PENN Entertainment: A Deep Value Jackpot

Summary

- PENN Entertainment is undervalued by 66% due to a market selloff, presenting a deep-value investment opportunity.

- The company has a mid-sized economic moat driven by its diverse product portfolio and psychologically "sticky" rewards program that enables increased extraction of revenue per customer.

- Risks include exposure to a cyclical market environment and ESG-related threats due to the controversial gaming industry.

- PENN is well positioned to remain the market leader and achieve tangible margin expansion which warrants my "Strong Buy" rating.

Michael Blann/DigitalVision via Getty Images

Investment Thesis

PENN Entertainment (NASDAQ:PENN) is one of the largest players in the commercial gaming industry in the U.S. Their extensive range of traditional and online gambling, betting and leisure products create a differentiated portfolio which allows for a tangible economic moat to exist for the firm.

The huge market selloff post-COVID has led to share prices dropping almost 90% since early 2021. In the meantime, PENN has only strengthened their operational abilities and cashflow generation potential.

Therefore, I believe a real deep-value play could be present thanks to the potential 66% undervaluation currently present in shares.

Company Background

PENN Entertainment (renamed from Penn National Gaming in 2022) is a North American provider of integrated entertainment, sports content and casino gaming experiences. The company is one of a few market leaders in the industry and operates an impressive portfolio of online sports betting and iCasino businesses.

The gaming firm operates multiple well recognized brands including Hollywood Casino, L’ Auberge and Barstool Sportsbook. Their business strategy revolves around maintaining a highly differentiated portfolio with a significant focus on maximizing cross-selling opportunities.

Recent acquisitions of Barstool Sports in 2020 and Score Media and Gaming (theScore) in 2021 have further increased the breadth and presence PENN achieves in the online betting marketplace.

PENN has recently launched a highly attractive loyalty program that reaches over 26 million members. The provision of exclusive rewards and offers to loyal customers has been designed to increase member satisfaction levels and create switching costs for consumers looking to bet using other platforms.

Economic Moat - In Depth Analysis

PENN harbors a robust and mid-sized economic moat driven primarily by the significant breadth of their product portfolio and the sticky nature of their rewards programs.

PENN FY23 Q1 Presentation

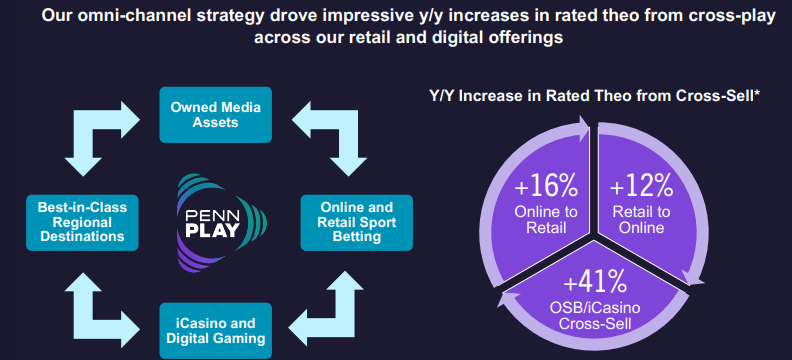

Through multiple acquisitions over time, PENN has grown to operate more than 43 casinos and racetracks, multiple market leading sports betting sites along with a host of online gaming and iCasino platforms.

The company also operates hotels and integrated gaming resorts along with two omnichannel media businesses which create content under the well-known “Barstool Sportsbook” moniker.

This wide approach allows PENN to target multiple different gaming categories and leverages their power to create organic cross-selling across these various businesses.

While gaming remains PENN's largest business segment by revenue stream, the significance of their hotels and foods & beverage segments cannot be overstated.

I believe these segments enable PENN to differentiate their products from the competition by offering customers with the option to engage in a more holistic leisure experience with their suite of product offerings.

PENN FY23 Q1 Presentation

While a customer may initially engage with PENN gaming brands, the ability for the same client to then book a resort holiday at a PENN casino resort allows for the potential to greatly increase the revenue earned per customer.

PENN's wide product portfolio also creates moatiness for the firm thanks to the high-profile and popular brands the company operates. Huge Casino brands such as L’Auberge, Hollywood Casinos, Margaritaville and Plainridge Park are just some of the 12 retail brands PENN operates.

