Analog Devices: New Analog Market Leader (Rating Upgrade)

Summary

- Analog Devices, Inc. (ADI) has emerged as a joint leader in the analog market alongside Texas Instruments, largely due to its acquisition of Maxim Integrated.

- ADI's organic growth of 32.6% in 2022 surpassed the previous forecast of 6.64%, indicating a strong performance independent of the Maxim acquisition.

- Despite the current stock price surpassing my previous target, there is still considerable upside potential for ADI, with a new price target of $229 reflecting an upside of 20.65%.

Sundry Photography

In our previous coverage of Analog Devices, Inc. (NASDAQ:ADI), we examined the company's acquisition of Maxim Integrated and its implications for ADI's business. Firstly, the acquisition solidified ADI's position in the Analog market by contributing 29.5% of the combined company's revenues and increasing its market share from 9.2% to 12.8%, just behind Texas Instruments (TXN) at 19.6%. Secondly, we anticipated that ADI's integration of Maxim's power management integrated circuit ('PMIC') would enable the exploration of semiconductor opportunities in healthcare. Lastly, we expected that the synergy between ADI and Maxim would lead to improved profit margins.

In this analysis of Analog Devices, we delve into the significant impact Maxim had on ADI's revenue growth, which reached an impressive 64.2% in 2022, surpassing our initial forecast of 37% growth. Firstly, we examine the changes in market share within the analog market since our previous coverage, specifically focusing on the gap between ADI and Texas Instruments (TI). Next, we identify the segments where Maxim's influence exceeded our expectations. Additionally, we evaluate the impact of Maxim on profit margins compared to our earlier predictions. Lastly, we assess the new product releases from the past six months and compare them with the preceding six months to determine if the growth resulting from the acquisition can be sustained through a continuous stream of product innovations. Based on this information, we provide an updated revenue and margin outlook for the company.

