Wipro Faces Soft Client Discretionary Spending Amid Macro Uncertainties

Summary

- Wipro Limited provides a range of IT consulting and advisory services to organizations worldwide.

- While management touted its strong growth in bookings, it has provided little forward guidance and Q1's guidance is negative for revenue.

- With clients reducing discretionary spending amid a macroeconomic slowdown, I remain Neutral [Hold] for WIT in the near term.

- Looking for more investing ideas like this one? Get them exclusively at IPO Edge. Learn More »

VioletaStoimenova/E+ via Getty Images

A Quick Take On Wipro Limited

Wipro Limited (NYSE:WIT) reported its FQ4 2023 financial results on April 27, 2023, missing revenue estimates and matching EPS estimates.

The firm provides a wide array of digital transformation consulting, outsourced business services, and IT products in India and worldwide.

I previously wrote about Wipro with a Hold rating.

Given an overall macro environment of high uncertainty combined with reduced spending by clients leading to forward growth concerns, my outlook for Wipro Limited remains very cautious, so I'm Neutral [Hold] on the stock for the near term.

Wipro Overview

Bengaluru, India-based Wipro Limited was founded to provide various IT consulting services, business outsourcing services and IT products globally.

The firm is headed by Chief Executive Officer Thierry Delaporte, who was previously Chief Operating Officer of Capgemini and currently lives in Paris, France.

The company's primary offerings include:

IT consulting

Business process outsourcing

Product engineering & design

Government services

Other services.

The company has more than 250,000 employees located on six continents.

Wipro's Market & Competition

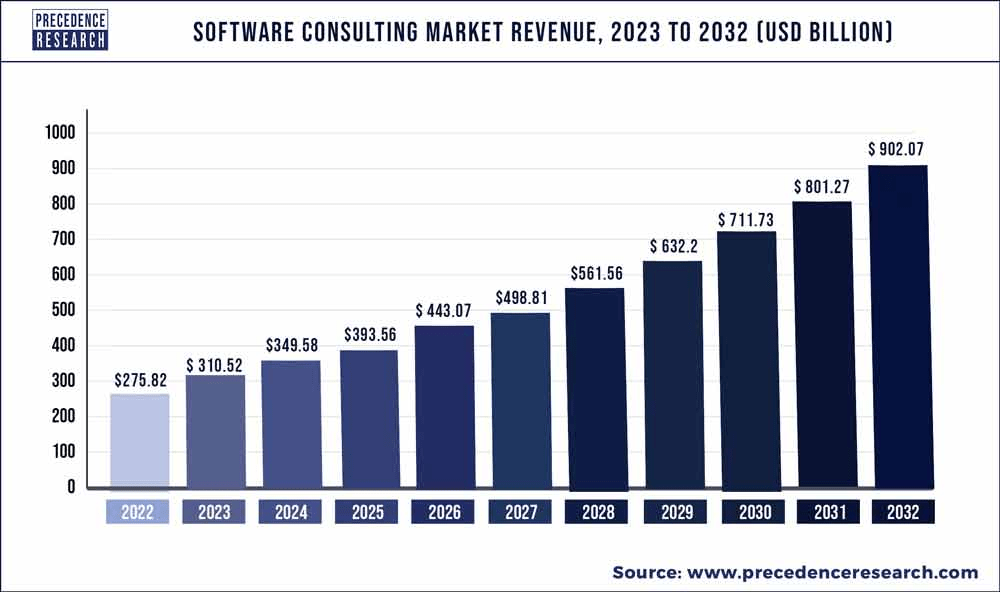

According to a 2023 market research report by Precedence Research, the global market for IT consulting was estimated at $276 billion in 2022 and is forecasted to reach $902 billion by 2032.

This represents a forecast CAGR (Compound Annual Growth Rate) of 12.58% from 2023 to 2032.

The main drivers for this expected growth are an increasing preference for the digitization of business processes across every industry in order to increase efficiency and support revenue growth.

Also, the chart below shows the software consulting market trajectory forecast through 2032:

Software Consulting Market (Precedence Research)

Major competitive or other industry participants include:

Accenture

Atos SE

Capgemini

CGI Group

Clearfind

Cognizant

Deloitte Touche Tohmatsu

Ernst & Young

Infosys

International Business Machines Corp.

