BlackRock Enhanced Capital and Income Fund has performed well in 2023 due to its focus on tech-heavy mega-cap growth names.

The fund's covered call strategy generates gains for the distribution and potential downside protection in uncertain economic times.

Despite some shifts in sector weightings, the fund's top holdings have remained consistent, with a focus on large-cap U.S. companies.

This idea was discussed in more depth with members of my private investing community, CEF/ETF Income Laboratory. Learn More »

Dragon Claws/iStock via Getty Images

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on June 5th, 2023.

BlackRock Enhanced Capital and Income Fund (NYSE:CII) has been performing well through 2023. This is thanks to the fund's emphasis on holding tech-heavy positioning into the mega-cap growth names. These exact names have been doing all the heavy lifting in the broader market. The names that, without them, the S&P 500 would be flat or slightly down throughout the year.

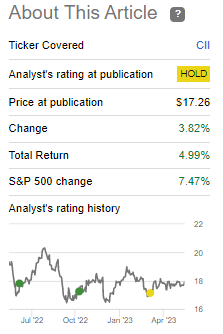

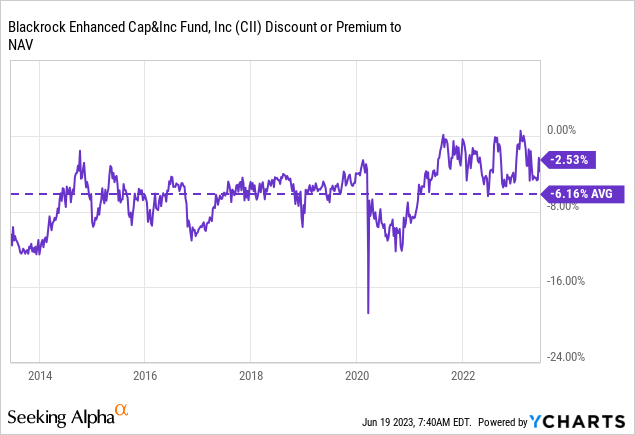

Since our previous update, the fund has performed quite well too. The last update was near the end of March. I rated it a hold at that time because the discount was quite narrow, but it was really on the fence. Today, the discount has sunk a bit lower, making it a bit more attractive.

CII Performance Since Prior Update (Seeking Alpha)

For a long-term investor, getting overly picky on the exact entry point probably isn't going to be make or break. The fund's covered call strategy could give up some upside, so if an investor is incredibly bullish, this might not necessarily be the right fit. However, for income investors, the monthly distribution and having a bit of downside protection or benefit from a flat market can be alluring.

The Basics

1-Year Z-score: 0.35

Discount: -2.53%

Distribution Yield: 6.45%

Expense Ratio: 0.89%

Leverage: N/A

Managed Assets: $832.5 million

Structure: Perpetual

CII has a simple objective and strategy; it "seeks to provide investors with a combination of current income and capital appreciation" by "investing in a portfolio of equity securities of the U.S. and foreign issuers." They will also "employ a strategy of writing call and put options."

This type of flexibility allows them to really invest wherever they'd like. However, the portfolio tends to overweight the large and mega-cap tech names. That is pretty standard for most straightforward equity funds.

The fund's expense ratio under 1% is rare in the closed-end fund space. While some may point out that ETFs can still charge lower expense ratios, the average expense ratio for an actively managed ETF is 0.70%.

So I'd consider the expense ratio quite competitive against even ETF peers. Which, again, tends to be quite rare in the CEF space.

Helping to keep this expense ratio lower is not employing any leverage. That could be another benefit if an investor is being more cautious during this uncertain economic period.

Performance - Discount Getting To An Appealing Level

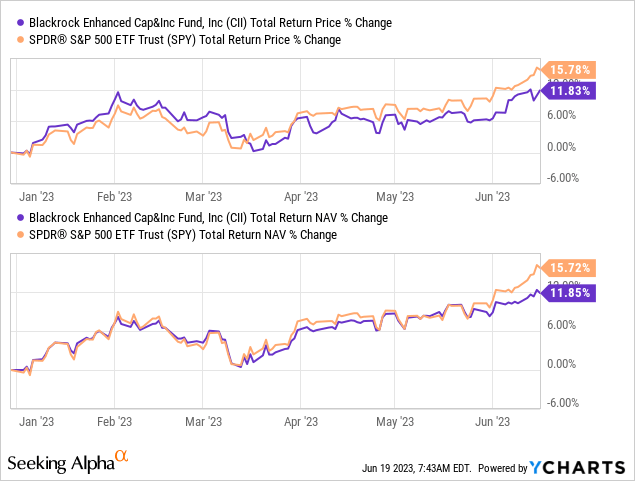

Despite the covered call strategy, the fund hasn't given up too much upside on a total NAV return basis. It was really only in the last week that (SPY) looks to have broken away from CII in a more material way.

