SQM: Tomorrow's Electricity With Lithium's Potential

Summary

- SQM presents an undervalued opportunity with strong potential, considering lithium's demand role in EVs and flexible energy storage solutions for intermittent renewable energy.

- Here's why I believe that there's limited potential for nationalization on SQM's, or at the least that the market doesn't seem to believe so.

- Macro concerns and potential softness in EV demand weigh on lithium prospects, but recent price movements in China show a positive trend.

- Future Outlook: Anticipating improved free cash flow for SQM in the coming quarters, making the current valuation and market cap appealing.

- Looking for more investing ideas like this one? Get them exclusively at Deep Value Returns. Learn More »

onurdongel

Investment Thesis

Sociedad Química y Minera de Chile S.A. (NYSE:SQM) is cheaply valued, with what I believe are strong prospects over the next 2 years.

Here I make the case that since more than 70% of SQM's business is tied to its lithium business, this necessarily requires that we focus on lithium, by highlighting its key opportunities.

But at the same time, we should also be mindful of a key risk facing the stock, which I also discuss here.

Why invest in Lithium?

The main reason to invest in lithium is its requirement for EVs. Lithium provides terrific energy storage capacity enabling the shift toward cleaner and more sustainable transportation.

But I believe, that beyond EVs, demand for lithium will also come from the need for flexible energy storage solutions. This is a topic that is less widely discussed, but I believe it could be just as pertinent or even more than the need for lithium in EV batteries.

The way to think about lithium demand is in terms of storage of power. Renewable energy by definition is intermittent. For example, you have solar power during the day to charge solar panels (photovoltaic technology), but you may only require peak electricity in the evening when you get home in the evening and activate your heat pump to warm up your home or to charge your EVs or even to charge your electronic devices (smartphones, laptops, plus smart devices throughout the household).

Enabling that flexibility, between charging the solar panel and when you actually use that power will require energy storage, which I believe will for the most part take place through lithium battery storage.

This is my critical argument. Even though EV batteries grab the most headlines, I believe that lithium-based storage solutions will actually end up being a much bigger market for lithium demand.

Next, let's discuss the main risks of investing in SQM.

The Main Risk Facing SQM

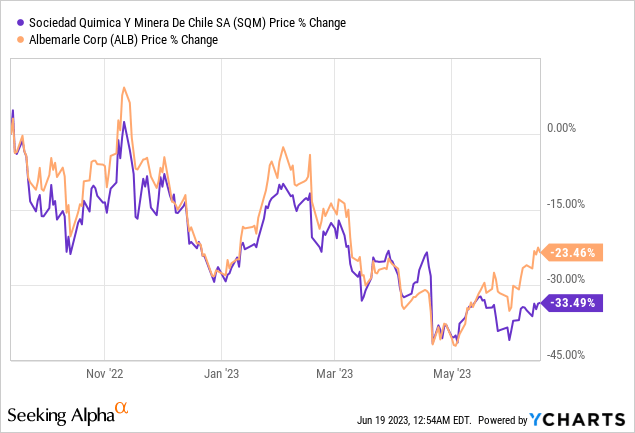

Note, I first recommended Albemarle (ALB) to Deep Value Returns members last September. And admittedly, Albemarle's stock has also underperformed.

Consequently, my point is this. Even though there's a significant risk overhanging SQM that it could be forced to in some way be nationalized, the reason the stock is down, is not only due to this consideration, given that Albemarle despite having a very different sort of business model with much longer contracts in place with Chile has also been a laggard.

Hence, this means that the market doesn't put too much emphasis on the potential for SQM to be fully or partially nationalized.

So What's Weighing on the Stock?

Even though I've been very bullish on lithium's prospects, the fact of the matter is that lithium prospects are mostly weighed down by macro concerns that we may at some point head into a recession.

And in the near term, even if we don't head into a recession, there's still a likelihood that there could be some softness in EV demand. That has been the prevailing thesis for a while.

