MercadoLibre: Navigating A Speed Bump On The Path To Growth

Summary

- MercadoLibre, Inc. is experiencing a temporary speed bump as its fintech business slows down, causing investor concerns.

- The company's revenue growth rates have been consistently around 30%, making it an appealing investment.

- Despite the recent deceleration, MercadoLibre's core commerce business remains strong and its fintech segment is expected to become the dominant segment.

- The company's profitability profile has stabilized, hinting at potential significant profitability expansion in the future.

- I do much more than just articles at Deep Value Returns: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

brianbalster/iStock via Getty Images

Investment Thesis

MercadoLibre, Inc. (NASDAQ:MELI) is growing at very attractive rates. That's the headline. But once we dig further, we see a business that is in a transition period. The way I describe it is as a business that's hit a temporary speed bump.

Investors had latched on to one story, that of MercadoLibre as a rapidly growing Fintech business. But in the past few quarters, the Fintech business hasn't lived up to investor expectations.

However, I make the case that its story isn't over. And that, with a few more quarters of consistent around 30% revenue growth rates, investors should be more than willing to jump back into the name, as they'll believe that it's now ''compelling once again.''

Why MercadoLibre? Why Now?

In my previous analysis, I said:

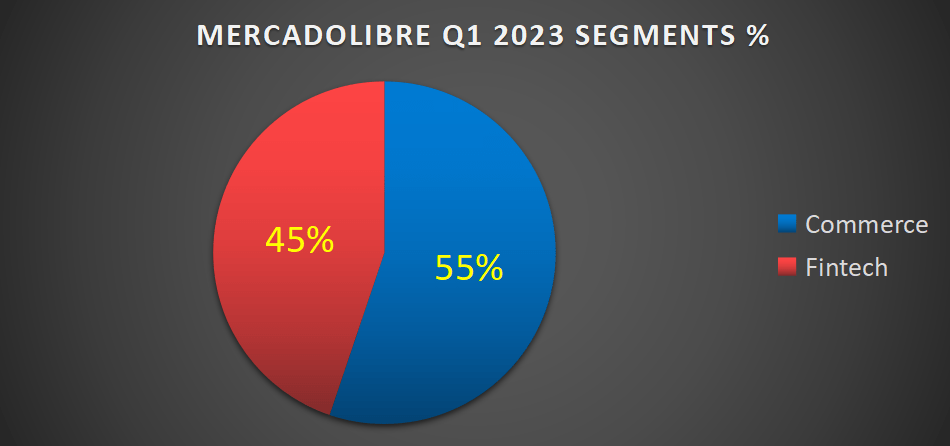

Even if MercadoLibre's Fintech business is growing at a breakneck pace, MercadoLibre's Commerce business is no pushover. However, it's just a matter of time before the Fintech business becomes MercadoLibre's biggest segment.

What follows is a graphic representation MercadoLibre's Q1 segment's breakdown.

MELI segments Q1 2023

At the core of the investment thesis was this contention.

Since investors had been so eager to see MercadoLibre's Fintech operations rapidly grow, investors had only one question in mind. How long will it take for MercadoLibre's Fintech business to dominate MercadoLibre's narrative?

Investors were fully focused and yearning to see MercadoLibre's Fintech business dazzle.

The business not only provided exposure to Latin America, a vibrant and growing market but also, crucially, MercadoLibre was meant to deliver very rapid growth. But suddenly, the bull case hit a speed bump.

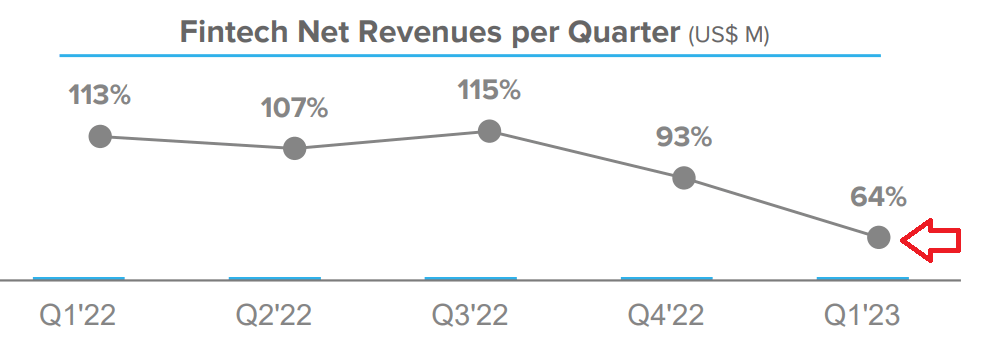

MELI Q1 2023

MercadoLibre's superfast growth segment, all of a sudden, was posting 2 back-to-back quarters of decelerating revenue growth rates. One quarter? That's fine. But two quarters? In this market?

MercadoLibre declared that this was a function of tough comparables within its credit business with the prior year. This news simply didn't still well with investors.

After all, in Q1 of the prior year, MercadoLibre's Fintech business was growing its revenue growth rates at nearly double this pace.