Similar blockbuster-level names are present in their online gaming segment with hollywoodcasino.com and PENN Play Casino. On the sports betting side, PENN now operates both Barstool Sportsbook and theScore Bet.

These huge name brands create significant moatiness for the company thanks to the reputation and interest these banners bring to the overall portfolio. By attracting customers into the business with popular brands, PENN is able to efficiently and effectively cross-sell products from other brand families.

I view PENN's sports betting, iCasino and media businesses as significant future moatiness and revenue drivers. The growing popularity of these digital gaming mediums and PENN's unique set of high-quality and trusted brands in these markets should yield the company with significant gains in the future.

PENN FY23 Q1 Presentation

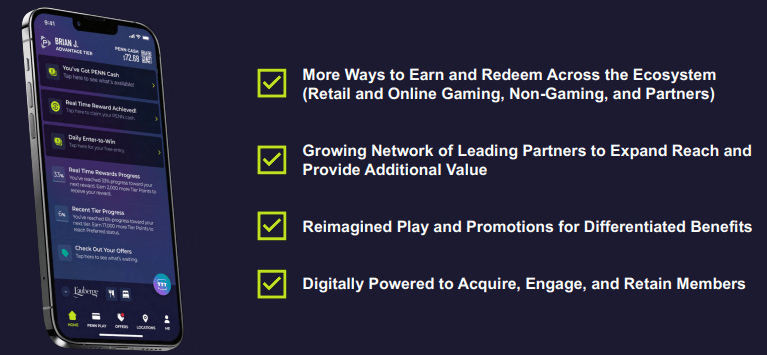

Another key driver I believe contributes meaningfully to PENN's economic moat is their extensive rewards program “PENNPLAY” (formerly “mychoice”). This program currently offers around 26 million members with a unique set of rewards and experiences across multiple different business channels.

PENN FY23 Q1 Presentation

The program allows members to receive personalized promotions and rewards ranging from discounts at different hotels and resorts to more PENN Cash and credits to use on the PENN Play Casino app.

PENN also offers customers the opportunity to obtain a PENN Mastercard (MA) Credit Card which further earns annual tier points and PENN Cash when making traditional credit purchases.

This rewards program is one of the most extensive in the industry. In my opinion this rewards scheme particularly increases the ability for PENN to retain customers who enter their gaming ecosystem.

Rewards programs are psychologically proven to be incredibly “sticky” factors consumers consider when choosing where to spend their discretionary income. Therefore, it should come as no surprise that PENN is leaning heavily into their new rewards program which creates motivation and desire for consumers to play more.

Overall, I believe PENN harbors a mid-sized economic moat that is robust enough to provide the company with a tangible competitive advantage over its rivals. While differentiation in the gaming industry can be difficult, PENN's unique set of brands and broad product portfolio help to achieve a tangible level of differentiation.

The breadth of their portfolio allows PENN to benefit from a true omnichannel business which aims to harness customers across a wide variety of digital and traditional mediums. When combined with their lucrative rewards program, I believe PENN holds a powerful set of resources primed for future value generation.

Financial Situation

PENN FY22 Q4 & Full Year Presentation

PENN has had a slightly mixed financial history over the last five years. While 2020 was a truly difficult annum for the firm due to the restrictions the COVID-19 pandemic placed on many in-person businesses, the post-covid period has been significantly more positive for the firm.

Average ROIC and ROE for the two years post-pandemic have been 5.1% and 8.3% respectively. PENN's net and operating margins (mean average) for the same period were 4.98% and 17% respectively.

The last two years have seen PENN become a significantly more profitable and fiscally efficient company than what was last seen pre-COVID-19.