Joint Analog Market Leader with Texas Instruments

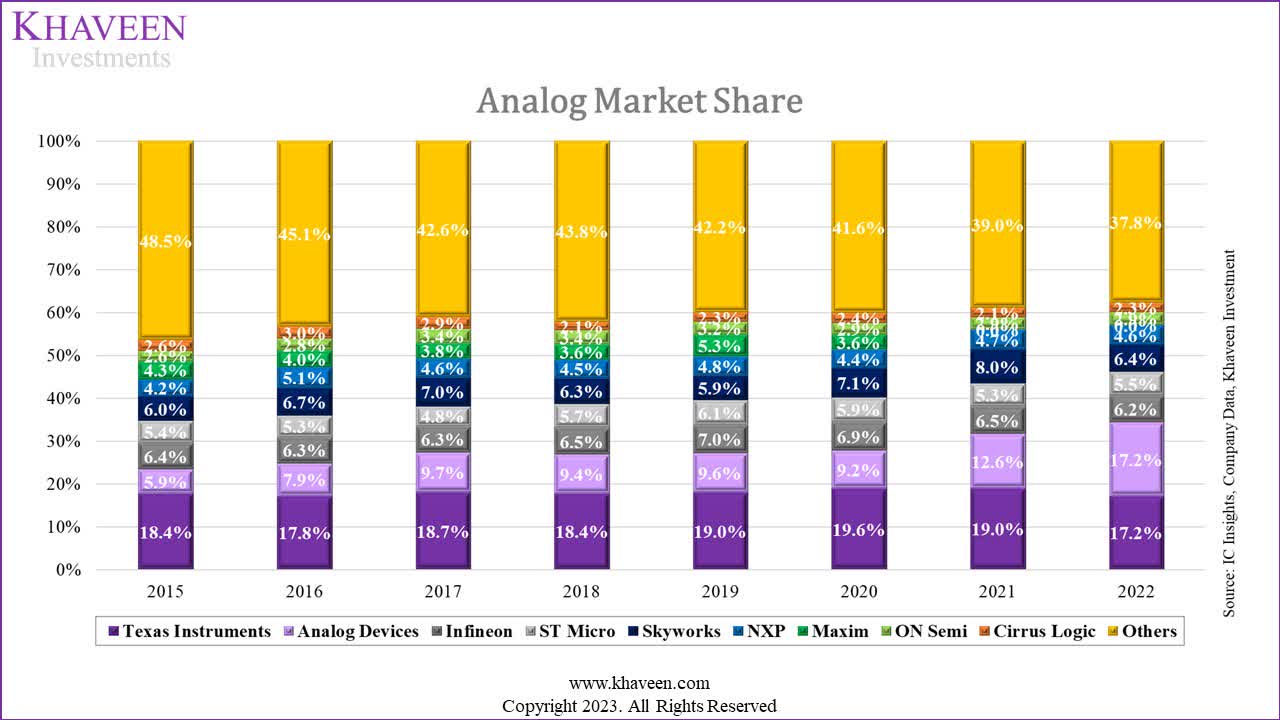

IC Insights, Company Data, Khaveen Investments

In the chart above, we calculated the analog market share in 2021 by taking each company’s analog revenues provided by IC Insights and dividing that by the total analog market revenue provided by WSTS. We estimated the 2022 analog market share by forecasting each company’s revenues (except TI) based on its most recent financial year growth rate and again divided by the analog market revenue provided by WSTS. For TI, we obtained its 2022 analog revenue directly from its annual report.

ADI’s market share in 2021 (12.6%) was relatively in line with the combined market share of ADI and Maxim in 2020 (12.8%). However, our forecasted analog market share in 2022 shows that we expect ADI to have gained significantly, with its market share expected to increase by 4.6% to reach 17.2% in 2022, joint highest with TI. We believe ADI to have gained that market share from TI, Skyworks (SWKS), and the Others, who all lost the most.

TI would have had a reduction in market share as its analog revenue growth was only 9.32% in 2022, lower than the market growth of 20.8%, whereas ADI grew 64.2% in 2022. Moreover, according to MarketWatch, automotive semiconductor sales are the “sole growth driver” for analog semiconductors due to the downturn in the semiconductor industry. Texas Instruments automotive revenue grew 30% in 2022 whereas ADI’s automotive segment grew by 101.5%. We also believe Skyworks to have lost 1.6% of its market share, which is a huge chunk of its 2021 market share (8.0%) due to its overall revenue growth also being below market growth at 7.4%. Our insights from the analog market share chart from 2015 to 2022 are as follows:

- ADI has consistently increased since 2015.

- TI has been stable over the past 8 years but dropped to its lowest level ever in 2022.

- Smaller competitors have been relatively flat.

- Other small companies have decreased their market share.

In conclusion, we believe ADI has caught up to become the joint market leader alongside TI with a 17.2% market share in the analog market in 2022. This was a combination of TI’s analog segment growing lower than the market in conjunction with ADI growing above the market. We expect ADI to gain market share in the coming years as it is pursuing the right strategy to operate in the Analog market, and this is reflected by it being the only company to consistently gain market share since 2015, whereas the market share of its competitors has either remained flat or decreased. Below, we will analyze the reasons behind ADI’s outstanding growth in 2022 and determine if Maxim played a part in boosting revenues above expectations.

Growth Driven by Maxim Acquisition

Revenue by Segment ($'000s) | 2019 | 2020 | 2021 | 2022 | 5-year Average | Our Previous Analysis 2022 Forecast |

