Zeta Global's Revenue Growth Rate Drops While Operating Losses Continue

Summary

- Zeta Global Holdings Corp. reported its Q1 2023 financial results on May 4, 2023.

- The firm provides organizations with AI-enhanced online advertising tracking technologies and services.

- Zeta Global Holdings' management increased 2023 guidance, but its revenue growth rate will be lower than 2022's growth rate.

- With operating losses still high, I'm on Hold for Zeta Global Holdings Corp. stock in the near term.

- Looking for more investing ideas like this one? Get them exclusively at IPO Edge. Learn More »

Khanchit Khirisutchalual

A Quick Take On Zeta Global

Zeta Global Holdings Corp. (NYSE:ZETA) reported its Q1 2023 financial results on May 4, 2023, beating expected revenue but missing EPS estimates.

The company operates a programmatic marketing automation and consumer intelligence platform for advertisers worldwide.

I previously wrote about Zeta Global with a Buy rating.

I'm concerned about Zeta's combination of slowing top line revenue growth and continued high operating losses, both of which have been punished in a higher cost of capital environment.

As such, I'm on Hold for ZETA stock for the near term.

Zeta Global Overview

New York, NY-based Zeta was founded to develop advanced online advertising capabilities for companies to generate greater returns from their online marketing efforts.

Management is headed by co-founder, Chairman and CEO David Steinberg, who has been with the firm since and was previously the founder and CEO of InPhonic, a wireless phone and communications products company.

The company's primary offerings include:

Opportunity Explorer.

Identity Graph.

Intent Graph.

Agile Intelligence.

APIs.

The firm pursues primarily large-sized clients across all major industry verticals via a direct sales model.

Zeta's Market & Competition

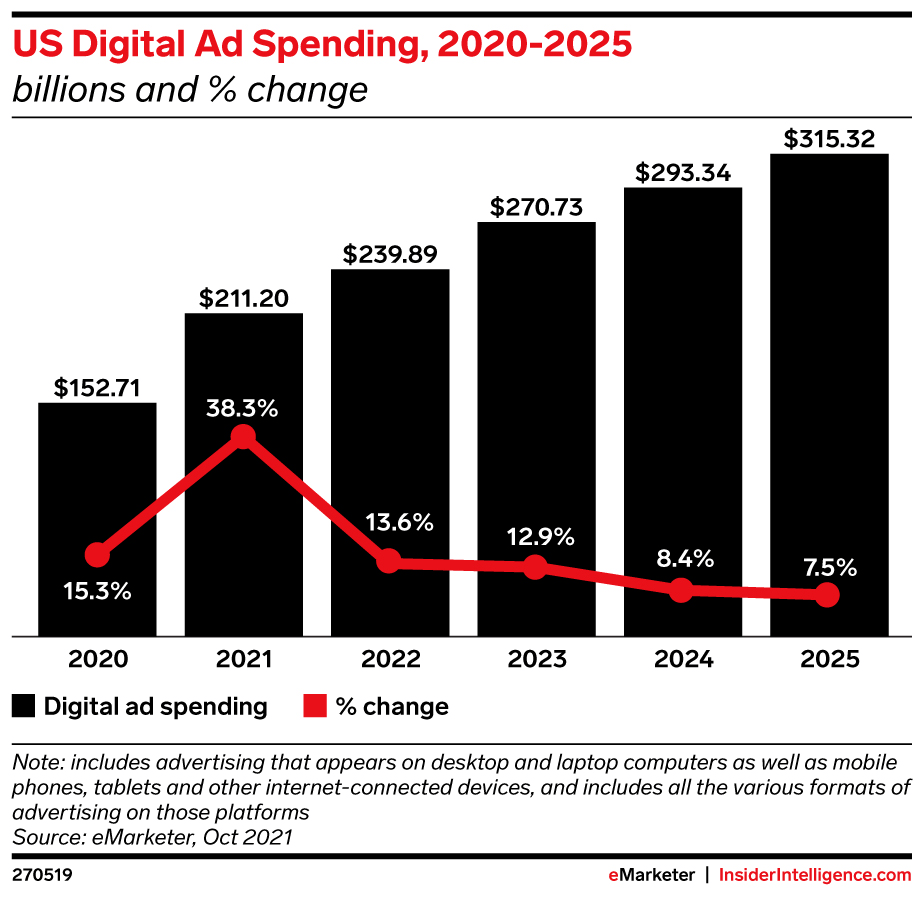

According to a market research note by eMarketer, the market for digital ad spending was an estimated $153 billion in 2020 and is forecast to reach $315 billion by 2025.

