Lantheus: Pylarify And Definity Driving Strong Growth

Summary

- Lantheus is growing revenue and earnings at an above-average pace.

- The strong pipeline of Phase 3 compounds can sustain growth for multiple years.

- The attractive low valuation and strong growth makes it likely that Lantheus' stock outperforms over the long term.

- Looking for a helping hand in the market? Members of Margin of Safety Investing get exclusive ideas and guidance to navigate any climate. Learn More »

Love Employee/iStock via Getty Images

Lantheus Holdings (NASDAQ:LNTH) looks like a long-term winner in the medical diagnostics field with strong sustainable growth. The company is a key player in radiopharmaceuticals and therapeutic and diagnostic products. Lantheus' strong projected growth from a reasonable valuation should allow the stock to outperform the broader market.

Lantheus' Key Products Driving Growth

Lantheus has multiple products on the market with two standouts driving the most growth with Pylarify and Definity. Pylarify is the largest growth driver for the company as it comprised 65% of total Q1 2023 revenue. Pylarify's revenue more than doubled in Q1 2023 over Q1 2022 from $92.7 million to $195.5 million.

Pylarify is a radioactive diagnostic agent for men with suspected prostate cancer metastasis who are candidates for initial therapy or suspected recurrence based on elevated PSA levels. Pylarify is an effective diagnostic as it uses a combination of detection factors such as pet imaging for accuracy, PSMA targeting for precision, F-18 radioisotope for clarity, and AI (artificial intelligence) for consistency. These factors give Pylarify advantages over conventional diagnostics such as MRIs, CT scans, and bone scans.

Pylarify achieved FDA approval two years ago. However, Lantheus has a near-term potential catalyst as it is pending EU approval. Recently, a panel of advisors to the European Medicines Agency recommended its approval. An EU approval would be a significant growth catalyst, as 30 million men are diagnosed with prostate cancer in their lifetime in Europe.

The other main driver for Lantheus is Definity, the company's high-resolution echocardiogram enhancement that comprised 23% of total Q1 2023 revenue. Definity provides prolonged enhancement at a low dose, so patients can get accurate echocardiograms and diagnoses. Definity revenue increased 18% in Q1 2023 over Q1 2022 to $68.8 million.

One of the reasons Definity is a strong growth driver is because 4 out of 5 contrast enhanced echocardiograms use it in the United States. Another reason is because of the high prevalence of heart disease in the United States. According to the CDC, one person dies of cardiovascular disease every 33 seconds in the United States. Heart disease is the leading cause of death in the United States. About 1 in 20 adults over 20 years of age have cardiovascular disease. Therefore, Definity is an important tool for obtaining accurate echocardiograms.

Lantheus also has two other FDA approved compounds on the market, with Azedra and TecheLite. However, they comprise a smaller portion of total revenue. TechneLite comprised about 7% of total revenue in Q1 2023. Azedra's sales are less than that and are not listed individually on the company's 10-K report. Sales of TechneLite declined 7% in Q1. So, I don't consider these two as growth drivers for Lantheus.

The Pipeline

In addition to having Pylarify filed for a potential EU approval, Lantheus has multiple compounds in the pipeline. Lantheus has 2 other compounds in Phase 3 clinical trials related to prostate cancer - one for diagnosing metastatic prostate cancer and another for detecting localized prostate cancer and bone metastases.

Definity is in Phase 3 for pediatric echocardiography. Revenue for Definity can expand if this indication achieves an approval. About 1.3% of U.S. children have a heart condition.

Lantheus has PNT2003 in Phase 3 for detecting neuro-endocrine tumors and Flurpiridaz in Phase 3 to assess myocardial perfusion. With 5 compounds in Phase 3 clinical trials, Lantheus has a strong pipeline that can keep growth going over the next several years if these can achieve FDA/EU approvals.

Lantheus also has 6 compounds in earlier phases of development. These can help provide a longer runway for ongoing growth.

The Growth Outlook

Lantheus is profitable with strong growth ahead. The company is expected to grow revenue at over 34% in 2023 and a little under 12% in 2024 according to consensus estimates. Earnings are expected to grow at over 32% in 2023 and over 11% in 2024. The average 3 to 5 year CAGR for earnings is expected to be about 15%.

Revenue and earnings estimates have been revised upwards over the past 3 months by significant amounts. Revenue estimates increased about 8.6% for 2023 and 9% for 2024. Earnings estimates increased 12.4% for 2023 and 11% for 2024. These upward revisions should have a positive effect on the stock if they are achieved or exceeded.

Lantheus' profitability is being driven by a gross margin of 63% vs. the sector median of 56% and an EBITDA margin of 14.5% vs. the sector median of 3.5%.

Valuation

Lantheus is trading with a reasonable valuation, with a forward PE of 16 and a PEG ratio of 1.07. This is below the sector median forward PE of 20 and PEG of 2.13. Lantheus also trades below the S&P 500's (SPY) forward PE of 18.8.

I like to see the PEG below 2 for strong growth companies. The stocks that I cover tend to perform well and have running room when the PEG ratios are below 2. With a PEG near one, Lantheus' stock has plenty of upside potential.

