Bandwidth: Leading CPaaS Provider Poised For Growth In The Cloud Communication Market

Summary

- Bandwidth Inc. is a leading CPaaS provider, has seen increased demand for its services due to the COVID-19 pandemic's impact on remote work and collaboration tools.

- BAND is also focusing on AI-driven customer experience interactions and has launched a product called Maestro to capitalize on this growth.

- Bandwidth's strong customer retention and the growing demand for cloud communication services position it well for future growth.

- It is actively investing in expanding presence in Europe and other international markets to drive this growth.

- I have an end of year price target of $20 on the stock.

JLco - Julia Amaral

Thesis

Bandwidth Inc. (NASDAQ:BAND), a leading CPaaS provider, offers a global network that enables seamless integration of voice, messaging, and emergency services into applications. The COVID-19 pandemic has expedited the adoption of collaboration tools and remote work infrastructure, resulting in increased demand for cloud communication services. BAND's differentiation lies in its comprehensive voice-CPaaS capabilities, global reach, and scalable capacity. I view the stock as a buy and have an end-of-year $20 price target based on an estimated $668 million in CY24 revenue and a ~1.5x EV/sales multiple.

Q1 Review & Outlook

Bandwidth reported better-than-expected 1Q23 results, surpassing lowered expectations in terms of revenue and non-GAAP earnings per share (EPS) estimates. The company's revenue was 4% higher than consensus estimates, while the non-GAAP EPS was $0.03 higher. However, the guidance for 2Q23 indicates that adjusted revenue, excluding A2P charges, is expected to remain relatively flat with a modest 1% year-over-year increase. This is due to challenging macroeconomic conditions impacting core UCaaS voice usage. The management emphasized that the company has made significant progress in reducing its debt leverage by paying off $65 million in convertible debt on top of the $160 million paid off in the fourth quarter.

The management believes that conversational AI has the potential to drive a significant increase in customer experience interactions. Bandwidth highlighted its product called Maestro, which enables customers to integrate their UCaaS platforms with top-tier AI solutions. The management sees this as a favorable position to capitalize on the anticipated growth in customer experience interactions. It is worth noting that Bandwidth Maestro is a cloud communications platform that allows chief information officers to integrate real-time voice applications across their unified communications, cloud contact center, and AI platforms.

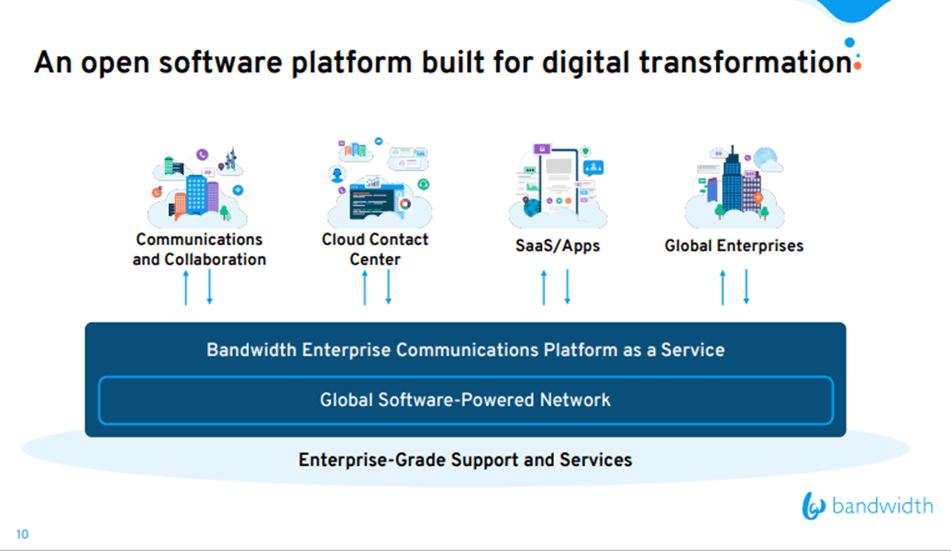

Focused CPaaS Provider

Before the emergence of CPaaS, businesses faced significant challenges when trying to incorporate communication functions into their applications. They often had to directly engage with carriers, which involved complex and costly agreements. However, CPaaS has revolutionized this landscape by offering a cloud-based development platform that eliminates the need for organizations to build or install their own network infrastructure and interfaces. By integrating CPaaS into their applications, websites, and business workflows, businesses can streamline communication delivery.

