Grifols: A Promising Buy Opportunity

Summary

- Grifols is a promising buy opportunity thanks to its potential to reduce its net debt/EBITDA ratio.

- The company's focus on deleveraging is showing results and is supported by higher savings and better margins. The plasma collection is also recovering.

- Better-than-anticipated results and a compelling valuation make Grifols a buy.

Tutye

Grifols, S.A. (NASDAQ:GRFS) is a Spain-based pharmaceutical player engaged in developing, manufacturing, and distributing blood plasma-based solutions. Since our last update, the company is now organized into four divisions (from five segments): Biopharma, Plasma Procurement, Diagnostic, Bio Supplies, and Others. Over the last months, there has been a lot of supportive news that deserves to be reported and makes Grifols, S.A. an interesting buy opportunity. We were not very lucky with our initiation of coverage even if we reported "Short-Term Turbulence;" since our latest update called the company "Needs To Deleverage," Grifols' stock price has been up by more than 20%. As a reminder, our supportive buy was due to: 1) a contrarian idea on plasma collection versus Wall Street estimates and 2) a higher cost-saving initiative with better profitability. On the contrary, our cautious approach was related to Grifols' high leverage, execution risk on aggressive M&A, and a business focused on plasma products.

Mare past analysis

Why are we supportive? And our changes in estimates.

The most relevant and recent catalyst is, without a doubt, the possible disposal of the Shanghai RAAS equity stake. Grifols hold 26.2% of the listed company, and its stake is currently valued at $1.62 billion. Here at the Lab, we are modeling a debt reduction of $1.5 billion. Grifols would potentially reduce its net debt/EBITDA ratio from 7.4x (at 2022-end, including IFRS 16) to 5.5x in 2023 (Fig 1). This is much better than our base case scenario of a 6.4x net debt/EBITDA ratio with no disposal. With this transaction, the Spanish pharmaceutical company could almost remove the €2 billion debt maturing in 2025 (Fig 3) and provide support from Wall Street's negative sentiment.

Grifols Q1 results presentation

Grifols deleverage path

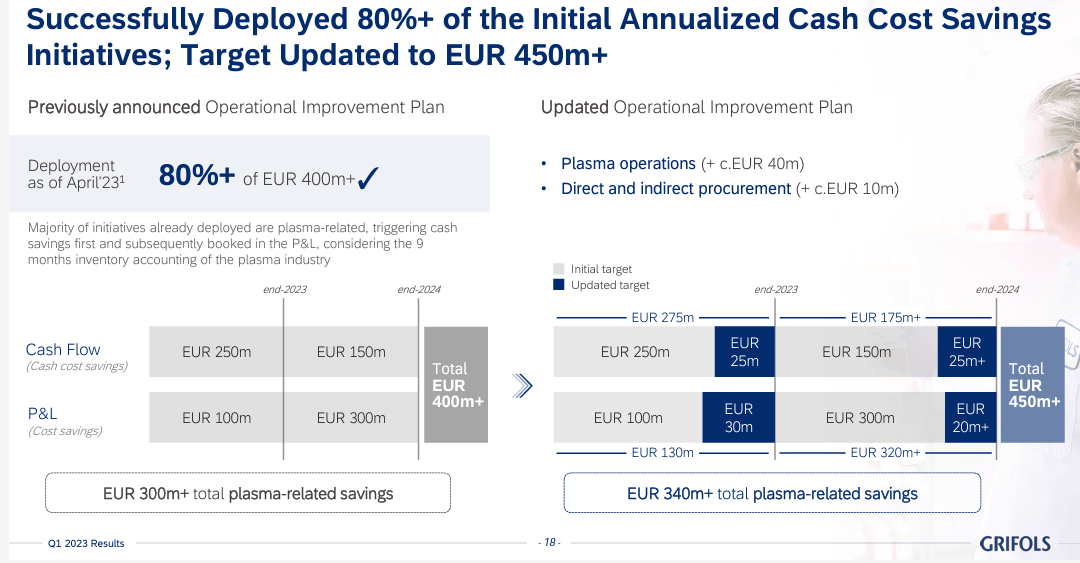

To support our thesis, Grifols debt development could go even lower with the higher run-rate savings that the company presented in the Q1 release. Looking at the latest news, in mid-February, the company communicated a €400 million cost savings initiative; however, this was upgraded to more than €450 million in Q1 (Fig 2). According to our estimates, this expected saving equals a 1.3x net leverage reduction. In detail, major savings will be derived from the following: plasma costs optimization (€340 million), lower cost at the corporate level (€60 million), supply chain efficiencies (€50 million), workforce reduction, especially in the US (in Q1, the company already took a negative one off charge for €140 million to restructure the US division).