Oracle Corp.

PricewaterhouseCoopers

Rapport IT

SAP SE

Others.

Wipro's Recent Financial Trends

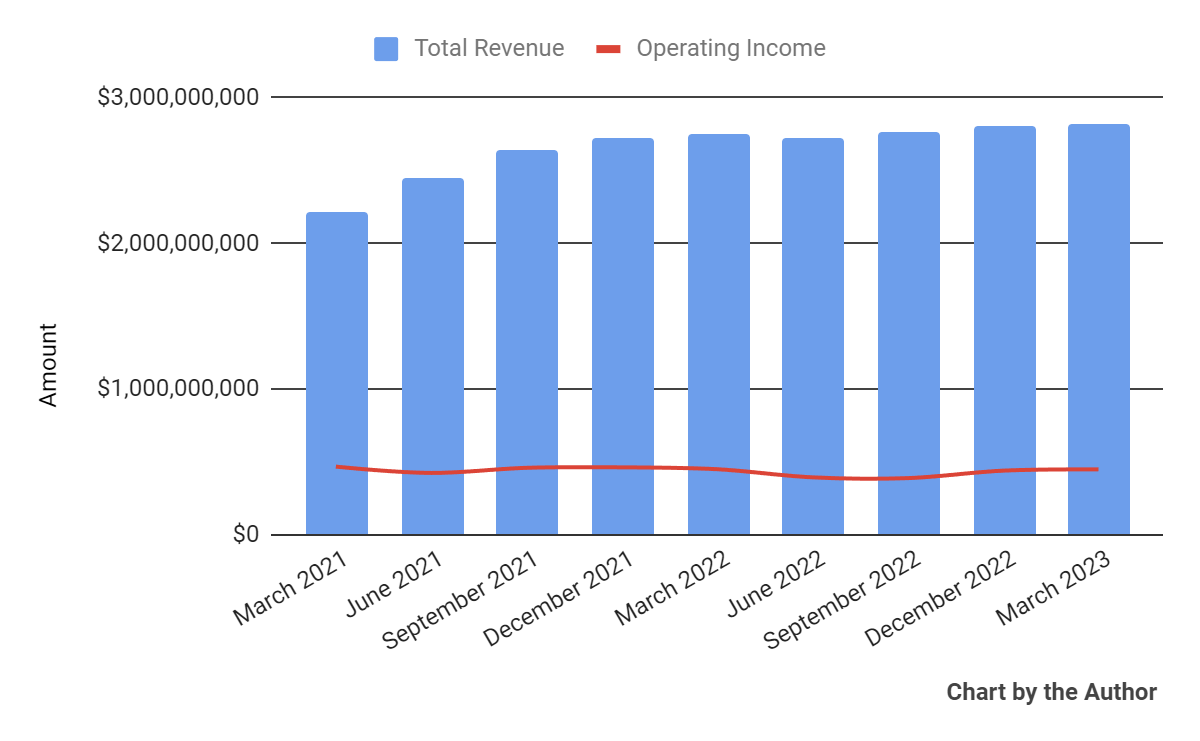

Total revenue by quarter has plateaued, as has operating income by quarter, as the chart shows below:

Total Revenue and Operating Income (Seeking Alpha)