Industrial | 3,003,927 | 3,005,585 | 4,026,909 | 6,069,332 | ||

Growth Rate % (YoY) | -4.0% | 0.1% | 34.0% | 50.7% | 23.1% | |

Automotive | 933,143 | 778,714 | 1,248,169 | 2,515,513 | ||

Growth Rate % (YoY) | -7.6% | -16.5% | 60.3% | 101.5% | 34.2% | |

Communications | 1,284,087 | 1,193,809 | 1,206,867 | 1,880,697 | ||

Growth Rate % (YoY) | 11.5% | -7.0% | 1.1% | 55.8% | 17.6% | |

Consumer | 769,908 | 624,948 | 836,341 | 1,548,411 | ||

Growth Rate % (YoY) | -17.6% | -18.8% | 33.8% | 85.1% | 11.4% | |

Total Revenue | 5,991,065 | 5,603,056 | 7,318,286 | 12,013,953 | 9,788,075 | |

Growth Rate % (YoY) | -3.8% | -6.5% | 30.6% | 64.2% | 20.6% | 33.7% |

Source: ADI, Khaveen Investments

The company’s revenue grew by 64.2% in 2022, higher than the 5-year average of 20.6% and our forecast of 33.7%. Although all segments grew above 50%, the one that stands out is the automotive segment which grew at 101.5% (20.9% of 2022 revenue). Industrial, 50.5% of 2022 revenue, grew at 50.7% and contributed 43.5% to revenue growth, the largest amongst all segments. Based on its annual report, management attributed the outstanding growth to the “acquisition, which contributed approximately 65% of the increase in total revenue year over year”. Therefore, we calculated that 41.7% of ADI’s 64.2% growth in 2022 is directly attributed to Maxim with the remaining 22.5% of the growth attributed to ADI’s organic growth, which is much higher compared to our forecasted organic growth of 6.64% from our previous coverage.

We expected ADI to benefit from integration with Maxim in terms of semiconductors in healthcare (industrial segment), however, we did not take into account the benefit of Maxim’s products for ADI’s automotive segment. In its Q4 2022 earnings briefing, the CEO of ADI, Vincent Roche previously stated that the company’s “growth in Automotive was underpinned by battery management systems”. In relation, looking at the Q4 2021 earnings briefing, the company highlighted its BMS position being supported by its Maxim acquisition.

Our BMS position is further strengthened with Maxim, we now sell to seven of the top 10 EV manufacturers, and our increased technology and product scale enables us to address new SAM.......... Maxim's strong and growing power management capabilities complement our portfolio. – Vincent Roche, CEO

Therefore, ADI’s automotive BMS portfolio which was strengthened from the acquisition of Maxim ended up being the biggest growth driver for the automotive segment, which had the highest growth rate out of all segments (101.5%). Moreover we previously identified “the company only expects revenue cross-selling opportunities from 2025 onwards”. However, ADI has already started to benefit from cross-selling opportunities as seen from management’s statement in Q4 2022 earnings briefing…

Importantly, our design pipeline is beginning to benefit from cross-selling our ADI and Maxim portfolios. This puts us on a path to achieve our target $1 billion in revenue synergies. For example, at a European auto manufacturer, we built upon our strong audio connectivity position to cross-sell our high-speed GMSL technology (Maxim product), connecting their advanced driver systems. – Vincent Roche, CEO

From its latest earnings briefing in Q2 2023, the company’s management cited the “secular tailwinds fueling content growth continue to drive ADI's leading battery management and in-cabin connectivity solutions” and grew by 40% YoY, thus indicating its high growth momentum being intact.

