Prologis: Strong Fundamentals But Not Sufficient To Justify The Valuation

Summary

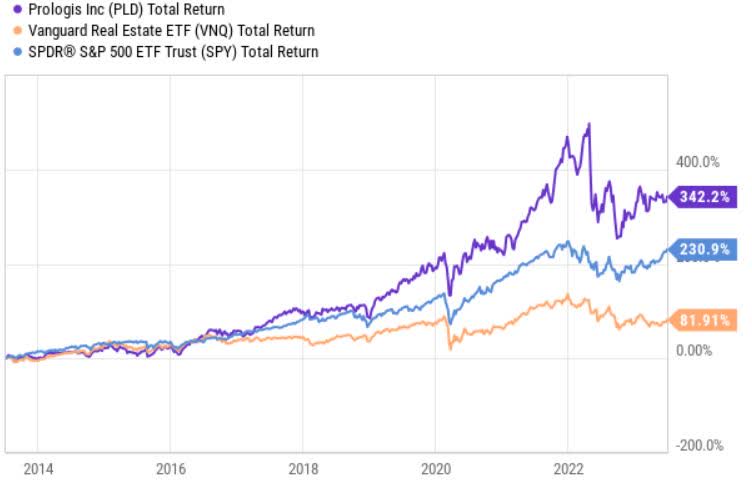

- Prologis, the largest publicly traded industrial REIT, has consistently outperformed the overall REIT market and the S&P 500 over the past decade.

- Despite high valuations, PLD's strong position, supported by factors such as significant e-commerce exposure and resilient occupancy rates, makes a short position risky.

- PLD's underpriced lease agreements and strong balance sheet further bolster its potential for long-term value creation and growth.

- However, the current valuation multiples create a very tough base from which to continue delivering alpha performance.

- Rich valuation in conjunction with recessionary signals and higher interest costs warrant a hold position.

Maxiphoto

Prologis (NYSE:PLD) is the largest publicly traded industrial REIT carrying over $115 billion in market cap. It is also included in major equity indices such as the S&P 500 ETF Trust (NYSEARCA:SPY) and the ProShares S&P 500 Dividend Aristocrats ETF (NOBL).

Ycharts

Due to its size and remarkable history, PLD has become a common investment darling among many investors, who seek not only dividends but also returns via capital appreciation. In the past 10 year period, PLD has outperformed both the overall REIT market and the S&P 500.

Ycharts

Even looking at the more recent history, which includes the FED's decision to suddenly impose restrictive monetary policy measures, we can see how PLD has still managed to outperform REIT market and deliver solid return somewhat in line with the S&P 500.

All this in combination with the dividend aristocrat prestige and some clear secular tailwinds on the industrial real estate front warrant relatively high valuations (at least higher than compared to the average REIT names).

However, in my humble opinion, the current valuation of PLD creates a difficult base from which to continue delivering alpha performance. Let me explain this in a bit more detail.

Key reasons why to not go against PLD

Before jumping to the argumentation of overvaluation (or very rich valuation), I want to make clear that currently I do not see how an outright short position could be substantiated with solid arguments and financial data.

In other words, PLD is set in a position, where the surrounding tailwinds and secular demand dynamics support long-term value creation. Also, looking at the FFO consensus estimates, we can see close to double digit FFO growth for the next couple of year ahead. In this context, a short position would seem very risky and mostly dependent on quarterly earnings surprise or a systematic shock in the overall equity / REIT market space.

The following elements capture the resiliency and long term story of PLD quite nicely:

- Significant portfolio exposure (~33%) to e-commerce renders the cash flows more durable and attaches a favourable long-term growth component. For example, the penetration of e-commerce of the total U.S. retail goods is expected to increase by an average of 1 % per year over the next 5 years. The growth of e-commerce introduces rather favourable conditions for a sustained demand as, typically, e-commerce uses 3x as much logistics space as brick-and-mortar solutions.