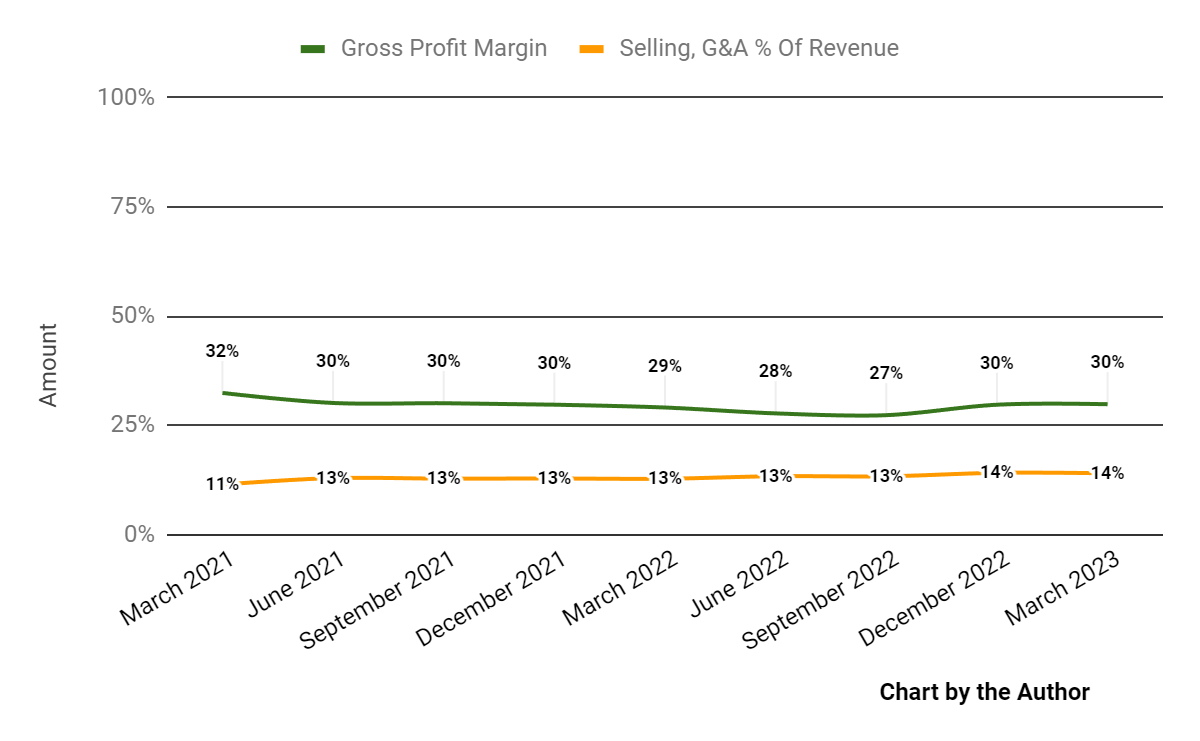

Gross profit margin by quarter has risen slightly recently; Selling, G&A expenses as a percentage of total revenue by quarter have also trended higher in recent quarters:

