Blackstone Mortgage: Still Priced For Doom And Gloom

Summary

- Blackstone Mortgage Trust investors have suffered the worst selloff since the COVID pandemic. However, buyers returned to defend the line in April.

- Investors are likely reflecting worst-case scenarios in assessing the opportunity in BXMT, leading to highly-depressed valuations.

- While its risk/reward profile is highly appealing, a quick recovery is not expected, as the Fed remains hawkish.

- Investors must be ready to hang on tight if they decide to add more positions.

- Ultimate Growth Investing members get exclusive access to our real-world portfolio. See all our investments here »

AlbertPego

Blackstone Mortgage Trust, Inc. (NYSE:BXMT) holders have suffered at the hands of sellers since BXMT topped out in November 2021. Despite being externally managed by a subsidiary of the world's leading alternative asset manager, Blackstone (BX), its exposure to office properties has led to significant uncertainty.

Management didn't believe it was justified for the market to use a "broad-brush" approach, as seen in BXMT's hammering. At the company's April earnings conference, CEO Katie Keenan stressed that a book value per share multiple of 0.64x "implies an over 90% impairment on all foreign-vibrated office loans, effectively a full principal loss on first mortgage loans."

The valuation dislocation has since improved, as dip buyers helped to defend the steep selloff in March. Accordingly, based on price performance and total return basis, BXMT has clawed back most of its March 2023 losses attributed to the shock due to the regional banking crisis.

However, while the crisis has subsided somewhat, BXMT's valuations remain highly depressed, in line with the broad undervaluation in the real estate sector. As a result, the sector has failed to participate in the overall market recovery, which saw S&P 500 (SPX) (SPY) notched highs last seen in April 2022. In contrast, Vanguard Real Estate Index Fund ETF Shares (VNQ) remains in the doldrums, mired at levels last seen in April 2023.

There were concerns raised at Blackstone Mortgage Trust's Q1 earnings conference that management attempted to address. However, the crux remains whether its credit loss reserve is sufficient to manage the ongoing crisis in office properties.

While management highlighted its confidence that its CECL reserve was prudent, it also acknowledged the uncertainties holders must be aware of when deciding whether to add more exposure. Keenan stressed that it's "possible to see more reserves over time." She added that the "environment is dynamic, reserves have been raised significantly in recent quarters, but future changes are uncertain." As such, I believe investors must take a more prudent approach with BXMT, reflecting a significant discount against its historical valuation average to assess its risk/reward profile.

Management indicated that its lower reserve levels compared to the regional banks were predicated on a reasonable basis. The company stressed that its "more granular" approach to determining the level of reserves is more appropriate for Blackstone Mortgage Trust than the "macroeconomic statistical models" adopted by banks. Therefore, management believes it offers them more clarity over their loss modeling.

Given their scale and pedigree, I don't doubt Blackstone's expertise in commercial properties. However, in a highly uncertain environment where risks could escalate if the macroeconomic conditions worsen, Blackstone's pedigree might not be sufficient to mitigate the challenges. Furthermore, management acknowledged that "future changes are uncertain," necessitating investors to reflect "worst-case scenarios" in BXMT's valuation before dip buyers could have the confidence to return.

Hence, I believe the critical question facing investors is whether BXMT's price action and valuation reflect such a scenario analysis.

