Fed Blinks, And It's Long Overdue

Summary

- U.S. equity markets climbed for a fifth-straight week after inflation data showed a continued cooldown in price pressures, allowing the central bank to pause its historically-aggressive rate hiking cycle.

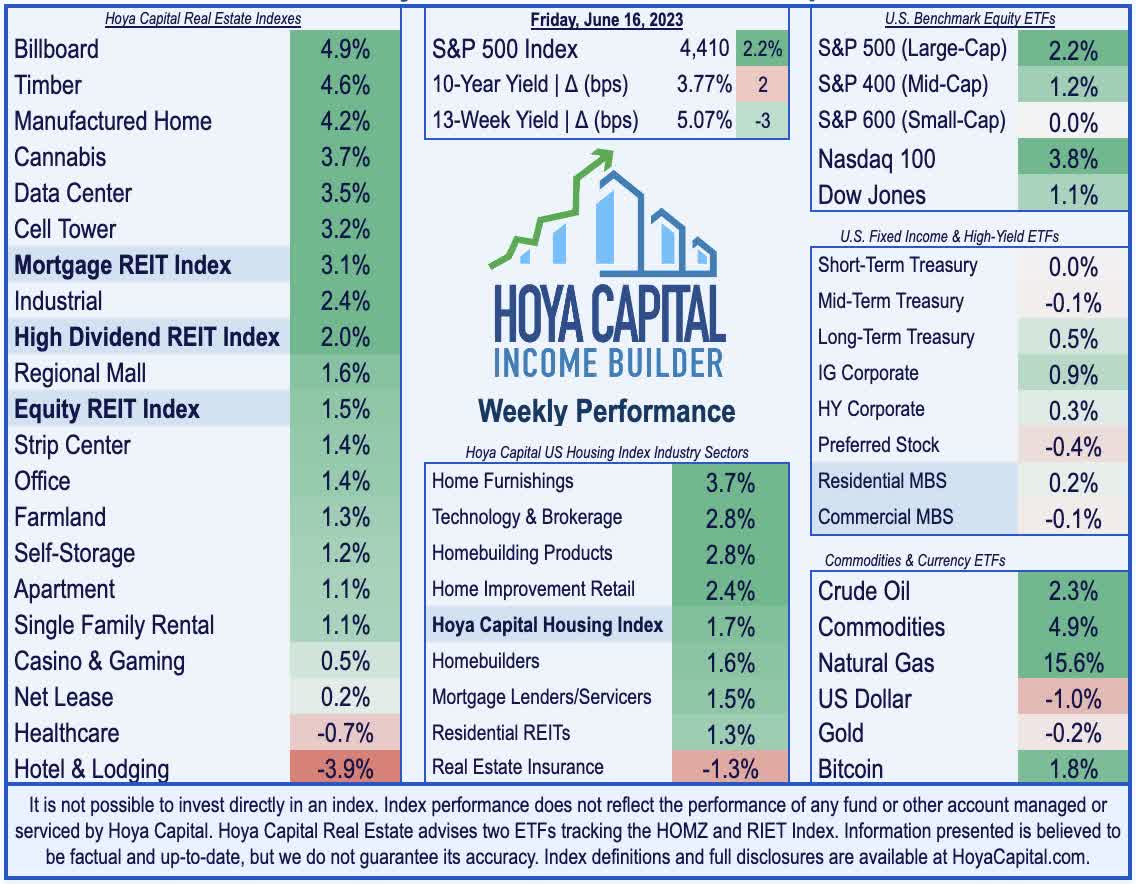

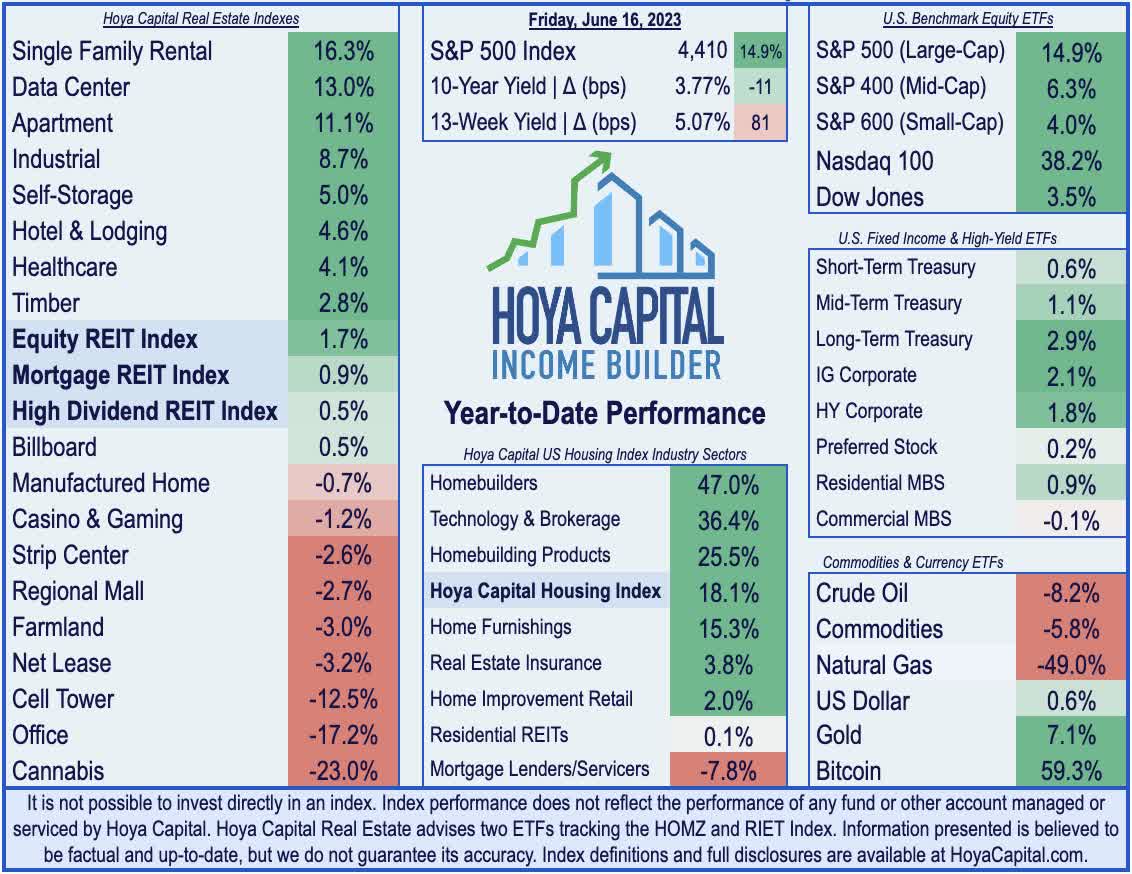

- Notching its longest weekly winning streak since November 2021, the S&P 500 advanced 2.2% this week, which lifted the major benchmark to levels that are now 23% above its October lows.

- Real estate equities also delivered a relatively strong week, an industry group that is perhaps the most directly impacted by the potential pivot in Fed monetary policy.

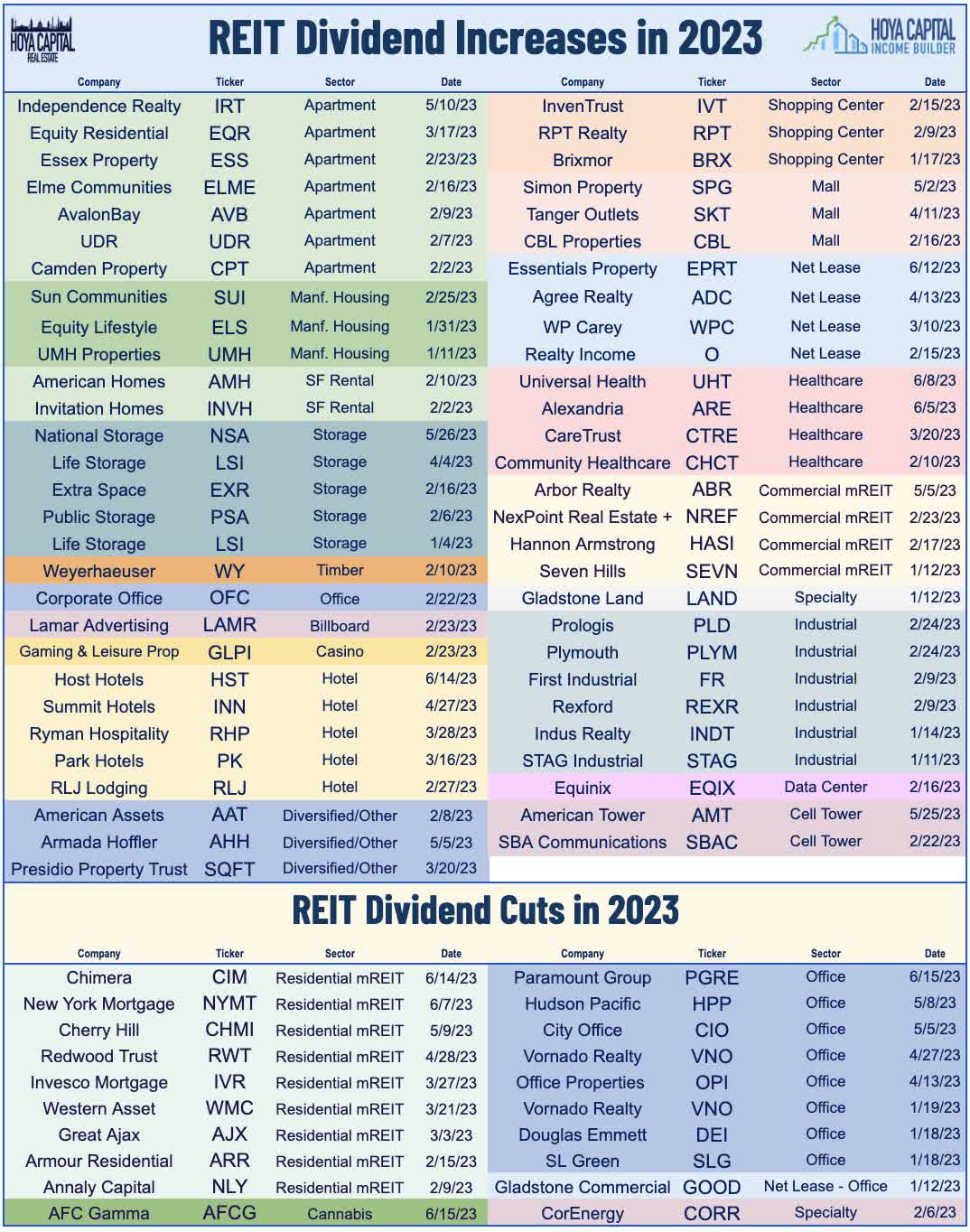

- We're in the midst of REIT dividend season. Five REITs raised their dividends this week - highlighted by a 15% increase from Host Hotels - but five REITs lowered their payouts, including a 55% cut from office REIT Paramount Group.