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

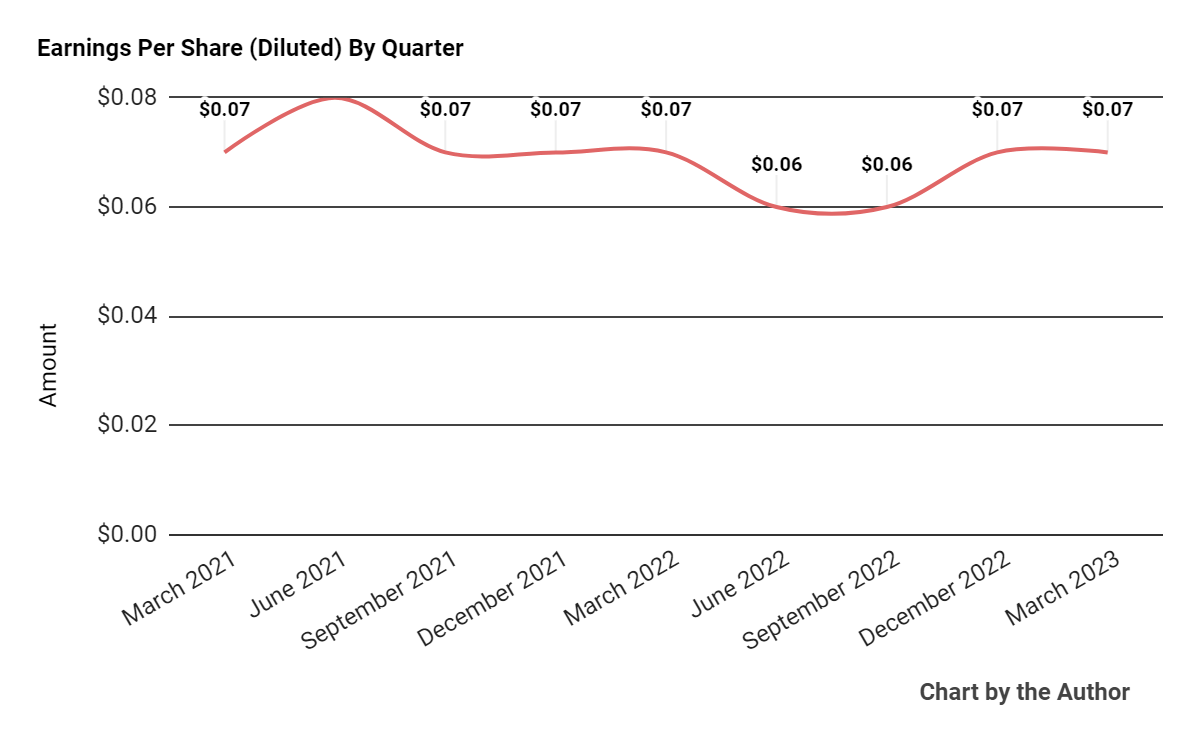

Earnings per share (Diluted) have fluctuated within a narrow range:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