In 2020, despite the global pandemic, digital ad spending grew by 12.7%.

The note asserts that 2021 saw significantly increased digital advertising growth after a slower than expected 2020, but that future growth rates will decline through 2025.

The chart below shows the report's forecasted growth trajectory and digital ad spend percentage of total, from 2020 to 2025:

US Digital Ad Spending (eMarketer)

Potential competitors include:

Google.

Adobe.

Yahoo.

Meta.

Oracle.

Skai.

Amazon.

Criteo.

Zeta's Recent Financial Trends

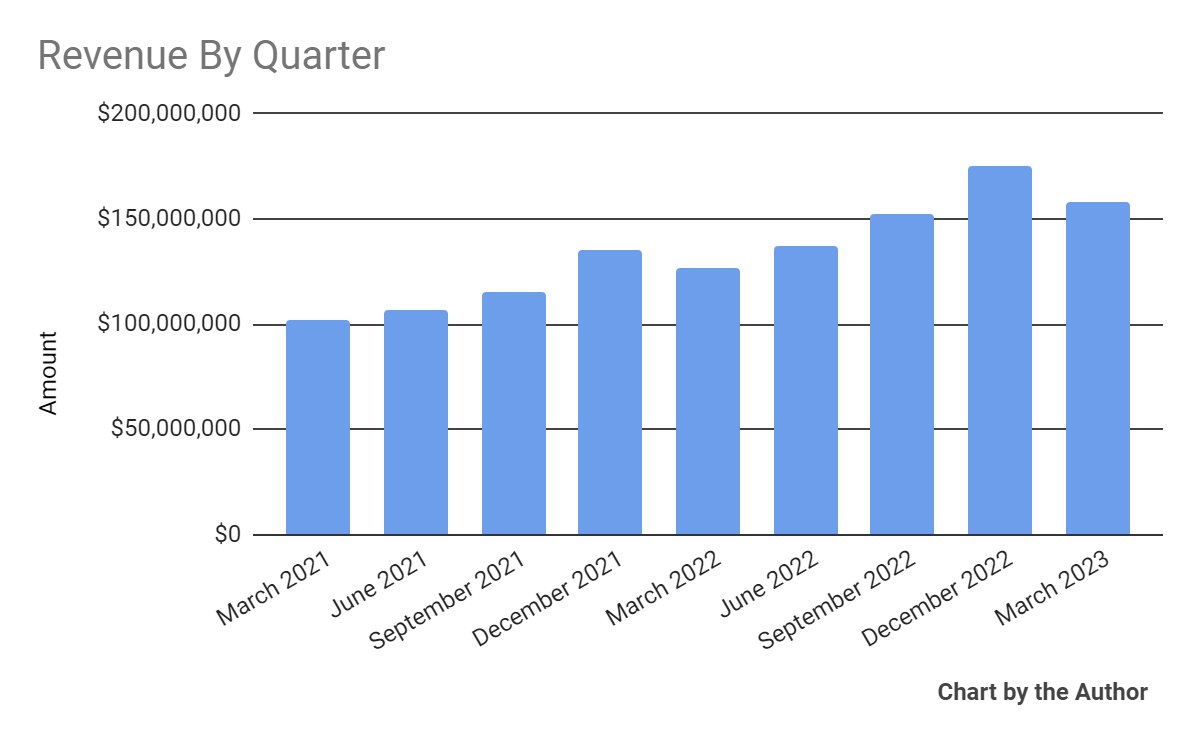

Total revenue by quarter has grown per the following chart:

Total Revenue (Seeking Alpha)