PENN FY22 10-K

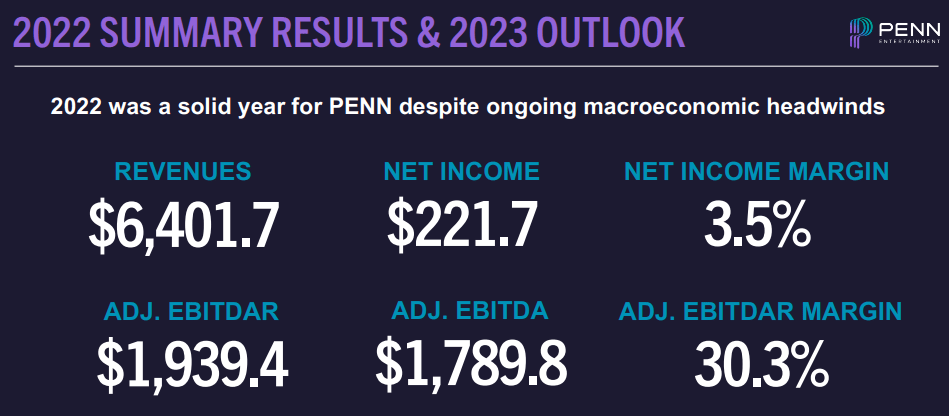

2022 was a solid year despite ongoing macroeconomic headwinds in the form of supply chain disruptions, significant levels of inflation and ongoing labor shortages.

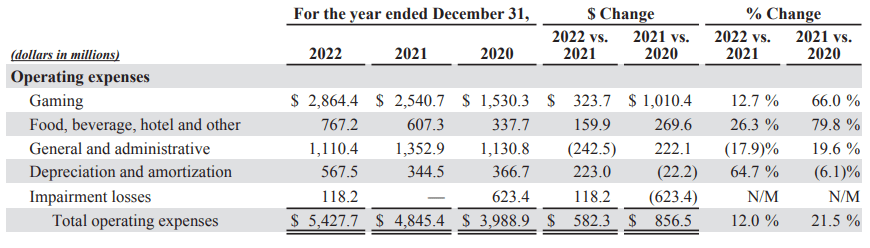

The firm managed revenues of $6.4B which represented an 8.3% YoY growth compared to FY21. This was driven by significant growth of 6% and 33% in their gaming and food, beverage and hotel segments respectively.

PENN's key geographic revenue driver remained their Northeast Segment which saw total revenues increase by $143.5M YoY totaling $2.7B. This was primarily due to the inclusion of operating results from Perryville which was acquired back in July of 2021.

The opening of both Hollywood Casino York and Hollywood Casino Morgantown in 2021 also contributed significantly to the Northeast segments results.

Unfortunately, increase COGS in the Northeast segment saw adjusted EBITDA decrease 190bps (0.7%) YoY. Many of these costs are linked to the highly inflationary market environment currently impacting companies across the globe and therefore should not plague the company indefinitely.

PENN's West and Midwest segments also saw strong revenue growth of 11.6% and 5.2% respectively. Adjusted EBITDA margins in the west increased a healthy 40bps despite the temporary closure of the Zia Park property due to lingering COVID-19 restrictions.

The West segment also recorded significant increases in spending per guest on gaming and increased visitation numbers at their food and beverage outlets. These strong results were earned despite the sale of the Tropicana Las Vegas property to Bally’s in September of 2022.

PENN FY22 10-K

Unfortunately, operating expenses as a percentage of revenue increased by 3% YoY. This was primarily due to increased COGS in their gaming and food, beverage and hotel segments.

PENN FY22 10-K

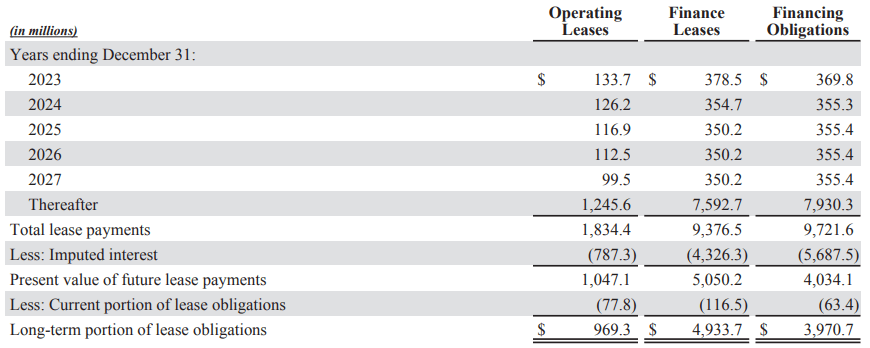

Overall, net income decreased 47% down to just $222.1M in FY22 due to a significant increase of $196M in net interest expenses. The primary factor that led to this huge surge in interest expense was the $171.3M increase in Master Lease interest costs due to changes in lease classifications.

This caused PENN's net income margin to decrease from 7.1% to 3.5%.

