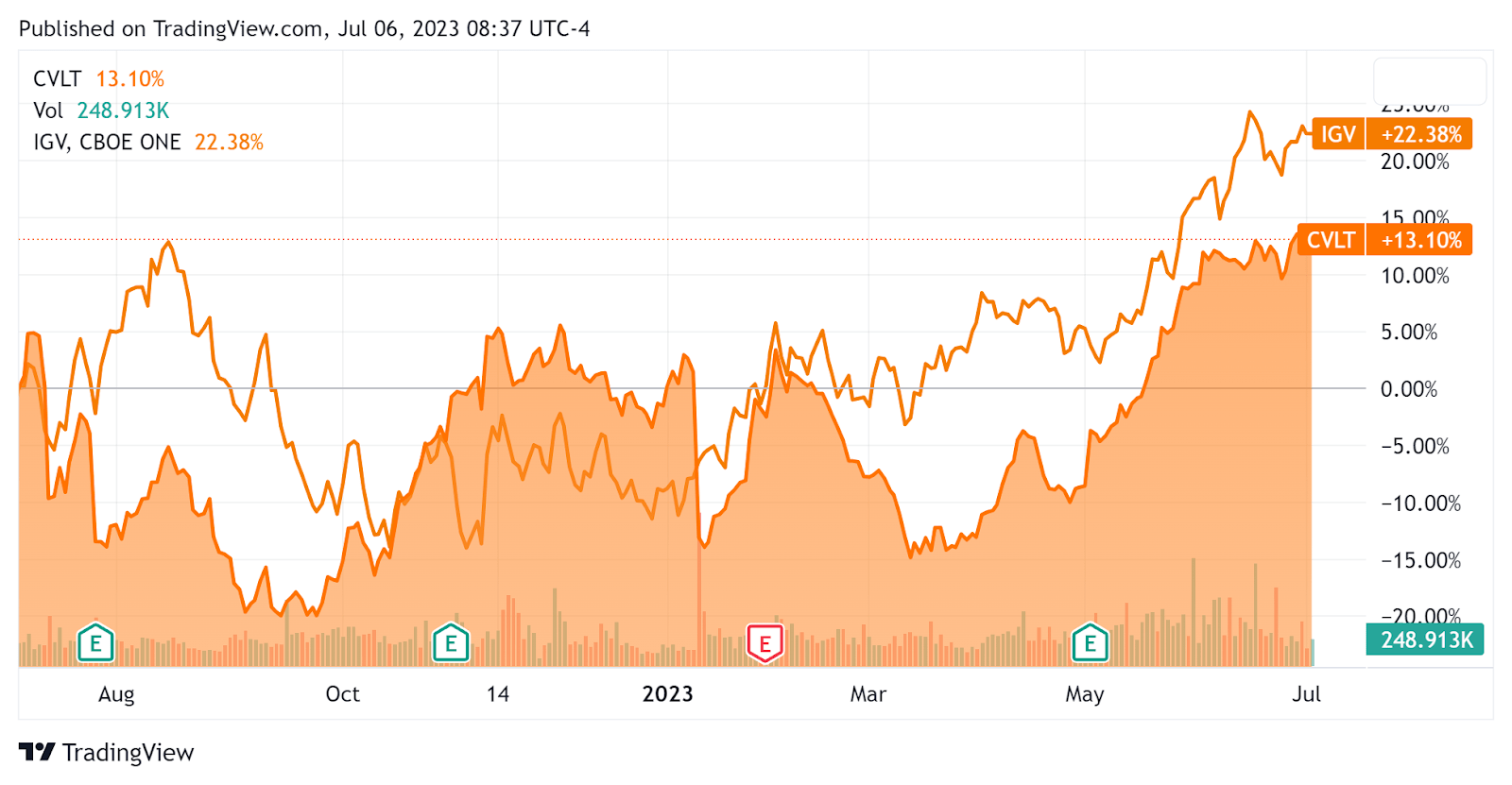

In the past 12 months, CVLT’s stock price has risen 13.1% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) rise of 22.38%, as the chart indicates below.

52-Week Stock Price Comparison (Seeking Alpha)

For the balance sheet, the firm ended the quarter with $287.8 million in cash and equivalents, and no debt.

Over the trailing twelve months, free cash flow was an impressive $167.1 million, during which capital expenditures were only $3.2 million. The company paid $105.7 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Commvault

Below is a table of relevant capitalization and valuation figures for the company.

Measure (TTM) | Amount |

Enterprise Value/Sales | 3.7 |

Enterprise Value/EBITDA | 45.9 |

Price/Sales | 4.1 |

Revenue Growth Rate | 2.0% |

Net Income Margin | -4.6% |

EBITDA % | 8.1% |

Net Debt To Annual EBITDA | -4.5 |

Market Capitalization | $3,190,000,000 |

Enterprise Value | $2,910,000,000 |

Operating Cash Flow | $170,290,000 |

Earnings Per Share (Fully Diluted) | -$0.81 |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

CVLT’s most recent Rule of 40 calculation fell sequentially to 10.0% as of Q1 2023’s results, so the firm needs improvement in this regard, per the table below.

Rule of 40 Performance | FQ3 2023 | FQ4 2023 |

Revenue Growth % | 4.3% | 2.0% |

EBITDA % | 6.7% | 8.1% |

Total | 11.0% | 10.0% |

(Source - Seeking Alpha)

Commentary On Commvault

In its last earnings call (Source - Seeking Alpha), covering Q1 2023’s results, management highlighted the growth of its Metallic offering reaching an annual run rate for recurring revenue of $100 million.

