Wintrust Financial Corporation: A Sturdy Bank That Continues To Grow Nicely

Summary

- Wintrust Financial Corporation continues to grow its top and bottom lines at a nice clip.

- The firm also stood up well earlier this year during the banking crisis, with deposits remaining quite sturdy.

- All things factored in, the company looks like a good prospect for investors to take very seriously.

- Looking for a helping hand in the market? Members of Crude Value Insights get exclusive ideas and guidance to navigate any climate. Learn More »

Fly View Productions

Like pretty much every bank out there, Wintrust Financial Corporation (NASDAQ:WTFC) experienced a great deal of downside after significant concerns developed regarding the financial stability of the banking sector earlier this year. Although shares have shown signs of recovery, they are still down 21.5% compared to what they were trading at on February 28th. Based on what data has been provided by management since then, I would make the case that the company deserves to move higher. Even though the business lacks the appropriate amount of liquidity to cover all of its uninsured deposits, it has only experienced a marginal decline in the value of its deposits during the first quarter of the year. Add on top of this a history of attractive revenue and profit growth, and the company makes for a compelling opportunity in my opinion.

An introduction to Wintrust Financial

The operations that comprise Wintrust Financial Corporation. Through its locations, which are largely centered around the Chicago metropolitan area, southern Wisconsin, and Northwest Indiana, the company provides customers with a wide variety of services. Its primary focus is on community banking operations. These activities service customers ranging from individuals, to small and medium-sized businesses, to local government units and institutional clients, and more. In addition to account services like checking and savings accounts, the company provides customers with loan opportunities. It's even engaged in the retail origination and purchase of residential mortgages, and it provides a variety of other lending products through several of its locations. One example is its Barrington Bank’s Community Advantage program, which offers customers lending, deposit, and treasury management services to condominium, homeowner, and community associations. Another is the Hinsdale Bank’s mortgage warehouse lending program that provides loans and deposit services to mortgage brokerage companies that are largely located near where the company is.

Outside of the community banking category, the company also provides specialty finance services. These include the financing of insurance premiums for both businesses and individuals, as well as accounts receivable financing, outsourced administrative services, and more. Its wealth management business provides a wide variety of wealth management services such as private client and securities brokerage services to customers largely located in the Midwest. It provides trust and investment management services to clients in downtown Chicago and at some of its other locations. Great Lakes Advisors, the company’s RIA, offers customers money management and advisory services. And it also has the ability to offer tax deferred services to its commercial real estate customers.

One of the most interesting aspects of the company is that it has a special offering called MaxSafe. This is a product that it provides its customers that grants them the opportunity to receive $3.75 million in FDIC insurance per person. It's likely because of this that the company's deposit base remained as high as it currently is. During the most recent quarter, for instance, deposits covered under this particular offering grew by $1.1 billion. But given that the average customer deposit on the company's books is less than $70,000, this only meets the needs of a small number of its clients. For everyone else, it's overkill.