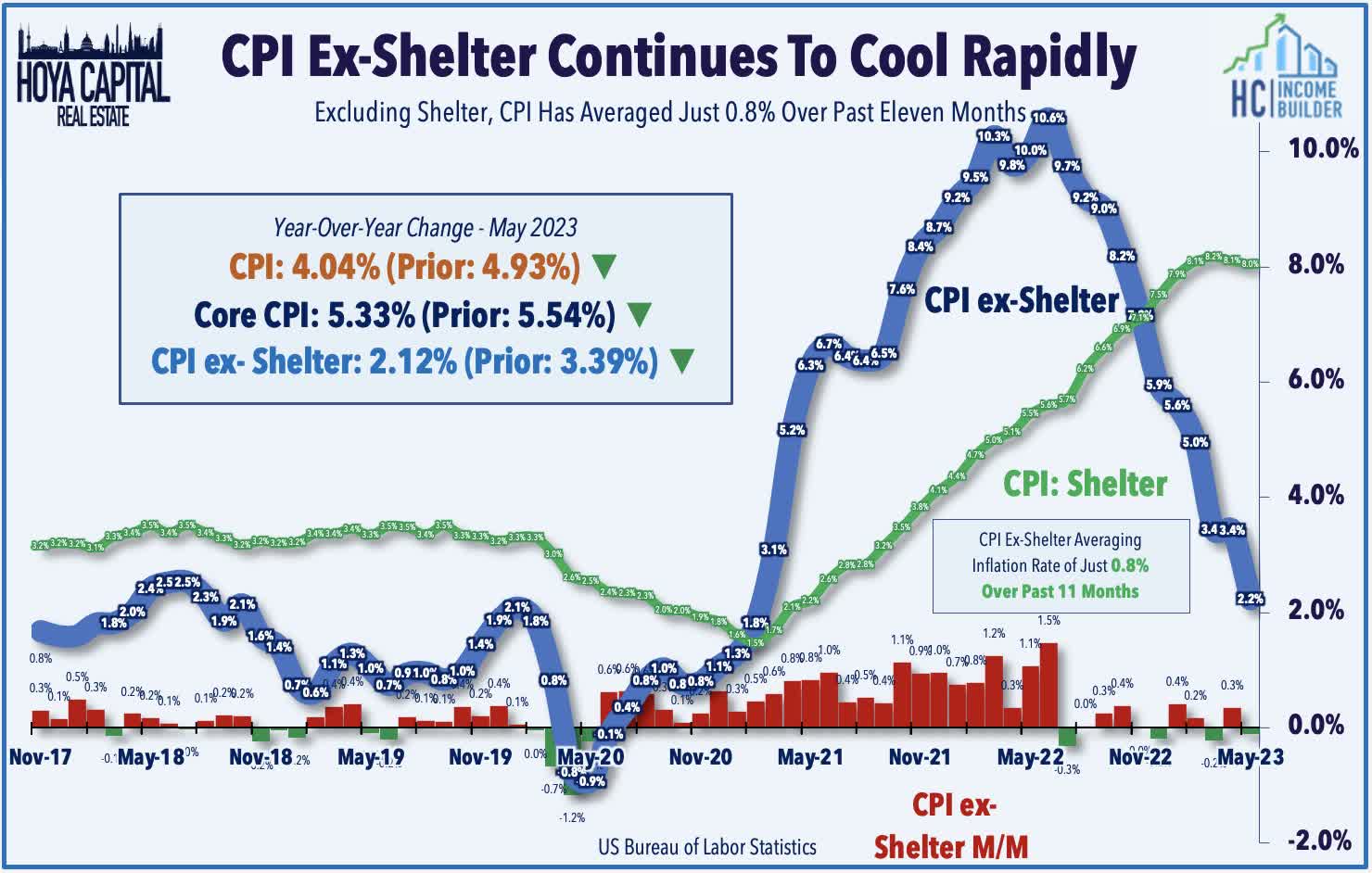

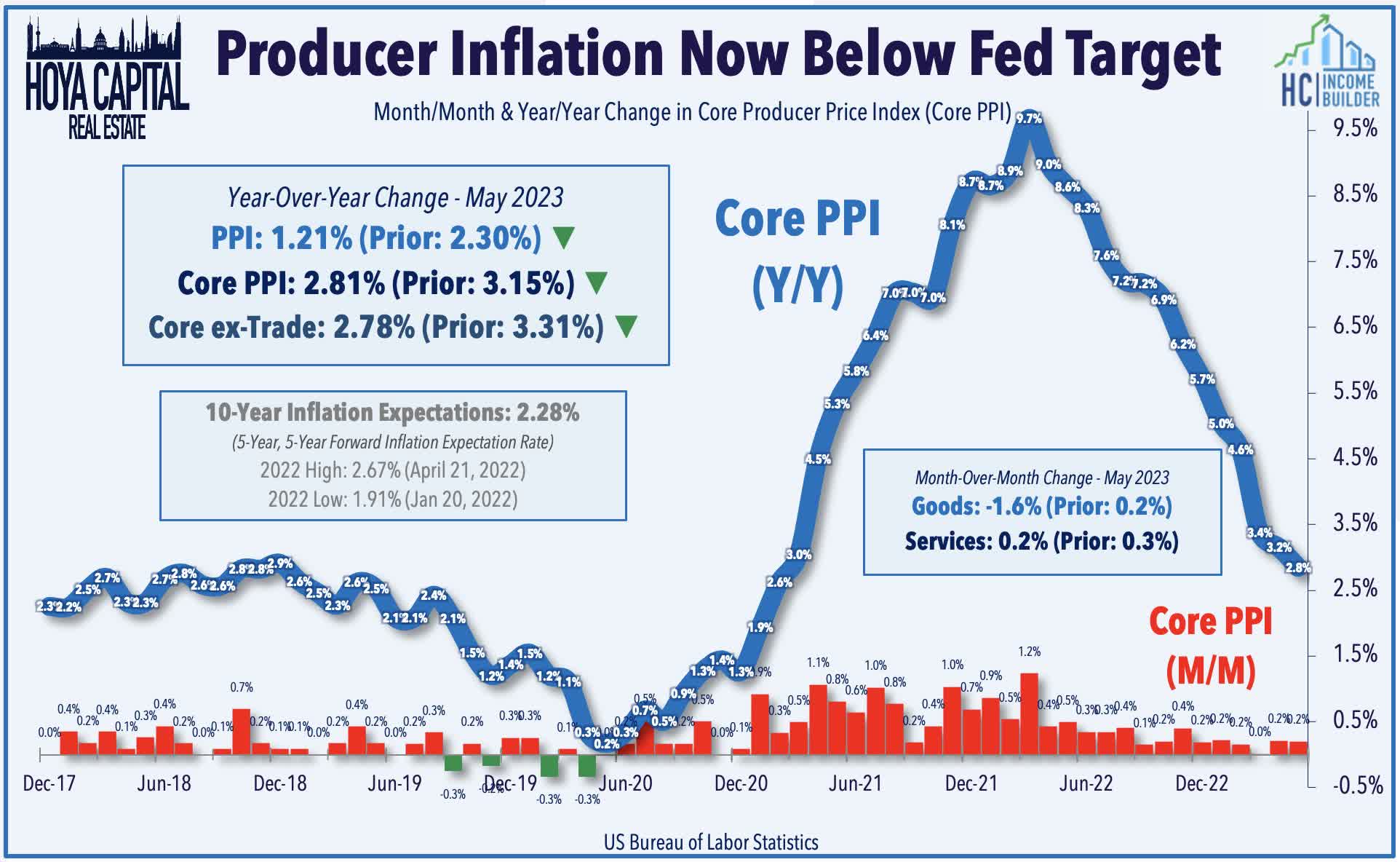

- Both major inflation reports this week revealed that 'real-time' inflation has been running below the Fed's 2% target level since last June. The CPI ex-Shelter has increased just 0.7% over the past eleven months while the PPI Index has increased just 0.3% during that time.

- I do much more than just articles at Hoya Capital Income Builder: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

Andres Victorero

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on June 16th.