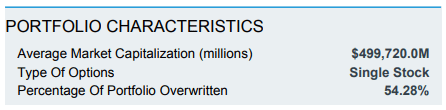

Being an actively managed fund means the managers have some flexibility in determining the amount being overwritten in their portfolio. Perhaps surprisingly, the fund last reported being overwritten by ~55.5%. That's actually fairly aggressive and above the fund's target range of 30-40%. Being around 55% overwritten was consistent with where they were at the end of March 31st, 2023, according to that fact sheet.

CII Portfolio Stats (BlackRock)

This is notable because being overwritten means potentially giving up further upside if they are overwriting stocks that are blasting higher. A covered call strategy has the benefit of bringing option premiums (capital gains) in upfront, but also capping some upside. So even despite being fairly aggressive on being overwritten, that hasn't limited the fund too significantly on a YTD basis.

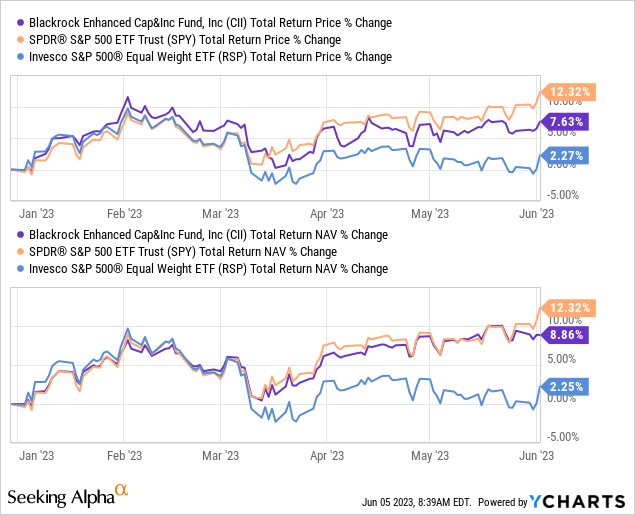

That being said, being actively managed means not only can they choose the level they are being overwritten, but they also write against single stock positions. That means they also have the flexibility to write against whatever positions they want. In their last annual report, we do see that they have written covered calls against names such as Alphabet (GOOG), Amazon (AMZN), Apple (AAPL) and Microsoft (MSFT) - however, they are also writing against a bunch of names that aren't having such a good year. Perhaps it is best reflected if we look at the Invesco S&P 500 Equal Weight ETF (RSP).

YTD, RSP is barely positive on a total return basis. I believe that really highlights that if it weren't for such an overweight to the mega-cap growth names, discussions of the 'market' would be much different this year. What it means for CII is that despite some of these covered calls probably being closed out at a loss, there could be a lot more of these covered calls that are offsetting the losses generated by the closing at a loss of the mega-cap growth names.

Ycharts

All this being said, the total share price return has lagged behind the fund's underlying portfolio results. Of course, this means that the fund's discount has widened through this period. CII is currently trading above its longer-term average, but it has come back some from the premium it touched at the start of the year. For the most part, CII has been able to buck the trend where CEFs are experiencing historically wide discounts.

Since our prior update, the fund hasn't had a new report showing updated coverage numbers. The next report should be the semi-annual report that would be available in early September if history is any indicator.