However, without this significant interest expense (which is usually tax-deductible for companies), PENN's EBITDA increased a healthy 16% to $1.789B in FY22. This left the company with an adjusted EBITDA margin of 28% compared to just 26.1% in FY21.

Ultimately, diluted EPS dropped from $2.48 in FY21 to $1.29 in FY22.

PENN FY23 Q1 Presentation

Q1 of FY23 has been hugely positive for the company with actual revenue of $1.67B beating analyst expectations by $82.94M. The quarter also saw net income margins increase to 30.7% with an adjusted EBITDAR margin of 28.6%.

Revenue growth YoY was 7% with net income increasing a whopping 897% from just $52M in Q1 FY22 to over $514M in Q1 FY23.

This strong quarterly performance was largely due to robust revenues earned by their Northeast geographic segment which offset slightly softer (on a YoY basis) results achieved in their South Segment.

This strong Northeastern performance was achieved despite gaming tax being the highest in this segment at an average of 41.8% compared to just 22.3% in their South segment.

Q1 also saw PENN's Interactive segment (mainly online betting and iCasino platforms) earn record revenues of $233.5M thanks to strong performance from Barstool Sports along with their iCasino services.

While the segment still produced an EBITDA of negative $5.7M, the segment is slowly but surely nearing profitability.

Most impressively, these relatively small losses are truly minute compared to what PENN's closest competitors such as MGM Resorts International's BetMGM (MGM) are able to achieve. In Q1 FY23, BetMGM earned MGM a loss of $81.9M.

This illustrates the powerful moatiness PENN has earned in their online gaming business which continues to provide increased profit generation ability for the firm. I believe their differentiated online product along with the extensive rewards program are primarily responsible for the strong results earned by the segment, especially in relation to their competitors.

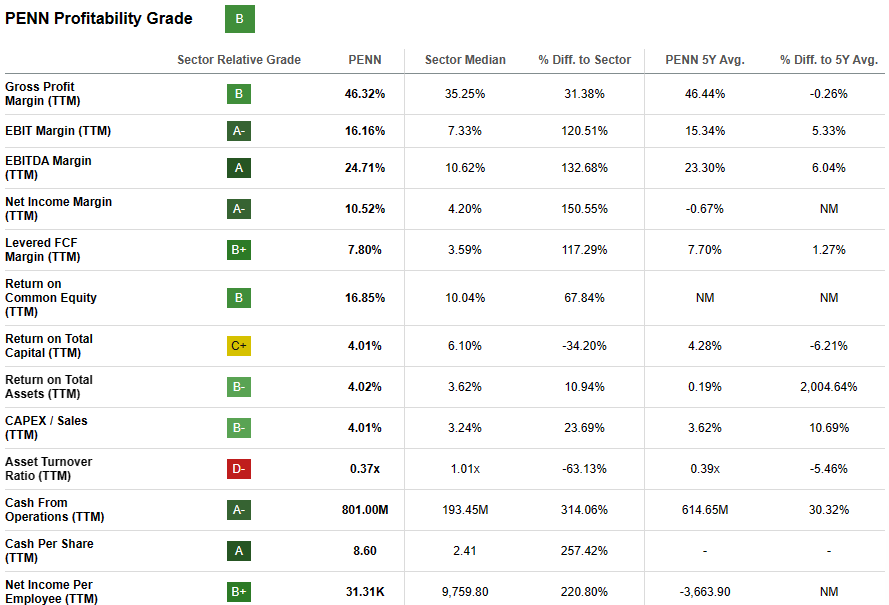

Seeking Alpha | PENN | Profitability

Seeking Alpha’s quant assigns PENN with a "B" profitability rating. I believe this rating is a representative snapshot of the company’s current profit generating abilities.

From a balance sheet perspective, the situation at PENN looks largely stable in my opinion. With $1.75B in total current assets and only $1.27B in total current liabilities, it is safe to say PENN faces no short-term liquidity issues which is welcomed news for investors.

This is supported by the company having a quick ratio (current assets minus inventory divided by current liabilities) of 1.24x. The quick ratio is an excellent indicator of a company’s short-term liquidity position and illustrates that PENN should face no issues meeting their short-term obligations.

The company’s overall debt/equity ratio is 2.80x due to PENN having a relatively large number of long-term maturities on their hands.

PENN FY22 10-K

Nonetheless, I believe PENN's overall long-term debt situation is largely under control. The majority of their debentures are maturing after 2027 with a good portion of notes being at fixed rates of 5.625% and 4.125% respectively.