Fig 2

Grifols higher saving

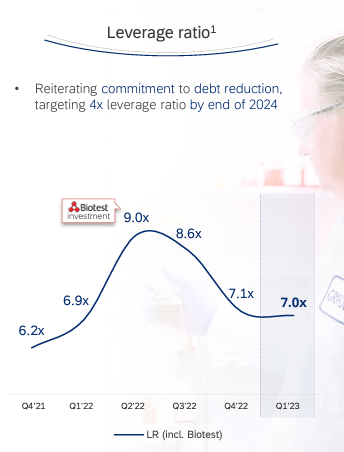

The company's deleveraging has been a top priority and is currently delivering. Grifols forecasted a 4x leverage by 2024 (Fig 3), which we believe is achievable. Dividends are also on pause until the deleveraging is completed. An earnings recovery trajectory also supports Grifols' debt story evolution.

Fig 3

Grifols 4x net debt target

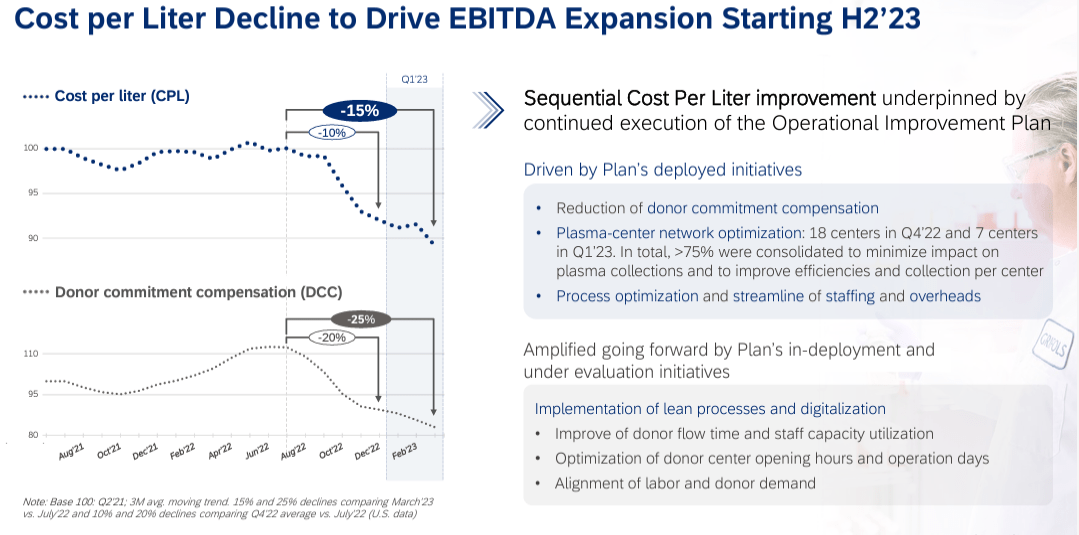

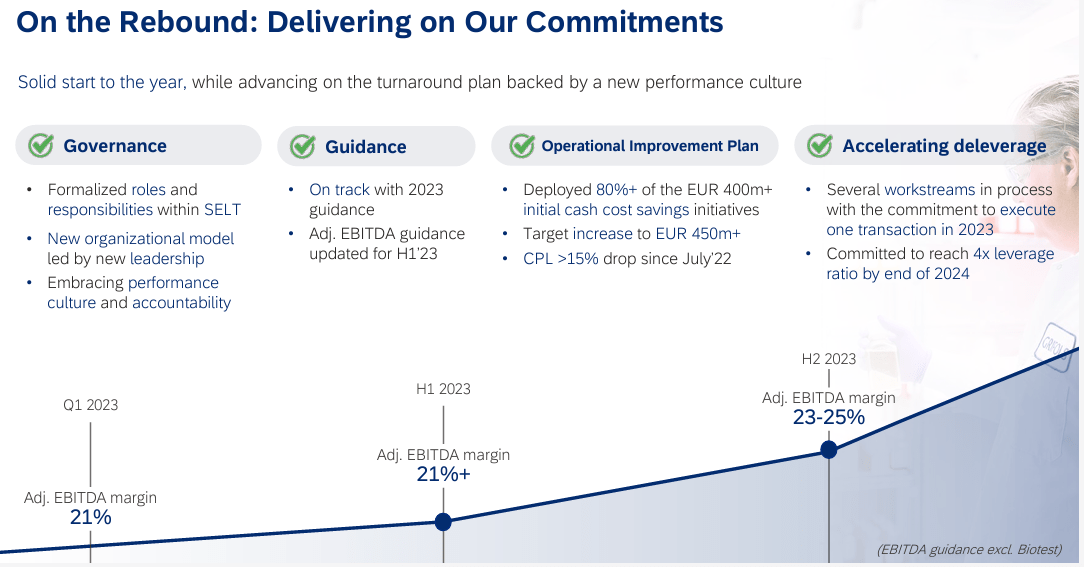

Indeed, plasma supply trends are now recovering, Mexican plasma donations are now allowed in the United States, and as a result, donor fees are reducing, positively impacting Grifols' P&L. In the latest quarter, plasma collection grew by 11%, and cost per liter decreased by >15% (Fig 4). Grifols expects an EBITDA margin rebound already in H2 (Fig 5), and we believe the company will provide higher guidance for the year. In addition, we are not forecasting new CAPEX, given the former investments.

Fig 4

Cost per liter evolution

Fig 5

Grifols H2 margin

Conclusion and Valuation

Since 2019, plasma collection capacity has increased with expansions around the globe, and more than 60 plasma collection centers have opened (25 were dismissed). This leaves upside scope once the plasma collection market normalizes (the pandemic outbreak still has some impact, given that there are fewer donors compared to the pre-COVID-19 level). Plasma availability has been the primary company challenge, not the patient demand. This is a key consideration and will support Grifols' earning recovery story. We also positively report the latest news on Canada. This is a better M&A approach than the Grifols' latest acquisition, and is also more prudent. The company has the option to buy Canadian Plasma centers by 2025-end, while also having the possibility to open five additional centers to make the country self-sufficient in plasma.