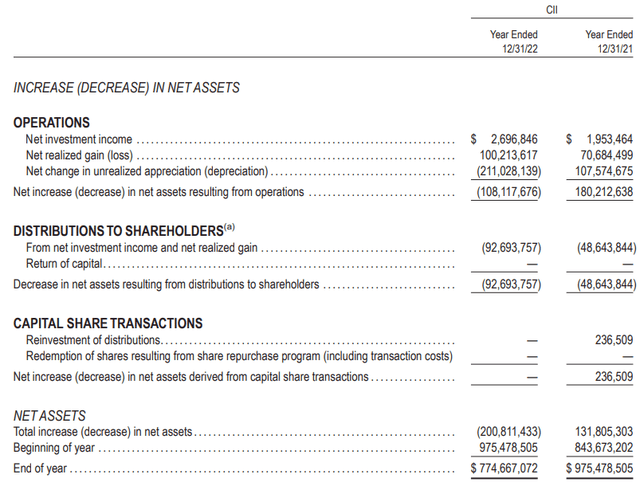

Given the NAV distribution rate of 6.73%, I think we are looking at a fairly sustainable level. That even includes the outsized year-end special of $0.90637 they paid at the end of last year. That was nearly doubling the annualized $1.194 the fund pays out now. Specials are great, but that's a lot of assets being paid out at one time that can sometimes impact the future earnings potential of the fund.

Naturally, with the distribution almost doubling, the distributions paid out to investors in the 2022 year were also doubled. They had to pay out the large year-end special due to realizing significant capital gains throughout the year. Even the realized gains they brought in last year were well in excess of the distribution amount paid out.

CII Annual Report (BlackRock)

Still, we can see that net investment income covers very little of the distribution. On a per-share basis, they reported an NII of $0.06 for 2022. Although not large on an absolute basis, on a relative basis, that was quite the jump from last year's $0.04. Of course, that's still well short of covering the fund's distribution through income.

Nothing since our previous update has changed except that the NAV rate has moved down to 6.28%, and the distribution yield on the share price has moved to 6.45%. Of course, that's the result of the fund appreciating since our prior update.

Since it is an equity fund, appreciation is essential as that will ultimately generate the ability to pay out the distribution to shareholders. As we noted above, the fund's NII is quite low and isn't nearly enough to sustain the payout to investors. Simply put, a rising NAV this year means that the distribution for CII has essentially been covered and then some.

CII's Portfolio

The turnover for CII bounced anywhere from 27 to 46% in the prior five-year period. That means the fund's management isn't overly active or inactive. That said, for the most part, the fund's overall weightings don't often change that dramatically between updates.

The fund has the ability to invest globally but mostly sticks fairly close to investing in the U.S. with mostly S&P 500 names. That's the large-cap U.S.-based companies that most investors are familiar with. Nearly 92% of the portfolio is allocated to the U.S. That's consistent with the ~93.3% that was listed previously.

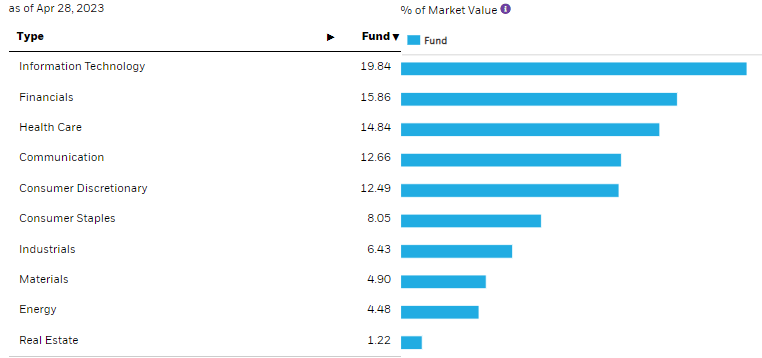

Similarly, sector weightings also remain fairly consistent. Tech has remained the largest weighting of the fund, but at the same time isn't overly overweight. It's actually less overweight to tech than the S&P 500 Index itself, where tech represents nearly 28% of the Index.

CII Sector Weighting (BlackRock)

Additionally, CII has also seen its tech weightings tick down a touch from the February 28th, 2023 level we saw previously of 23%. That may not seem too meaningful at first, but you also have to remember that during this time, that's the area of the market that has continued to perform incredibly well. Therefore, had they not made any moves and let the fund be, we'd naturally expect tech's weightings to increase during this period, not decrease. This would suggest that they actively sought to limit tech exposure.

Simultaneously, we've seen a change in the weighting of financials to nearly 16%. That had previously been around 13% of the fund. We know that financials have been under pressure due to the banking crisis. Therefore, this seems to be another conscious effort to move the fund into a more undervalued area of the market while potentially reducing an overvalued allocation of the market.

