Upwork: Falling Stock Price And The Power Of Perception

Summary

- Upwork Inc.'s share price has fallen by more than 60% in the past year, but the extent of bad news may already be priced into the stock.

- Upwork's business model, targeting larger enterprises and recurring collaborations, was expected to be more resilient than that of Fiverr International Ltd., but Fiverr's stock has only declined by 16% compared to Upwork's 50%.

- Upwork's newly updated terms, including a flat 10% take rate, aim to deliver more value to customers and stimulate further client demand.

- While Upwork's revenue growth rates have declined and the outlook for the end of 2023 is not favorable, the company anticipates improved profitability starting in Q4 2023, with a potential path toward 15% EBITDA margins.

- Looking for a helping hand in the market? Members of Deep Value Returns get exclusive ideas and guidance to navigate any climate. Learn More »

PixelsEffect

Investment Thesis

Upwork Inc. (NASDAQ:UPWK) has seen its share price demolished. Case in point, from the highs set in the past 12 months, this stock has fallen by more than 60%. Yes, there are plenty of issues facing Upwork. I will not declare otherwise. But what I will say is, how much of that bad news isn't already priced in?

I make the case that paying approximately 11x forward EBITDA for Upwork provides investors with an enticing risk-reward profile.

Why Upwork? Why Now?

Upwork is a freelance platform. The platform provides tools for communication and secure payment processing, facilitating the entire freelance work process.

On the surface, I would have presumed that Upwork would have been slightly more immune to an economic downturn than Fiverr International Ltd. (FVRR), since Upwork's business predominantly targets larger enterprises and more of a recurring collaboration rather than small one-off tasks, typically associated with the vulnerable SMB (small and medium-sized business) part of the market.

And yet, as it transpires, Fiverr is only down 16% in the past 12 months, compared with Upwork, which is down 50%.

In hindsight, it appears that Upwork's sticky customer base, wasn't so sticky after all. And what's even more interesting, is that Upwork's newly updated terms call for a flat 10% take rate which is indeed quite low, particularly when compared to Fiverr's, which is about 3 times higher.

Furthermore, consider that up until this point, Upwork had been increasing its take rate in an effort to drive revenues higher.

UPWK SEC filing

Indeed, it appears that Upwork believes it can deliver more value to customers by reducing their take rate.

Here's a quote from the earnings call that provides further context into the thought behind this action:

We did conclude that the new flat fee structure is both simpler, which has a huge benefit for customers.

And also has really positive impact in terms of reducing pricing for the vast majority of talent and relationships that actually will unlock stimulate further client demand, which is the number one thing that freelancers care about other than making sure that they get paid for.

Those are the two things that people want more jobs, and making sure that they get paid for the work they're doing.

In a nutshell, Upwork is striving to stimulate the health of its platform. Because for now, Upwork's outlook for the end of 2023 leaves a lot to be desired.