Wintrust Financial

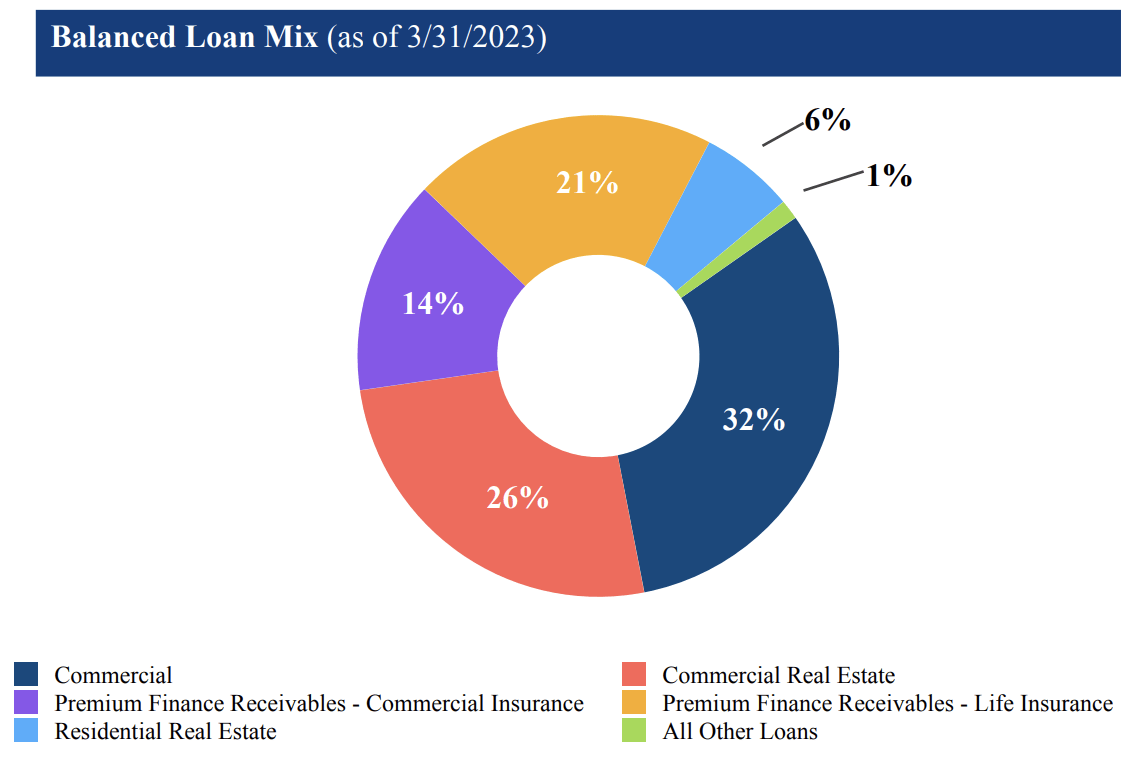

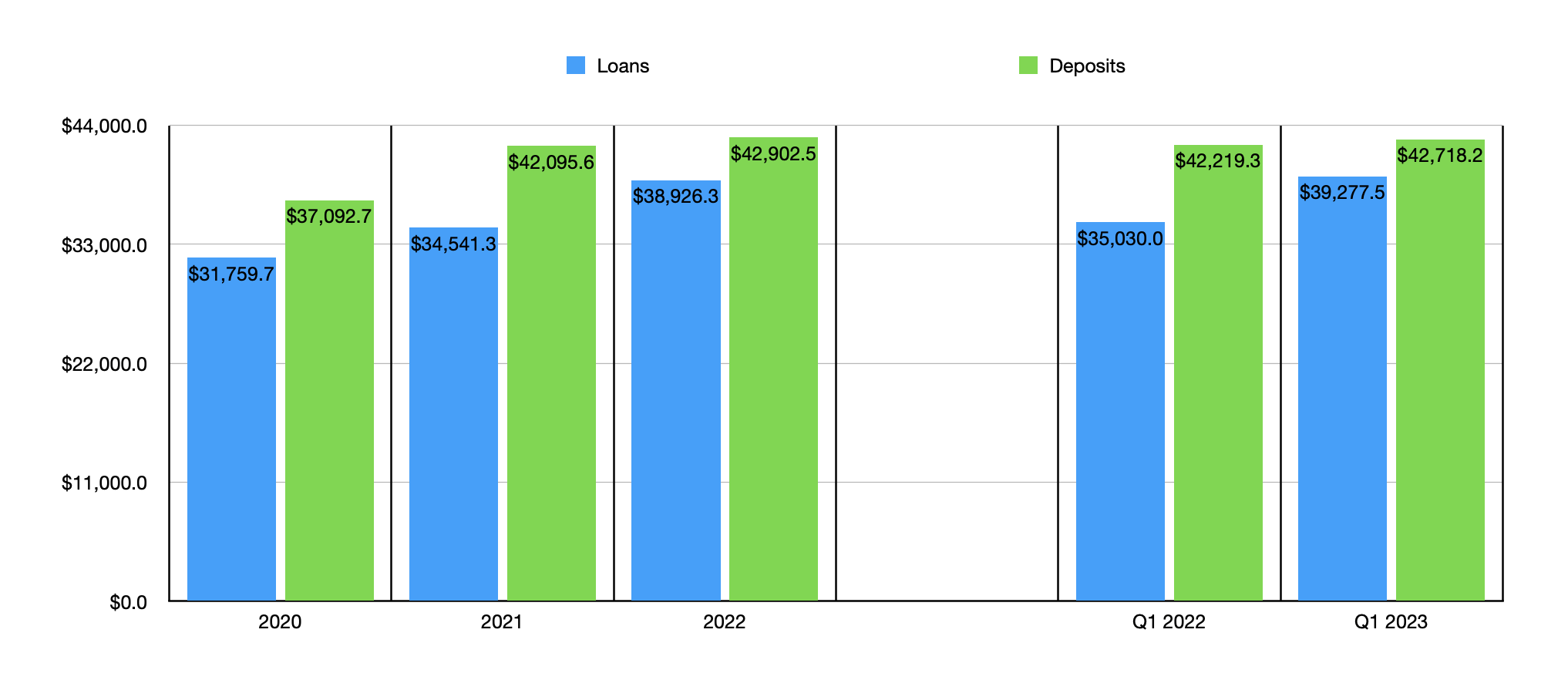

During the most recent quarter, Wintrust Financial Corporation demonstrated a great deal of stability. Total deposits for the company came in at $39.3 billion. That's up from the $35 billion reported one year earlier, and it stacks up nicely against the $38.9 billion that the company reported at the end of 2022. Loans have typically increased over the past few years. Back in 2020, for instance, net loans on its books came in at a more modest $31.8 billion. Of its current loan portfolio, 32% by value is in the form of commercial loans, while 26% falls under the category of commercial real estate. Only 14% of its commercial real estate loans, or 3.6% of its loan portfolio in its entirety, involves office properties. Interestingly, the company has a hefty 21% of its loan portfolio dedicated to premium finance receivables associated with life insurance, with another 14% in the form of premium finance receivable associated with commercial insurance.

Author - SEC EDGAR Data

Over this window of time, other asset values have also increased. Held to maturity securities for the company, for instance, grew from $579.9 million in 2020 to $3.6 billion in the first quarter of 2023. It is true that cash and cash equivalents have declined, dropping from $5.1 billion to only $2 billion during the same period of time. But available for sale securities managed to increase from $3.1 billion in 2020 to $3.3 billion in the first quarter of this year.

Deposits for the company have also performed quite well. During the most recent quarter, they came in at $42.7 billion. This represents only a modest decrease over the $42.9 billion reported at the end of 2022. But they also represent an increase over the $42.2 billion that the company had one year ago. The company does not provide detailed data when it comes to uninsured deposits prior to the current fiscal year. But it did say that uninsured deposits in the first quarter of 2023 totaled $14.8 billion. Of this amount, $1.8 billion was in the form of collateralized deposits. So actual uninsured deposits came in at $13 billion. That's about 30% of total deposits that the company had at that time.

Many of the banks I have looked at, some of which have gone under and others have not, have lauded their massive liquidity that sometimes well exceeds 100% of their uninsured deposits. But Wintrust Financial Corporation does not quite have this luxury. Total liquidity for the company that it has access to is about $10.9 billion, which translates to about 84% of its uninsured deposits. But there are two reasons why I am okay with this. For starters, the stability the company experienced on the deposit side during the first quarter of this year is encouraging. And the second, the company has not had to materially change its overall borrowings. At the end of 2022, it had $3.6 billion in overall borrowings. By the end of the first quarter, borrowings had actually dropped by about $13 million.

