Dr. Reddy's Laboratories: Unpacking The Critical Factors, Reiterate Buy

Summary

- Dr. Reddy's Laboratories Ltd. (RDY) remains an attractive investment due to its strong Q4 and FY'23 numbers, exposure to the Indian generics market, and consistent new product launches.

- RDY is well-positioned in the high-growth generics market, along with other favorable business economics.

- Findings suggest RDY stock could be a buy with a target price of $60/share.

narvikk

Investment Summary

Shares of Dr. Reddy's Laboratories Ltd. (NYSE:RDY) remain attractively valued in my firm opinion and after the company's latest numbers, I am looking to $60/share to the next objective. This is in-line with my previous analysis, and I am keeping the $64 target found in that analysis in situ.

The company rolled in with a strong set of Q4 and thus FY'23 numbers, and further analysis reveals positive trends. Here I'll unpack the company's profitability and demonstrate further the catalytic factors of its exposure to the Indian generics market. These factors combined present a unique value proposition that may be worthwhile looking at for those looking at value-orientated companies, but are prepared to pay 13x pre-tax earnings to do so. Net-net, reiterate buy.

Figure 1. RDY Uptrend since Jan 2022

Data: Updata

Critical Facts

There are two major segments to cover, first, the critical facts, and then the additional factors investors may be overlooking.

1. Q4, FY'23 earnings

There's plenty to be gleaned from the company's latest numbers. It posted Q4 and FY'23 earnings last month.

First to the financial takeouts:

- Q4 sales came to $766mm, a 16% YoY growth rate, on core EBITDA of $198mm. The revenue clip is a 7% sequential decline, which management attributed primarily to sales volatility in its energy business. Looking to the full-year, it is worth noting the 15% YoY growth in net sales to $2.99Bn.

- Growth was underscored by new product launches, which is a key factor in the RDY investment debate. There is good research from McKinsey suggesting that new product launches typically create the most shareholder value, and pharmaceutical companies are one of the major players in new product launches. On asset factors alone (discussed below), I believe this is integral to RDY rating higher over time.

Another point I'd add into the RDY investment mix is the gross it pulls in both on revenues and on operating assets. Consider these results, from Q4 and full-year:

- Q4 gross profit margin pulled in to 57.3% a decompression of ~430bps compared to the previous year. Further, gross pulled into 61.7% and 25.2% for its global generics ("GG"), and pharmaceutical services and active ingredients ("PSAI") segments respectively.

- FY'23 gross margin lifted to 56.7%, another 360bps over the previous year. You can put the decompression down to new product sales, (therefore higher margin mix). Comparatively, it booked 52.1% in GG and 16.2% in PSAI for the year.

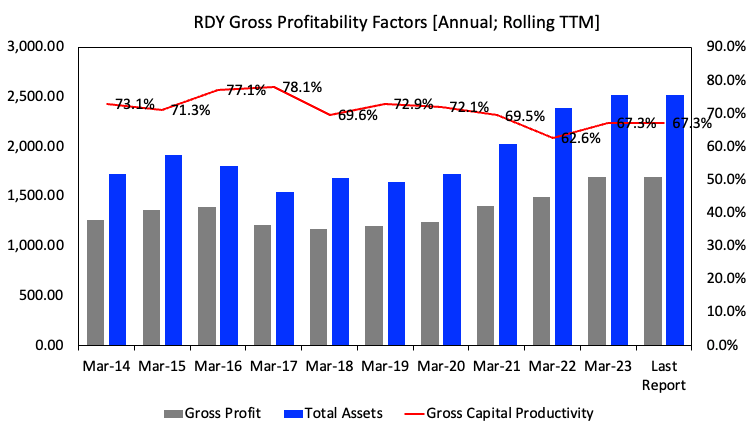

Looking at it from a productivity perspective, you can see the company's gross capital productivity in Figure 2. The annual gross profit is scaled by total assets on a rolling basis. In particular, despite a large jump in operating capital at risk since FY'21, stretching up from ~$1.5Bn to ~$3.5Bn in that time. Yet, the gross profit produced on this has remained steady, paring back from 72% in 2020 to 67% in the last year, despite the broader capital base. To me this is telling of the firm's profitability. You're getting $0.67 in gross back on $3.5Bn on a regular basis, quite attractive business economics in my view.