If the Fintech business can so dramatically decelerate in a few quarters, naturally, this leaves investors edgy.

And then, to further confound matters, consider this insight that follows.

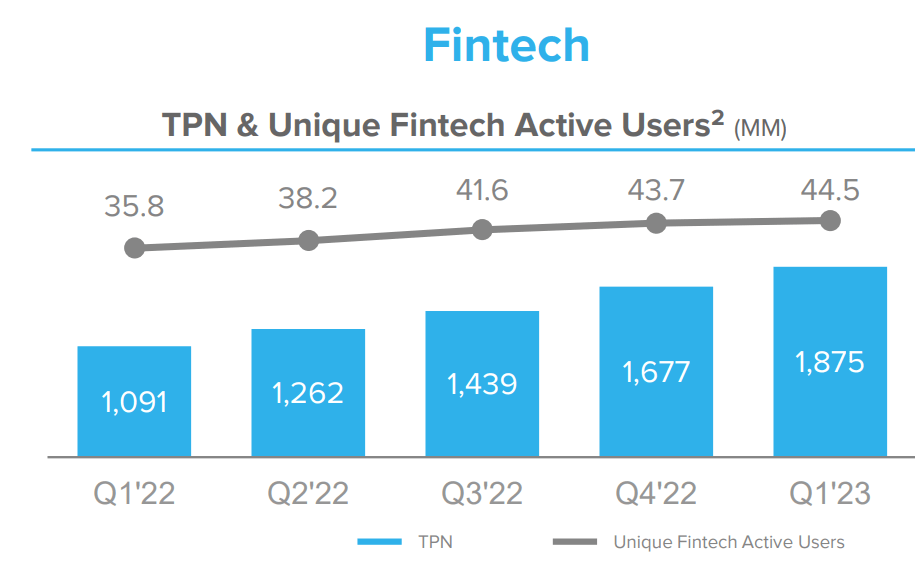

MELI Q1 2023

What we see above is that MercadoLibre's unique Fintech Active Users' sequential growth is approximately 2%.

Why is this a problem? Because you end with a group of shareholders that are having to rotate out of the name. Why?

Because a certain group of investors had latched on to one premise, but what they are now seeing is a slightly different business unfolding. And that's why, I declare, for nearly 6 months MercadoLibre's share price has been virtually glued to $1,200.

All that being said, I make the case that MercadoLibre's story isn't finished.

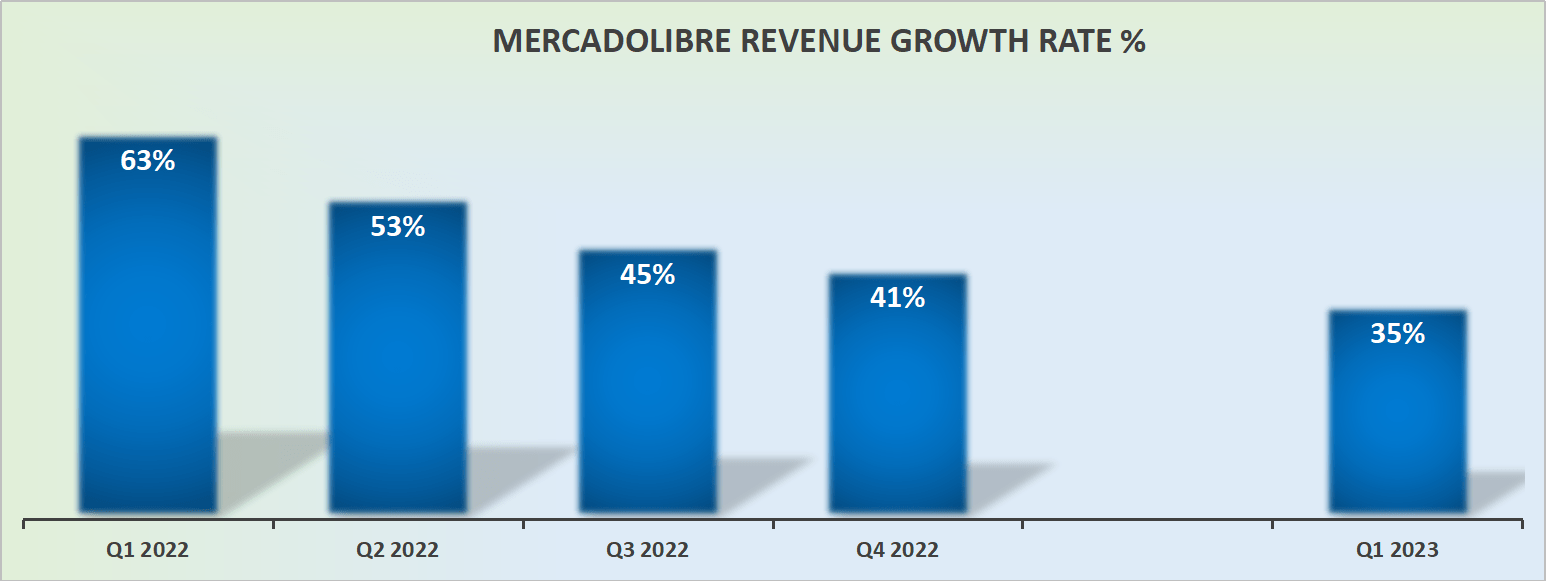

MELI Revenue Growth Rates Are Enticing

MELI revenue growth rates

Ultimately, the way we should think about MercadoLibre is as a business that's growing in the ballpark of 30% CAGR. It's not a business that's growing at +50%.