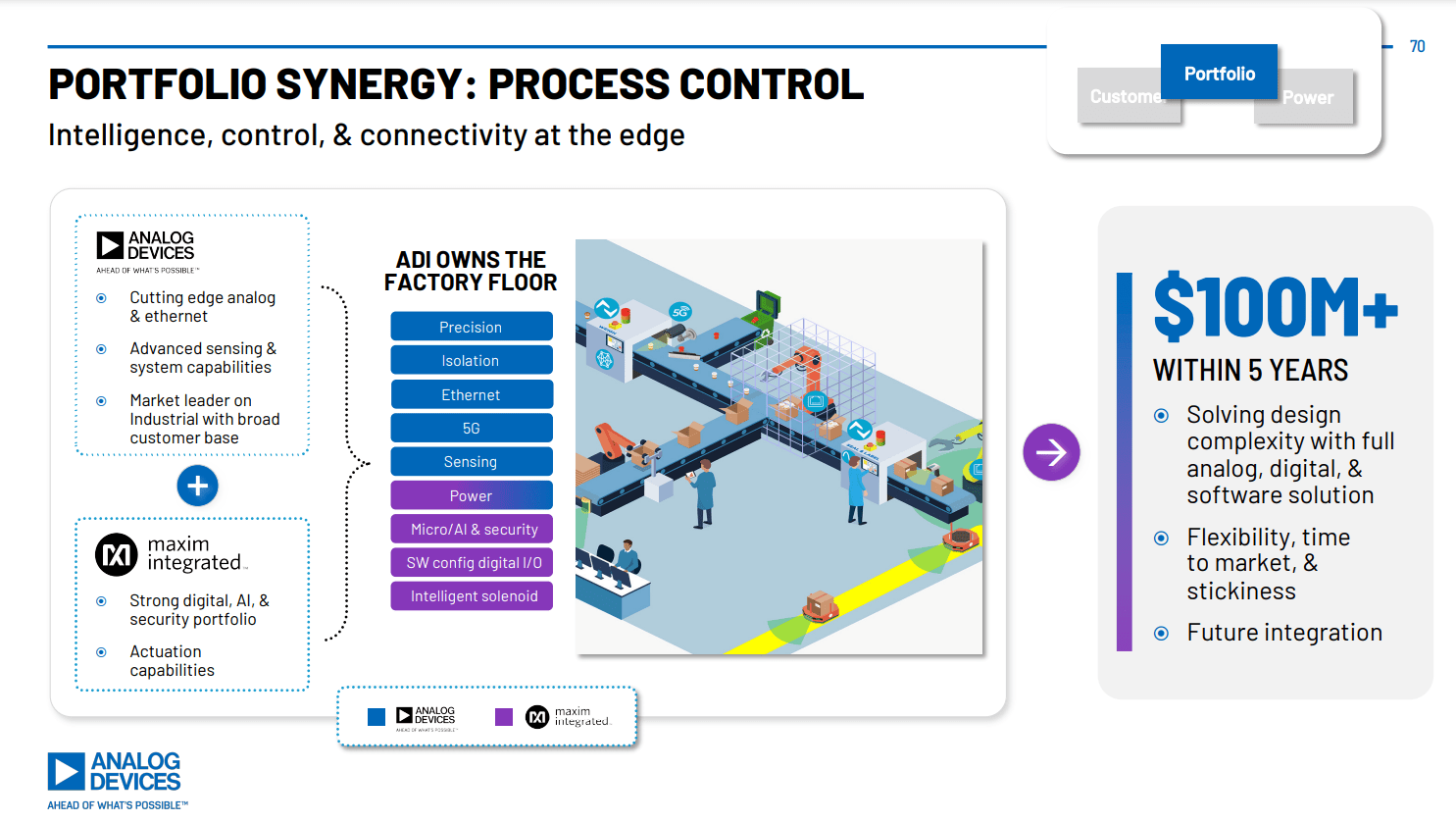

The automotive segment is not the only segment boosted by the Maxim acquisition. In its Q2 2022 earnings briefing, management stated that the communications segment benefited from “the technologies that Maxim are bringing to that wireline area”. ADI also benefited from Maxim’s power and “advanced sensing and system capabilities” in the industrial segment, which can be seen in the diagram below.

