Hut 8 Mining: Starting To Get Answers

Summary

- Hut 8 Mining's recently announced merger with USBTC is still on track.

- The merger brings more production capacity to Hut 8 and new revenue segments. But that growth comes with a cost.

- As of December 31st, USBTC had just $6.7 million in cash, $750k in BTC, and $265 million in total liabilities.

- BlockChain Reaction members get exclusive access to our real-world portfolio. See all our investments here »

adventtr

Hut 8 Mining (NASDAQ:HUT) is a Bitcoin (BTC-USD) mining company that I covered for Seeking Alpha earlier this year. At one point, HUT happened to be my largest BTC mining equity position. However, since the proposed merger with US Bitcoin Corp ("USBTC"), I've taken a much more cautious outlook for HUT shares as I've moved to the sidelines while we wait out merger finalization. If you're not familiar with what I wrote back in January and February, I'd encourage you to also read those notes as well:

- Hut 8 Mining: More Questions Than Answers, 1/11/23

- Hut 8: Even More Questions Now, 2/16/23

The purpose of this article will be to add context to my previous HUT coverage given the latest information.

New HPC Client

In early 2022, Hut 8 completed the purchase of its high-performance computing subsidiary TeraGo. Since then, growth in that category has been slow nominally even though the segment has become a larger portion of the company's total revenue by percentage:

| Q1-22 | Q2-22 | Q3-22 | Q4-22 | Q1-23 | |

|---|---|---|---|---|---|

| Total Revenue | $53,333 | $43,845 | $31,671 | $21,833 | $19,021 |

| HPC Revenue | $3,290 | $4,711 | $4,403 | $4,487 | $4,495 |

| HPC % of Total | 6.2% | 10.7% | 13.9% | 20.6% | 23.6% |

Source: Hut 8, 000s of CAD

On June 14th, Hut 8 announced a new HPC services client in the healthcare sector. The agreement is for 5 years with a company called Interior Health and the services will go through Hut's Kelowna location. We don't yet know what the revenue from the agreement will look like but we do know the deal goes through 2028. If my interpretation of the press release is correct, Hut won't see realized revenue from this agreement until first quarter 2024.

Revised Merger Details

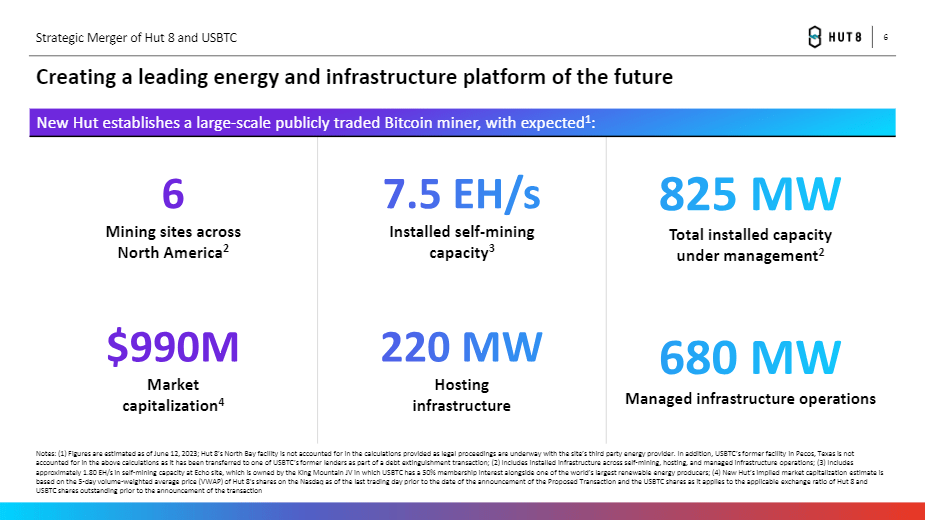

The company also recently revised the post-merger "New Hut" mining capacity projection higher to 7.5 exahash. This revision up in mining capacity is as a result of additional miner energization at US Bitcoin's mining sites.

June Investor Deck, Slide 6 (Hut 8)

In addition to the fresh capacity figures, we now also have more insight into what US Bitcoin Corp's balance sheet looked like at the end of 2022. My expectation in February was that USBTC's financial position would be in tough shape:

I think we can safely assume US Bitcoin Corp is bringing some financial baggage with that EH/s capacity and probably not a lot of BTC.

