Turnstone Biologics Begins $86 Million U.S. IPO Plan

Summary

- Turnstone Biologics has filed to raise $86 million in a U.S. IPO, although the final figure may differ.

- The company is developing treatment candidates for various cancers.

- TSBX is still in Phase 1 safety trials for its lead candidate; the firm has notable life science investors and collaboration agreements with major pharmaceutical companies.

- Looking for more investing ideas like this one? Get them exclusively at IPO Edge. Learn More »

Sean Anthony Eddy

A Quick Take On Turnstone Biologics

Turnstone Biologics Corp. (TSBX) has filed to raise $86.25 million in an IPO of its common stock, according to an S-1 registration statement.

The firm is a clinical-stage biopharma developing treatments for solid tumors and other major cancer conditions.

When we learn more IPO details, I’ll provide an update.

Turnstone Overview

La Jolla, California-based Turnstone Biologics Corp. was founded to develop differentiated treatment approaches using tumor infiltrating lymphocytes [TILs] for treating various cancers.

Management is headed by president and CEO Sammy Farah, M.B.A., Ph.D., who has been with the firm since October 2015 and was previously president of Synthetic Genomics Vaccines and was Chief Business Officer at Immune Design Corp.

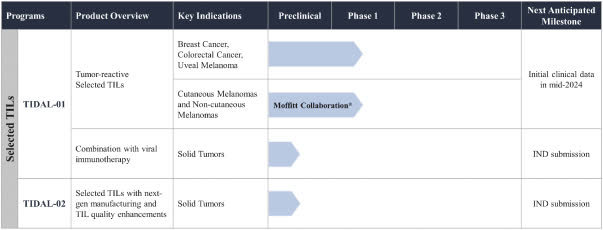

The firm's lead candidate, TIDAL-01, is in Phase 1 trials for breast cancer, colorectal cancer and uveal melanoma and other cancer types.

Turnstone's company pipeline is as follows:

Company Pipeline (SEC)

As of March 31, 2023, Turnstone has booked fair market value investment of $193 million from investors including Versant Ventures, OrbiMed, F-Prime Capital and FACIT Inc.

Turnstone’s Market & Competition

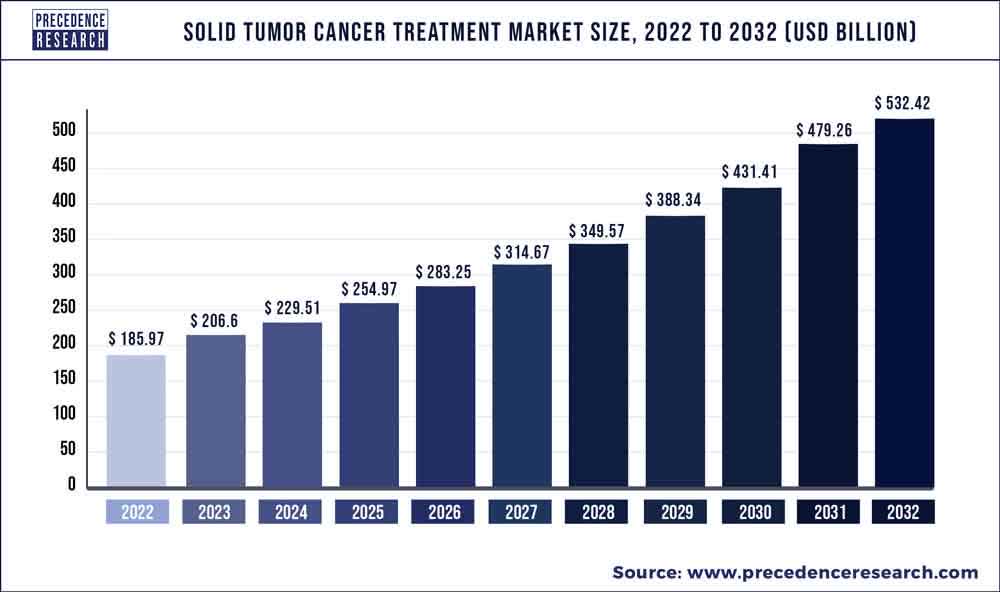

According to a 2023 market research report by Precedence Research, the global market for solid tumor cancer treatments was an estimated $186 billion in 2022 and is forecast to reach $532 billion by 2032.

This represents a forecast CAGR (Compound Annual Growth Rate) of 11.09% from 2023 to 2032.

The main drivers for this expected growth are improvements in treatment options coupled with government emphasis on creating greater availability amid higher demand from patients worldwide.