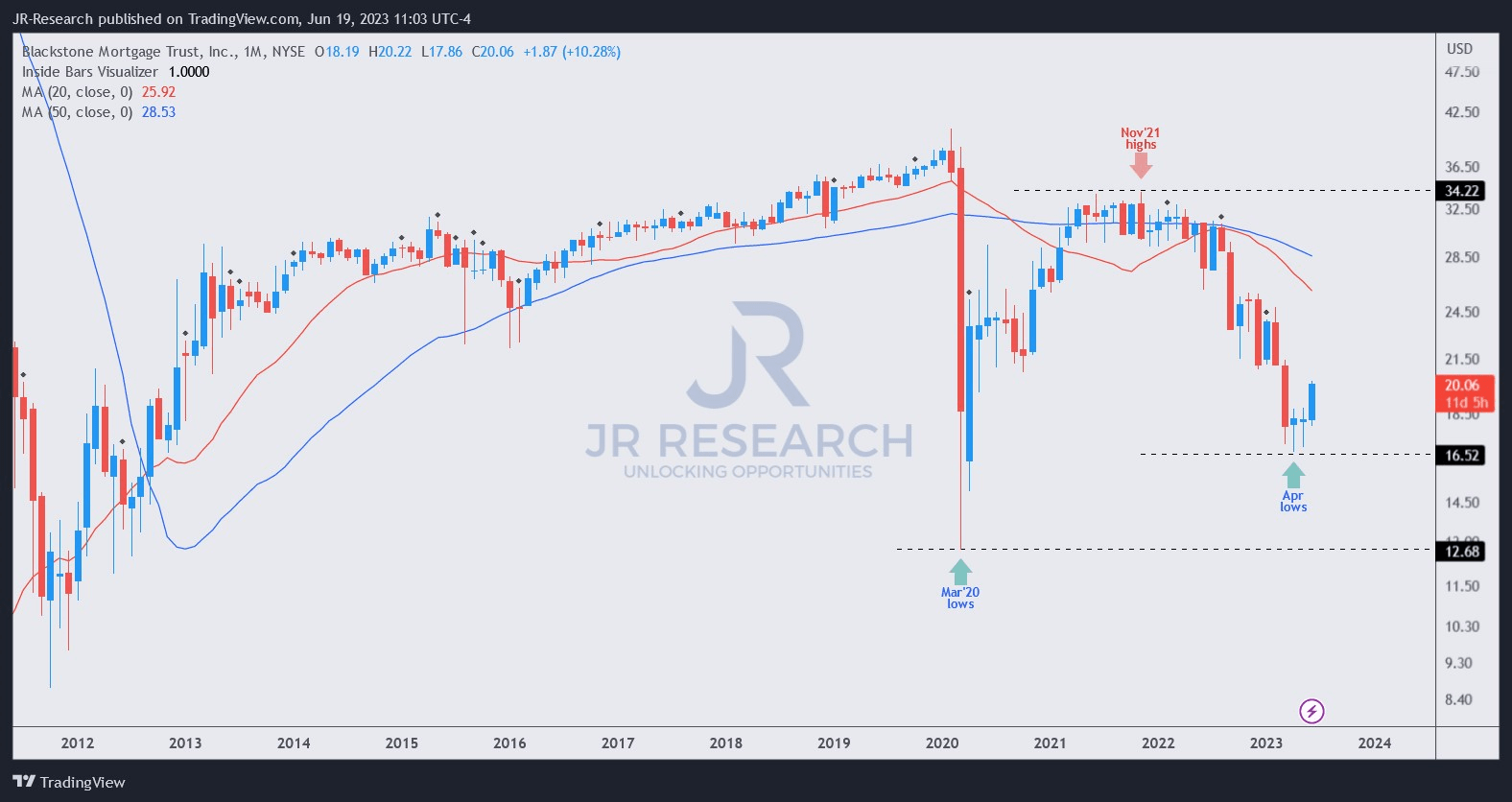

BXMT price chart (monthly) (TradingView)

As seen above, BXMT's price action indicated the worst selloff since the waterfall decline triggered by the COVID pandemic in early 2020.

I don't expect such a rapid mean-reversion recovery from BXMT this time, given the Fed's still hawkish stance. Despite that, BXMT remains well-primed to benefit from a well-battered valuation that reached its bottom in April. At 6x its forward distributable earnings, it is below the two standard deviation zone under BXMT's 10Y valuation average. In other words, it reached highly attractive zones in April.

While BXMT's valuation has recovered somewhat, it's still only 7.5x, well below its 10Y average of 12.2x. However, as highlighted, I don't expect buyers to re-rate BXMT much further upward in the near term to reflect significant risks over commercial real estate properties, coupled with its reserves modeling.

Hence, investors looking to add more exposure need to be very patient while riding out the volatility in the near term. However, the risk/reward is appealing, and I assessed that steep pullbacks should be capitalized, given the significant undervaluation zones that were robustly defended in April and May.

Rating: Buy.

Important note: Investors are reminded to do their own due diligence and not rely on the information provided as financial advice. The rating is also not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have additional commentary to improve our thesis? Spotted a critical gap in our thesis? Saw something important that we didn’t? Agree or disagree? Comment below and let us know why, and help everyone in the community to learn better!

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA's bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!

This article was written by

Ultimate Growth Investing, led by founder JR Research, helps investors better understand a range of investment sectors with a focus on technology. JR specializes in growth investments, utilizing a price action-based approach backed by actionable fundamental analysis. With a powerful toolkit, JR also provides insights into market sentiments, generating actionable market-leading indicators. In addition to tech and growth, JR also offers general stock analysis across a wide range of sectors and industries, with short- to medium-term stock analysis that includes a combination of long and short setups. Join the community today to improve your investment strategy and start experiencing the quality of our service.

Seeking Alpha features JR Research as one of its Top Analysts to Follow for the Technology, Software, and the Internet category, as well as for the Growth and GARP categories.

JR Research was featured as one of Seeking Alpha's leading contributors in 2022.

About JR: He was previously an Executive Director with a global financial services corporation and led company-wide, award-winning wealth management teams consistently ranked among the best in the company. He graduated with an Economics Degree from Asia's top-ranked National University of Singapore and currently holds the rank of Major as a Commissioned Officer (Reservist) with the Singapore Armed Forces.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.