That has proven to be true per Hut 8's merger prospectus. As of December 31st 2022, USBTC had about $751k in bitcoin and just $6.7 million in cash against roughly $106 million in current liabilities. USBTC also showed $157 million in non-current liabilities. The unaudited pro-forma current assets are mainly coming from Hut 8:

| Current assets | USBTC | Hut 8 | Acquisition Transaction Adjustments | Debt Extinguishmentand Joint Venture Investment | New Hut Pro Forma |

|---|---|---|---|---|---|

| Cash | 6,707 | 22,530 | -13,620 | | 15,617 |

| Accounts receivable | 110 | 1,173 | | | 1,283 |

| Cryptocurrency, net | 751 | 118,768 | 32,154 | -285 | 151,388 |

| Prepaid expenses and other current assets | 16,923 | 7,304 | -200 | -9,801 | 14,226 |

| Total current assets | 24,491 | 149,775 | 18,334 | -10,086 | 182,514 |

Source: Hut 8 S-4, figures in 000s of USD

The $13.6 million reduction in cash for the combined entity is due to banking, legal and accounting fees from the merger transaction. The $32.2 million transaction adjustment in cryptocurrency is due to revaluation of the assets from the date of the purchase rather than December 31st. Though the current Hut 8 entity is providing most of the current assets in the deal, the majority of the non-current assets come from USBTC:

| Non-Current assets | USBTC | Hut 8 | Acquisition Transaction Adjustments | Debt Extinguishment and Joint Venture Investment | New Hut Pro Forma |

|---|---|---|---|---|---|

| Property and equipment, net | 75,906 | 87,284 | | -39,917 | 123,273 |

| Right- of- use assets | 623 | — | | | 623 |

| Deposits on miners | 62,320 | — | | -20,753 | 41,567 |

| Other deposits | 6,277 | 20,097 | | -2,500 | 23,874 |

| Investment in unconsolidatedjoint venture | 100,169 | | | | 100,169 |

| Intangible assets andgoodwill | 4,427 | 11,175 | 218,787 | | 234,389 |

| Total non-current assets | 249,722 | 118,556 | 218,787 | -63,170 | 523,895 |

Source: Hut 8 S-4, figures in 000s of USD

As of December 31st, New Hut would have had $123 million in property and equipment as well as $41.5 million in miner deposits. One of the major assets USBTC is bringing to the table is the company's joint venture investment in King Mountain JV where it shares 50% of mine capacity.

As was previously noted, USBTC forfeited property to settle with a lender. We now know the value of that debt was over $97 million and settlement came primarily through relinquishing miner deposits, equipment, property, and prepaid expenses. At the end of 2022, the combined entity would have had $706.4 million in total assets, of which $182.5 million were current. Also somewhat telling is the $219 million adjustment to intangible assets and goodwill due to the transaction. I view that as a bit of a red flag.

| | USBTC | Hut 8 | Acquisition Transaction Adjustments | Debt Extinguishment and Joint Venture Investment | New Hut Pro Forma |

|---|---|---|---|---|---|

| Total current liabilities | 105,954 | 22,248 | — | -95,355 | 32,847 |

| Total non-current liabilities | 158,646 | 23,038 | 156 | — | 181,840 |

| Total Liabilities | 264,600 | 45,286 | 156 | -95,355 | 214,687 |

Source: Hut 8 S-4, figures in 000s of USD

From a debt standpoint, USBTC is still saddled with quite a bit of obligations even after adjusting for the debt extinguishment. Current HUT had just $45 million in total liabilities as of year end. That figure rockets to just under $215 million in the post-merger company. And this is obviously before factoring in any new liabilities from Q1 or Q2 of this year. Which is certainly a possibility given the losses each of these companies experienced last year as individual companies:

| 6 months ended 12/31/22 | USBTC | Hut 8 | New Hut Pro Forma |

|---|---|---|---|

| Total revenue | 45,985 | 40,488 | 86,473 |

| Total costs and expenses | 113,833 | 190,873 | 285,140 |

| Operating income (loss) | -67,848 | -150,385 | -198,667 |

| Total other expense | 15,213 | 3,350 | 5,640 |

| Loss before income tax provision (benefit) | -83,061 | -153,735 | -204,307 |

| Income tax provision (benefit) | -1,808 | — | 5,014 |

| Net loss | -81,253 | -153,735 | -209,321 |

Source: Hut 8 S-4, figures in 000s of USD

At $46 million, USBTC generated slightly more revenue than Hut 8 in the second half of 2022 and it did so while losing less money. Even when factoring in income tax provisions and adjustments from the acquisition transaction, New Hut still has a $209 million loss in the second half of last year alone. It's certainly possible the new company may be able to cut expenses and operate more efficiently as a combined entity, but this company needs much higher bitcoin prices to break even if the pro forma numbers are an indication of current operations.

