Why REITs Earn Higher Returns Than Private Real Estate

Summary

- REITs outperform private real estate by 2-4% per year on average.

- I present 10 reasons why REITs earn higher returns.

- I think that, especially today, REITs are much better investments than private properties.

- High Yield Landlord members get exclusive access to our real-world portfolio. See all our investments here »

Feverpitched

Investors are often surprised to hear that real estate investment trusts, or REITs, have historically been more rewarding investments than private real estate.

After all, aren't you supposed to be rewarded for taking higher risks?

Private rental properties are illiquid, concentrated, and management-intensive investments, whereas REITs are liquid, diversified, and management-free.

You would expect the former to earn higher returns to compensate for higher risk and effort, but numerous studies prove otherwise.

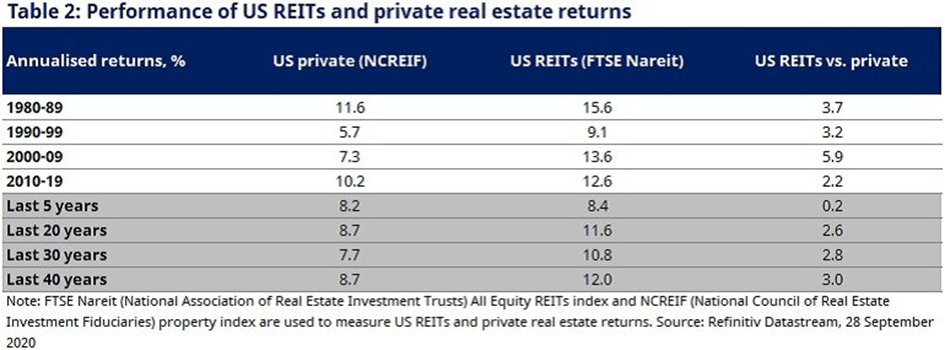

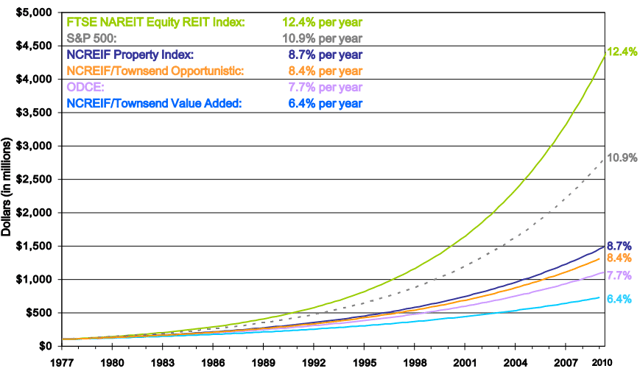

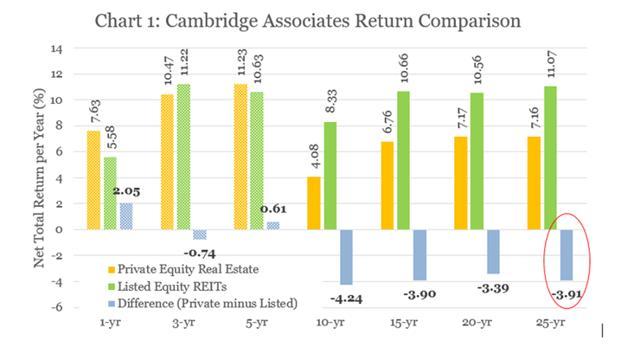

REITs outperform private real estate by 2-4% per year on average, depending on the study that you look at:

NAREIT EPRA Cambridge

How could this be?

Well, there is a good explanation, but for you to understand it, you will need to give me 10 minutes of your time. There are about 10 reasons why REITs earn higher returns, and I highlight all of them below. I also correct important misconceptions in the process, so make sure to read till the end if you are interested in this topic:

Reason #1: Better Access to Capital

A common misconception that I hear from real estate investors is that rental properties are better investments than REITs because they can use leverage to boost their returns.

What they misunderstand is that REITs are also leveraged investments. When you buy shares of a REIT, you are providing the equity, and the REIT then adds debt on top of it to boost returns.

It is no different.