- Resilient occupancy rates landing at 98% in Q1, 2023. In the past 12 year period, PLD has on average maintained occupancy rate of 96%, which is a testament of the underlying attractiveness and need for PLD's industrial properties. The fact that on a YTD basis (until May, 2023), PLD had received more proposals covering higher chunk of the available (or soon to be available) space than in the pre COVID-19 year (2019) confirms the PLD's portfolio strengths.

- Underpriced lease agreements create an additional opportunity of growth for PLD. According to the Management, if all leases were to reset to market today, rents would be 68% higher. Granted, it will not be possible to quickly tap into this hidden value and enjoy a sudden surge in the lease cash flows as most of PLD's contracts are of a long-term nature. However, the most recent like-for-like performance indicates that the majority of the prevailing lease contracts are truly underpriced and offer an opportunity for decent organic growth.

- Fortress balance sheet. As of Q1, 2023, PLD had one of the strongest balance sheets in the sector with net-debt-to-EBITDA at 4.3x, debt ratio of 19.1% and a sizeable liquidity position of $5.7 billion. In times like these, when the overall lending conditions have become tight, a robust balance sheet allows to weather the storm without issuing debt at overly unfavourable terms and, at the same time, provides a luxury to scope underpriced growth opportunities.

Considering the aforementioned, a short sale of PLD is obviously out of the questions.

Key reasons why to not expect alpha from PLD at these valuation levels

As elaborated earlier, the strong fundamentals and excellent track-records of PLD has rendered the stock richly valued, which, in turn, imposes notable headwinds for prospects of alpha performance. Put differently, it is highly likely that PLD will continue generate positive returns (unless there is a material market correction) and make stable dividend payments, but the odds are stacked against of those total returns exceeding the benchmark (i.e., overall REIT market).

There are a couple of reasons, which, in my opinion, justify a hold or decreased exposure towards PLD stock.

- Aggressive valuation. Currently, PLD is priced at (TTM) P/FFO of 22.3x, which is 82% above sector median and 21% above the benchmark consisting of pure play U.S. equity industrial REITs. On a forward looking basis, the P/FFO metric still trades considerably above the sector median (i.e., 43% above). Interestingly, that the PLD's current P/FFO multiple implies that the valuations exceed those of the 5-year average, which includes a period of depressed interest rates. Namely, the market seems to totally ignore the notion that for PLD, the question of interest rates really dictates the long-term value of future earnings and asset prices as the underlying cash flows closely resemble bond-like characteristics.

- Headwinds from higher interest rates. While the fact that the rates have gone up does not seem to impact the PLD's valuation levels, it is clear that we will inevitably see some challenges on the cash flows front stemming from more expensive debt financing. In PLD's case, there is a meaningful room for gradual convergence to a higher (more market reflective) cost of debt. Currently, the weighted average cost of debt is at 2.6%, which in the context of recently stipulated financings (e.g., syndicate loans and publicly traded bond YTM revolving around ~5%), implies materially higher interest costs down the road. Moreover, gradually more unfavourable interest rates will put a pressure on the FFO as the spread between the cost of financing and current (including future properties via development or M&A) yields narrows. For example, about two weeks ago PLD acquired ~14M square feet of industrial properties for $3.1B in cash at a cap rate of ~4%, which is already lower than the prevailing cost of debt levels.

- Recessionary signals. There is a gradual buildup of consensus towards the economy falling at a recessionary territory. Against the backdrop of surging interest rates, services and manufacturing PMI data with a negative trajectory near or below 50-mark, inverted yield curve and other leading economic indicators suggesting a slowdown in the business activity, there is an elevated probability of PLD facing additional hardship in the foreseeable future. Considering that 28% of PLD's portfolio is exposed to cyclical sectors (e.g., automotive, appliances, construction and home goods), we could expect some drag on the future FFO figures.

The bottom line

In my opinion, PLD is richly valued, where if we factor in elements of consequences from a recession, increasing interest costs and PLD's exposure to cyclical sectors of the economy, the prospects of alpha performance seem rather weak.

However, given the underlying strengths of PLD and its exposure to secular tailwinds, there is no substantial case for going short the stock despite the aggressive valuations. So, it is a hold for me.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.