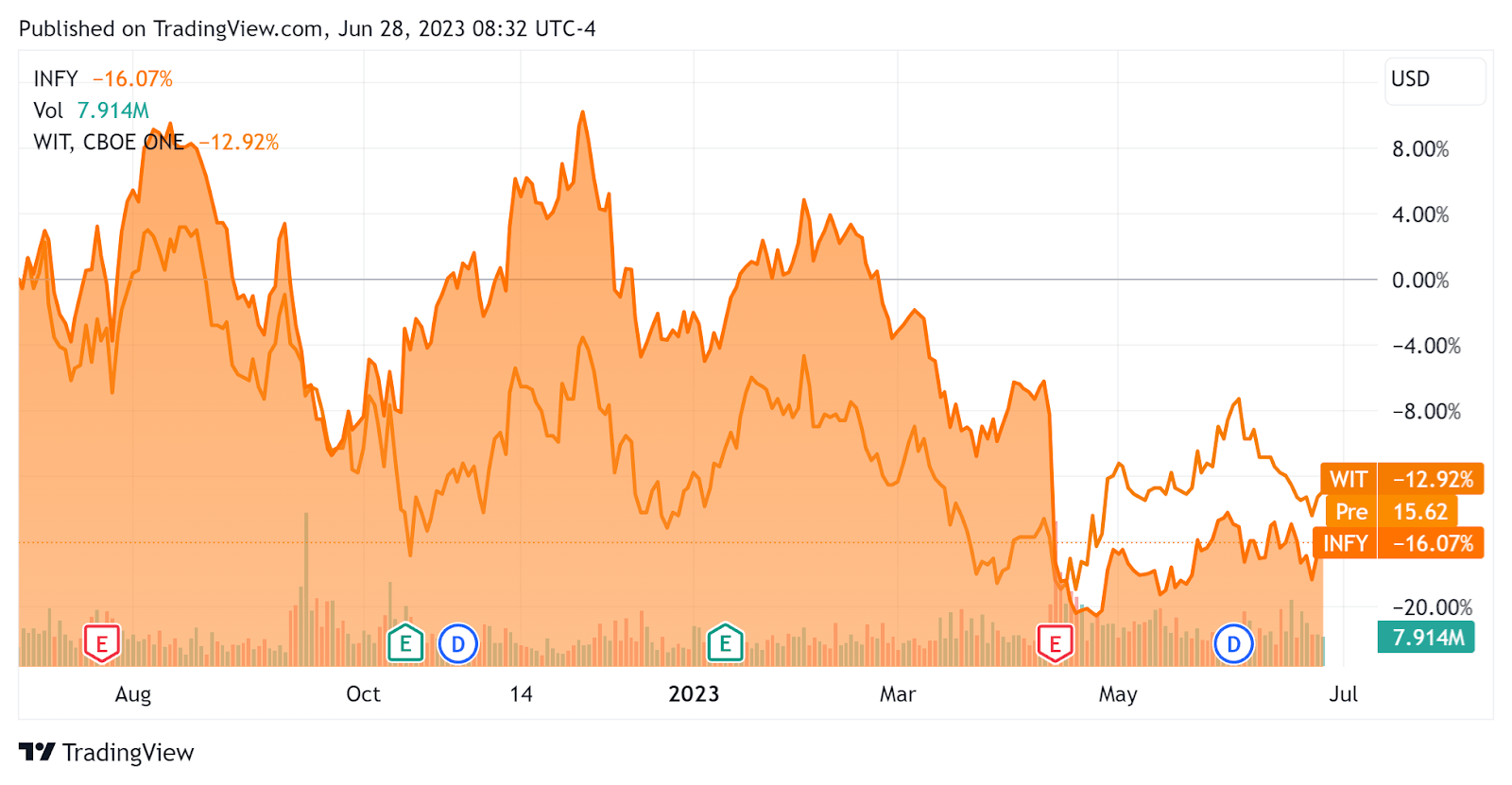

In the past 12 months, WIT's stock price has dropped 12.92% vs. that of Infosys Limited's (INFY) fall of 16.07%, as the chart indicates below.

52-Week Stock Price Comparison (Seeking Alpha)

For the balance sheet, the firm ended the quarter with $4.9 billion in cash, equivalents and short-term investments and $1.8 billion in total debt, of which a hefty $1.1 billion was categorized as the current portion due within 12 months.

This is a significant cost risk for the company in the years ahead, as rolling over a large portion of its debt in the current higher interest rate environment will likely have a negative impact on its earnings and cash flow.

Over the trailing twelve months, free cash flow was $1.4 billion, during which capital expenditures were $180.6 million. The company paid $48.3 million in stock-based compensation ("SBC") in the last four quarters.

Valuation And Other Metrics For Wipro

Below is a table of relevant capitalization and valuation figures for the company.

Measure [TTM] | Amount |

Enterprise Value / Sales | 2.1 |

Enterprise Value / EBITDA | 11.5 |

Price / Sales | 2.3 |

Revenue Growth Rate | 14.4% |

Net Income Margin | 12.5% |

EBITDA % | 17.9% |

Net Debt To Annual EBITDA | 1.5 |

Market Capitalization | $25,450,000,000 |

Enterprise Value | $22,710,000,000 |

Operating Cash Flow | $1,590,000,000 |

Earnings Per Share (Fully Diluted) | $0.26 |

(Source - Seeking Alpha.)