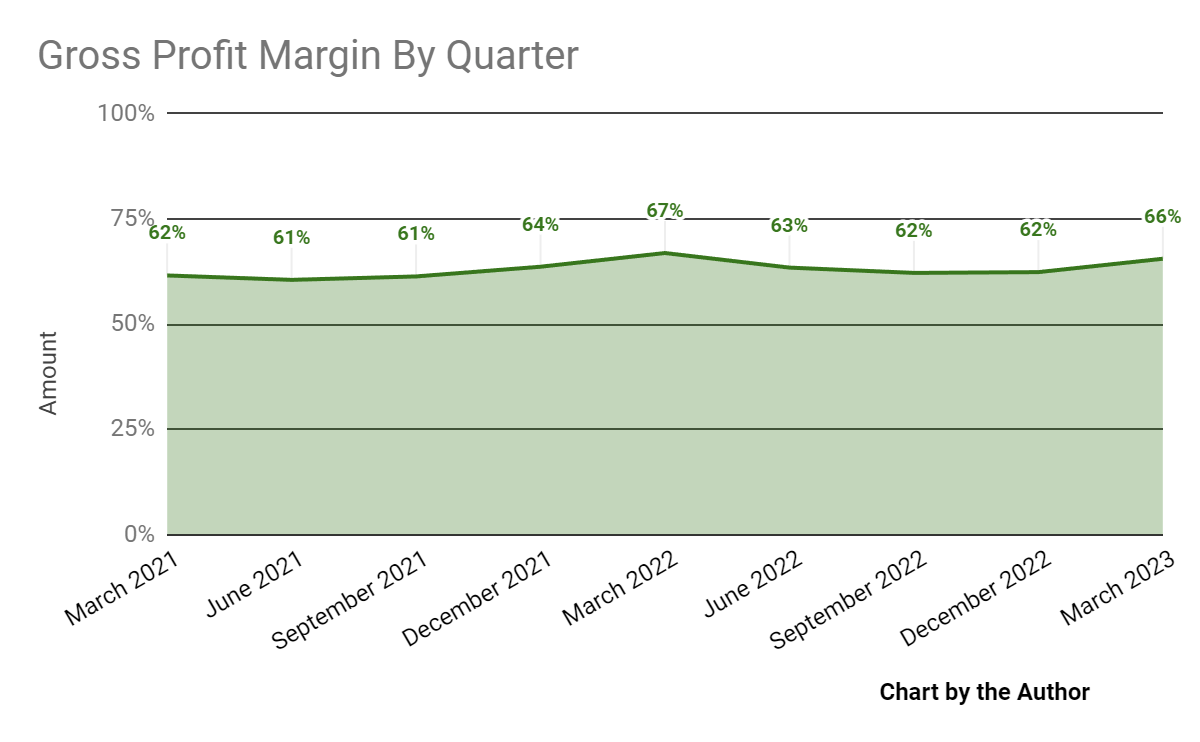

Gross profit margin by quarter has trended slightly lower in recent quarters:

Gross Profit Margin (Seeking Alpha)