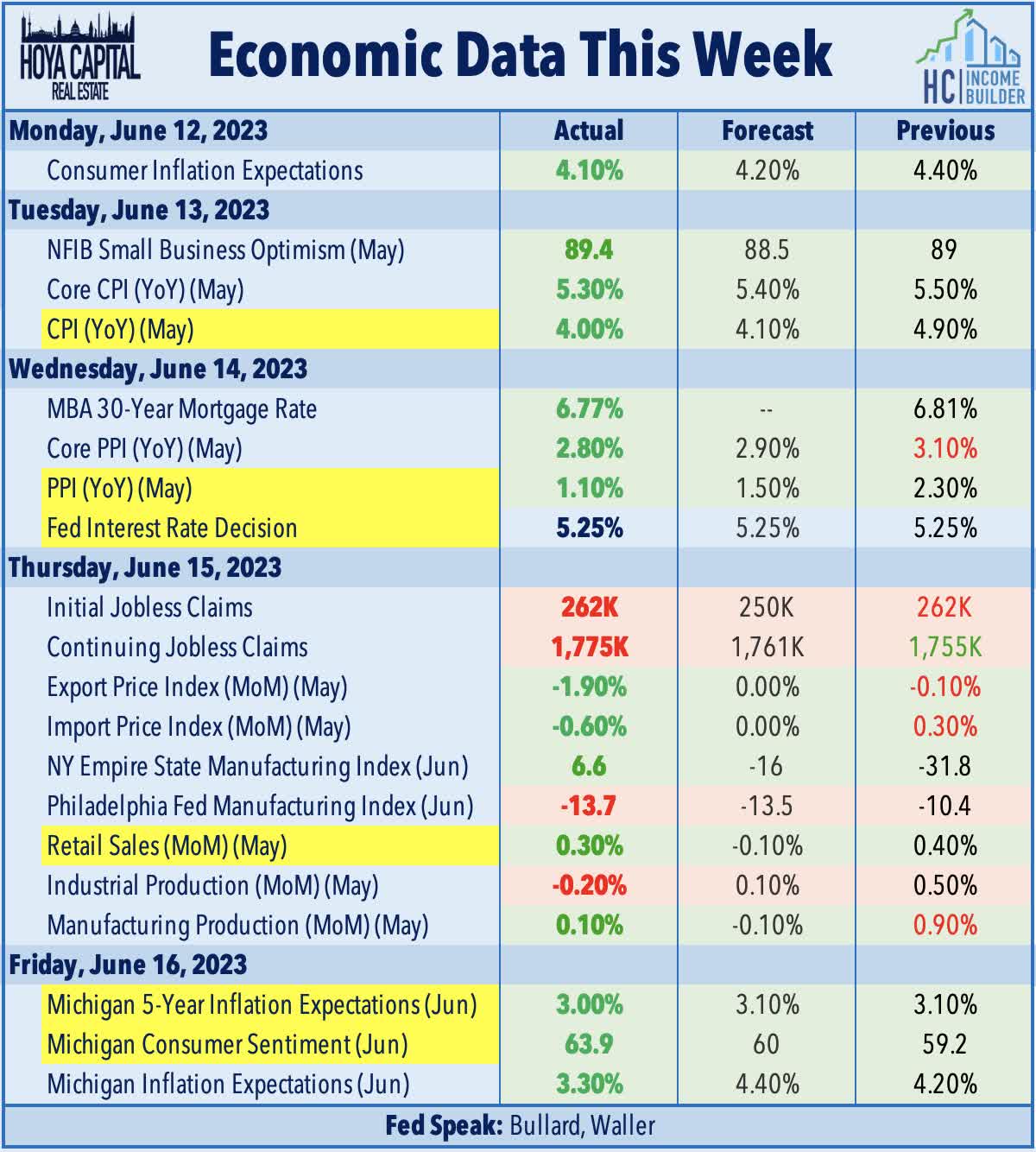

U.S. equity markets climbed for a fifth-straight week after inflation data showed a continued cooldown in price pressures, allowing the central bank to pause its historically-aggressive rate hiking cycle. As anticipated, the Federal Reserve left the benchmark lending rate at a 5.25% upper-bound, but indicated that at least one more rate hike is still on the table until it sees "credible evidence that inflation is topping out." The comments were 'on brand' for a central bank whose actions and commentary have consistently lagged six-to-nine months behind current economic conditions, coming just hours after both major inflation reports revealed that 'real-time' inflation has been running below the Fed's 2% target level since last June.

Hoya Capital

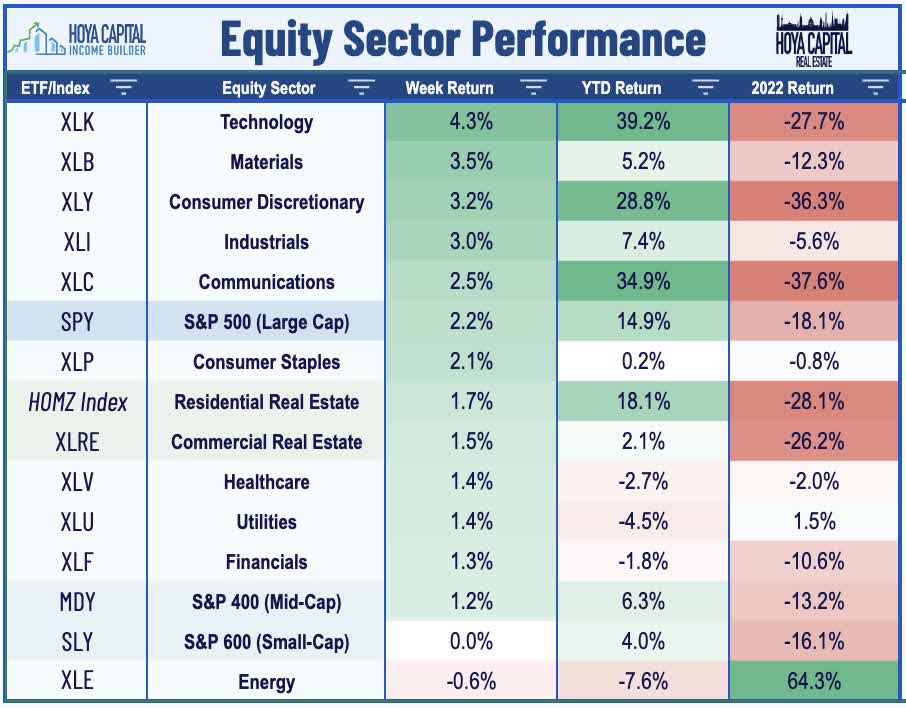

Notching a fifth-straight week of gains for the first time since November 2021, the S&P 500 advanced 2.2% this week, which lifted the major benchmark to levels that are now 23% above the lows of last October. The tech-heavy Nasdaq 100 rallied nearly 4%, significantly outpacing the muted gains from the Mid-Cap 400 and Small-Cap 600. Real estate equities also delivered a relatively strong week, an industry group that is perhaps the most directly impacted by the potential pivot in Fed monetary policy. The Equity REIT Index advanced 1.5% with 16-of-18 property sectors in positive territory, while the Mortgage REIT Index gained another 3.1%. Homebuilders and the broader Housing Index added to their impressive year-to-date gains after strong earnings results from Lennar, which reported a year-over-year increase in new orders despite headwinds from higher mortgage rates.

Hoya Capital

Despite the pause - perhaps temporary - in the Fed's rate hiking cycle, benchmark interest rates returned to their highest levels since the Silicon Valley Bank Collapse in early March, with the 2-Year Yield jumping 12 basis points to 4.72%, while the 10-Year Yield advanced 2 basis points to close at 3.75%. The US Dollar slid to one-month lows after the European Central Bank diverged from the Fed, hiking its lending rate by 25 basis points to the highest level since 2001. The weak dollar supported commodities prices with WTI Crude Oil rebounding about 2% after hitting their lowest levels since late 2021 last week, while Natural Gas futures rallied from two-year lows on renewed supply concerns in Europe. Ten of the eleven GICS equity sectors finished higher on the week, with Technology (XLK) and Materials (XLB) stocks leading on the upside, while Energy (XLE) stocks lagged.

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

Hoya Capital

All eyes were on the Consumer Price Index report this week, which showed a continued moderation in inflationary pressures from the four-decade-high levels seen last summer. Headline CPI inflation moderated to a 4.0% year-over-year rate in May - below consensus estimates of a 4.1% print - as lower energy prices offset upward pressure from housing, used cars, and food prices. The delayed recognition of shelter inflation continues to heavily distort the headline and core metrics, however, resulting in a significant understatement of inflation from mid-2021-2022 and an overstatement of inflation since mid-2022. The metric that we watch most closely - CPI-ex-Shelter Index - declined 0.1% in May and showed an eleventh straight month of cooling in the year-over-year rate to just 2.1% in May. Since July, this CPI ex-Shelter Index has shown an annual inflation rate of just 0.8%. Notably, the housing component CPI explained roughly two-thirds of the annual increase in the index.

Hoya Capital

After the cooler-than-expected Consumer Price Index report, the Producer Price Index data the following day showed an even sharper moderation of price pressures. The headline PPI declined 0.3% in May - the fourth monthly decline in six months - dragging the annual increase to just 1.1%, its lowest reading since December 2020. Sharp declines in energy prices helped to drag goods inflation lower by 1.6% in the month, while services prices - which had been 'stickier' in recent months - slowed to 0.2% in May. Forward-looking sub-series within the PPI report were encouraging as well, with the cost of partly finished goods falling for the tenth time in eleven months while services inflation on partially finished goods has declined in three of the past six months. The two cooler-than-expected reports dragged the Citi Inflation Surprise Index into negative territory for the first time since mid-2020.