But it is even better in the case of REITs, because they can access many more capital sources, and generally they will also get better terms than you could. Banks and other capital providers prefer to work with REITs because they are large public companies that are well-diversified, professionally managed, SEC-regulated, and highly scrutinized by countless analysts.

By simply getting better terms on their financing and accessing many more capital sources (preferred equity, convertible bonds, etc.), they get to earn higher risk-adjusted returns over time.

Consider that Agree Realty (ADC) was able to issue some perpetual preferred equity at a 4.25% yield back in 2021 to boost the returns of its common equity. A private investor would have been happy if it could access preferred equity at a 2x higher rate.

Reason #2: Highly Efficient Management

Another common misconception that I hear is that REITs generate lower returns because they pay high salaries to their managers.

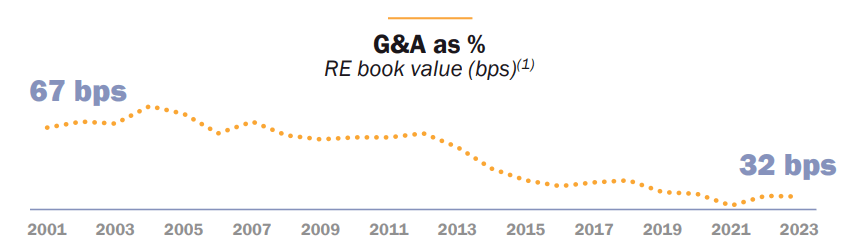

In reality, it is the opposite. The management cost of REITs is far lower than the management of private properties.

REIT can afford to hire the best talent and pay them millions in some cases because they enjoy significant economies of scale. To give you an example: Realty Income (O) pays millions to its top executive, but its management cost is just 0.3% of total assets each year because they own $10s of billion worth of real estate. That's a very low management cost:

Realty Income

In comparison, the management of private property is highly inefficient and expensive if you properly account for all expenses.

If you do it yourself, then you need to account for the value of your time, because you could use your time to earn a salary doing something else.

Assuming that you spend just 3 hours per week on the property on average, and you value your time at $30 per hour, that's $360 per month. If the property's NOI is $1,000 per month, that's over a third of it wasted on management expenses. And before you tell me that "oh, 3 hours is too much, I do nothing most weeks," I hear you, but this is an average. Some weeks, you will spend 10s of hours working on a property. This is perhaps the main reason why private real estate investors routinely overestimate their returns. They forget to account for their own management cost, which eats into their returns.

Alternatively, you could outsource the management to a property manager, but again, the cost is way higher because you don't enjoy the same scale, and besides, here you would also introduce significant conflicts of interest since property managers typically earn a percentage of revenue, which pushes them to grow as much as possible. Internally-managed REITs enjoy better alignment of interest because the salaries of executives are heavily dependent on the returns of shareholders.

Reason #3: Enormous Economies of Scale On Other Fronts

But REITs don't save money, just on the management cost.

The savings also apply elsewhere.

Just imagine Mid-America Apartment (MAA) having a deal with a contractor to change 100 carpets in a specific region each year. It will get a much better rate than you would for changing a single or a few carpets with the same contractor.

The same applies to all costs: brokerage, property management, renovations, constructions, banking, legal, admin, etc. Real estate is a low-margin business, and scale makes a big difference.

Reason #4: Ability to Develop Properties

REITs are not just buying stabilized properties to earn rental income, which is what most private real estate investors are doing.

REITs will commonly buy land and go through the entire process of developing a new property to earn superior returns.

To give you an example: AvalonBay (AVB) will commonly build its own apartment communities, earning a ~7% stabilized yield, which is far higher than the ~4.5% cap rate that it would need to pay if it bought a comparable property.

Reason #5: Ability to Earn Additional Profits from Other Real Estate Related Businesses

REITs are also able to benefit from their scale to launch additional businesses to earn extra profits.

- Armada Hoffler (AHH) has a construction arm, and it offers construction services to other investors in exchange for a fee. Shareholders share these profits.

- Farmland Partners (FPI) has a brokerage and auctioning business to earn extra profits.

- SL Green (SLG) is now developing an asset management business.

- Etc.

Private landlords don't earn such extra profits, and so naturally their returns will be lower.