BAND is a prominent player in the CPaaS industry, specializing in voice-based services. The company offers software APIs that enable businesses to integrate voice, messaging, and emergency services into their products and automate various communication processes. BAND's unique advantage lies in owning and operating a global network, which sets them apart from other CPaaS providers. In addition to their nationwide IP voice network in the US, BAND has expanded its reach through the acquisition of Voxbone, incorporating the European-based company's international IP voice network into its portfolio. This strategic move has further increased BAND's footprint and scale in the market. BAND's customers include many of the cloud communications leaders in meetings, UCaaS and CCaaS, such as Google, RingCentral, Inc. (RNG), Microsoft Corporation (MSFT) and Zoom Video Communications, Inc. (ZM).

Company Presentation

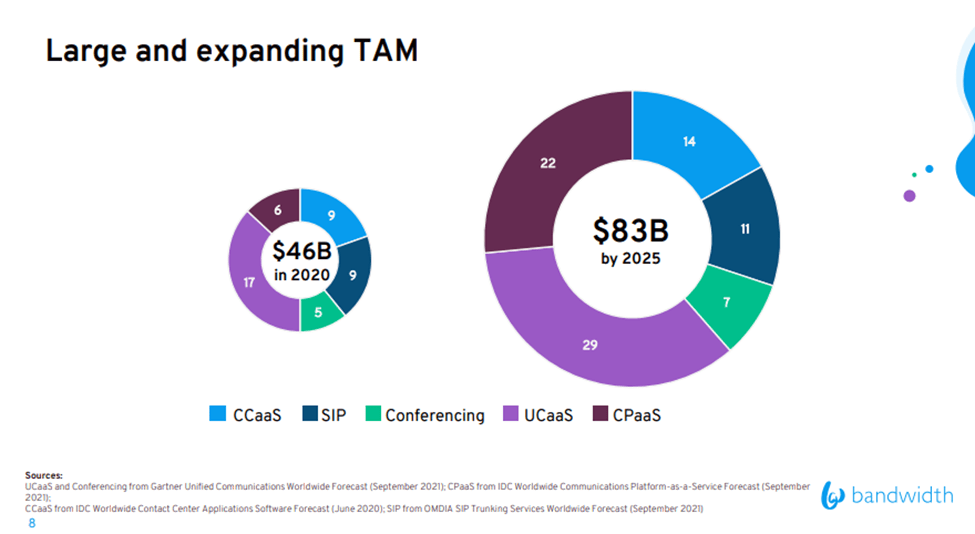

TAM & Differentiation

According to IDC, the CPaaS market is expected to expand from $14.3 billion in 2022 to $29.7 billion by 2026. IDC's analysis suggests that North America accounts for 60% of the total TAM for CPaaS globally, and this market is expected to reach approximately $18 billion by 2024. Among the various segments of CPaaS, voice CPaaS experiences slower growth compared to messaging or video CPaaS. BAND, a prominent player in the industry, anticipates a 20-25% annual growth in the voice market, primarily driven by the transition of business voice lines from traditional telecom infrastructure to cloud-based solutions.

Among the major global IP voice operators such as Verizon Communications Inc. (AZ), AT&T Inc. (T), Lumen Technologies, Inc. (LUMN), BAND stands out as the only provider offering comprehensive voice-CPaaS capabilities. BAND's competitive advantage lies in its global reach and scalable capacity, distinguishing it from competitors like Twilio Inc. (TWLO), whose revenue contribution from voice is relatively small. While there is significant investor interest in SMS-CPaaS due to Twilio's success, the complexity of public switched telephone network (PSTN) interfaces and regulatory requirements make voice-CPaaS more challenging than other offerings.

