Celsius Holdings Hits My Price Target - Where To Go From Here?

Summary

- Celsius Holdings has seen significant growth and surpassed $250 million in revenues, with its partnership with PepsiCo contributing to its success.

- Celsius is taking market share away from competitors like Red Bull and Monster, and its stock price target has been raised to $164-$180.

- Despite the rally, short interest in Celsius remains high at 21.6%, which could lead to a short squeeze in the near term.

Romain Maurice/Getty Images Entertainment

Investment Thesis And Introduction

Celsius Holdings (NASDAQ:CELH) has unequivocally been one of the best growth stocks in the entire market over the last several years. The recent earnings report showed that the company surpassed the all important mark of $250 million in quarterly revenues, with EPS that came in at double what analysts were expecting. Largely, this is because the PepsiCo (PEP) distribution has impacted the company in a dramatic way even early into the partnership. This caused shares of Celsius to gap up in price in early May, hitting the $130 level and the stock has been trending higher still to new all-time highs as of this week. The question on many minds is, when will the rally end?

In my last article on Celsius, I gave a price target range between $135 - $157 for the year, citing the potential for Celsius to break above the $1 billion annual revenue target and to continue on the path of market share growth. With quarterly revenue numbers coming in higher than previously expected and the summer beverage season kicking off, it seems that the market is pricing in the likelihood of another highly profitable quarter and record growth. With my previous price target hit much faster than I was expecting, I am now raising my annual price target range to between $164 - $180.

Celsius Is Winning The War Against Monster

In a recent research note, Piper Sandler stated that Monster Beverage's (MNST) earnings growth prospects were largely priced into the stock already, while Celsius is becoming a more attractive stock to invest in the energy drink space. Many market participants have noted in the past that despite much higher growth, Celsius trades at a similar forward price-to-sales multiple as Monster Beverage. Celsius currently trades at around 9x forward sales, while Monster Beverage trades at 8.5x forward sales estimates. It is virtually impossible for Monster to double its revenues year-over-year, but for Celsius, this is attainable with the company on track to do $1-2 billion in annual revenues over the next couple years.

The premium valuation for both stocks speaks to the current environment, as the summer beverage season is just starting and gross margins are expected to recover more over the coming months. As inflation eases, this will impact the financial results of both companies in a positive way, but Celsius has much more upside given the fact that the company is taking market share away from competitors such as Red Bull and Monster. Competition remains a substantial risk for the long-term as new entrants come into the market, but both Monster and Celsius enjoy dominant market positions currently, with Celsius on track to cause further disruptions in the industry thanks to the distribution deal with PepsiCo.

Monster, in my opinion, does deserve a high valuation given that it is the industry leader with the more dominant market position. Both stocks could be great additions to a portfolio, but Celsius stands out for many reasons as the better option for investors going forward.

One reason is that Celsius is still lagging in terms of international growth compared to rivals. While this could be seen as a negative in the short-term, it is likely that the company's distribution deal with PepsiCo will expand the brand's awareness to a worldwide audience, although I estimate that it will be several years before seeing penetration into these new markets. Still, it appears that Celsius is continuing to take market share at a rapid pace in North America, and if the company can continue to beat earnings estimates, proving sustainable and profitable growth, the stock could continue to rally into the end of the year and beyond. Despite the share price at an all-time high, Celsius stock is worth holding and even worth buying given a decent correction.

The Elephant In The Room - Short Interest

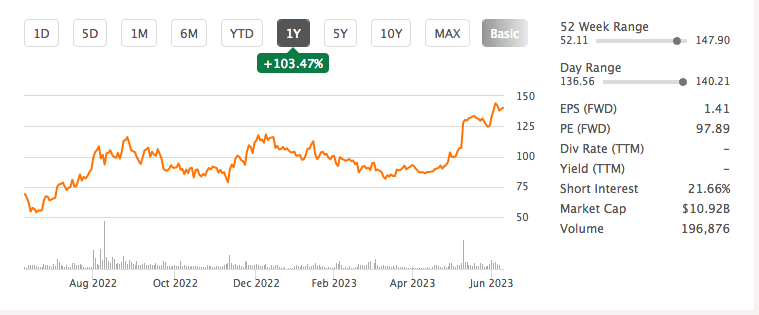

Despite an incredible rally and continuation of the bullish uptrend, short interest in the company is still elevated beyond what I would consider normal. As of June 8th, 2023, Monster's short interest according to Seeking Alpha sat at less than 1.5%, while short interest in Celsius Holdings is currently a whopping 21.6%. Both stocks are barely off from their all-time highs, but the market is not willing to give up selling stocks short in 2023, as CELH already had elevated short interest going into the last earnings report.