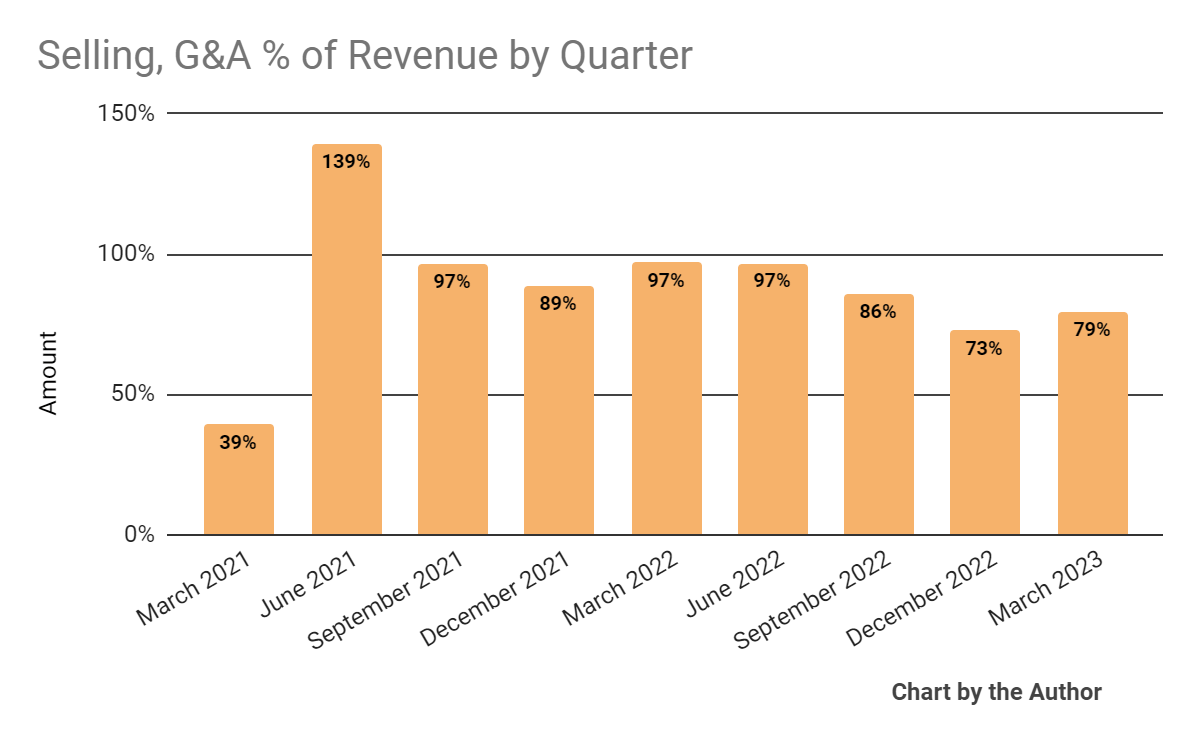

Selling, G&A expenses as a percentage of total revenue by quarter have also trended lower, a positive sign:

Selling, G&A % Of Revenue (Seeking Alpha)

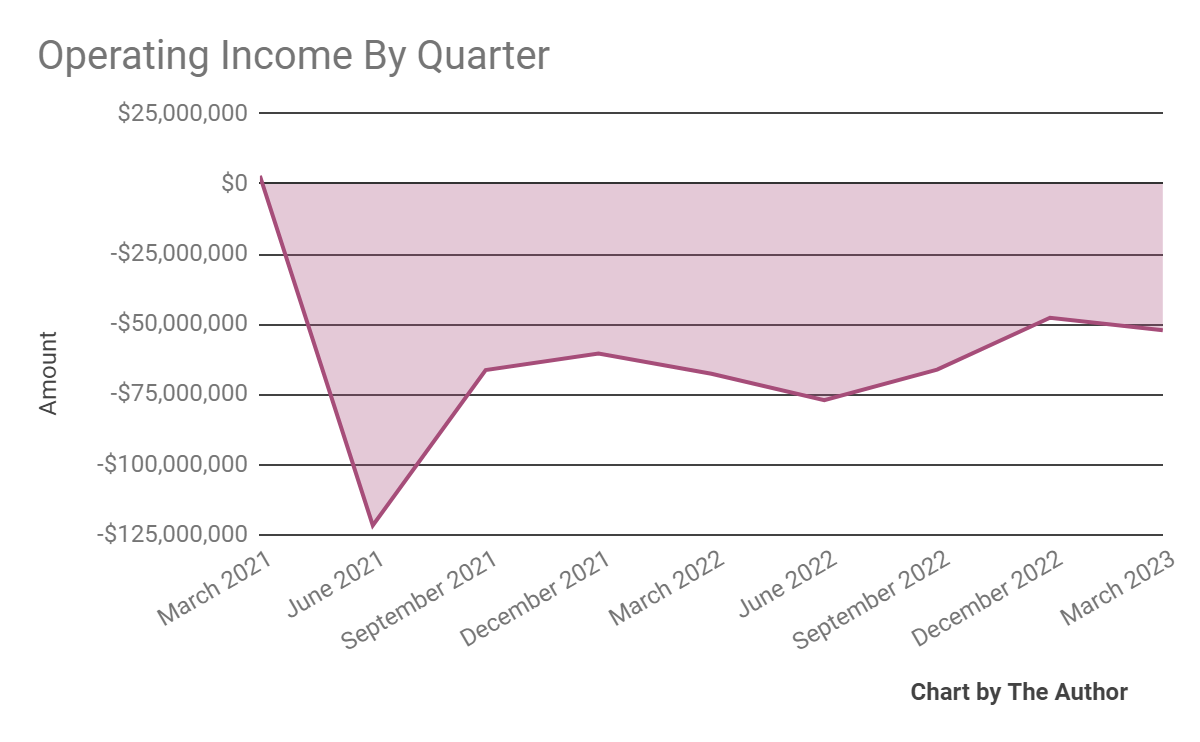

Operating income by quarter has remained heavily negative, as the chart shows:

Operating Income (Seeking Alpha)