Reason #6: Ability to Do Spread Investing

This point is tied to reason #1.

REITs enjoy better access to capital because they are publicly listed companies.

This allows them to grow faster by raising additional capital to buy additional properties when their cost of capital is below their expected returns, resulting in a positive spread.

Example: Realty Income has historically traded at a small premium to its NAV during most times, and this has allowed it to raise equity, which combined with debt, had a blended cost of around 4-5%. It would then use this capital to buy net lease properties at a 6-7% cap rate - pocketing the spread.

Its share count would go up, but because these investments are accretive, the cash flow per share would also rise.

This is how Realty Income has managed to grow its cash flow per share by 5% annually, even as its rent hikes were just 1% per year.

Private investors cannot keep up with this growth because they can't do spread investing on the same scale.

Reason #7: Ability to Pursue Sale & Leaseback Transactions

REITs will also skip brokers and make deals directly with property owners in sale and leaseback transactions.

As an example, VICI Properties (VICI) is able to buy properties from casino operators like Caesars (CZR) and MGM (MGM) and structure its own leases with them. This has many advantages:

- Lower transaction cost

- Less competitive buying process

- Likely better cap rate

- Better lease terms

- Value creation by originating an off-market deal.

A private investor wouldn't be able to pursue such deals because of their lack of scale.

Reason #8: REITs Can Afford to Hire the Best Talent

I mentioned this already in section #2, but I want to add that REITs not only have lower management costs, but they also have better management.

Real estate is a management-heavy business, and a simple explanation for the outperformance of REITs is that they can afford to hire the best talent. Better talent will find ways to optimize risk-adjusted returns.

Reason #9: REITs Enjoy Better Bargaining Power With Tenants

The scale of REITs also gives them another important advantage.

They are less dependent on a specific tenant, and it gives them better bargaining power.

REITs own large and diversified portfolios. They have lots of tenant relationships. And they even have their own leasing teams in most cases.

As such, they don't fear a vacancy nearly as much as private investors would. This allows them to be more aggressive with rent hikes and other lease terms.