And if you think about it, that's a more than acceptable growth rate. However, again, the issue that investors have here is uncertainty.

A business that's steadily and consistently growing at 20% CAGR can be rewarded with a much higher multiple than a business that goes from growing at 60% CAGR to mid-30s% in a period of 12 months.

That being said, I would counter that by admitting, yes, MercadoLibre's growth rates are slowing down, but some bumpiness in business is inevitable.

For instance, consider this:

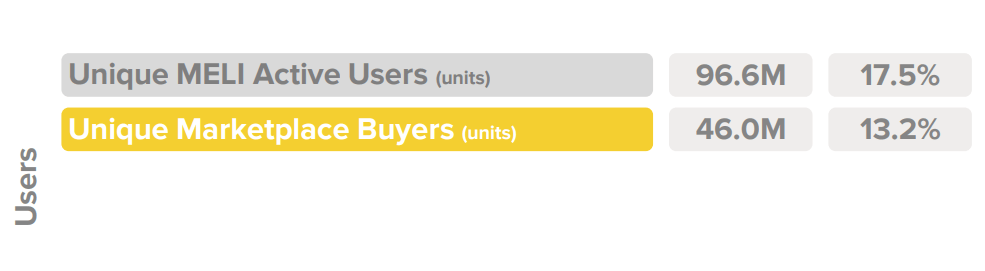

MELI Q4 2022

Back in Q4 2022, MercadoLibre's unique Marketplace Buyers (actual buyers, rather than someone who just posed a question on the site), were up 13% y/y.

And then, in the following quarter, this number grew to 17% y/y.

MELI Q1 2023

This is my point, a business can grow at around 30% CAGR for a really long period of time. Just because the business so significantly decelerated from its hypergrowth rates last year does not mean that's where the story ends.

Particularly if the business is self-funding, which takes me to our next section.

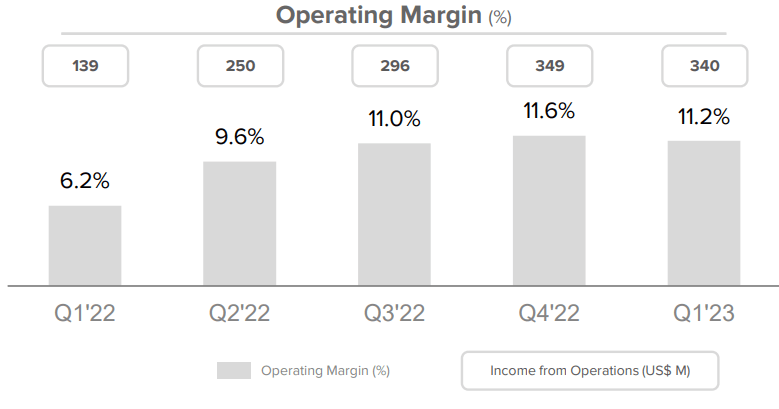

MELI Profitability Profile Has Stabilized

MELI Q1 2023

This is the same story that we touched on throughout this analysis, that MercadoLibre was delivering very strong top line growth and this was percolating through to significant profitability expansion.

But in the past 2 quarters, and most noticeably in Q1 2023, MercadoLibre didn't quite see its excess revenues falling to the bottom line.

Altogether, this is how I sum up MercadoLibre today: the business has hit a speed bump, and this has seen many hypergrowth investors step away from MELI stock. But over the medium term, investors should be more than content to return to the stock and bid it higher, once the business growth rates stabilize somewhat.

The Bottom Line

MercadoLibre, Inc. is currently facing a temporary speed bump as its fintech business experiences a slowdown, leading to investor concerns.

However, the company's story is far from over, and with consistent revenue growth rates of around 30%, investors may find it compelling once again.

Despite the recent deceleration, MercadoLibre's core commerce business remains strong, and the fintech segment is expected to become its dominant segment in due time. The company's profitability profile has also stabilized, indicating a potential for significant profitability expansion in the future.

Although MercadoLibre's growth rates have moderated, the business is poised for stability and long-term growth, making MELI stock an attractive investment opportunity once the growth rates stabilize.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.

This article was written by

DEEP VALUE RETURNS: The only Marketplace with real performance. No gimmicks. I provide a hand-holding service. Plus regular stock updates.

We are all working together to compound returns.

WARNING: Any stocks that you feel like buying after discussions with me are your responsibility.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.