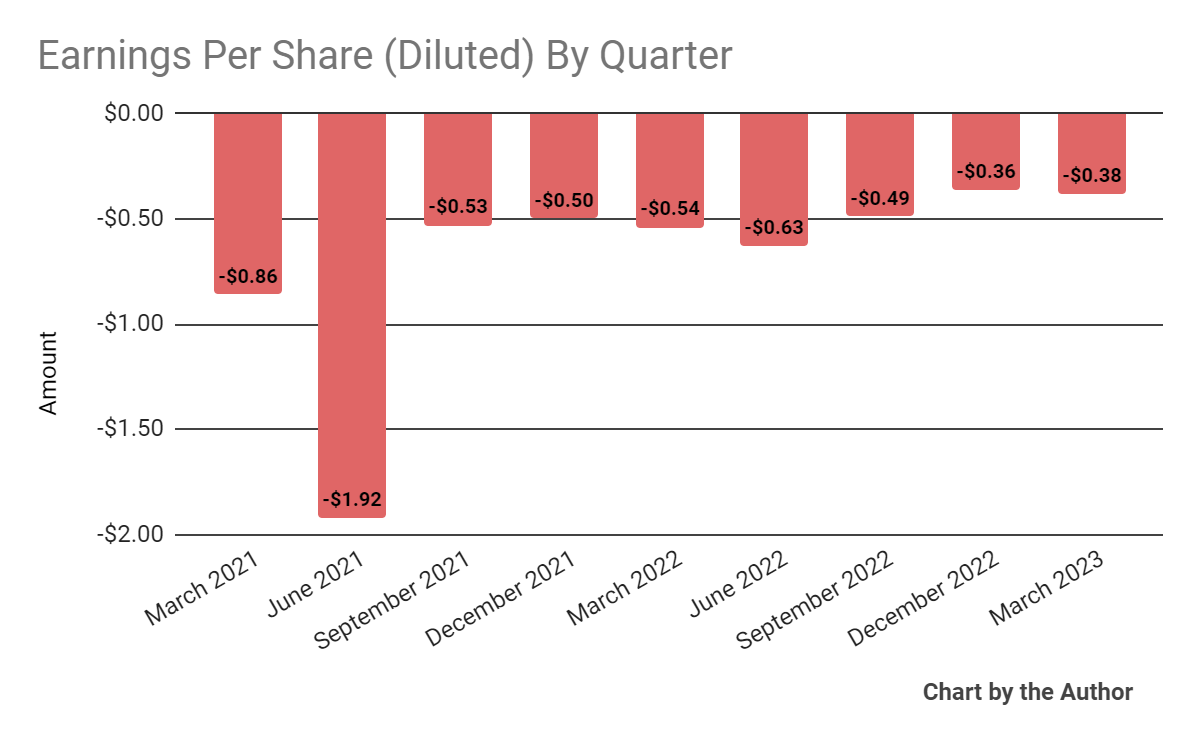

Earnings per share (Diluted) have also remained negative:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