Reasons for Optimism?

Even though USBTC's balance sheet is unsurprisingly in bad shape, I think it's a good sign that HUT hasn't been forced to liquidate much of the company's BTC holdings in treasury since the deal went public. Hut 8's merger was originally announced in early February. At that time, the company indicated that it would be selling both mined BTC and HODL'd BTC to pay for operations. As of January 31st, Hut 8 held 9,274 BTC in treasury.

Hut 8, Author-generated Image

As of May 31st, Hut 8 holds 9,233 BTC. This is actually up 100 BTC from the company's end of March balance. From a year to date standpoint, the company has still been able to grow holdings to a larger degree than many of large industry peers like Riot Platforms (RIOT), Marathon Digital (MARA), Bitfarms (BITF), CleanSpark (CLSK), and Cipher Mining (CIFR):

| Month-end balances | RIOT | MARA | HUT | BITF | CLSK | CIFR |

|---|---|---|---|---|---|---|

| December 2022 | 6,952 | 12,232 | 9,086 | 405 | 228 | 394 |

| May 2023 | 7,190 | 12,259 | 9,233 | 510 | 451 | 407 |

| YTD Change | 238 | 27 | 147 | 105 | 223 | 13 |

| % | 3.4% | 0.2% | 1.6% | 25.9% | 97.8% | 3.3% |

Source: Company filings, values in BTC

Only Riot Platforms and CleanSpark have been able to add more BTC to balance sheet holdings year to date.

Risks

One thing that I've maintained in almost all of my public miner coverage is my belief that most of these companies aren't great long term investments due to the declining BTC-denominated revenue from the block reward halving every four years. The recent surge in transaction fees as a percentage of the block reward can certainly challenge that viewpoint, but it remains to be seen if the Ordinals/BRC-20-driven spike in fees from May is more of a flash in the pan or if it's the beginning of a sustainable long term trend. But to be clear, that's an industry-wide risk.

More specifically to Hut 8, while we have much better insight into the balance sheet of USBTC than we did back in February, the pro forma data for the two companies is as of December 31st and a lot can change in six months. While I think it's encouraging that Hut may soon have a top 5 operating exahash figure in the public equity markets, I'm concerned that such a large portion of New Hut's projected total assets will come from goodwill and intangibles.

Summary

Hut 8 currently has one of the largest BTC treasury balances in the entire public equity market. To me, that's the only real reason to consider longing HUT shares at this point. We don't have all of our answers yet on Hut 8 Mining. But we're starting to get some of them. USBTC's balance sheet isn't terribly surprising. Going forward, I would like to see some clarity on how much revenue the company expects from the recently announced HPC deal.

If nothing else, New Hut should have a better diversified revenue segment breakout following the merger. The exahash growth and new revenue segments are coming with a price; namely quite a bit more debt. Since there are other miners that will have cleaner balance sheets and solid production capacity, I still think it's wise to wait on HUT for now.

Decode the digital asset space with BlockChain Reaction. Forget about the dog money. With over 20,000 coins, malinvestment was begging to be purged. But not every coin is disaster. In BCR I'll help you find the ones that have staying power. Service features include:

Decode the digital asset space with BlockChain Reaction. Forget about the dog money. With over 20,000 coins, malinvestment was begging to be purged. But not every coin is disaster. In BCR I'll help you find the ones that have staying power. Service features include:

- My Top Token Ideas

- Trade Alerts

- Portfolio Updates

- A Weekly Newsletter

- Full Podcast Archive

- Live Chat

Crypto Winter can be cold and brutal. But there is value in public blockchain and distributed ledger technology. Sign up today and position your portfolio for the future!

This article was written by

5 years as a media research analyst. Main coverage areas are crypto, BTC miners, and media equities. Outside of Seeking Alpha, I write the Heretic Speculator newsletter where I share additional thoughts on finance with more of a social backdrop.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of RIOT, BITF, CLSK, BTC-USD either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I'm not an investment advisor.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.