CELH Metrics (Seeking Alpha)

It seems as though investors are betting on an end to the rally in Celsius in conjunction with the summer beverage season, which makes little sense to me. In analysis of past trends, typically the winter season has a meaningful drop-off in terms of sales while the summer season is the strongest. Celsius was recently able to buck that trend, with the company's Q4 revenues coming in much stronger than expected.

There is a remarkable amount of short interest in Celsius Holdings and virtually none in Monster Beverage, despite the recent change in how analysts and market participants are viewing these two companies. This could produce more exaggerated movements in price action, such as witnessed with Celsius on the last earnings report where the stock moved into the new range above $125 per share and after a brief pullback, has now reached well above the lower end of my price target of $135 per share.

When Will The Rally End?

The rally in Celsius Holdings continues on, with shares hitting a new all-time high of $150.35 in today's trading session (6/13), and with continued profitable growth and market share gains, I would not expect the stock to falter much over the coming months as the summer beverage season picks up. Short-sellers have not covered their positions to a great degree, even with the stock at all-time highs and the company continuing to buck seasonal trends which were apparent in the past. While I do not incorporate the potential for short squeezes into my investment decisions, there is a possibility that the stock could experience a short squeeze in the near-term as the 21%+ short interest is winded down. I would rate Celsius Holdings with a 'Hold' recommendation until this phenomenon plays out, but would be a buyer on a decent correction in the share price.

There is no way to definitively say when the rally in Celsius might end, but there are risks that one should be aware of when investing in the company over the long-term. The biggest thing to consider is one's time horizon, as this is paramount to produce favorable results when investing. In my previous article on Celsius, I stated that:

With shares about 25% off of the recent highs, the market has been much too focused on the short-term, with many market participants willing to sell even before the PepsiCo distribution begins to take full effect and show up more in the company's financial results. Now that Celsius has reported Q3 earnings showing continued revenue growth, improving margins, and market share growth to 4.9%, there are telltale signs that the stock could once again double in the coming years."

Source: Celsius: Q3 Earnings Show That The Stock Could Potentially Double Once More

Celsius is a very high-growth stock, with volatile price movements and potential short-term risks, such as multiple contraction, that can throw investors and traders alike for a loop. Being able to battle short-term thinking is one of the biggest advantages one can have, and be willing to see oneself as an owner of a business, not a trader looking to make a profit in the next week or month.

Conclusion

Celsius Holdings has unequivocally been one of the best growth stocks in the entire market over the last several years. As inflation eases, costs should come down which will improve margins further, and more market share gains with profitable growth spurred on by the PepsiCo distribution will likely continue to impact the financial results in a positive way. Celsius stock has much more upside here than competition, such as Monster Beverage, given the out-sized growth relative to the stock's valuation. Celsius currently trades at around 9x forward sales, while Monster Beverage trades at 8.5x forward sales estimates. With Celsius on track to do between $1-2 billion in annual sales over the next couple years, the current valuation looks much more attractive than peers. I would not expect the stock to falter much over the coming months as the summer beverage season picks up, but a high valuation for both Monster and Celsius invites the possibility of a multiple contraction as a substantial risk for shareholders. Another thing to keep in mind is the current short interest of CELH, as this could have a profound effect on the stock in the near-term as short-covering, in my opinion, is somewhat likely given the recent stock performance. Having revisited the stock after my previous price target was hit, I am once again raising my annual price target for shares of Celsius Holdings to $164 - $180 and rate the stock as a 'Hold,' but would be a buyer upon a decent correction in the stock price.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CELH either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.