Hoya Capital

Equity REIT Week In Review

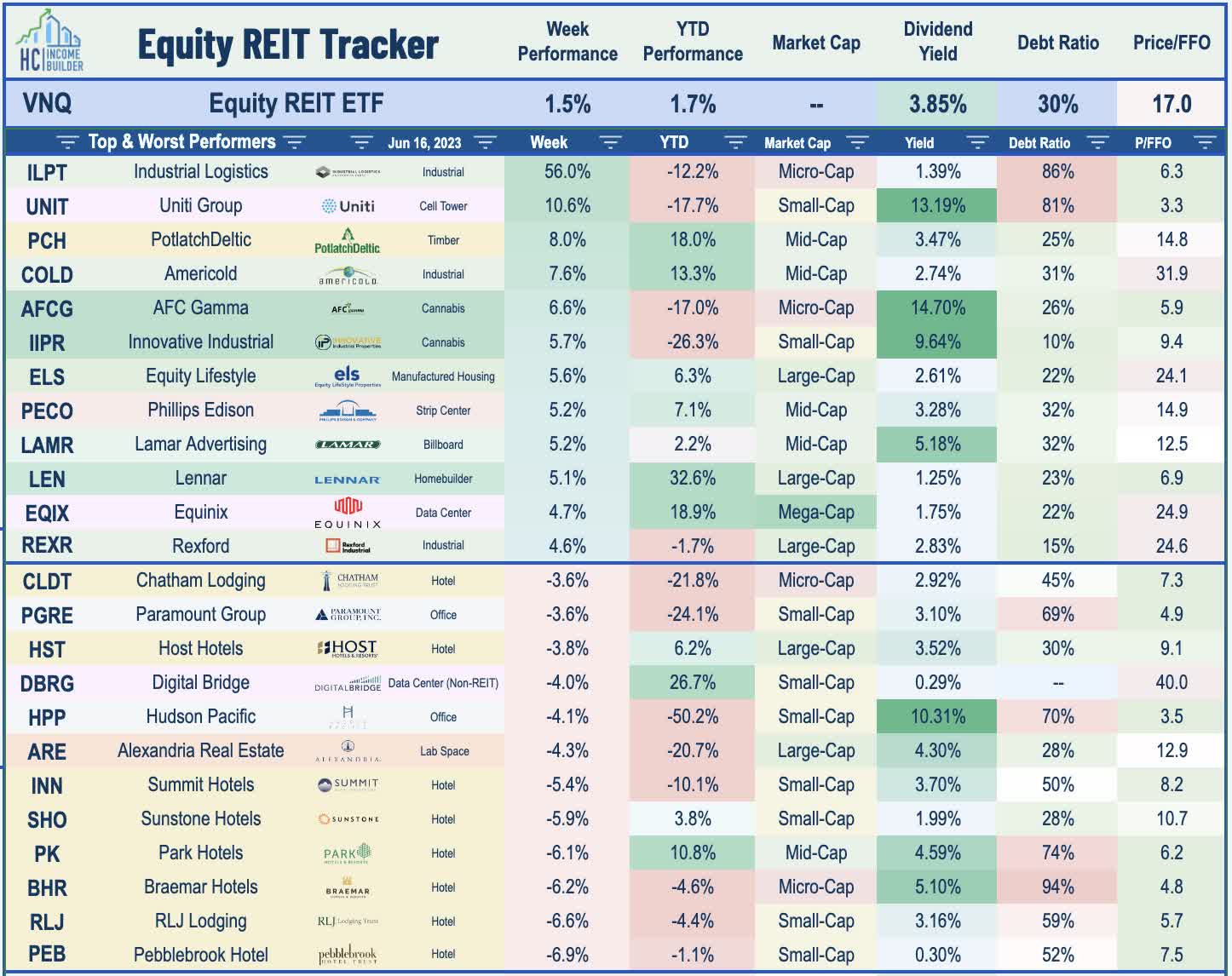

Best & Worst Performance This Week Across the REIT Sector

Hoya Capital

Another week, another wave of REIT dividend increases. Host Hotels (HST) raised its dividend by 15%, the fifth hotel REIT to raise its payout this year. A trio of net lease REITs also announced nominal dividend hikes. Essential Properties (EPRT) raised its quarterly dividend by 2%. Realty Income (O) - the largest net lease REIT - hiked its monthly dividend for the third time this year to levels that are 3% above its dividend declared last June. W. P. Carey (WPC) hiked its quarterly dividend for the second time this year to levels that are 1% higher than a year ago. Small-cap Presidio Property (SQFT) also hiked its quarterly dividend for the second time this year. While dividend increases continue to outpace dividend cuts this year, we've seen the "cut list" begin to creep higher in recent weeks. NYC-focused office REIT Paramount (PGRE) slashed its quarterly dividend by 55%, the eighth office REIT to reduce its dividend this year. Cannabis REIT AFC Gamma (AFCG) reduced its quarterly dividend by 14%. A trio of mortgage REITs - Chimera (CIM), Redwood (RWT), and Cherry Hill (CHMI) also reduced their payouts, as discussed in the mortgage REIT section below.

Hoya Capital

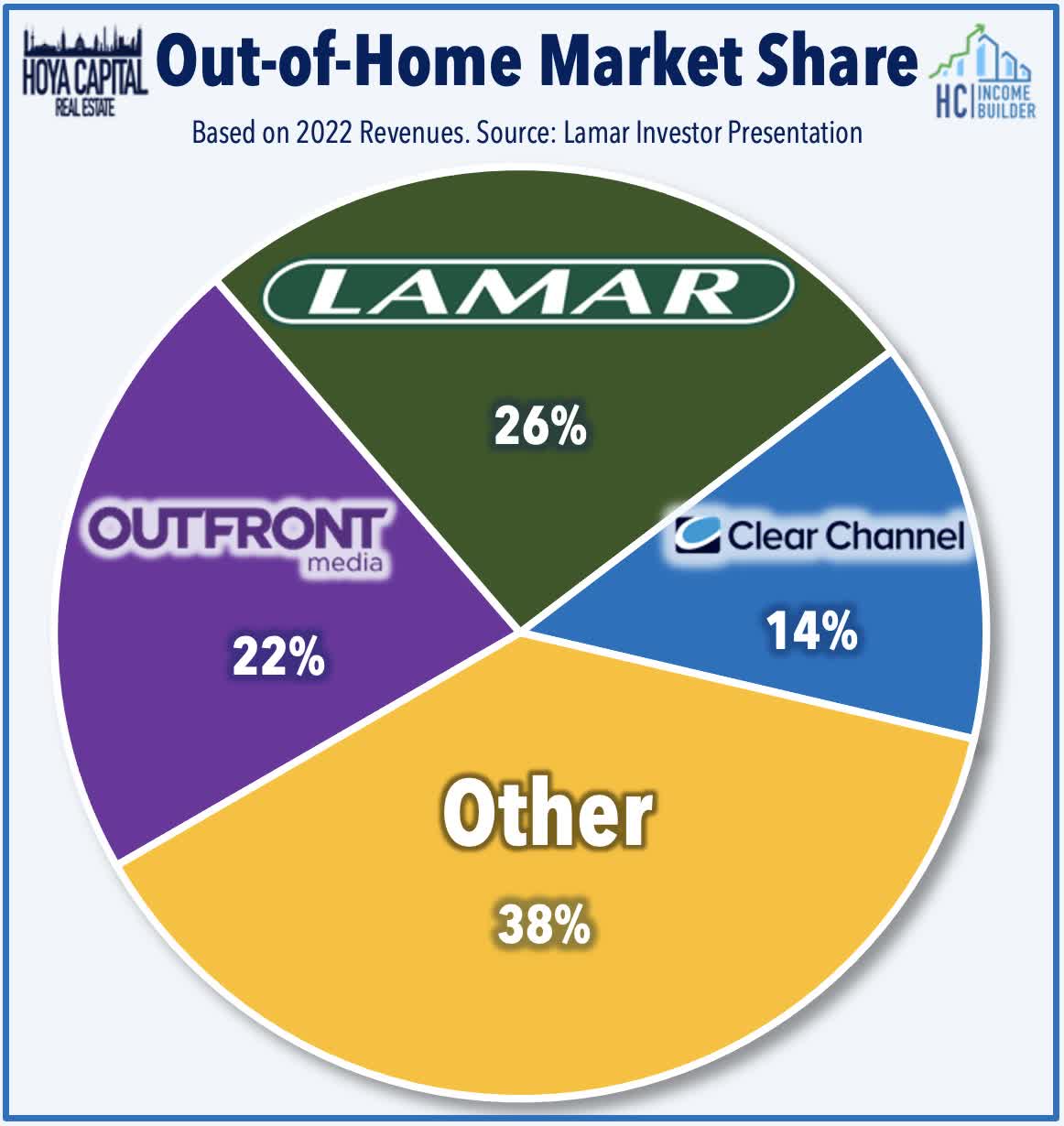

Billboard: Asset manager Blackstone (BX) announced this week that its Tactical Opportunities fund acquired a majority stake in billboard owner New Tradition Media at a transaction that reportedly valued the firm at $500M-$700M. Founded in 2010, New Tradition owns roughly 200 billboards with a focus on digital displays in the Los Angeles and New York markets. The two billboard REITs - Lamar Advertising (LAMR) and Outfront Media (OUT) - which own the lion's share of the nation's 500,000 Out-of-Home ("OOH") ad displays - each rallied nearly 5% on the week. A surprisingly resilient business that has seen revenues and profitability fully recover to pre-pandemic levels after an abrupt decline early in the pandemic. These two billboard REITs have traded roughly flat this year after maintaining their full-year FFO outlook during Q1 earnings season last month. The mass transit segment of the OOH market was hit particularly hard amid a plunge in ridership, and while the traditional billboard segment has now seen a more-than-full recovery to pre-pandemic levels, with spending levels now 15% above 2019-levels, transit spending remains about 30% below pre-pandemic levels.

Hoya Capital

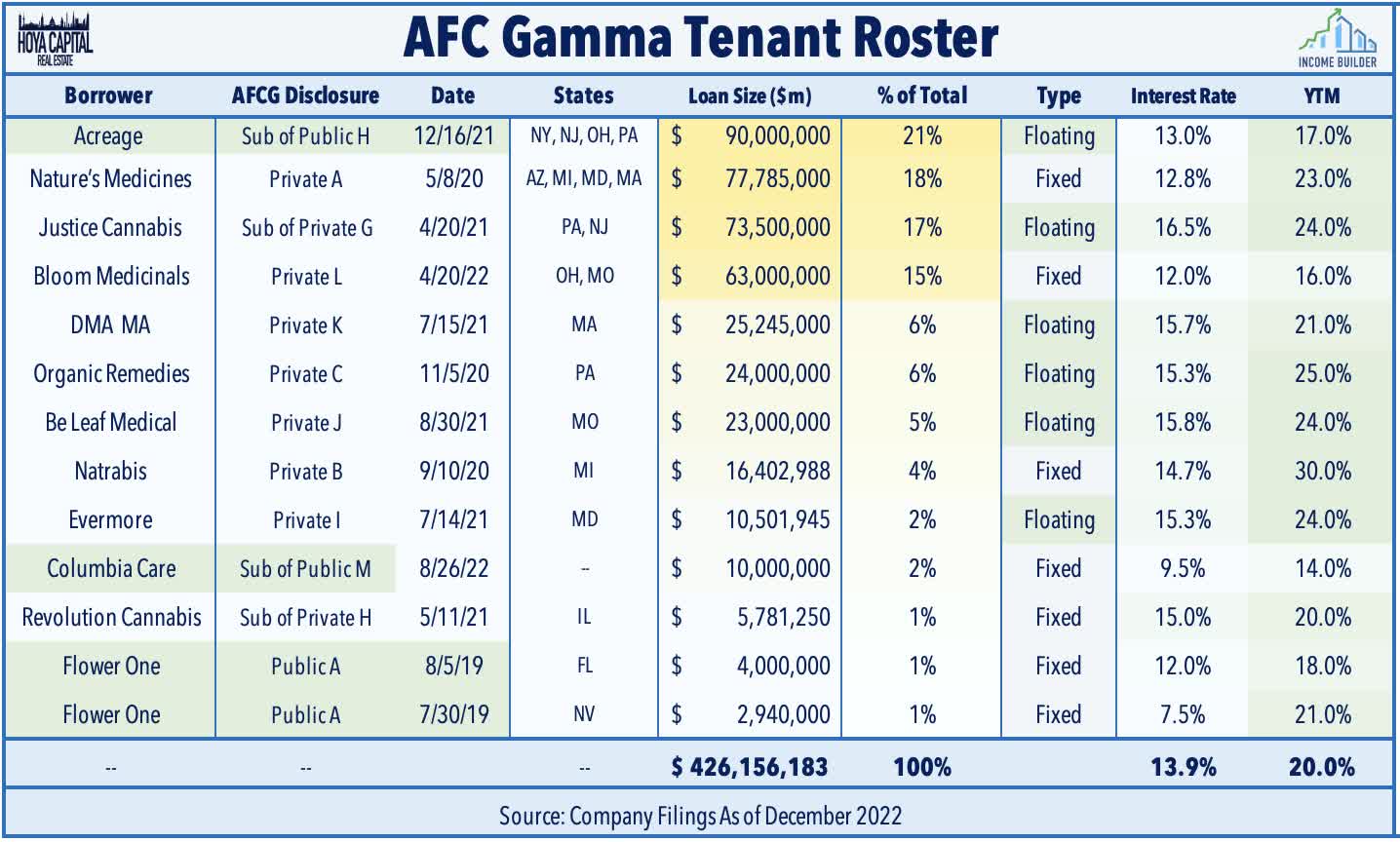

Cannabis: Cannabis-focused mortgage REIT AFC Gamma rallied more than 6% this week after providing a business update alongside a new share buyback program and the aforementioned 14% reduction in its quarterly dividend. AFCG commented that this reduced dividend "represents a sustainable dividend level.... and takes into account recent repayments and cash drag associated with the current liquidity." The company noted that since its last earnings call, Justice Cannabis (Private G) - its third largest tenant - has resumed paying cash interest payments, with AFCG receiving 60% of its June interest payment in cash with a payment plan to receive the rest this month. AFCG also sold two-thirds of the Evermore (Private I) credit facility at par value - which was a 4/5 on its risk scale - to a multi-state cannabis operator. It also received a paydown of $5.9M on its portion of Nature's Medicine (Private A) credit facility from the sale of its Maryland assets, and a repayment of all principal and interest to maturity on its credit facility to Revolution Cannabis (Private H). Elsewhere, Innovative Industrial (IIPR) - the largest cannabis REIT - advanced nearly 6% on the week after it maintained its quarterly dividend at the current level.