ADI

In terms of profitability, the company’s gross margin and operating margin in 2022 were 64.96% and 31.80% respectively. This is higher than our forecasts of 63.32% gross margin and 27.69% operating margin. In its Q2 2022 earnings briefing, management stated that…

The gross margin percentage and the growth in gross margin percentage that you see is really being driven, as I mentioned, by the synergies - Prashanth Mahendra-Rajah, ADI CFO

Moreover, we identified “the company expected to achieve costs synergies of $275 mln within 24 months after the acquisition”. However, in its Q2 2022 earnings briefing, management stated…

We captured basically the entire $275 million that we originally committed to as we exited our second quarter. And that at Investor Day, we said we're raising that target to $400 million, and we'll hit that number coming out of -- or as we exit 2023. That first $275 million was a little more tilted towards cost of goods, and the following piece will sort of be balanced between cost of goods and OpEx. - Prashanth Mahendra-Rajah, ADI CFO

Therefore, the company managed to hit its cost synergy target more than a year earlier and increased its target by adding $125 mln, which explains the gross margins and operating margins being above our forecasts.

In conclusion, the majority (41.7%) of the 64.2% total company growth in 2022 was attributed to Maxim Semiconductor, with the remaining 22.5% of the growth attributed to organic ADI growth, much higher than our forecasted organic growth of 6.64% in our previous coverage. We find that Maxim boosted the automotive segment growth with its power management systems improving ADI’s BMS portfolio, which was the biggest growth driver for the automotive segment (101.5% segment growth). Additionally, cost synergies helped increase ADI’s gross margin (64.96%) and operating margin (31.80%), which was higher compared to our forecasts of 63.32% and 27.69% respectively.

Maxim to Continue Boosting Revenue Growth

New Product Releases | Total Company Products | Maxim Products | Maxim as a % of Total Products |

December 2022 to May 2023 | 111 | 47 | 42.3% |

June 2022 to December 2022 | 90 | 23 | 25.6% |

Source: ADI, Khaveen Investments

Product Applications | Industrial | Automotive | Communications | Consumer |

Maxim Products (December 2022 to May 2023) | 17 | 24 | 5 | 15 |

Maxim Products (June 2022 to November 2022) | 12 | 7 | 3 | 5 |

Source: ADI, Khaveen Investments

In the first table above, we analyzed the new product releases from the whole company and also the new products that were from Maxim. In the past 6 months, the company released a total of 111 products, of which 47 of those were Maxim products. In the 6 months before that, the company released a total of 90 products, and 23 of those were Maxim products. Therefore, the number of new products from Maxim has more than doubled and Maxim products as a percentage of total company products went from 25.6% in the first 6 months to 42.3% in the next 6 months. Moreover, from the second table, the new Maxim products in the past 6 months have more applications in all four segments (Industrial, Automotive, Communications, and Consumer) than the new Maxim products released 6 months before.

We previously forecasted revenues by taking market growth forecasts for each segment, from which we derived a post-acquisition total company growth forecast of 6.7%. However, as we identified in the point above, ADI had organic growth of 22.5% in 2022, slightly higher than analog market growth of 20.8%. Therefore, excluding the effect of the 41.7% company growth from Maxim, the company has already been able to grow higher than the market. Thus, with the baseline growth of the company being much higher than our previous coverage, we believe it is not appropriate to use market CAGR to forecast revenue.

Organic Revenue Growth ($'000s) | 2018 | 2019 | 2020 | 2021 | 2022 | 5-Year Average |

Maxim Organic Revenue | 2,314,330 | 2,191,390 | 2,354,000 | 2,769,600 | 3,052,184 | |

Growth Rate % (YoY) | -6.7% | -5.3% | 7.4% | 17.7% | 10.2% | 4.66% |

ADI Organic Revenue | 6,224,689 | 5,991,065 | 5,603,056 | 6,759,786 | 8,961,769 | |

Growth Rate % (YoY) | 18.6% | -3.8% | -6.5% | 20.6% | 32.6% | 12.33% |

Source: ADI, Maxim, Khaveen Investments

For our new forecasts, we took the weighted average of the 5-year average organic growth of Maxim and ADI. We estimated Maxim’s 2021 organic revenue by prorating the sum of its Q321 (quarter ending March 2021) and Q421 (quarter ending June 2021) revenues for the remaining 6 months of the year. Then, we estimated Maxim’s 2022 organic revenue by taking 65% of ADI growth in 2022 which was attributed to Maxim and added it to our forecasted Maxim 2021 organic revenue.