I think this protects PENN relatively well from the increasingly difficult high-interest rate environment and should allow the company to maintain solid profitability despite the challenging macroeconomic environment.

Valuation

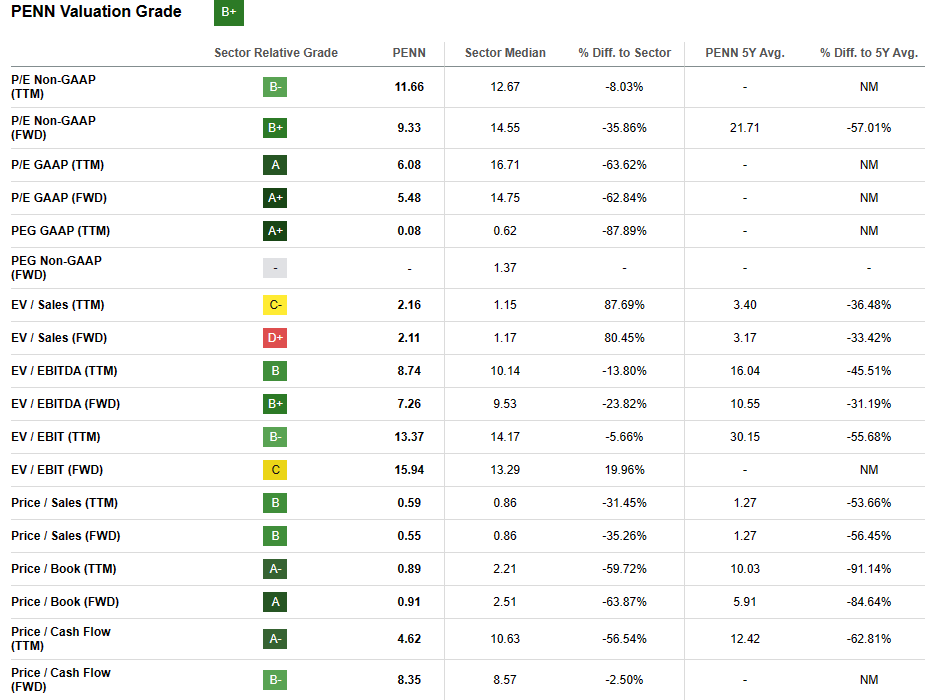

Seeking Alpha | PENN |Valuation

Seeking Alpha’s Quant assigns PENN with a "B+" Valuation rating. I believe this is a relatively good indicator of the value currently present in PENN shares.

The firm currently trades at a P/E GAAP FWD ratio of just 5.48x along with a P/CF TTM of 4.62x. Their FWD EV/EBITDA of 7.26 is quite reasonable especially when considering their Price/Sales FWD of 0.55.

While these metrics already suggest that PENN could be trading at somewhat of a discount relative to their worth, I believe it is important to delve a little deeper to develop an even better objective understanding of the situation.

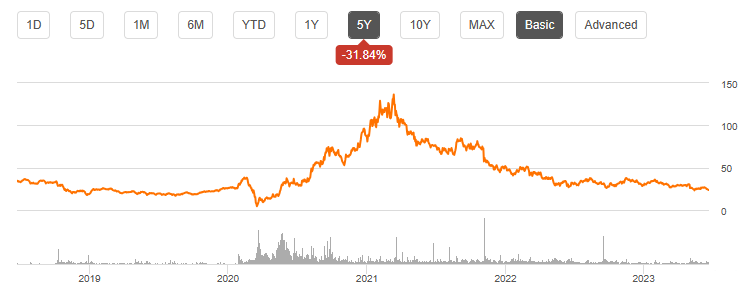

Seeking Alpha | PENN | Summary Chart

From an absolute perspective, PENN is trading at historically low prices. Shares have fallen around 83% since their highs of almost $140 in early 2021 to just $23.00 today. This has largely been due to PENN experiencing a massive post-pandemic rally as earnings recovered sharply.

However, I believe the ensuing market selloff has been excessive given the long-term profitability present at the gaming firm.

The Value Corner

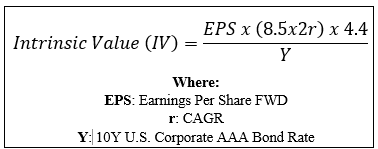

By utilizing The Value Corner’s Intrinsic Valuation Calculation, one can better understand what value exists in the company from a more objective perspective.