Hoya Capital

Proxy battles were also a theme in the REIT sector this week as a pair of controversial pending mergers involving externally-managed REITs have sparked movement from activist investors. Activist firm Blackwells Capital issued a presentation that describes its rationale for supporting the proposed merger of Global Net Lease (GNL) and Necessity Retail (RTL) - which it had previously opposed prior to a settlement with the companies' external advisor, AR Global, which included a $23M payment of stock to Blackwell. The settlement sparked another activist to enter the scene, Orange Capital, who called the settlement “corrupt” and commented that the deal "resembles a greenmail payment." Orange Capital's note stated that “$375 million of value is being transferred to AR Global as compensation” as part of the merger and internalization plan. If approved by shareholders, the merger would create the fifth-largest net lease REIT by asset value. Elsewhere, a pair of firms - DE Shaw and Flat Footed - issued letters outlining opposition to the merger between Diversified Healthcare (DHC) and Office Properties Income (OPI), which are externally managed by RMR Group. Flat Footed's note highlighted the recent trading activity surrounding RMR Group's suite of REITs, the prices of which have surged in recent months amid a battle over control.

Hoya Capital

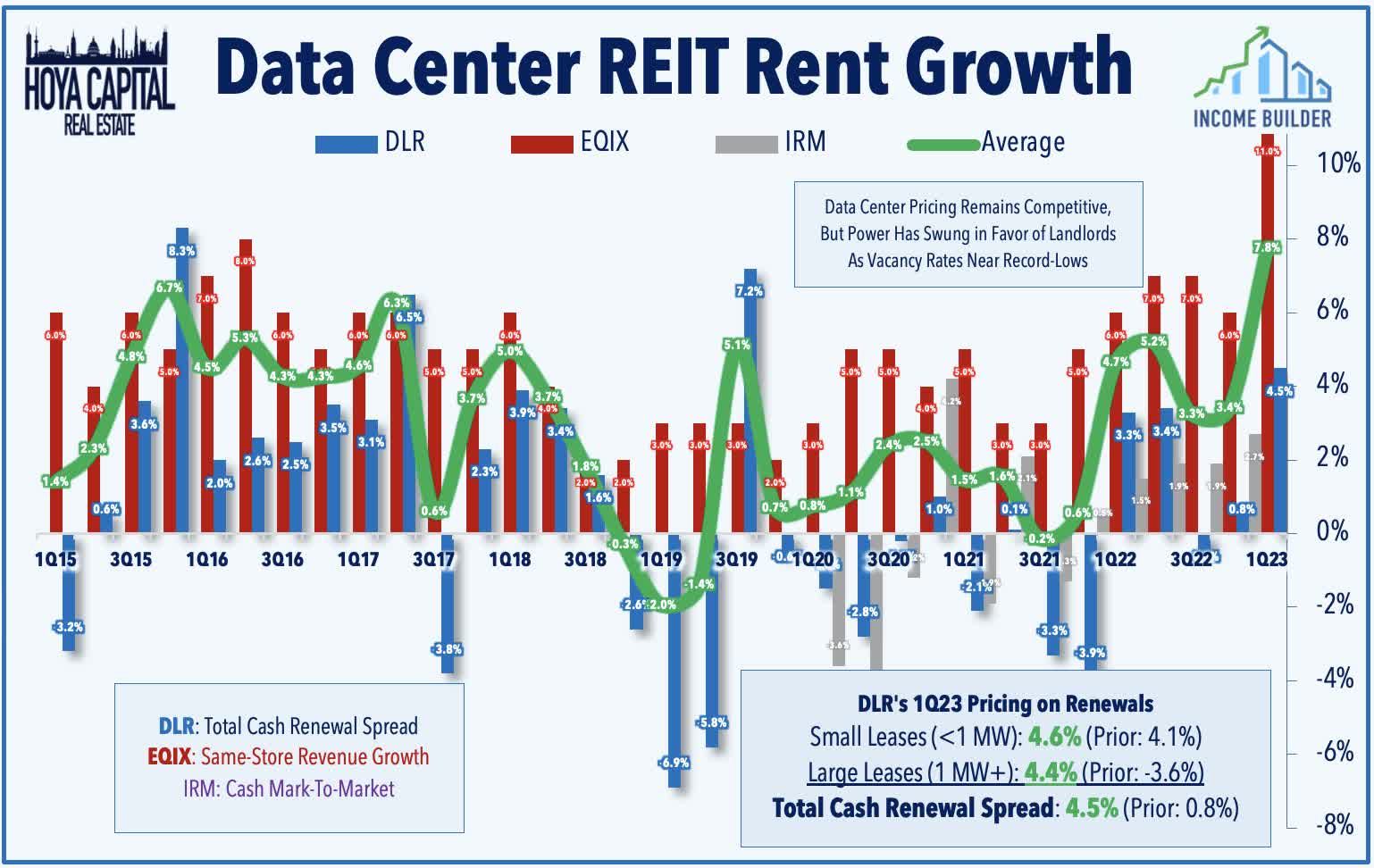

Data Center: Equinix (EQIX) rallied 5% this week after it announced plans to expand deeper into the Asia-Pacific region, announcing that it open its first data center in Kuala Lumpur in Q1 2024. Its second planned data center in Malaysia, EQIX is currently developing a data center in Johor which is also scheduled to begin operations in Q1 2024. Last week, we published Data Center REITs: The Epicenter of AI. Among the top-performing property sectors this year, the Data Center REIT rebound has been augmented by reports of "booming" demand for artificial intelligence ("AI") focused data center chips. Even before the Nvidia report, Data Center REITs were on the upswing in early 2023 after an impressive slate of earnings results showed improved pricing power and record-high occupancy rates. A confluence of development bottlenecks - power shortages, higher cost of capital, supply chain constraints, ecopolitics, and NIMBYism - have created a more favorable dynamic and swung the pendulum of pricing power towards existing property owners.

Hoya Capital

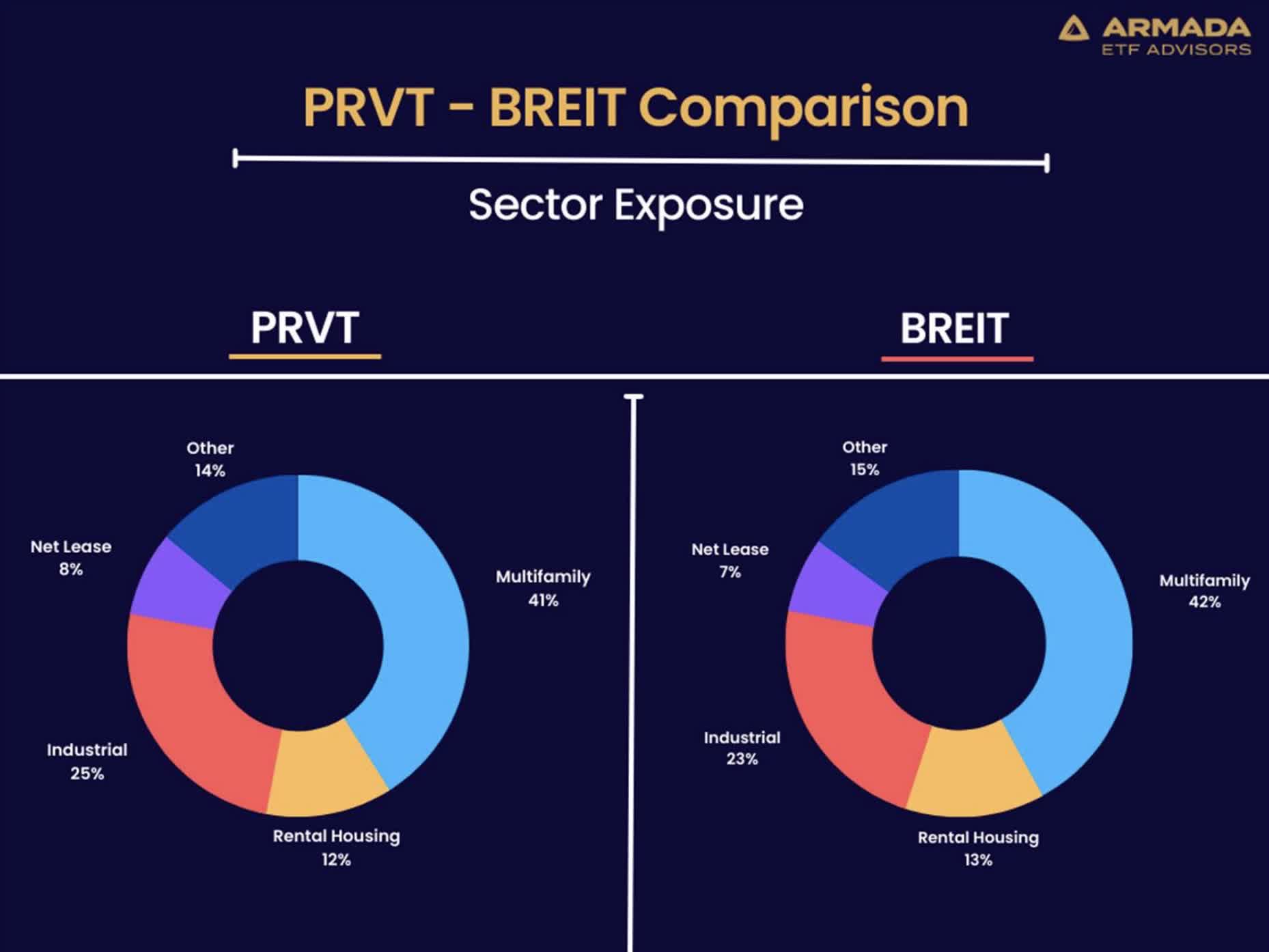

This week, Income Builder contributor Armada Advisors announced the launch of a new real estate ETF - Private Real Estate Strategy ETF - which seeks to "mirror the asset allocation and geographic exposure deployed by the largest private REITs" through a basket of roughly 50 publicly-traded REITs. The fund is seen as a way to play the existing arbitrage opportunity between private and public real estate valuations and as a potential alternative or hedge to Blackstone's (BX) troubled nontraded real estate platform, BREIT, which has limited investor redemptions due to a wave of outflows that exceeded its monthly and quarterly limits since last November. The ETF - which is actively managed - charges a management fee of 59 basis points, which Armada highlights is less than half of the typical private REIT management fee of over 1%. A trio of Sunbelt-focused apartment REITs are the fund's top three holdings: Independence Realty (IRT), Mid-America (MAA), and Camden Property (CPT), followed by industrial REIT Prologis (PLD) and casino REIT VICI Properties (VICI). The industrial and residential property focus positions the fund on the "growth" side of the real estate sector with a computed index dividend yield of 3.64% (3.05% net after expenses).