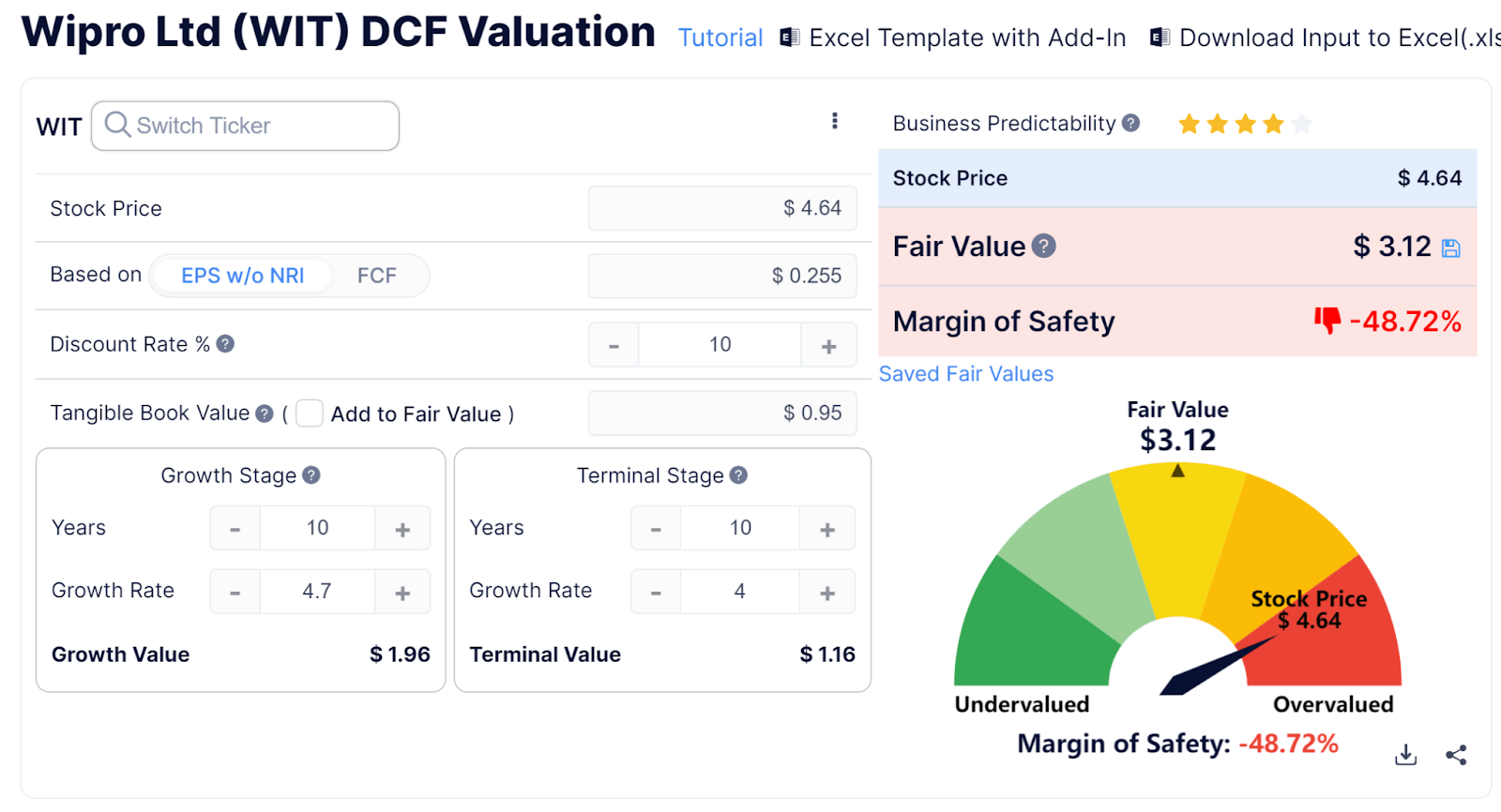

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm's projected growth and earnings.

Discounted Cash Flow - Wipro (GuruFocus)

Assuming generous DCF parameters, the firm's shares would be valued at approximately $3.12 versus the current price of $4.64, indicating they are potentially currently overvalued, with the given earnings, growth, and discount rate assumptions of the DCF.

As a reference, a relevant partial public comparable would be Infosys; shown below is a comparison of their primary valuation metrics.

Metric [TTM] | Infosys | Wipro | Variance |

Enterprise Value / Sales | 3.5 | 2.1 | -40.8% |

Enterprise Value / EBITDA | 15.1 | 11.5 | -23.6% |

Revenue Growth Rate | 11.7% | 14.4% | 23.7% |

Net Income Margin | 16.4% | 12.5% | -23.4% |

Operating Cash Flow | $2,850,000,000 | $1,590,000,000 | -44.2% |

(Source - Seeking Alpha.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

WIT's most recent Rule of 40 calculation was 32.3% as of FQ4 2023's results, so the firm's results have dropped slightly sequentially, per the table below.

Rule of 40 Performance | FQ3 2023 | FQ4 2023 |

Revenue Growth % | 18.4% | 14.4% |

EBITDA % | 17.6% | 17.9% |

Total | 36.0% | 32.3% |

(Source - Seeking Alpha.)

Commentary On Wipro

In its last earnings call (Source - Seeking Alpha), covering FQ4 2023's results, management highlighted the firm's partnership strategy, which seeks to drive large, complex deals through strategic partnerships and alliances.

While the firm appears to be winning larger deals due in part to market consolidation, it is seeing softness in demand from its banking, insurance and technology client base.

On a positive note, bookings rose 28% year-over-year in total contract value terms, hinting at stronger growth in the future as these deals are implemented.

However, implementation can take longer than anticipated as clients decide the pace and speed of their digital transformation or cost-efficiency initiatives.

The firm's employee attrition rate was 14.1%, indicating declining attrition rates throughout the fiscal year.

Total revenue for FQ4 rose only 2.8% YoY, while gross profit margin increased by 0.8%.

Selling, G&A expenses as a percentage of revenue grew by 1.3%, indicating less efficiency, and operating income dropped by 0.3% YoY.

Looking ahead, management guided only for FQ1 revenue at a sequential drop of 2% at the midpoint on a constant currency basis.