We derived ADI organic revenue in 2021 by subtracting total ADI revenue by the $558.5 mln of Maxim revenue from the acquisition date (August 2021) till the end of ADI’s fiscal year (October 2021). We then estimated ADI’s 2022 organic revenue by taking 35% of total company growth in 2022 which was attributed to ADI’s organic growth and added it to ADI’s 2021 organic revenue.

We identified above Maxim products taking up a larger portion (42.3%) of total company product releases in the past six months, compared to 25.6% of total company product releases in the six months before that. Therefore, we believe Maxim will still be able to drive increased revenue growth going forward. We derived a weighted average organic growth rate for the combined company as follows:

Weighted Average Calculation | Figures |

Maxim Weight (%) ('a') | 25.4% |

Maxim Organic 5-year Average Growth (%) ('b') | 4.7% |

ADI Weight (%) ('c') | 74.6% |

ADI Organic 5-year Average Growth (%) ('d') | 12.3% |

Weighted Average Growth Rate | 10.4% |

*Weighted-Average Formula: (a x b) + (c x d)

Source: ADI, Khaveen Investments

Using the formula, we derived a growth forecast for the company in 2023 at 10.4%. We also note that the company’s actual H1 revenues and Q3 guidance of $3.1 bln from its latest earnings briefing represent a growth of 9.9%, in line with our forecasts. Tapering the growth forecast by one percent over the next four years as a conservative estimate, our forecasted total company revenue over the next five years is shown in the table below:

Revenue Forecast ($'000s) | 2023F | 2024F | 2025F | 2026F | 2027F |

Total Revenue | 13,260,849 | 14,157,603 | 15,113,735 | 16,133,067 | 17,219,653 |

Growth Rate % (YoY) | 10.4% | 9.4% | 8.4% | 7.4% | 6.4% |

Source: ADI, Maxim, Khaveen Investments

Risk: Increasing Days Inventory Outstanding

Efficiency Analysis | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | TTM | Average |

Inventory Turnover | 5.87x | 2.74x | 2.44x | 2.50x | 2.45x | 2.07x | 1.95x | 1.81x | 1.53x | 1.47x | 1.37x | 2.48x |

Days Inventory Outstanding (dAys) | 62 | 133 | 149 | 146 | 149 | 177 | 187 | 202 | 238 | 248 | 266 | 169 |

Source: ADI, Khaveen Investments

We believe one of the risks for the company is its increasing days inventory outstanding which has increased from 62 days in 2013 to 248 days in 2022 and 266 days TTM. This is as the company’s inventory turnover ratio decreased from 5.87x to 1.37x over the period. This scenario may indicate deteriorating inventory management or a build-up of excess inventory due to lower demand. In its Q4 2022 briefing previously, management highlighted that it was planning to hold more inventory “during these uncertain times” and the company was rebuilding its “die bank” which was reduced “over the last couple of years”. In its latest briefing, the company reiterated its “to hold more finished goods inventory versus restocking the channel” which contributed to higher inventory days.

Verdict

Khaveen Investments

Seeking Alpha, Khaveen Investments

In summary, we believe ADI has emerged as a joint leader in the analog market alongside TI, boasting a substantial market share of 17.2%. This represents a remarkable gain from ADI's 2021 market share of 12.6%, while TI's market share declined from 19% in 2021. ADI's exceptional growth in 2022 (64.2%) greatly contributed to its increased market share, outpacing the analog market's growth rate of 20.8%. Maxim played a significant role in ADI's growth, accounting for 41.7% of its 2022 growth. Maxim's impact was particularly notable in ADI's automotive segment, driving a substantial 101.5% growth in its automotive BMS portfolio.