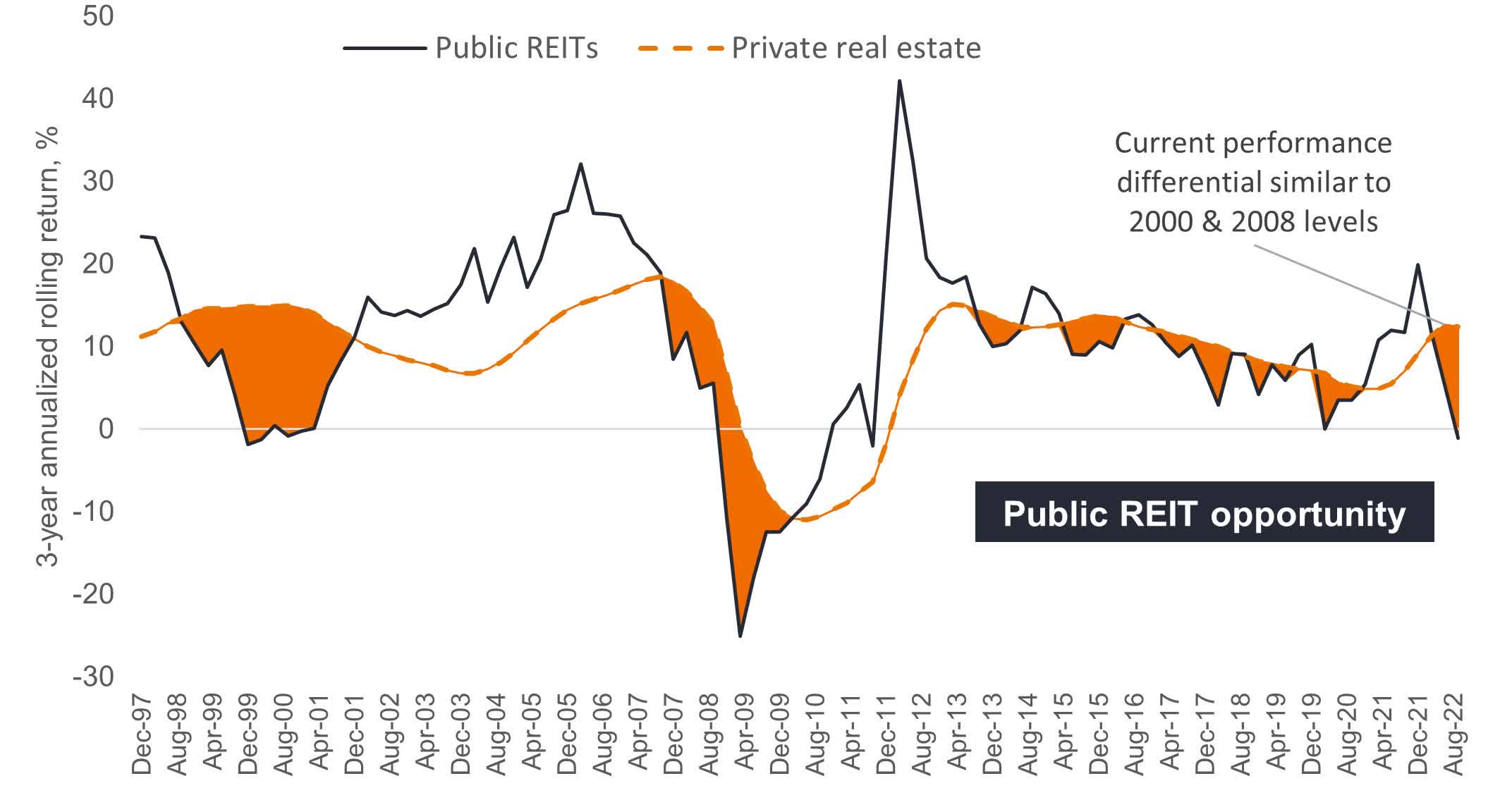

Reason #10: Today, REITs are Hugely Discounted

This is perhaps the most important reason today.

Over the past year, REIT share prices have crashed even as their cash flows kept on rising and property values remained resilient for the most part. As a result, they are now priced at historically low valuations with large discounts to NAV.

According to Janus and Henderson, REITs traded at a 28% discount to NAV on average in late 2022 and valuations have dropped further since then:

Janus Henderson

This essentially means that you get to buy real estate at a discount to fair value through the REIT market, and you then still get all the benefits that we discussed earlier.

A lower price means a higher yield and greater upside potential in a future recovery.