Author - SEC EDGAR Data

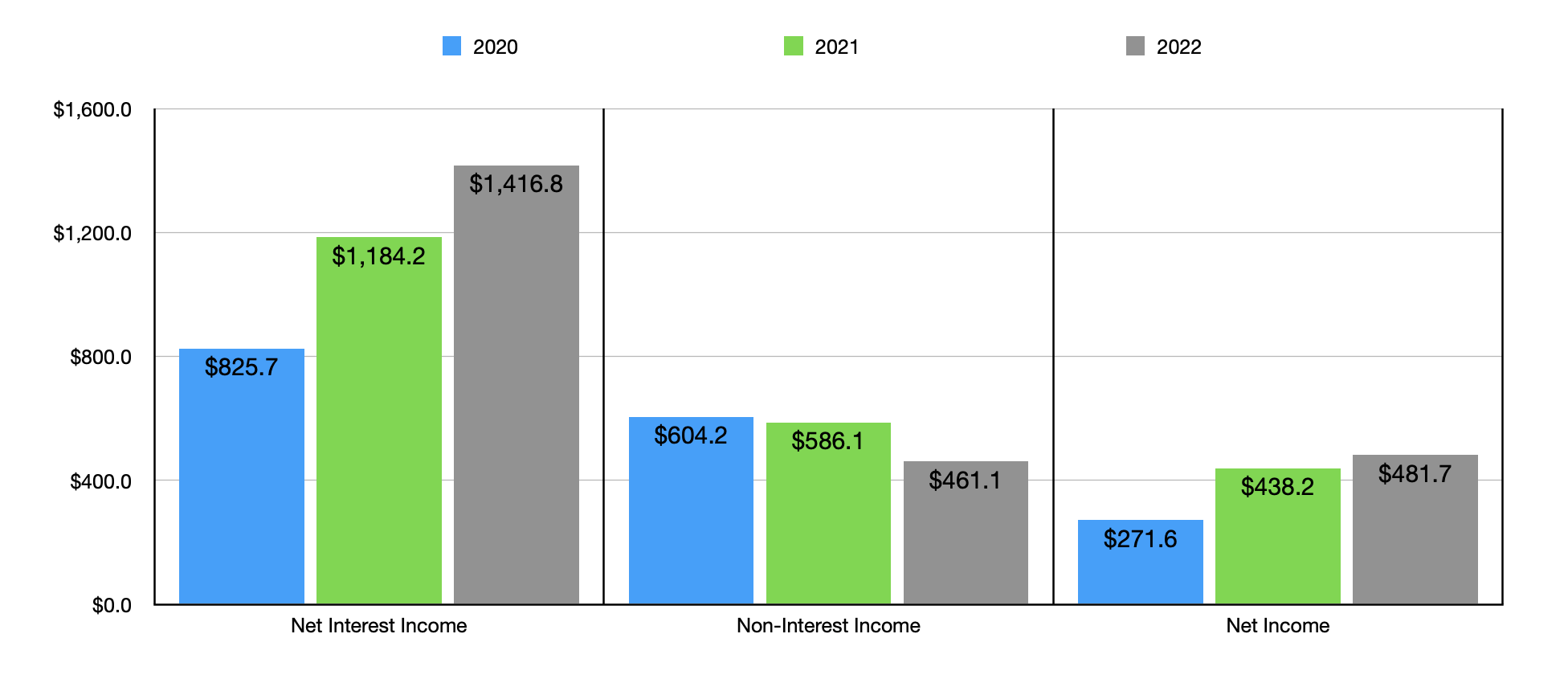

In addition to being a sound financial institution, Wintrust Financial Corporation has a nice track record from a revenue and profit perspective. Back in 2020, net interest income for the enterprise came in at $825.7 million. By 2022, this number had grown to $1.4 billion. It is true that non-interest income decreased during this time, dropping from $604.2 million to $461.1 million. But this did not stop net income for the company from climbing from $271.6 million to $481.7 million. So far this year, things continue to look up. Net interest income of $435 million dwarfs the $295.2 million reported one year ago. Non-interest income has continued to decline, dropping from $162.8 million to $107.8 million. But again, this has not been an inhibitor for the company. Net income has actually grown over this time from $120.4 million to $173.2 million.