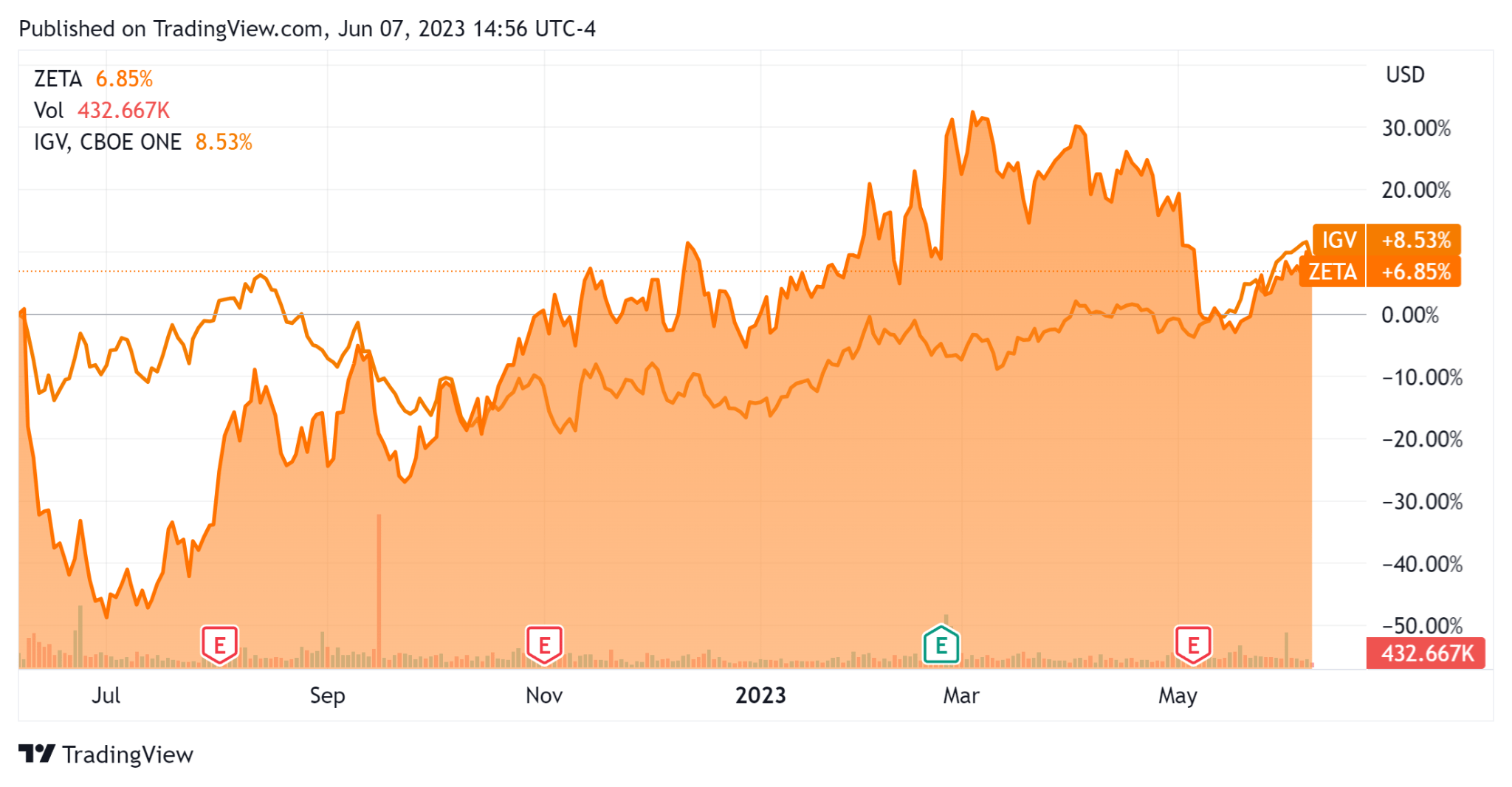

In the past 12 months, ZETA's stock price has risen 6.85% vs. that of the iShares Expanded Technology-Software ETF's (IGV) growth of 8.53%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

For the balance sheet, the firm ended the quarter with $107.8 million in cash and equivalents and $183.8 million in total debt, none of which was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $56.7 million, of which capital expenditures accounted for $20.7 million. The company paid a whopping $289.7 million in stock-based compensation, or SBC, in the last four quarters.

Valuation And Other Metrics For Zeta Global

Below is a table of relevant capitalization and valuation figures for the company:

Measure [TTM] | Amount |

Enterprise Value / Sales | 3.2 |

Enterprise Value / EBITDA | NM |

Price / Sales | 2.0 |

Revenue Growth Rate | 28.8% |

Net Income Margin | -42.5% |

EBITDA % | -30.9% |

Net Debt To Annual EBITDA | -0.4 |

Market Capitalization | $1,900,000,000 |

Enterprise Value | $1,970,000,000 |

Operating Cash Flow | $77,410,000 |

Earnings Per Share (Fully Diluted) | -$1.86 |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

ZETA's most recent Rule of 40 calculation was negative (2.1%) as of Q1 2023's results, so the firm has performed poorly in this regard, per the table below:

Rule of 40 Performance | Calculation |

Recent Rev. Growth % | 28.8% |

EBITDA % | -30.9% |

Total | -2.1% |

(Source - Seeking Alpha)

Commentary On Zeta Global

In its last earnings call (Source - Seeking Alpha), covering Q1 2023's results, management highlighted the market environment of seeing "organizations more willing to take risks with new partners and adopt new solutions in order to drive better outcomes."

Leadership believes that the firm's long-time integration of machine learning and AI technologies to enhance its offering puts the company's solution in the sweet spot of where the market is heading.

Management did not disclose any company or customer retention rate metrics for the quarter.

Total revenue for Q1 2023 rose 24.8% YoY, while gross profit margin fell 1.4 percentage points.

Selling, G&A expenses as a percentage of revenue dropped 17.4 percentage points, a very positive move, and operating losses narrowed by 22.9% YoY while still remaining quite high.

Looking ahead, management increased its 2023 revenue guidance by $10 million to $701 million at the midpoint, or 19% growth over 2022.