The company's financial position is reasonably strong, with ample liquidity. However, a large part of its long-term debt is rolling over and the firm faces higher interest rates and debt service costs ahead.

WIT's Rule of 40 performance has been reasonably good but declining.

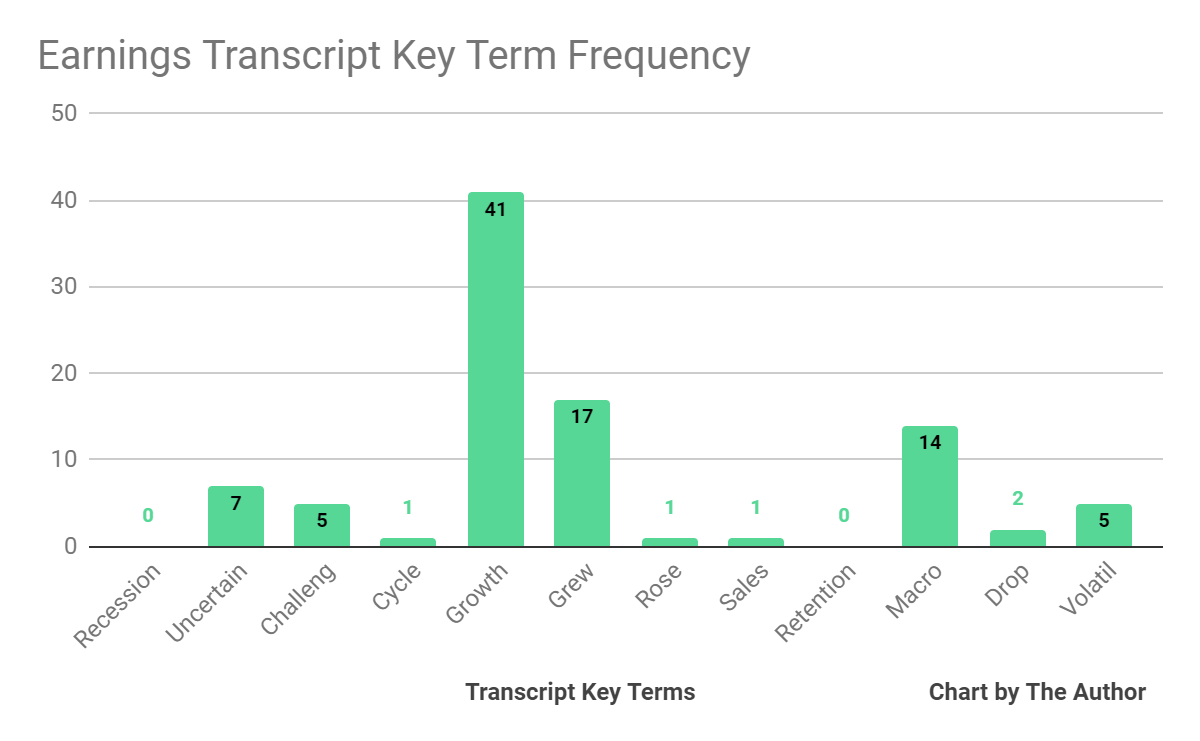

From management's most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below.

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I'm most interested in the frequency of potentially negative terms, so management or analyst questions cited "Uncertain" seven times, "Challeng[es][ing]" five times, "Macro" fourteen times, "Drop" twice and "Volatil[e][ity]" five times.

The negative terms refer to the difficulties the company is facing with respect to slowing client activity and is something that I'm seeing at other major consulting firms with exposure to numerous industries and geographies.

Analysts questioned company leadership about forward guidance, which was only for Q1 of the new fiscal year. Management responded by noting strong bookings even as some clients chose to cut discretionary spending.

Given an overall macro environment of high uncertainty combined with reduced spending by clients leading to forward growth concerns, my outlook for WIT is very cautious, so I remain Neutral [Hold] on the stock for the near term.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis.

Get started with a free trial!

This article was written by

I'm the founder of IPO Edge on Seeking Alpha, a research service for investors interested in IPOs on US markets. Subscribers receive access to my proprietary research, valuation, data, commentary, opinions, and chat on U.S. IPOs. Join now to get an insider's 'edge' on new issues coming to market, both before and after the IPO. Start with a 14-day Free Trial.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.