Also, the chart below shows the historical and projected future growth rate of the solid tumor treatment market, from 2023 to 2032:

Solid Tumor Cancer Treatment Market (Precedence Research)

Major competitive or other industry participants include the following:

Iovance Biotherapeutics (IOVA)

Achilles Therapeutics (ACHL)

Instil Bio (TIL)

KSQ Therapeutics

Lyell Immunopharma (LYEL)

Obsidian Therapeutics

Intima Bioscience

Adaptimmune Therapeutics (ADAP)

Adicet Bio (ACET)

Alaunos Therapeutics (TCRT)

Atara Biotherapeutics (ATRA)

Immatics N.V. (IMTX)

Others

Turnstone Biologics Financial Performance

The company’s recent financial results can be summarized as follows:

Variable collaboration revenue

Uneven operating results

Increasing cash used in operations

Below are relevant financial results derived from the firm’s registration statement:

Total Revenue | ||

Period | Total Revenue | % Variance vs. Prior |

Three Mos. Ended March 31, 2023 | $ 19,306,000 | 80.1% |

2022 | $ 73,300,000 | -27.6% |

2021 | $ 101,293,000 | |

Operating Profit (Loss) | ||

Period | Operating Profit (Loss) | Operating Margin |

Three Mos. Ended March 31, 2023 | $ (394,000) | -2.0% |

2022 | $ (31,626,000) | -43.1% |

2021 | $ 32,993,000 | 32.6% |

Net Income (Loss) | ||

Period | Net Income (Loss) | Net Margin |

Three Mos. Ended March 31, 2023 | $ - | 0.0% |

2022 | $ (31,024,000) | -160.7% |

2021 | $ 3,479,000 | 18.0% |

Cash Flow From Operations | ||

Period | Cash Flow From Operations | |

Three Mos. Ended March 31, 2023 | $ (17,170,000) | |

2022 | $ (71,062,000) | |

2021 | $ (45,629,000) | |

(Source - SEC)

As of March 31, 2023, Turnstone had $33.5 million in cash and $20.5 million in total liabilities.

Turnstone Biologics Corp. IPO Details

Turnstone intends to raise $86.25 million in gross proceeds from an IPO of its common stock, although the final figure may differ.

No existing shareholders have indicated an interest in purchasing shares at the IPO price, although that may change in a future filing.

The firm is an ‘emerging growth company’ as defined by the 2012 JOBS Act and may elect to take advantage of reduced public company reporting requirements; prospective shareholders would receive less information for the IPO and in the future as a publicly-held company within the requirements of the Act.

Management says it will use the net proceeds from the IPO as follows:

to fund the continued development of TIDAL-01 in our two Phase 1 clinical trials for the treatment of breast cancer, colorectal cancer, uveal melanoma and other non-cutaneous and cutaneous melanomas;

to advance our TIDAL-02 and TIDAL-01 and viral immunotherapy combination programs; and

remaining proceeds, if any, for working capital and general corporate purposes

(Source - SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management says the firm is not currently involved in any legal proceedings that would have a material adverse effect on its financial condition or operations.

The listed bookrunners of the IPO are BofA Securities, SVB Securities and Piper Sandler.

Commentary About Turnstone’s IPO

TSBX is seeking public capital market investment to fund the development of TIDAL-01 and TIDAL-02 treatment candidates.

The company’s financials have shown fluctuating collaboration revenue, variable operating results and growing cash used in operations.

The firm's lead candidate, TIDAL-01, is in Phase 1 trials for breast cancer, colorectal cancer and uveal melanoma and other cancer types.

TIDAL-02 is still in preclinical development for the treatment of solid tumors.

The company’s investor syndicate includes a number of well-known life science venture capital firms.

Turnstone has two major pharmaceutical company collaboration agreements, one with AbbVie (ABBV) and one with Takeda Pharmaceuticals (TAK).

The market opportunity for treating solid tumors and other major cancers is extremely large and will continue to grow over the coming years as the global population ages.

BofA Securities is the lead underwriter, and the two IPOs led by the firm over the last 12-month period have generated an average return of 19.7% since their IPO. This is a middle-tier performance for all major underwriters during the period.

Risks to the company’s outlook as a public company include normal and customary risks associated with its trial efforts in difficult-to-treat cancers.

When we learn more about management’s assumptions about IPO pricing and valuation, I’ll provide a final opinion.

Expected IPO Pricing Date: To be announced.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis.

Get started with a free trial!

This article was written by

I'm the founder of IPO Edge on Seeking Alpha, a research service for investors interested in IPOs on US markets. Subscribers receive access to my proprietary research, valuation, data, commentary, opinions, and chat on U.S. IPOs. Join now to get an insider's 'edge' on new issues coming to market, both before and after the IPO. Start with a 14-day Free Trial.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.