Hoya Capital

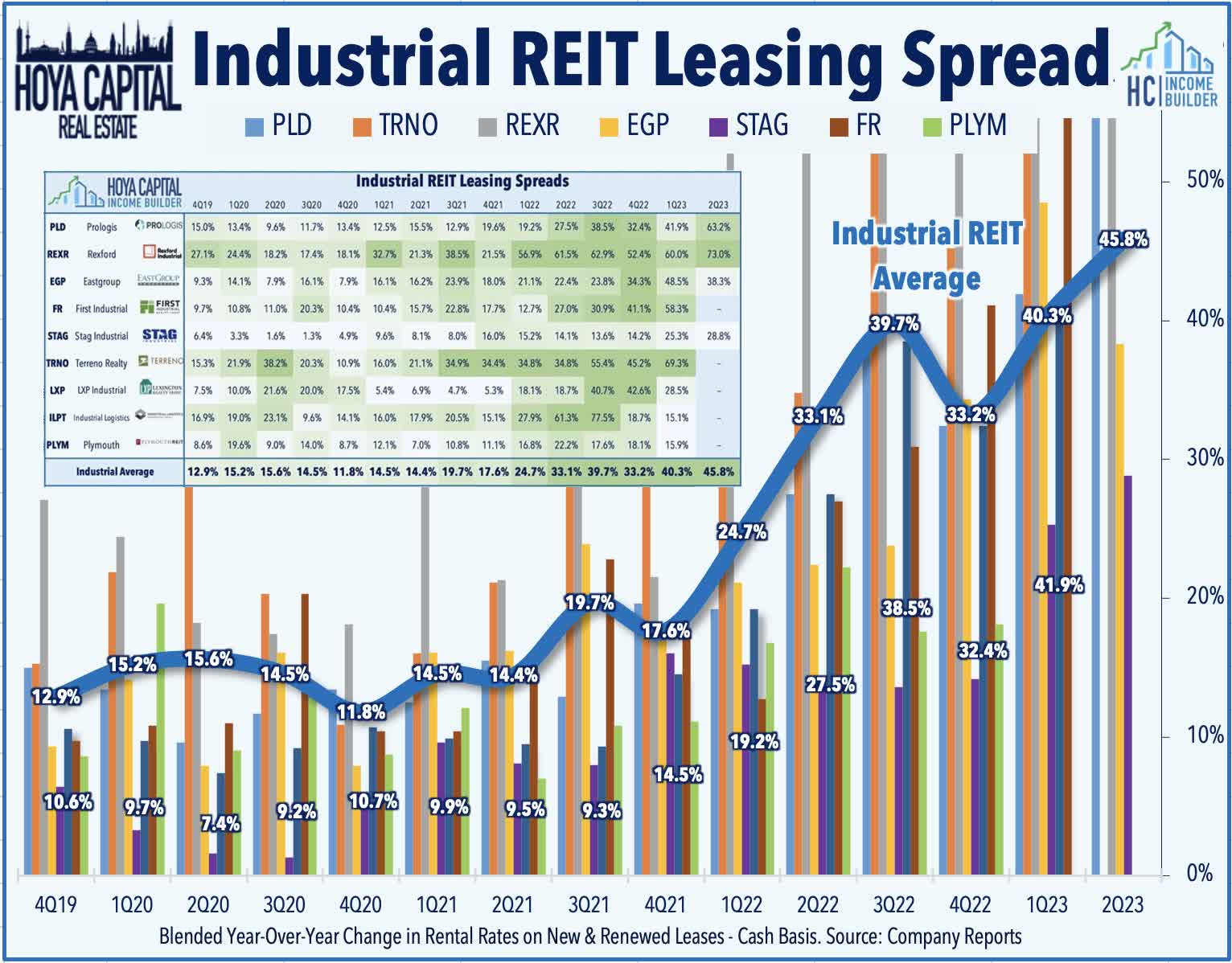

Industrial: On the topic of industrial REITs, Rexford (REXR) - which focuses exclusively on the Southern California logistics market - rallied nearly 5% on the week after it provided a business update showing impressive leasing momentum, pushing back on concerns of industrial demand softness around Los Angeles amid data showing reduced West Coast port traffic and a steep plunge in freight rates from their mid-2022 peaks. REXR reported that comparable rental rates on new and renewal leases increased by 94% compared to prior rents on a net effective basis and by 73% on a cash basis, an acceleration when compared to the first quarter of 2023 and to the full year 2022. The report was consistent with the strong slate of REITweek updates over the past two weeks with industrial REITs tracking to set a new record-high for cash rental rate spreads at nearly 50% in the second quarter.

Hoya Capital

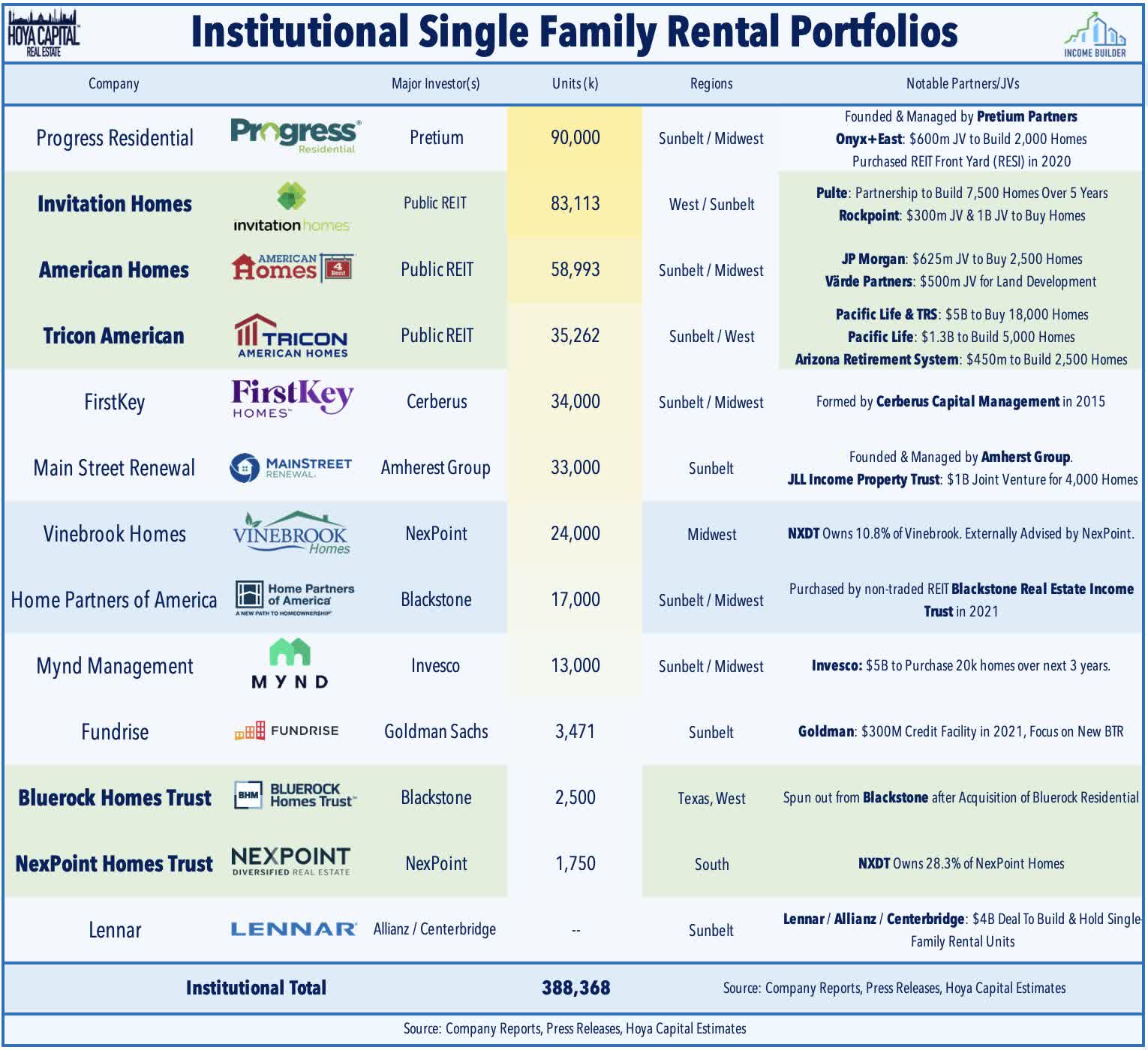

Single-Family Rentals: Speaking of non-traded REITs, Starwood Real Estate Income - the second-largest non-traded REIT behind BREIT and has faced a similar wave of redemption requests - is reportedly seeking to sell a portfolio of roughly 2,000 single-family rental properties that it acquired from Pretium in 2021. SREIT owned 3,210 single-family rental homes valued at roughly $1.26B as of March 31, 2023, the company disclosed in an SEC filing. Single-family rental REITs Invitation Homes (INVH) and American Homes 4 Rent (AMH) have also been "net sellers" this year, but noted in REITweek commentary last week that they would seek to become more aggressive as opportunities in private markets start to emerge. The latest data from Zillow (Z) shows that annual rent growth for the median U.S. market moderated to 4.8% in May - down from the 17.0% peak in early 2022 - but recorded a sequential month-over-month increase for a fifth straight month.