Technical Perspective

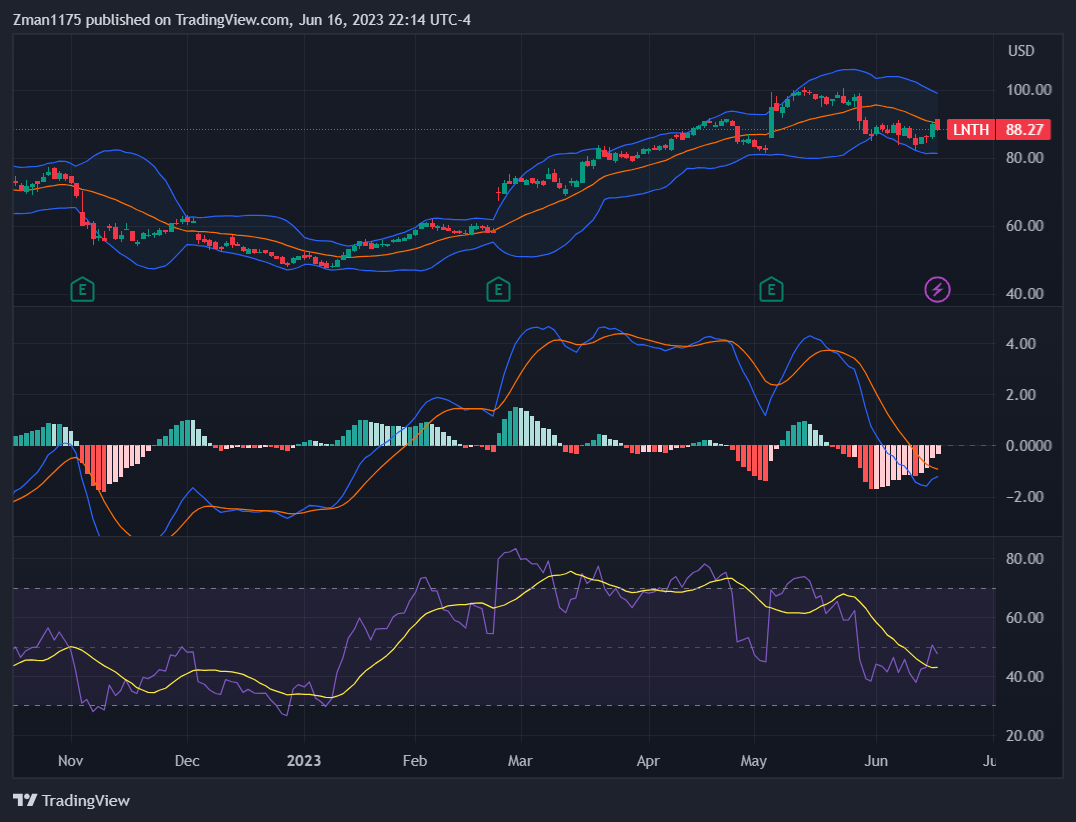

Lantheus: stock price, MACD, RSI (tradingview.com)

Lantheous' daily chart shows that the stock price appears to be recovering from the recent dip. The MACD indicator (middle of the graph) shows that the negative momentum is subsiding, with a potential positive crossover about to occur (blue line about to cross above the red signal line). The RSI (bottom of the chart) looks positive as it moved higher close to the 50 mark. A move above the 50 mark would indicate positive momentum. Potential investors might want to wait for a MACD positive crossover (blue line crossing above the red line) would confirm a new uptrend. This would be confirmed with the RSI sustaining a move above the 50 level.

Lantheus' Long-Term Investment Outlook

Lantheus looks like a promising investment over the next several years. Pylarify and Definity are driving strong growth in the near term. Pylarify's pending EU approval is also a near-term possible positive catalyst. The company's pipeline could provide continued growth over the next few years. Having 5 compounds in Phase 3 (the last stage of clinical trials), Lantheus has the potential to sustain steady growth for multiple years.

Investors should also watch for any potential acquisitions which have been a part of Lantheus' growth strategy. The company announced the acquisition of Cerveau Technologies in February 2023. This acquisition would bring a new asset to Lantheus with MK-6240, an F-18 labeled PET imaging agent that targets Tau tangles in Alzheimer's disease. MK-6240 is currently in a Phase 3 clinical trial.

Investors should be aware that the stock can be highly volatile, with above-average swings in price. This is one of the main risks for the stock. Another risk is the possibility that one or more compounds in clinical trials do not achieve FDA/EU approvals. As a result of this, investors should consider Lantheus as a stock with above-average risk.

With the attractive valuation and strong above-average potential revenue and earnings growth, I expect Lantheus to outperform the S&P 500 over approximately the next two years and possibly longer depending on if and when other compounds get approved. Analysts have a one-year price target of $122 for the stock, which would be about 39% above the current price. The target price would take the PE to about 19.6 based on expected EPS of $6.24 for 2024. That would still be below the Drug Manufacture-Specialty & Generic industry's PE of 30.

Consider joining Kirk Spano's Margin of Safety Investing which offers a more in-depth analysis of individual companies.

Try Margin of Safety Investing free for two weeks and get your first year for 20% off.

Learn the 4-step investment process that top hedge funds use.

Invest with us in a changing world that demands a margin of safety.

This article was written by

Through diligent analysis, he is ranked in the top 1% of blogging analysts on Tipranks.com for performance and accuracy. David previously contributed to Kirk Spano's Margin of Safety Investing [MoSI] Marketplace Service and Risk Research Inc.

David focuses on growth & momentum stocks that are reasonably priced and likely to outperform the market over the long-term. He is a long term investor of quality stocks and uses options for strategy.

David told investors to buy in March 2009 at the bottom of the financial crisis. The S&P 500 increased 367% and the Nasdaq increased 685% from 2009 through 2019.

He wants to help make people money by investing in high-quality growth stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of LNTH either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The article is for informational purposes only (not a solicitation or recommendation to buy or sell stocks). David is not a registered investment adviser. Investors should do their own research or consult a financial adviser to determine what investments are appropriate for their individual situation. This article expresses my opinions and I cannot guarantee that the information/results will be accurate. Investing in stocks involves risk and could result in losses.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.