Using PENN’s estimated 2023 EPS of $4.43, a conservative “r” value of 0.04 (4%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 4.67%, I derive a base-case IV of $68.90. This represents a whopping 66% undervaluation in shares.

When using a more pessimistic bear case CAGR value for r of 0.02 (2%), PENN still appears to be undervalued by around 55% with an intrinsic value of $52.20.

Considering all of these valuation metrics holistically, I believe PENN is absolutely trading in deep-value territory. The meaningful expansion into further online sports betting businesses and iCasino operations should yield PENN a moat which they can use to drive future profitability.

In the short term (3-7 months), I am reluctant to make too many predictions on what the stock will do. While the current market valuation seems unfounded, forecasting the timescale on which a short-term market correction may occur is almost impossible.

Much depends on the trends prevailing macroeconomic conditions take moving into H2 of 2023 and the rate at which investor sentiment improves for PENN.

In the long-term (1-3 years), I believe PENN could make for a great investment given the undervaluation currently present in shares. The pricing mistake made by Mr. Market post-Covid has opened the door for a potentially lucrative value play in PENN shares.

Risks Facing PENN

PENN faces a multitude of risks stemming both from their ultimate exposure to a cyclical market environment as well as ESG related threats arising from the gaming environment in which they operate.

A prolonged economic downturn in the U.S. could lead to PENN struggling to remain profitable. The commercial gaming industry in the U.S. is particularly exposed to cyclical downturns with recessionary periods historically leading to very poor returns for the sector.

Despite PENN's meaningful differentiation and tangible competitive advantages, I do not believe the firm would be immune to such a macroeconomic event. Given the increasing probability for the U.S. economy to enter a recession in 2023, this threat could expose PENN to a particularly sharp short-term risk of poor profitability.

Furthermore, the increasing calls for stricter regulation of the commercial gaming industry due to the effects gaming addiction have on individuals could harm PENN's overall business model. PENN relies on maintaining their gambling licenses in different states to allow their operations to continue. While the governance threat of states removing these licenses is minute, the arguably "ethically gray" industry in which PENN operates raises some other ESG concerns.

Socially PENN must continue to make meaningful steps to prevent gambling addiction from harming their customers lives. While this responsibility must be balanced along with their cross-selling strategy and overall desire to extract the maximum revenue per customer, its importance cannot be overstated.

Furthermore, I believe a conscious and responsible approach from management will further help the company differentiate from the competition and position them in a better position moving forwards into the future.

From an environmental perspective little threats arise that could create tangible risk for the firm. While a more devoted approach to achieving net-zero carbon emissions would be nice to see, the overall negative impact of their operations on the environment is quite small.

Given the relatively serious social and governance risks associated with PENN's operations, I would not easily recommend PENN to an ESG conscious investor.

Summary

PENN has had a mixed set of results for the last couple of post-pandemic years. Shares got obliterated post-COVID due to the excessive valuations reach during the 2020 bull run. This led to the huge market selloff which ultimately brings us to the current situation at PENN.

While shares prices have been damaged the fundamental business PENN operates has only grown stronger in my view. A series of smart and future-oriented acquisitions have allowed PENN to differentiate their range of products form an otherwise homogenous market which helps earn the company some degree of economic moat.

I believe this moatiness will be key to PENN achieving greater profitability moving forwards.

Given the significant 66% undervaluation that exists in PENN shares using a base-case CAGR, I believe a real value opportunity exists in the gaming giant.

Therefore, I rate PENN a “Strong Buy” given the simply rock-bottom prices reached by shares. Intrinsically the firm seems to be worth significantly more than the market currently believes which I think presents value-oriented individuals with a classic lagging market sentiment opportunity.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I do not provide or publish investment advice on Seeking Alpha. My articles are opinion pieces only and are not soliciting any content or security. Opinions expressed in my articles are purely my own. Please conduct your own research and analysis before purchasing a security or making investment decisions.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (5)

16 months ago Penn was trading around 53 SP, then Portnioy escapade emerged and the stock took a dive. Eric’s also made the news, Penn leadership remained quiet. Barstool had potential, as shareholders have taken a big SP hit?

Penn needs to hit the road and get on the business programs to tout the stock again, just my 2 cents,