Hoya Capital

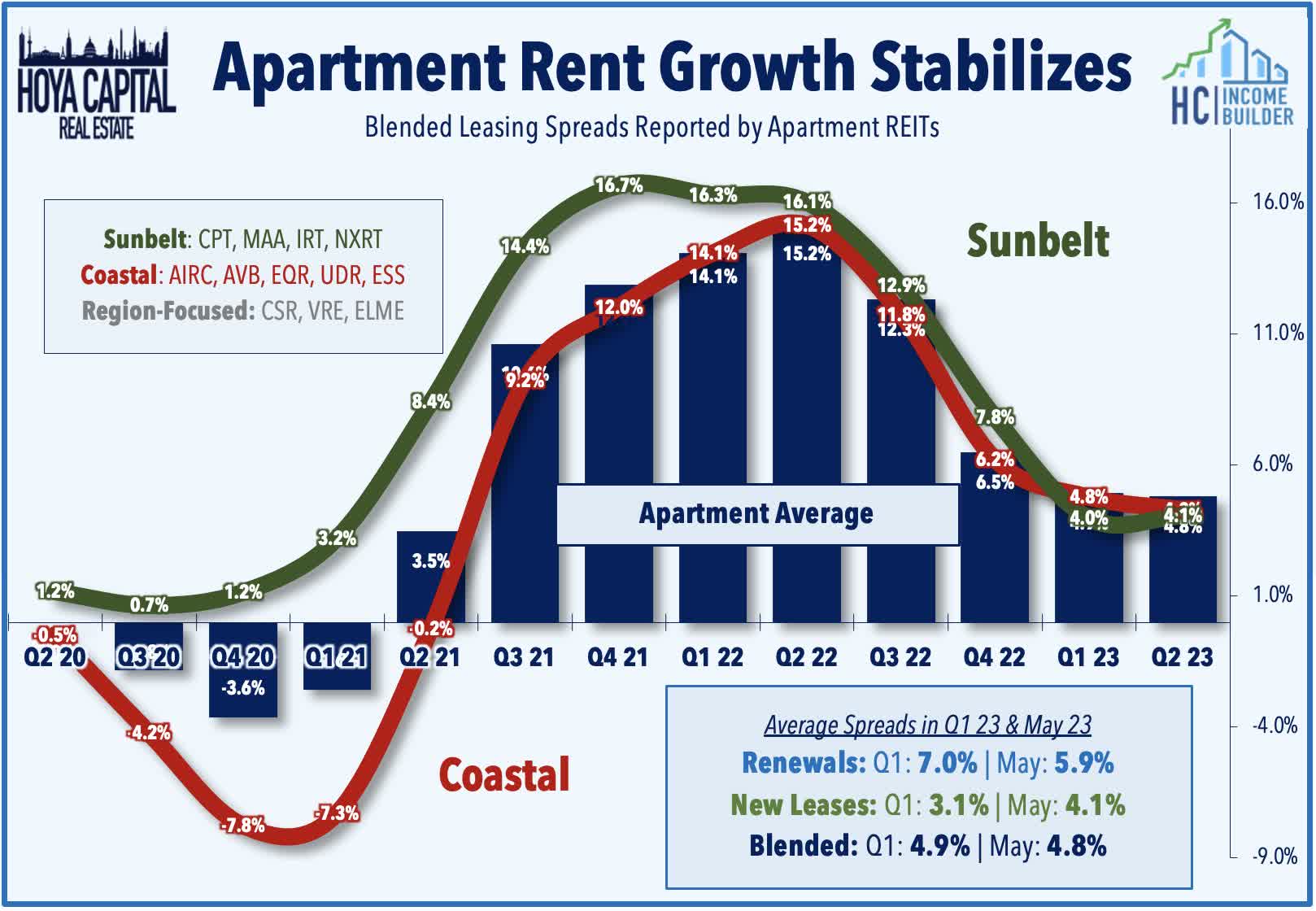

Apartment: On that topic, this week we published Apartment REITs: Rents Are Rising, Again. Left for dead in late 2022 on expectations of a "hard landing" across rental markets, Apartment REITs are the third-best-performing property sector this year, lifted by surprisingly buoyant property-level fundamentals. Recent industry data has shown a reacceleration in rental rate and occupancy trends since bottoming in January, with rent growth appearing to stabilize in its typical "inflation-plus" range between 4-5%. This "inflation-plus" level of rent growth was the norm in the pre-pandemic era as housing demand outpaced new home development. Supply concerns have been the unabating refrain from 'bears' over the past decade of outperformance and while the multifamily pipeline is historically large, overall housing development remains below equilibrium levels while tighter financing conditions have curbed new groundbreaking. While fundamentals remain more favorable on the single-family side - where the lack of supply is perhaps the bigger issue - we're also maintaining our overweight positioning on the multifamily side.

Hoya Capital

Mortgage REIT Week In Review

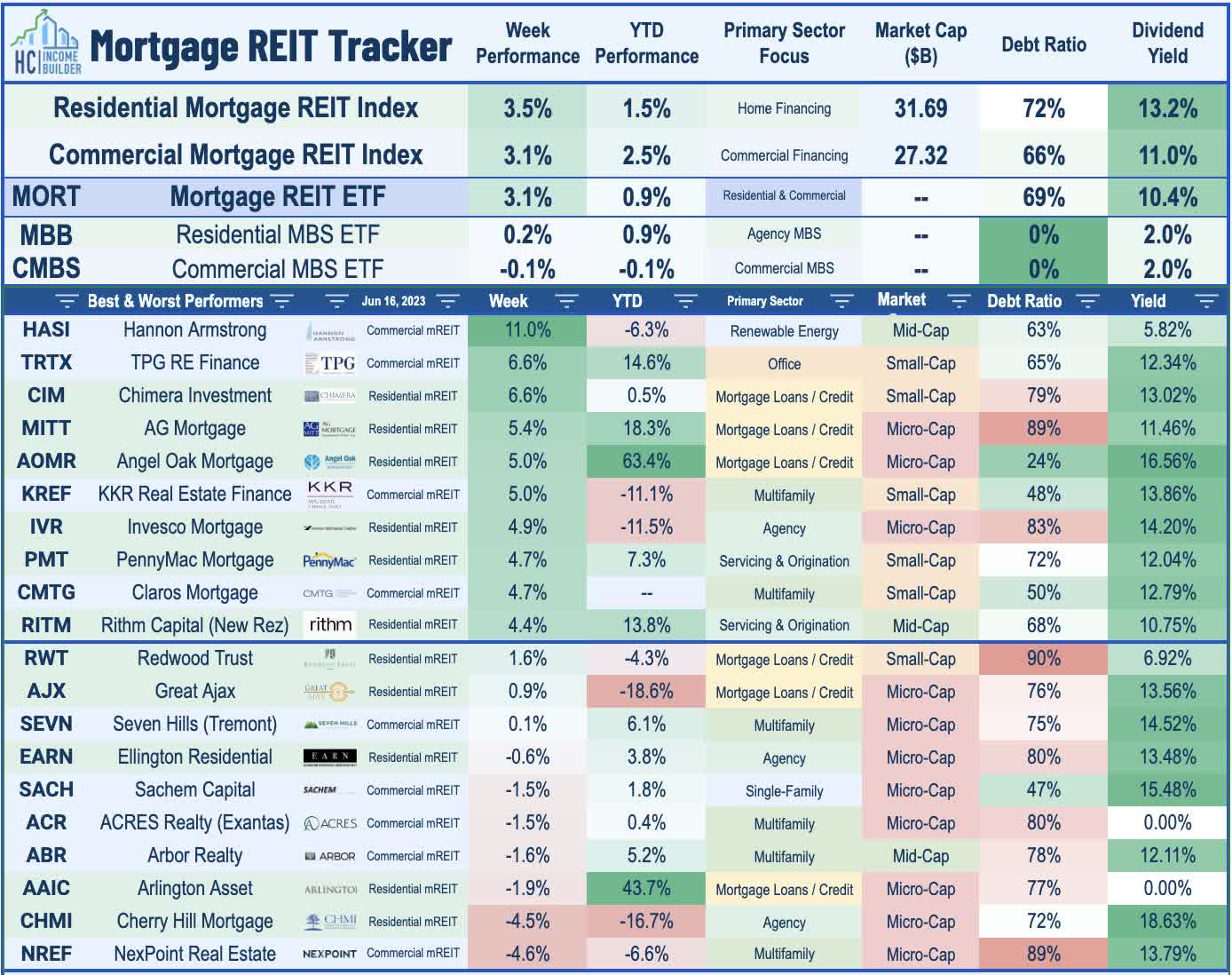

Mortgage REITs continued their post-SVB rebound, with the iShares Mortgage Real Estate Capped ETF (REM) advancing another 3.1% this week to push the benchmark's year-to-date total returns above that of their Equity REIT peers for the first time since February. A trio of residential mREITs trimmed their dividend this week. Chimera (CIM) rallied nearly 7% despite trimming its quarterly dividend by 22% to $0.18/share (13.4% dividend yield), a decrease that was anticipated given its payout ratio and commentary in its first quarter earnings call. Redwood Trust (RWT) advanced 2% despite reducing its dividend by 30% to $0.16/share (9.8% yield), consistent with commentary in late April that it expected to reduce its dividend by "20% to 30%." Cherry Hill Mortgage (CHMI) dipped 5% after it trimmed its dividend by 44% to $0.15/share (11.6% yield), a steeper cut than that implied by commentary last month in which it commented that it would "realign" its dividend to a level "closer to a yield of 13% to 15% of our current book value," which would have implied a quarterly rate of $0.19 based on its Q1 book value.