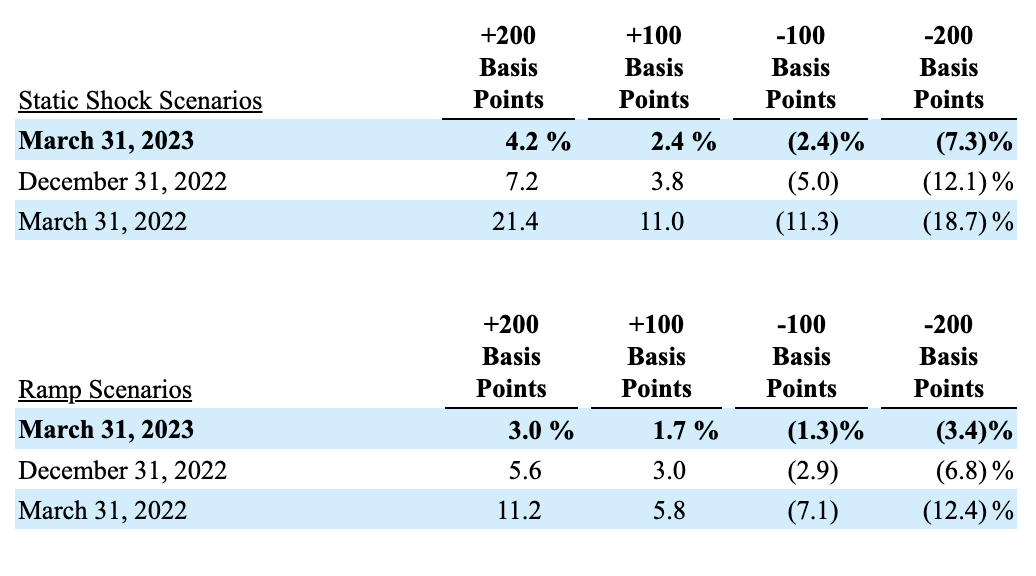

For those who believe that interest rates are either going to stay elevated or will continue to climb from here, Wintrust Financial Corporation looks particularly appealing. Management has provided a sensitivity analysis looking at both a shock scenario and a slow ramping up scenario. In the event that we see a sudden 1% increase in interest rates, net interest income for the company would pop up by 2.4%. A 2% increase would push it up by 4.2%. If these increases occur over a shorter window of time, then the rise would be 1.7% or 3%, respectively. Of course, the opposite is also true. As the image below illustrates, a decline in the interest rate would negatively affect the company. But that's the case with pretty much every bank out there.

Wintrust Financial

The last bullish indicator that I would like to point to involves the company’s book value per share. As of this writing, shares of the company are trading at $71.83. As of the end of the most recent quarter, the book value per share of the company was $75.24. Tangible book value was, obviously, lower, coming in at $64.22 per share. But in the grand scheme of things, having a company that's trading around book value is never a bad idea.

Takeaway

From all that I can tell, Wintrust Financial Corporation seems to be in solid shape. I do acknowledge that the company does not have quite as much liquidity as I would like to see. But they have made-up for this to some degree by seeing stable deposits during times of volatility. The overall track record for revenue and profitability for the company have been very impressive. And absent anything unexpected coming out of left field, I suspect that the firm's future should be bright. Given all of these points, I have decided to rate the business a ‘buy’ for now.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!

This article was written by

Daniel is an avid and active professional investor. He runs Crude Value Insights, a value-oriented newsletter aimed at analyzing the cash flows and assessing the value of companies in the oil and gas space. His primary focus is on finding businesses that are trading at a significant discount to their intrinsic value by employing a combination of Benjamin Graham's investment philosophy and a contrarian approach to the market and the securities therein.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.