In the end, as growth continued to show strength, that could be one of the reasons why we've seen CII start to slip compared to SPY more recently in the last week or so.

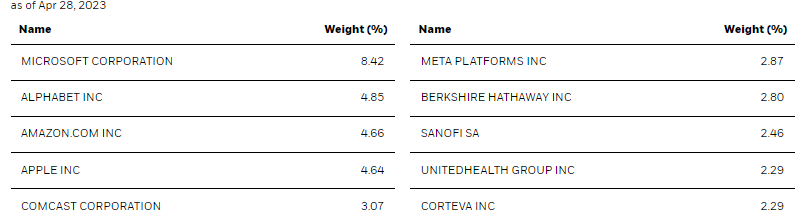

With that being said, while we saw some shifting in terms of sector weightings, overall, the top holdings haven't changed materially. In fact, it's interesting that we've seen MSFT and AAPL have increased weightings since our prior update. That would suggest that they are cutting their tech exposure to other names. MSFT was perhaps the most notable increase as it rose from the 6.59% weighting listed at the end of February 2023.

CII Top Ten Holdings (BlackRock)

Meta Platforms (META) and GOOG often get classified in the communications sector. We saw a tick higher from around 11% to 12.66% for CII's weighting in the communication sector. META and GOOG also saw their weightings increase since our prior update. Finally, AMZN get classified as a consumer discretionary stock, but in that case, we saw the sector weighting decrease to that sector for CII. It went from 14.59% to 12.49%. At the same time, AMZN saw its weight increase a touch from 4.32% to 4.66%.

This reflects that they have allowed the mega-cap growth names to grow in terms of the weightings they comprise in the fund. That was even if they were reducing exposure to the tech and consumer discretionary sectors.

Overall, I feel that the sector weightings being more spread out amongst several different allocations in fairly even amounts is a benefit. I believe that the S&P 500 and, therefore, SPY are getting too concentrated.

Conclusion

CII has been providing solid results for investors and, thanks to those results, has delivered regular and reliable monthly distributions to investors. At this time, the weighting in the fund favors mega-cap growth names, but it isn't necessarily too concentrated either. At least relative to how concentrated the S&P 500 Index itself is getting, with its weighting in tech becoming a larger and larger portion of the pie. CII can also provide some downside protection aside from being less concentrated due to its covered call strategy. A covered call strategy can work best in a flat market but can provide some gains to offset losses if the market turns lower too.

Profitable CEF and ETF income and arbitrage ideas

At the CEF/ETF Income Laboratory, we manage ~8%-yielding closed-end fund (CEF) and exchange-traded fund (ETF) portfolios to make income investing easy for you. Check out what our members have to say about our service.

To see all that our exclusive membership has to offer, sign up for a free trial by clicking on the button below!

CEF/ETF income and arbitrage strategies, 8%+ portfolio yields

Nick Ackerman is an avid student of the markets and has been investing in his own accounts for over 14 years. He is a former Financial Advisor and has previously qualified for holding Series 7 and Series 66 licenses. These licenses also specifically qualified him for the role of Registered Investment Adviser (RIA), i.e., he was registered as a fiduciary and could manage assets for a fee and give advice. Since then he has continued with his passion for investing through writing for Seeking Alpha, providing his knowledge, opinions, and insights of the investing world. His specific focus is on closed-end funds as an attractive way to achieve income as well as general financial planning strategies towards achieving one’s long term financial goals.

I provide my work regularly to CEF/ETF Income Laboratory with articles that have an exclusivity period, this is noted in such articles. CEF/ETF Income Laboratory is a Marketplace Service provided by Stanford Chemist, right here on Seeking Alpha.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of CII, MSFT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments

Disagree with this article? Submit your own. To report a factual error in this article, . Your feedback matters to us!

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.

At the CEF/ETF Income Laboratory, we manage ~8%-yielding closed-end fund (CEF) and exchange-traded fund (ETF) portfolios to make income investing easy for you. Check out what our members have to say about our service.

At the CEF/ETF Income Laboratory, we manage ~8%-yielding closed-end fund (CEF) and exchange-traded fund (ETF) portfolios to make income investing easy for you. Check out what our members have to say about our service.