Company Presentation

Valuation & Financial Outlook

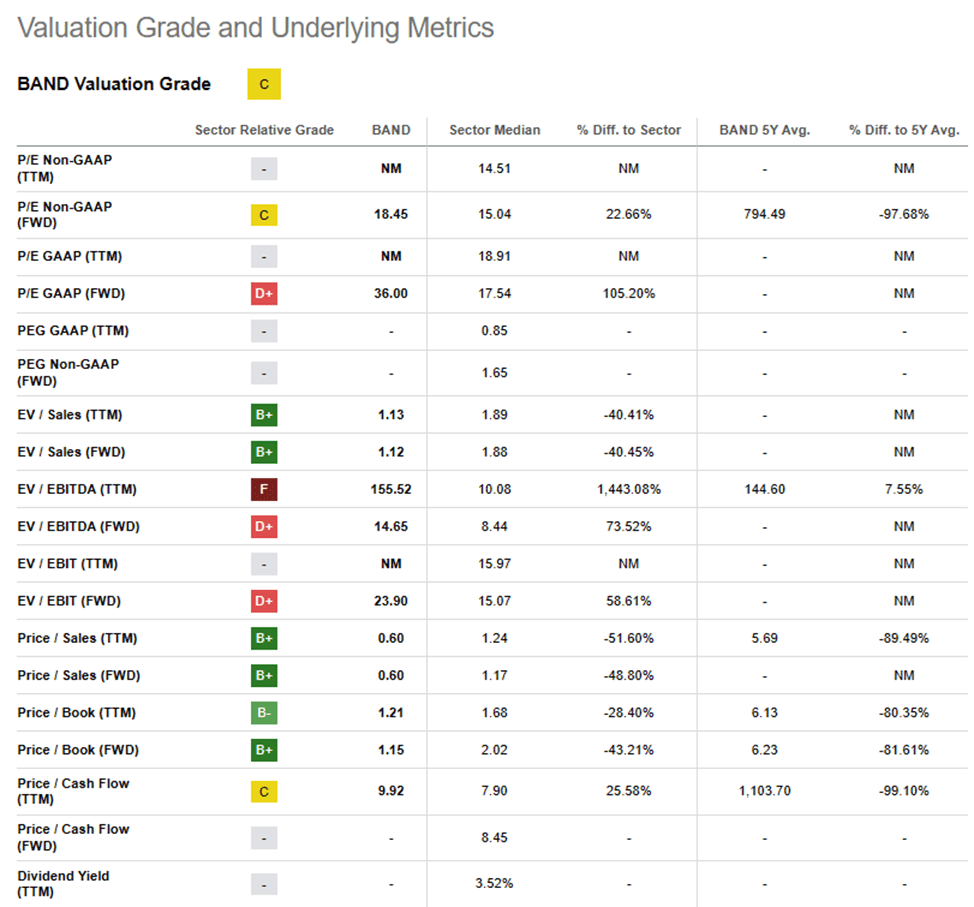

I think international expansion has the potential to fuel BAND's growth in the medium term, particularly considering the demand from its Direct Enterprise Solution customers who require a global presence. Furthermore, the international SMS market offers more favorable pricing dynamics. As BAND continues to develop this aspect of their business, with expectations to reach approximately 10% of sales by 2026 compared to around 5% in 2022, there is a possibility of experiencing an expansion in gross margins. My end-of-year $20 price target is based on an estimated $668 million in CY24 revenue and a ~1.5x EV/sales multiple. The multiple is lower than sector median owing to macro uncertainty driving pressure on BAND's near-term revenue outlook.

Seeking Alpha

Risks

BAND faces competition from CPaaS rivals, particularly in the voice segment, which challenges its leadership position. Moreover, while no single customer contributes more than 10% of BAND's revenue, the top 10 customers collectively account for a significant portion, approximately 30%. Losing any of these key customers could have adverse effects on the company. However, the majority of these top customers have committed to multi-year contracts, indicating a high level of customer retention.

Although BAND's primary operations are currently centered in the United States, the company is actively investing in expanding its presence in Europe and other international markets to drive future growth. This strategy exposes BAND to potential challenges related to local regulations and other risks associated with international expansion. Any missteps in executing this expansion plan could hinder the company's growth prospects in the future.

Conclusion

BAND is a leading CPaaS provider that offers a cloud-based communications platform to enterprises, encompassing services like voice, messaging, and 911-enabled phone numbers. The COVID-19 pandemic has accelerated the adoption of various technologies, such as collaboration tools and work-from-home infrastructure, driving the demand for cloud communication services. Given the substantial market opportunity and the valuation gap compared to high-growth CPaaS competitors like Twilio, I believe that BAND has significant growth potential in the coming years. I view the stock as a long-term buy and have an end-of-year price target of $20 on the stock

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.