Its total ARR rose 15% YoY while adding more than 600 subscription/SaaS customers in the quarter.

Notably, management believes that ‘on-prem and SaaS are not mutually exclusive’, since customers migrating to the cloud still require services to ‘protect and manage data that is distributed and fragmented across clouds, regions, applications, services, and datacenters.’

The company’s SaaS net dollar retention rate was 125% and its term-based result was 107%, indicating reasonably strong product/market fit and sales & marketing efficiency for its SaaS product.

Total revenue for FQ4 2023 fell by 1.2% YoY and gross profit margin dropped 1.6%. Revenue from customers with greater than $100,000 spend accounted for 72% of software revenue.

Selling, G&A expenses as a percentage of revenue dropped 3.3%, a positive signal of greater efficiency, while operating income rose sharply by 158.4% YoY.

Looking ahead, total revenue for fiscal 2024 is expected to be $810 million at the midpoint of the range, or 3.2% growth over FYE 2023.

Free cash flow is expected to reach $170 million, and the Board approved ‘a refresh of our stock purchase authorization for up to $250 million of stock.’

The company's financial position is strong, with ample liquidity and no debt on the balance sheet, combined with strong free cash flow.

CVLT’s Rule of 40 performance is in need of improvement, with low revenue growth the chief culprit.

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below.

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I’m most interested in the frequency of potentially negative terms, so management or analyst questions cited ‘Uncertain’ once, ‘Challeng[es][ing]’ three times, ‘Macro’ four times and ‘Drop’ once.

The negative terms refer to the ‘unsettled’ macro environment the company is operating in, which is indicative of its 3% forward revenue growth guidance.

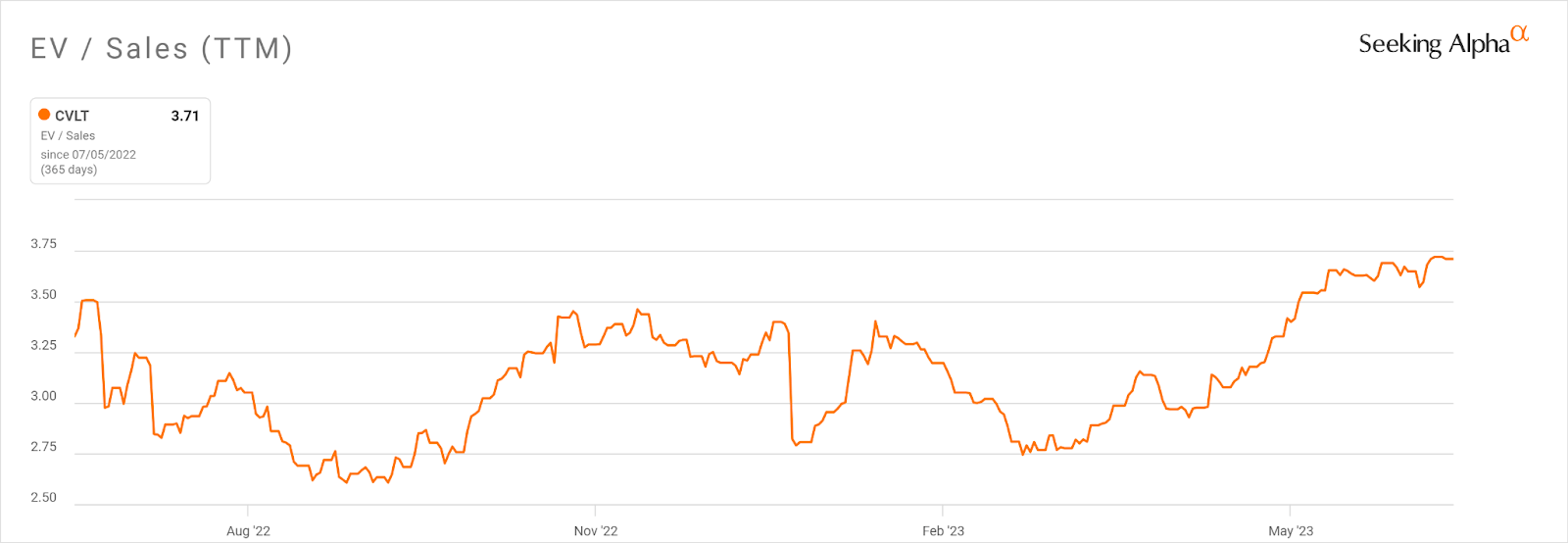

Regarding valuation, in the past few months, the firm's EV/Sales valuation multiple has risen markedly, as the chart from Seeking Alpha shows below.

EV / Sales Multiple History (Seeking Alpha)

While it may be difficult to pinpoint the exact reason for the increase in valuation multiple, the firm may be seeing stronger growth resiliency for its line of products compared to competitors.

Also, management expects to continue ‘repurchasing more than 75% of our annual free cash flow’, which based on its forward guidance, would be approximately $128 million in fiscal 2024.

While the primary business risk to the company’s outlook is the uncertain macro environment, the firm’s strong cash flow generation, expected stock buybacks and continued progress toward a cloud-first approach for mission-critical functions should help mitigate macro risks impacting its stock.

My outlook on CVLT in the near term is a Buy at around $72 per share.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis.

Get started with a free trial!

This article was written by

I'm the founder of IPO Edge on Seeking Alpha, a research service for investors interested in IPOs on US markets. Subscribers receive access to my proprietary research, valuation, data, commentary, opinions, and chat on U.S. IPOs. Join now to get an insider's 'edge' on new issues coming to market, both before and after the IPO. Start with a 14-day Free Trial.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.