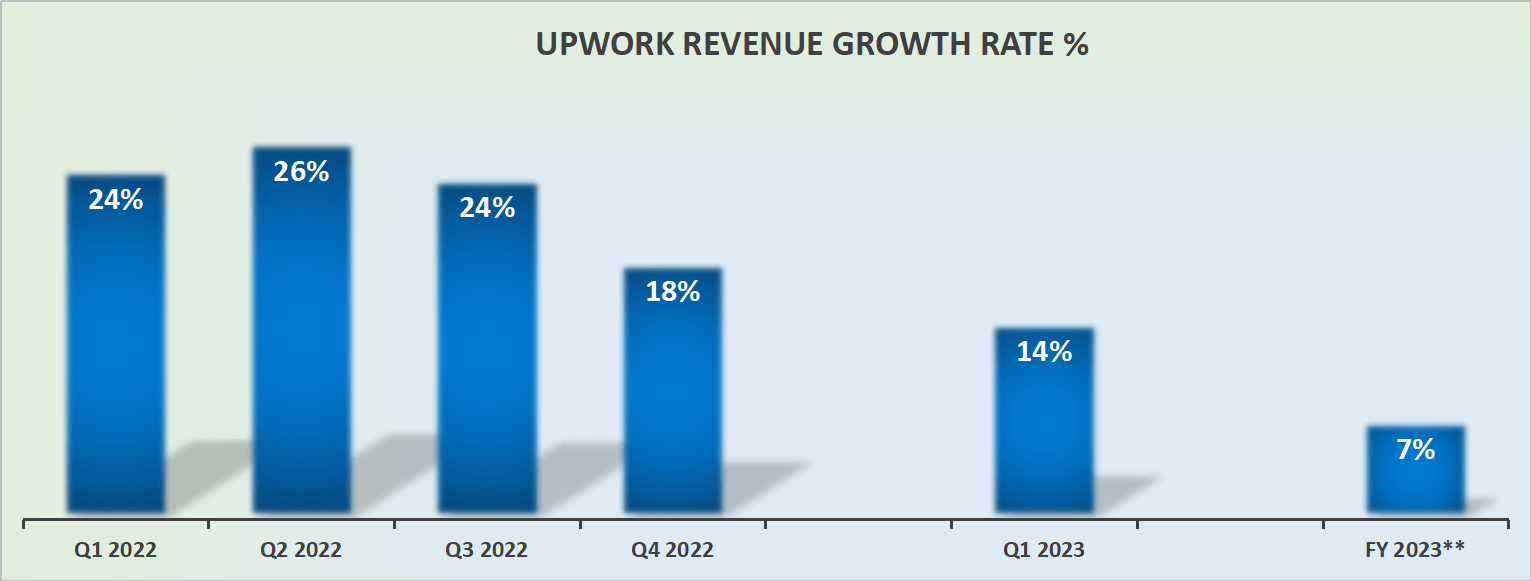

Revenue Growth Rates Fizzled Out, What's Next?

UPWK revenue growth rates

As alluded to already, there's very little to entice investors to seriously consider Upwork. After all, this is a company that 12 months ago could be counted on for 26% y/y revenue growth rates.

And what's Q2 likely to end up as? I would be positively surprised if Upwork could deliver half the growth rate it reported in the same period a year ago.

Particularly given that management is actively seeking to cut costs and reduce the size of its workforce. Consequently, allow me to state the obvious now. Expectations among investors are extremely low.

Profitability Profile Could Improve Starting Q4 2023

Before discussing Upwork's profitability, it's worthwhile to get an understanding of Upwork's balance sheet. As of Q1 2023, Upwork's balance sheet had a net cash position of approximately $150 million.

Given that the business is expected to return to profitability later in 2023, this means that there's more than enough cash on its balance sheet and that the business has no near-term restrictions. Needless to say, that's a positive aspect.

Looking out to the back end of this year, Upwork's guidance implies that it will be on a path toward 15% EBITDA margins.

Consequently, if we were to presume that in 2024, Upwork's revenues could grow by somewhere around 10% in 2024, this would mean that Upwork could in 2024 report about $110 million of adjusted EBITDA.

This would put the stock priced at about 11x next year's EBITDA. For perspective, consider this.

It wasn't long ago that investors were paying more than 6x forward sales for Upwork. Today, I'm making the argument that paying around 11x forward EBITDA is a very compelling entry point.

The Bottom Line

Upwork has experienced a significant decline in its share price, dropping by over 60% from its highs set in the past year.

While the company faces various challenges, the question arises as to how much of the negative news is already reflected in its stock price?

I believe that paying around 11 times forward EBITDA for Upwork offers an appealing risk-reward profile for investors.

Further, Upwork's revenue growth rates have fizzled out, and Upwork's outlook for the end of 2023 is not enticing.

And yet, despite these challenges, Upwork still guides for alluring profitability for Q4 2023.

With a potential path toward 15% EBITDA margins and some projected revenue growth, I estimate that Upwork's stock is valued at around 11 times forward EBITDA. I declare that this is an attractive entry point.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.

This article was written by

DEEP VALUE RETURNS: The only Marketplace with real performance. No gimmicks. I provide a hand-holding service. Plus regular stock updates.

We are all working together to compound returns.

WARNING: Any stocks that you feel like buying after discussions with me are your responsibility.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (1)