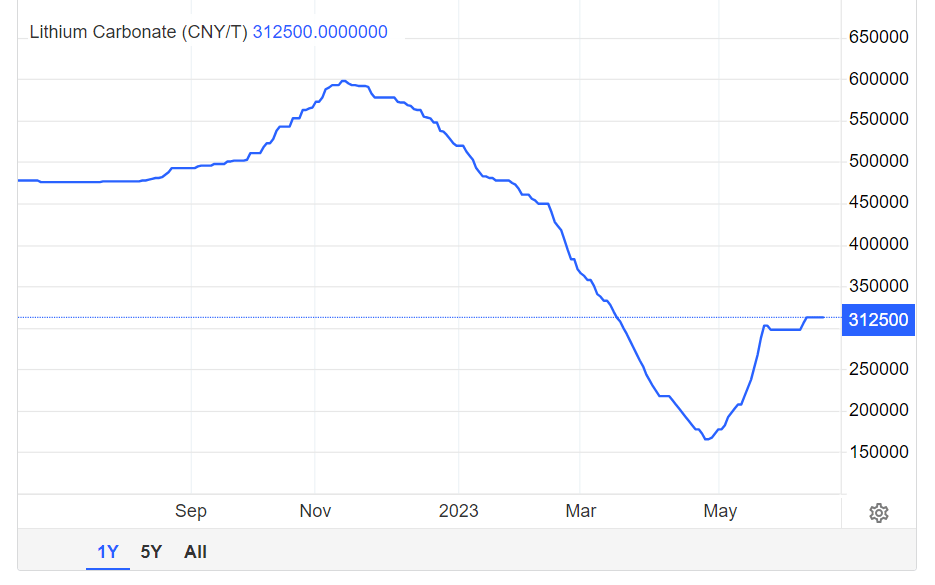

Trading Economics

Meanwhile, I point your attention to the graphic above. It shows that prices for lithium in China have moved off the lows in May. Jumping more higher than 80% from the lows. That being said, note that there are more indexes for lithium prices, depending on the country. This is a very rough proxy, not a perfect approximation for global lithium prices.

How to Think About SQM's Valuation?

SQM is a miner. Consequently, the business is extremely capital-intensive.

On the one hand, that's obviously a negative consideration. But on the other hand, this means that there's only a handful of global players that have the financial means to significantly deploy capital to ramp up production.

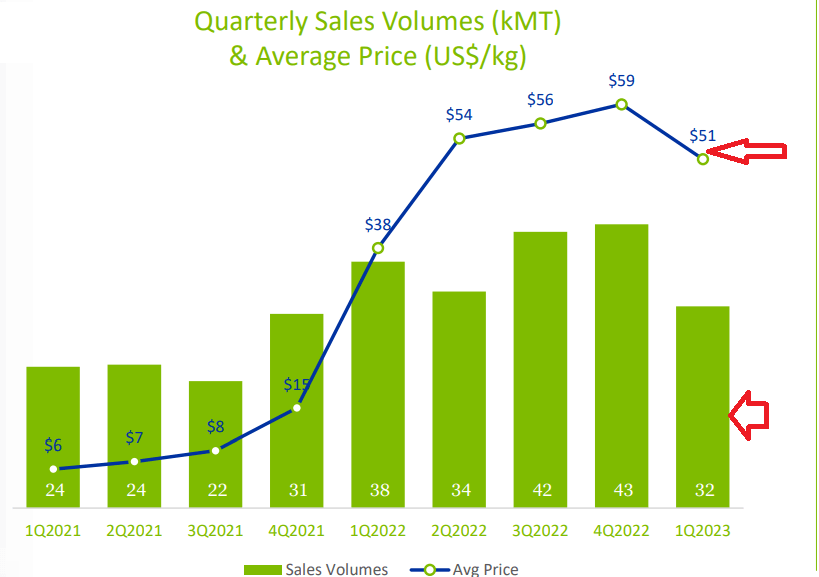

In 2022, SQM made approximately $4.9 billion of free cash flow. However, in the very near term, SQM's free cash flow isn't very strong. As discussed already, lithium prices and volumes have not been particularly strong of late.

SQM Q1 2023

But I don't believe this is where the story ends for SQM. I believe that in the coming few quarters, we'll look back to SQM when it was priced at 5x free cash flow and think that paying a $20 billion market cap for SQM was a very attractive entry point to get in.

The Bottom Line

I am excited about the prospects of Sociedad Química y Minera de Chile S.A. as an undervalued investment opportunity with strong potential over the next two years.

Investing in lithium is primarily driven by its indispensable role in EVs. Furthermore, the demand for lithium extends beyond EVs, encompassing flexible energy storage solutions for intermittent renewable energy sources.

However, it is important to consider the main risk associated with investing in SQM, which revolves around the possibility of nationalization.

The current market sentiment surrounding lithium is primarily impacted by macro concerns and the potential softness in EV demand.

While SQM's near-term free cash flow may not be strong due to recent lithium price and volume performance, I believe that in the coming quarters we will consider the current market cap of $20 billion as an attractive entry point for SQM, but only in hindsight.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.

This article was written by

DEEP VALUE RETURNS: The only Marketplace with real performance. No gimmicks. I provide a hand-holding service. Plus regular stock updates.

We are all working together to compound returns.

WARNING: Any stocks that you feel like buying after discussions with me are your responsibility.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Michael is long ALB.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.