After turbulent years, plasma collection is recovering. In addition, the company achieved Q1 results better than anticipated, with a higher cost-saving target and a better view of the 2023 H2 margin. The Grifols margin recovery story is on track and supported by a clear path to deleveraging organically (thanks to a solid free cash flow generation) and inorganically (with Shanghai RAAS potential disposal). We believe that already in 2023 end, the company could achieve a net debt/EBITDA of 4.2x (3.5x in 2024 and below 3x in 2025). Grifols' closest competitor (CSL Limited) trades at 25x EV/EBITDA with a PE >40x. Our Spanish pharmaceutical company's 2023 low-end EBITDA target is €1.2 billion. We arrive at a debt of €7.9 billion by guiding FCF estimates and Shanghai RAAS disposal. Valuing Grifols with a 17.5x EV/EBITDA, in line with its historical average, we arrive at an equity value of €13.1 billion versus a current market cap of €7 billion. This should support a buy rating of €20 per share.

Risks to consider: 1) capital structure evolution and credit rating development (Grifols is still a company with an aim to reach a net debt/EBITDA of 4x in 2024) - 65% of debt is at fixed interest rates; however, raising rate might still impact the company P&L, 2) Shanghai RAAS exit (again this is related to the company deleveraging plan) and we might associate regulatory risks when a pharmaceutical transaction is involved, 3) higher restructuring costs, 4) plasma collection evolution, and 5) donor fee price.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.