After The Yield Curve Inversion

Summary

- The extreme yield curve inversion over the past year indicates that time is running out for the current macro backdrop.

- Gold is generally correlated to a steepening yield curve, while stocks are correlated to a flattening curve; the end of the yield curve inversion and the arrival of the next steepener will signal a change in market dynamics.

- Overly bullish sentiment is a condition for a broad market top, and the current environment suggests a coming top in speculation, with gold potentially benefiting as a result.

Melpomenem

As the 10yr-2yr yield curve inversion plays out, the time is coming for a turn in fortunes

Before proceeding, I'd like to remind you that this article is not written by a perma-bear. It is important to have credibility and indeed, NFTRH planned for a potential humdinger of a bear market rally back in Q4, 2022 based on the inputs of then extremely over-bearish sentiment, the bullish mid-term election cycle (which on average projects bullish for a year, post-election), a coming fade in inflation signals (with the attendant hopes for a softening Fed) being its primary elements. Here is one post discussing the rally in November, 2022.

There are plenty of other high risk indicators currently in play on the macro; but focusing on one important indicator, let's note that the extreme yield curve inversion that has taken place over the last year indicates that time is running out for the current macro backdrop, which sees a hawkish (and once again tardy, as it was with its silly "transitory inflation" blathering a couple years ago) Fed tilting at the inflationary windmill it was primary in creating. Goldilocks, favoring Tech, Semiconductor and Growth stocks, has held sway as we also projected.

Goldilocks lives during a yield curve flattener. She dies with a curve steepener.

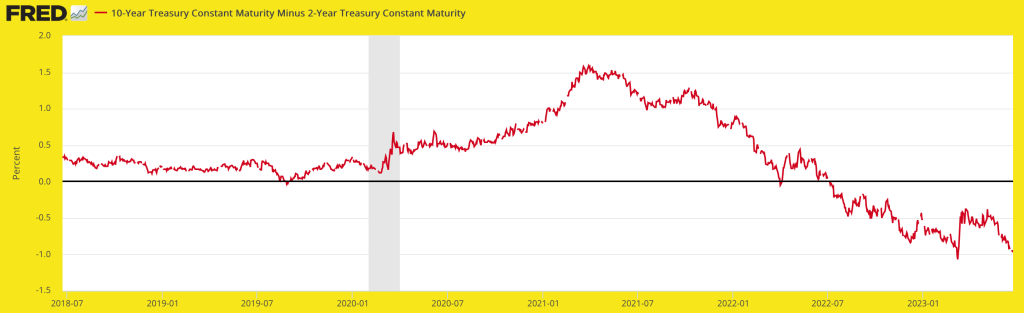

The 10yr-2yr curve is burrowing southward, perhaps for a test of the inversion low earlier this year. While people tend to worry about a yield curve inversion being a trigger to economic recession, it is actually the steepening that follows that usually brings the trouble, whether it be inflationary or deflationary. *

St. Louis Fed

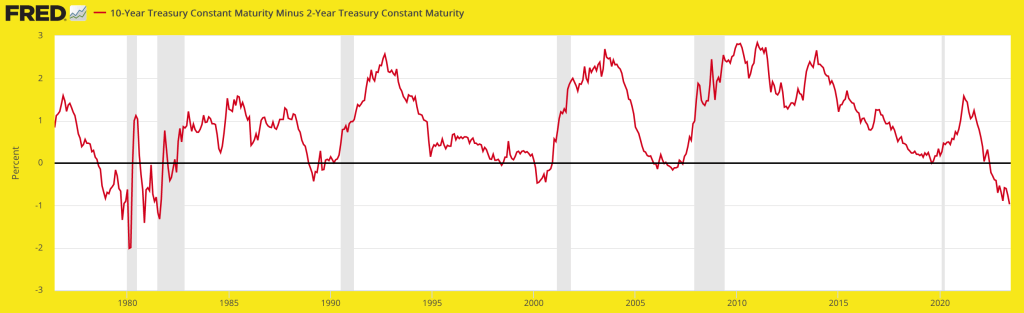

Today's situation is testing the inverted levels of uproarious events of the late 1970s to early 1980s. That situation, after a couple of recessions (shaded areas), resolved pleasantly disinflationary (as opposed to outright deflationary) as the resulting steepener - after several stops and starts - never did become impulsive. Nor did the next yield curve inversion in 1989.

St. Louis Fed

While there is much play in the wheel, so to speak, with respect to timing between the correlations of gold and the stock market (SPX as the broad US measure) to the yield curve, gold is generally correlated to a steepening yield curve and stocks are correlated to a flattening curve.

Gold is sought after when monetary regulators are indicated to be either losing control (under pains of inflation) ** or going overtly dovish (under deflation) while stocks would tend to either rotate toward commodity/resource producers and certain cyclical/value areas under inflation or go flat out bearish under deflation (as opposed to disinflationary Goldilocks) or a more virulent stagflationary inflation.

Recall that gold led the 2020 inflation phase by a country mile and then led the correction in the traditional inflation trades (commodities, resources and their producers) by another country mile as it saw the Fed donning its hawk costume as far back as August 2020. The Fed sure was tardy, but gold had been forecasting the hawk for quite some time before the eggheads actually got off their "transitory inflation" stance.

Goldilocks, and the Tech-led stock market rally have enjoyed the inversion, as would be expected. When the new steepener follows, in concert with an oncoming recession, there will not be much enjoyment. What there will be is the end of this massively risk 'ON' phase, the job of which always was to turn Q4, 2022's unsustainable over-bearish sentiment profile on its ear, to its opposite condition.

While over bullish dumb money indicators have not always signaled a market top, they are always a condition for a top. That condition is in place now, whether or not the market has already begun its topping process (not yet technically indicated).

Smart/dumb money (Sentimentrader.com)

Gold on the other hand, has been wearing its 'anti' suit (or more to the point, its "insurance" utility) generally since mid-2020 when the correction began. True to form, it did lead the broad rally in Q4, 2022 until Goldilocks took over, dumb money got back in the game (perhaps climaxing with the recent AI hype fest) and speculative forces went into overdrive.

It's all a sign of a coming top in speculation, and then there will be gold, as it always is. The end of the yield curve inversion and coming of the next steepener will be an important signal even as we patiently manage the gold, silver, and miners correction on a weekly basis with clear downside objectives laid out back in April.

* A steepener is inflationary if nominal yields are rising and deflationary if they are falling. At this time we continue to expect the latter to be the case, but there are elements in play that could see a global inflationary situation regenerate sooner rather than later. So, open minds, at least…

** Today's Fed is not indicated to have lost control. Quite the contrary; the Wizard is in full control as the market obsesses on every word out of its collective, and tardy orifice.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

No companies were mentioned.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.