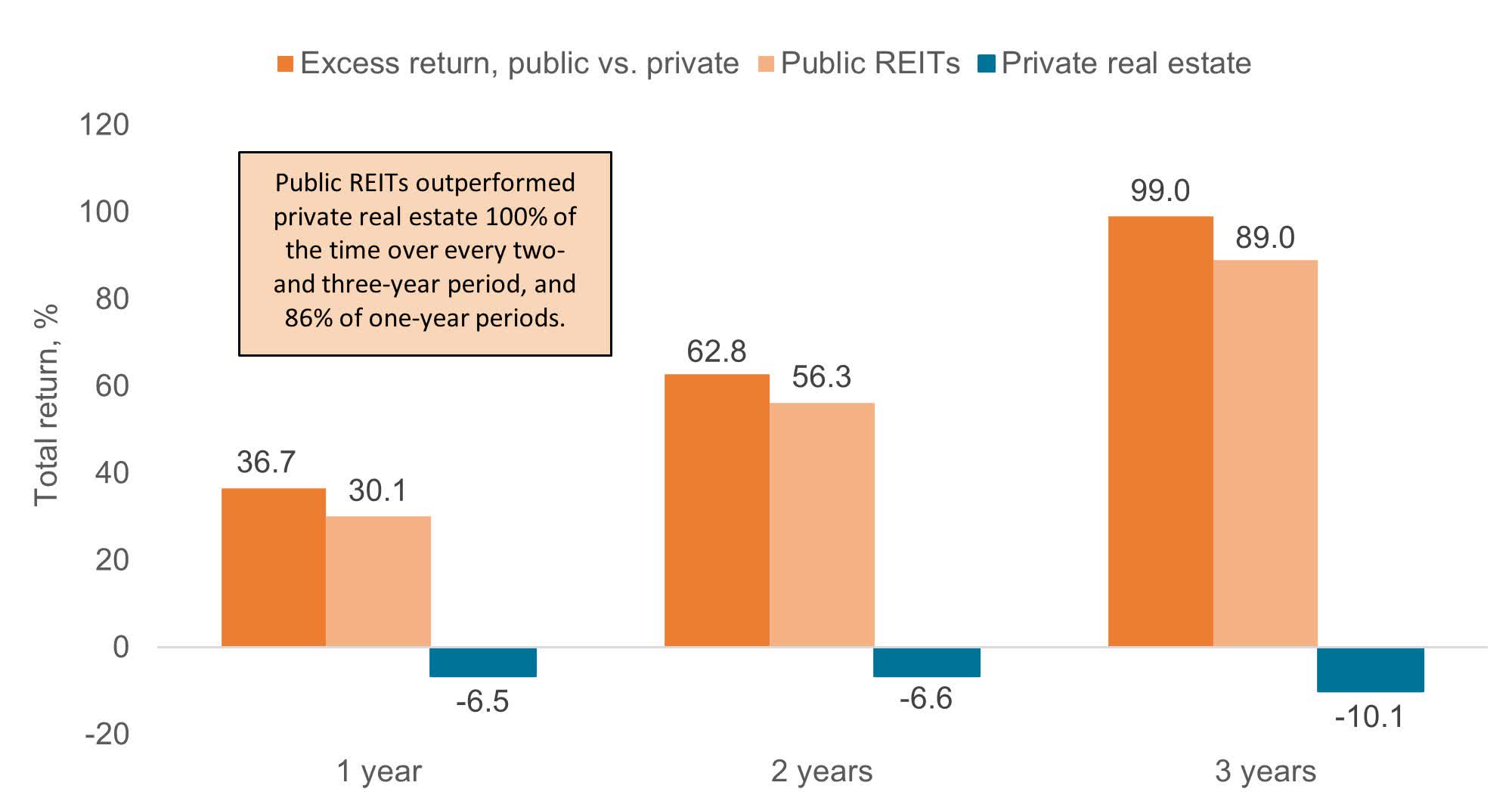

For this reason, REITs have historically been exceptionally rewarding following a correction:

Janus Henderson

Bottom Line

I come from a private equity real estate background, but I am buying REITs instead of private real estate because of the reasons that I outlined in this article.

I believe that they offer better risk-and-hassle-adjusted returns during most times, and this is especially true today, with most REITs trading at large discounts to their fair value.

If you want full access to our Portfolio and all our current Top Picks, feel free to join us at High Yield Landlord for a 2-week free trial

We are the largest and best-rated real estate investor community on Seeking Alpha with 2,500+ members on board and a perfect 5/5 rating from 500+ reviews:

You won't be charged a penny during the free trial, so you have nothing to lose and everything to gain.

Start Your 2-Week Free Trial Today!

This article was written by

Jussi Askola is a former private equity real estate investor with experience working for a +$250 million investment firm in Dallas, Texas; and performing property acquisition in Germany. Today, he is the author of "High Yield Landlord” - the #1 ranked real estate service on Seeking Alpha. Join us for a 2-week free trial and get access to all my highest conviction investment ideas. Click here to learn more!

Jussi is also the President of Leonberg Capital - a value-oriented investment boutique specializing in mispriced real estate securities often trading at high discounts to NAV and excessive yields. In addition to having passed all CFA exams, Jussi holds a BSc in Real Estate Finance from University Nürtingen-Geislingen (Germany) and a BSc in Property Management from University of South Wales (UK). He has authored award-winning academic papers on REIT investing, been featured on numerous financial media outlets, has over 50,000 followers on SeekingAlpha, and built relationships with many top REIT executives.

DISCLAIMER: Jussi Askola is not a Registered Investment Advisor or Financial Planner. The information in his articles and his comments on SeekingAlpha.com or elsewhere is provided for information purposes only. Do your own research or seek the advice of a qualified professional. You are responsible for your own investment decisions. High Yield Landlord is managed by Leonberg Capital.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AVB; O; VICI; ADC; AHH; FPI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.