In addition to Maxim's contribution, we calculated ADI experienced stronger organic growth of 32.6% in 2022, surpassing our previous forecast of 6.64%. To determine revenue forecasts, we opted for a weighted average of the five-year organic growth rates of both Maxim and ADI. This approach accounts for ADI's higher growth compared to the overall market and considers Maxim's potential to further enhance revenue growth through a higher proportion of product releases in the past six months compared to the preceding period. Based on these factors, we derived a weighted average growth rate of 10.4% for 2023, gradually tapering it down by one percent over the following four years.

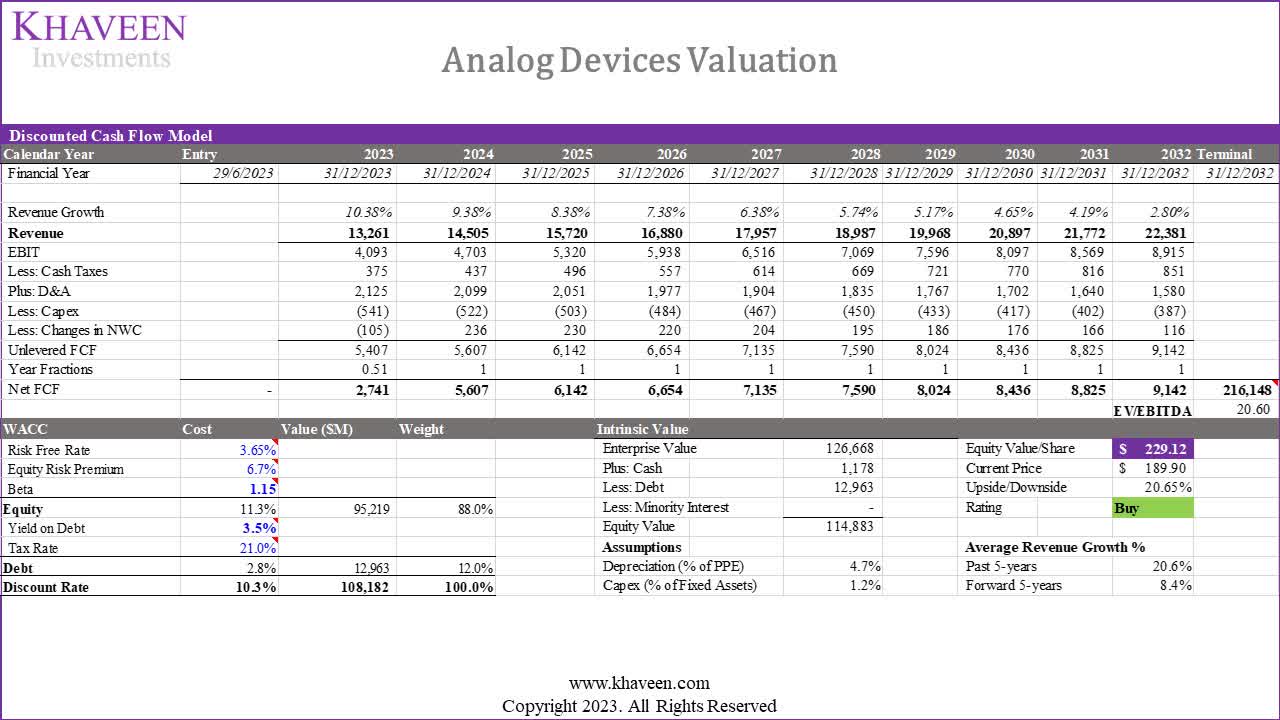

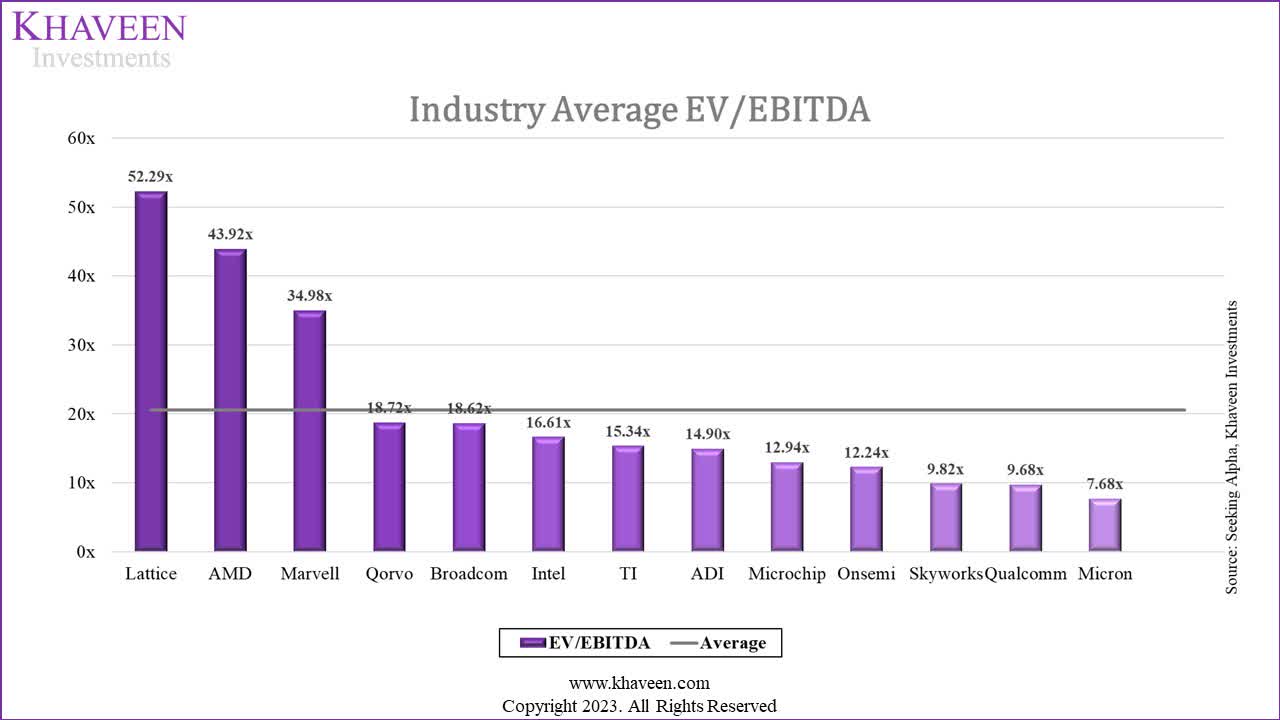

For valuing the company, we utilized a DCF valuation methodology. The terminal value was based on US chipmakers' average EV/EBITDA ratio, which averaged 20.6x. We excluded Nvidia from this calculation due to its outlier EV/EBITDA ratio of 166.44x. Notably, the EV/EBITDA value we derived is lower than the one obtained in our previous coverage, which stood at 23.87x.

Consequently, we arrived at a price target of $229.12 for ADI, reflecting an upside of 20.65%. This new target price represents a significant increase of 39% compared to our previous target price of $164.47. Despite the current stock price ($189.90) surpassing our previous target, we believe there is still considerable upside potential. This outlook is driven by our revised forecast of an 8.4% forward 5-year growth rate (excluding 2022 due to the acquisition), compared to the previous forecast of 6.6%. Additionally, the company's current 5-year average net margin stands at 22.13%, higher than the 20.62% average net margin from our previous coverage and we forecasted higher margins for the company moving forward. Taking all these factors into account, we assign a Buy rating to Analog Devices.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ADI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No information in this publication is intended as investment, tax, accounting, or legal advice, or as an offer/solicitation to sell or buy. Material provided in this publication is for educational purposes only and was prepared from sources and data believed to be reliable, but we do not guarantee its accuracy or completeness.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.