If achieved, that 19% annual expected growth rate would be considerably less than 2022's 28.95% growth rate over 2021, so the firm's growth rate appears to be slowing significantly.

The company's financial position is solid, with plenty of liquidity, a moderate amount of long-term debt and strong free cash flow.

ZETA's Rule of 40 performance has been negative, with good revenue growth but poor operating results.

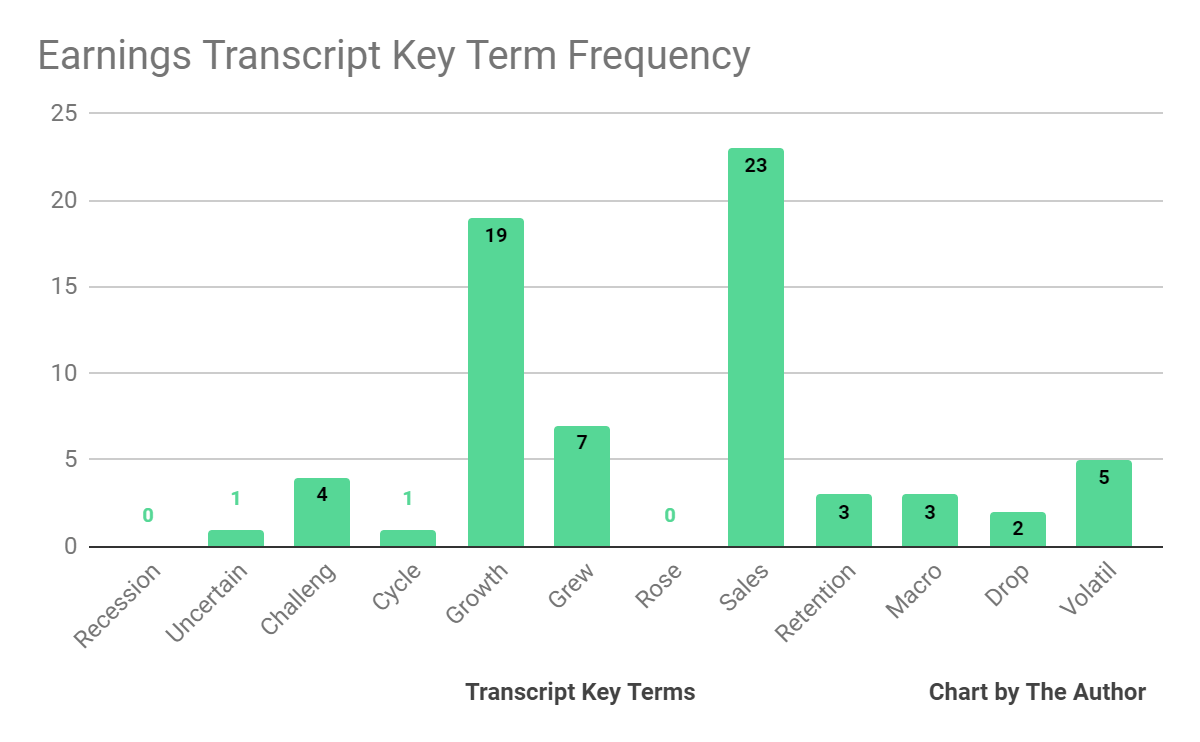

From management's most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I'm most interested in the frequency of potentially negative terms, so management or analyst questions cited "Uncertain" once, "Challeng[es][ing]" four times, "Macro" three times and "Volatil[e][ity]" five times.

The negative terms refer to the current volatile macroeconomic conditions, which can be a negative or a positive for the company.

Regarding valuation, the market is valuing ZETA at an EV/Sales multiple of around 3.2x.