Hoya Capital

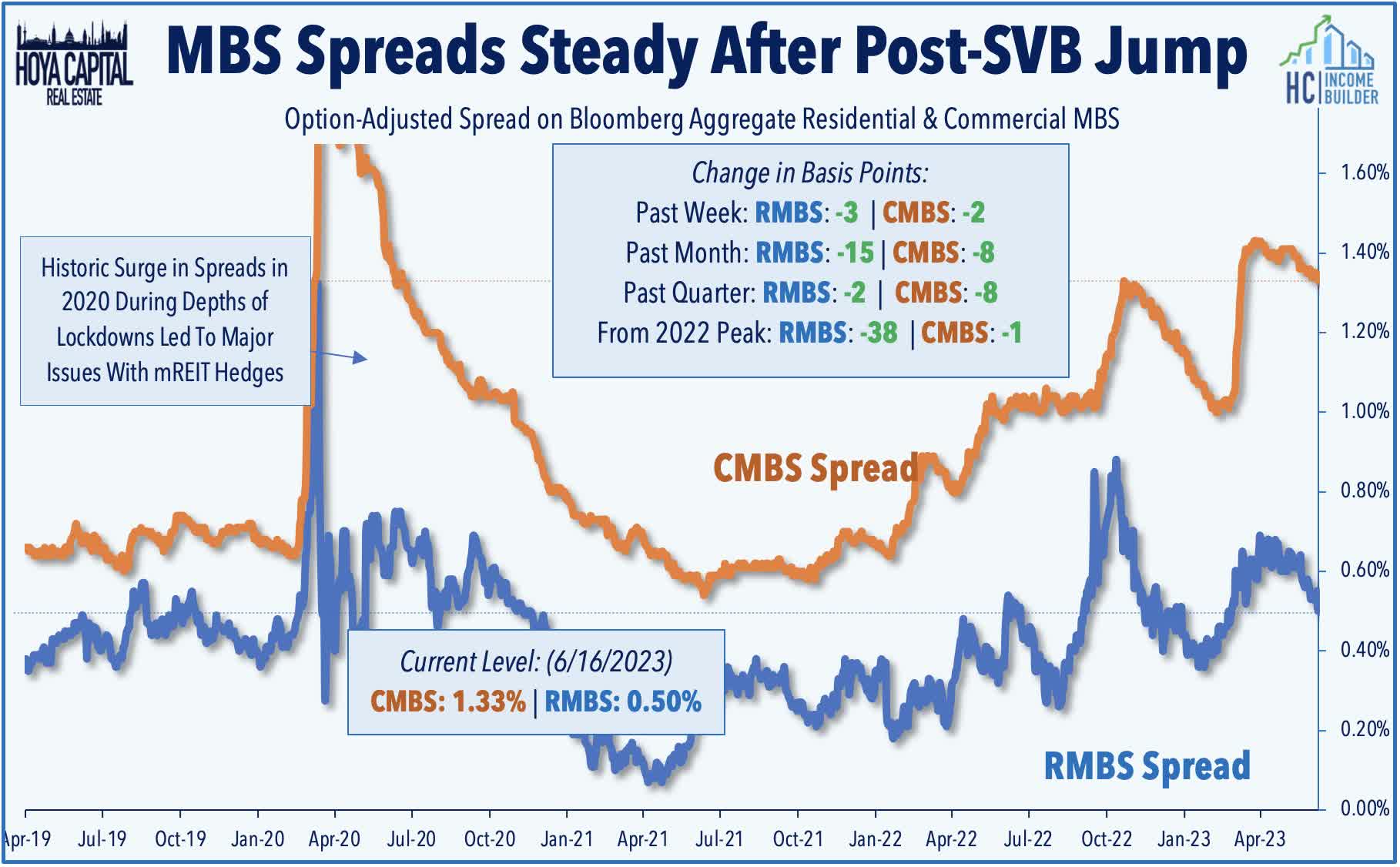

The remaining dozen REITs that declared dividends this week held their payouts steady at current levels. On the residential side, AGNC Investment (AGNC) maintained its payout with a dividend yield of 14.3%, Dynex Capital (DX) maintained its yield of 12.8%, Orchid Island (ORC) at an 18.8% yield, and MFA Financial (MFA) at a 12.2% yield. On the commercial side, Blackstone Mortgage (BXMT) and Starwood Mortgage (STWD) held their payouts steady at yields of 12.4% and 9.9%, respectively. TPG RE Finance (TRTX) maintained its payout with a 12.8% yield, Lument Finance (LFT) at a 12.8% yield, Claros Mortgage (CMTG) at a 12.9% yield, and Apollo Commercial (ARI) at a dividend yield of 12.5%. Spreads on mortgage-backed bonds ("MBS spreads") have both narrowed following the surge in the wake of the Silicon Valley Bank collapse in early March. At 0.50%, Residential MBS spreads have narrowed considerably from their peaks in late 2022 amid concern over housing market distress. Commercial MBS spreads are still relatively elevated at levels that are roughly even with their 2022 highs at 1.33% - up from 1.16% at the start of the year.

Hoya Capital

2023 Performance Recap & 2022 Review

Through twenty-four weeks of 2023, the Equity REIT Index is now higher by 1.2% on a price return basis for the year (+3.1% on a total return basis), while the Mortgage REIT Index is higher by 0.9% (+3.2% on a total return basis). This compares with the 14.9% gain on the S&P 500 and the 6.3% advance for the S&P Mid-Cap 400. Within the real estate sector, 9-of-18 property sectors are in positive territory on the year, led by Single-Family Rental, Data Center REITs, and Apartment REITs, while Office and Cell Tower REITs have lagged on the downside. At 3.77%, the 10-Year Treasury Yield has declined by 11 basis points since the start of the year - up from its 2023 intra-day lows of 3.26% - but still below its late-2022 closing highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 2.2% this year. Crude Oil - perhaps the most important inflation input - is lower by 8% on the year and roughly 40% below its 2022 peak.

Hoya Capital

Economic Calendar In The Week Ahead

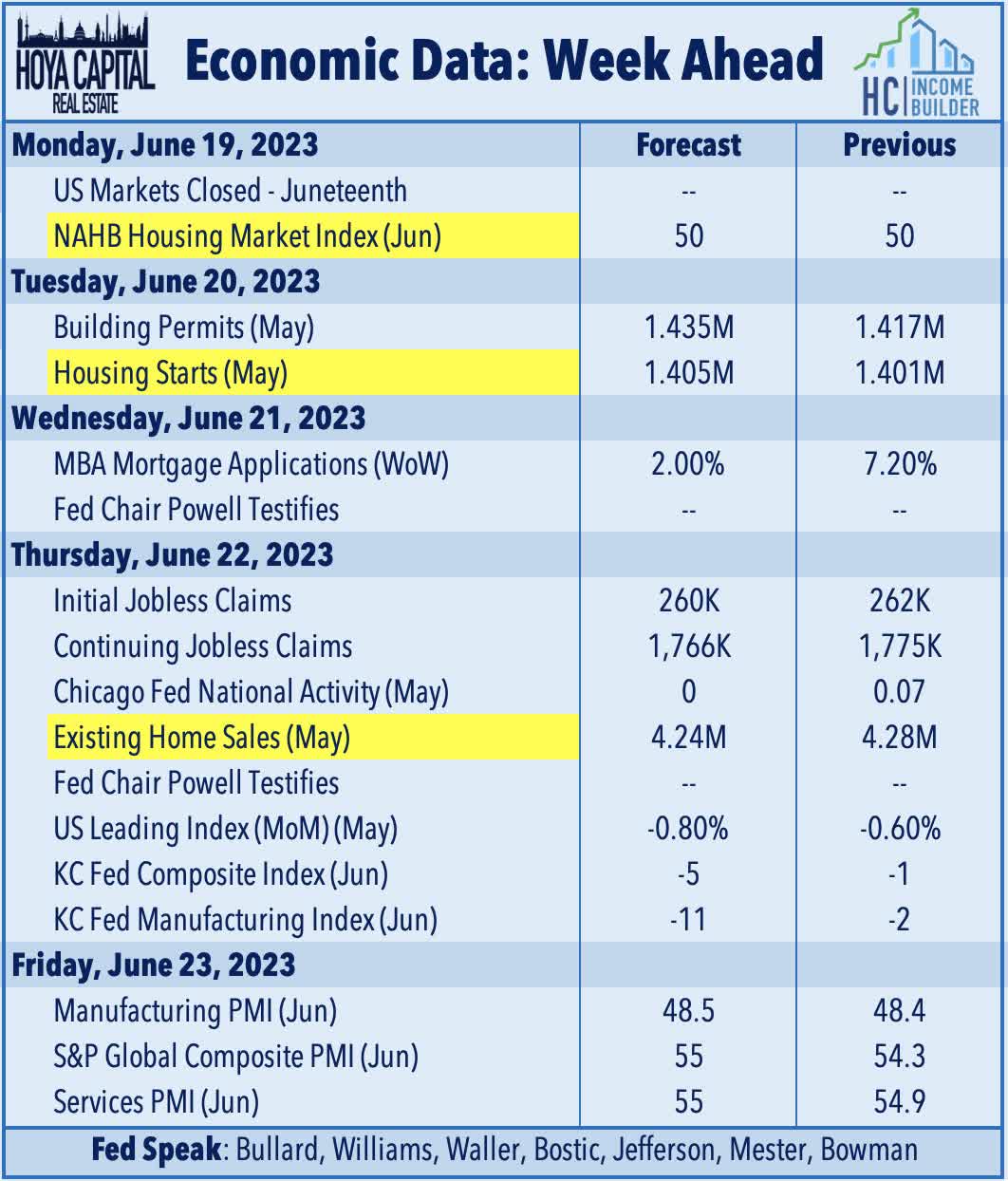

The state of the U.S. housing market will be in focus in the week ahead. Most U.S. equity and bond exchanges will be closed on Monday in observance of Juneteenth. The busy week starts with the NAHB Homebuilder Sentiment data for June, which looks to extend its streak of five-straight monthly increases after dipping to near-15-year lows late last year. On Tuesday, we'll see Housing Starts and Building Permits data for May, which are expected to accelerate slightly after a stronger-than-expected April. Investors will be parsing comments from Federal Reserve Chair Powell during two days of Congressional testimony, beginning with testimony to the House on Wednesday and concluding with the Senate on Thursday. We'll see Existing Home Sales data on Thursday which is expected to decline slightly in May to a 4.28 million seasonally-adjusted annualized rate - up from the lows in January of 4.0 million but well below the 2021 highs of over 6.5 million. We'll also be watching weekly Jobless Claims data on Thursday, and a busy slate of PMI data throughout the week.

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read The Full Report on Hoya Capital Income Builder

Income Builder is the premier income-focused investing service on Seeking Alpha. Our focus is on income-producing asset classes that offer the opportunity for sustainable portfolio income, diversification, and inflation hedging. Get started with a Free Two-Week Trial and take a look at our top ideas across our exclusive income-focused portfolios.

With a focus on REITs, ETFs, Preferreds, and 'Dividend Champions' across asset classes, members gain complete access to our research and our suite of trackers and portfolios targeting premium dividend yields up to 10%.

This article was written by

Real Estate • High Yield • Dividend Growth

Visit www.HoyaCapital.com for more information and important disclosures. Hoya Capital Research is an affiliate of Hoya Capital Real Estate ("Hoya Capital"), a research-focused Registered Investment Advisor headquartered in Rowayton, Connecticut.

Founded with a mission to make real estate more accessible to all investors, Hoya Capital specializes in managing institutional and individual portfolios of publicly traded real estate securities, focused on delivering sustainable income, diversification, and attractive total returns.

Collaborating with ETF Monkey, Retired Investor, Gen Alpha, Alex Mansour, The Sunday Investor, and Philip Eric Jones for Marketplace service - Hoya Capital Income Builder.Hoya Capital Real Estate ("Hoya Capital") is a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations is an affiliate that provides non-advisory services including research and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital has no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of RIET, HOMZ, WPC, LEN, CIM, NXRT, CPT, IRT, MAA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry. This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing. The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized. Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receive compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.