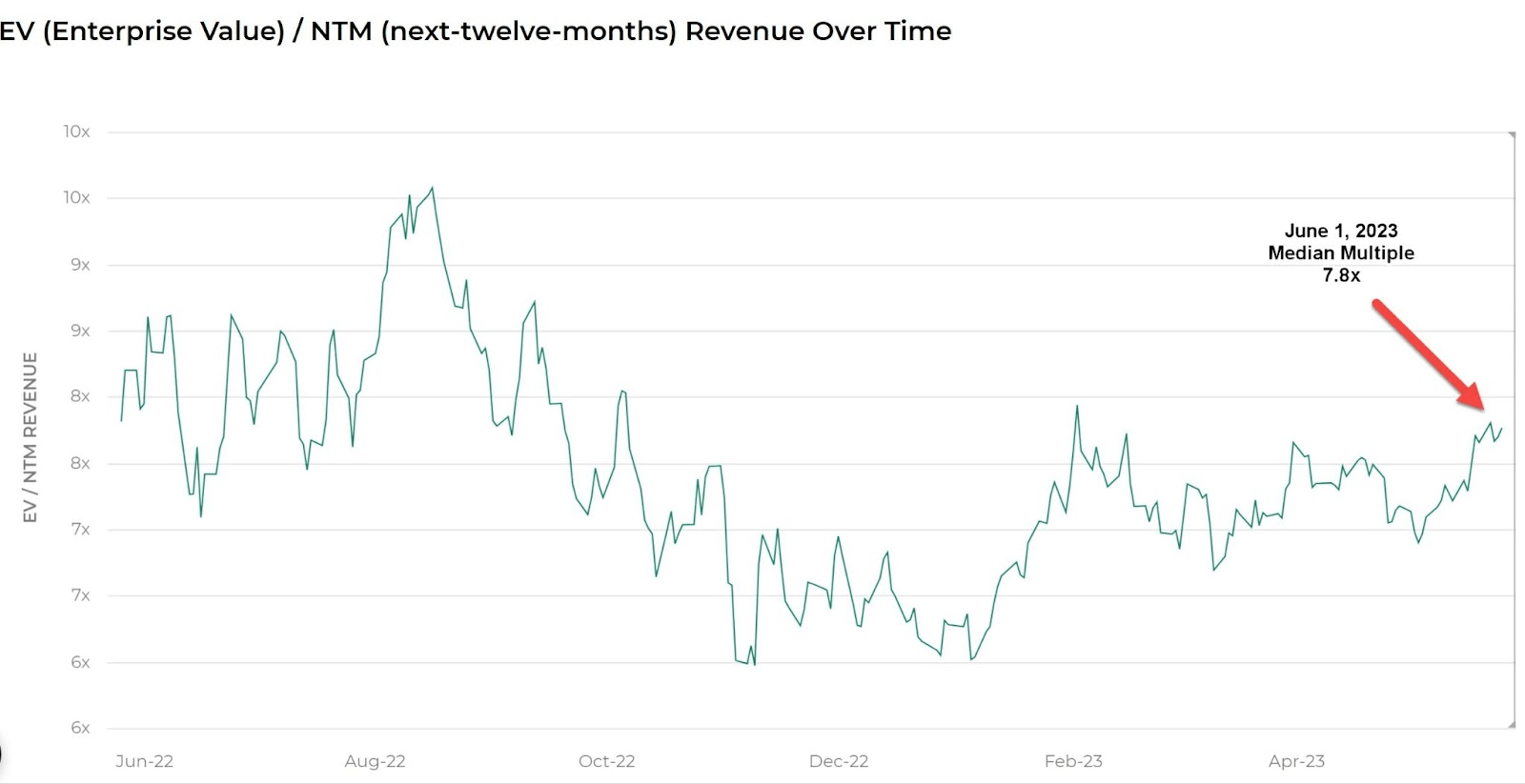

The Meritech Capital Index of publicly held SaaS application software companies showed an average forward EV/Revenue multiple of around 7.9x on June 1, 2023, as the chart shows here:

EV/Next 12 Months Revenue Multiple Index (Meritech Capital)

So, by comparison, ZETA is currently valued by the market at a substantial discount to the broader Meritech Capital SaaS Index, at least as of June 1, 2023.

Risks to the company's outlook include an economic slowdown that may be underway, reduced credit availability which may affect customer/prospect spending plans and lengthening sales cycles which may reduce its revenue growth potential in the near term.

A potential upside catalyst to the stock could include growing interest in the firm's AI-related services, leading to revenue upside in the coming quarters.

However, I'm concerned about the combination of slowing topline revenue growth and continued high operating losses, both of which have been punished in a higher cost of capital environment.

As such, I'm on Hold for Zeta Global Holdings Corp. stock for the near term.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis.

Get started with a free trial!

This article was written by

I'm the founder of IPO Edge on Seeking Alpha, a research service for investors interested in IPOs on US markets. Subscribers receive access to my proprietary research, valuation, data, commentary, opinions, and chat on U.S. IPOs. Join now to get an insider's 'edge' on new issues coming to market, both before and after the IPO. Start with a 14-day Free Trial.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.