Figure. 2

Data: Author, RDY SEC Filings

Moving down the P&L, it lost 15% leverage at the SG&A line, reaching $808mm for the full-year (10% growth). Notably, the SG&A cost as a percentage of sales decreased by 130bps compared to the previous year, a result of some operating leverage. Furthermore, RDY's R&D investment came to $65mm, accounting for 8.5% of sales. Importantly, the company's pipeline, currently concentrated in biosimilars, is well capitalized, as R&D expenditure reached $238mm, amounting to 7.9% of sales. The fact RDY has a multitude of potential investment opportunities is also a bullish factor in my view.

Naturally, there are investment implications from the company's latest numbers:

- Core business momentum. RDY experienced consistent growth momentum in FY '23 across all its businesses, even after adjusting for the contribution of COVID-related products.

- Expansion in North America. The firm's revenue in the North American generics and branded markets exceeded the $1Bn mark for the 2nd consecutive year. This is quite the mark, and evidence of the points I was making earlier about value creation through new product launches.

- Capital budgeting. Strategic decisions to divest certain noncore brands in India demonstrates to me the firm's commitment to strengthening its core business. By streamlining operations and concentrating on core competencies, it looks to unlock value this way, through operational efficiencies (to free up margin for earnings growth).

2. Returns on incremental capital

It is also essential to point out RDY's ability to compound capital at rates above the market return, thereby creating shareholder value. This is integral to the RDY investment case in my opinion. Why?

One, the firm is deploying up to $3.5Bn in capital in order to push forward on its growth targets. On these investments, it increased the incremental returns back to 17%, in-line with 2016 range. You're looking at $595mm in annual profit on investor capital based on these numbers, and if it continues on this track, my estimates have the company to be doing at least 17% ROIC into FY'25, quite attractive.

Two, equally as important, you can see the total equity value in the firm has stretched up on an annual basis in Figure 3. As a going concern, investors are paying up to 3x this book value on this firm, as the stock is trading above the 100DMA and 200DMA, as I believe they know the value RDY can create on their equity long-term.

Three, as the equity and capital values grow, you're still seeing 21% ROE and 17% ROIC respectively. Both numbers are ahead of the S&P 500's annualized return, suggesting the company is investing in opportunities more lucrative than what investors can achieve elsewhere. In my view, this is critical in seeing RDY rate higher over time, as it has done to date.

Net-net, these are bullish factors in the risk/reward calculus in my opinion.

Figure 3.

Note: All figures in $mm. (Data: author, RDY SEC Filings)

Potential catalyst - Generics in India

One major point underpinning the RDY investment thesis is the fact it manufactures several generic labels in India. I touched on this in my last publication: "One emergent theme that's spurred up in the past 12-24 months has been the skew of distribution of generic drug volumes away from the U.S. towards Indian pharmaceutical companies. This is propelled by FDA regulatory/approval policies and U.S. patent roadblocks facing competing labels."

I'd like to touch on this further to highlight the investment considerations that investors should consider here, and to illustrate my own thoughtful analysis. Firstly, if you didn't realize, the Indian pharmaceutical industry has witnessed remarkable growth over the years, establishing itself as a global powerhouse in producing and exporting generic drugs. This has been fuelled by domestic and international factors. The market is projected for ~7% CAGR into 2028, to reach a potential $24.5Bn. Plenty of opportunities for RDY to capture this in my view.

Importantly, there are two critical factors here as well, namely:

1. Understanding the growth trends

- One key driver has been the increasing demand for affordable healthcare solutions worldwide. Generic drugs offer cost-effective alternatives to their branded counterparts and have gained significant traction, particularly in emerging markets. India's ability to produce high-quality generic medications at lower prices has positioned it as a prominent player.

- This has been compounded by the patent expiration of several blockbuster drugs in recent years, opening the window of opportunities for Indian pharmaceutical companies.

2. Factors Driving Forecasts

- Cost-effective manufacturing. Principally, the access of large players to low labour costs, availability of skilled human resources, and a well-developed infrastructure for drug production contribute to competitive pricing. Data from FY'19 suggested the average minimum wage for contract workers is US$148/month, vs. US$6,228/month in the U.S. This cost advantage allows Indian pharmaceutical companies to offer generic drugs at significantly lower prices than their global counterparts, quite a competitive advantage that shouldn't be overlooked.

- Large domestic market. India's population of over 1.3Bn presents a substantial domestic market for pharmaceutical products and production. With increasing healthcare awareness and a growing middle class, the demand for affordable drugs is escalating.

- Favourable regulatory environment. Notably, as another competitive layer to pricing, Indian government has implemented policies promoting the pharmaceutical industry's development and growth. Initiatives like the "Make in India" campaign and the introduction of the goods and services tax ("GST") have added a well-needed overhaul to manufacturing standards. This is important in dealing on the global scale, where large contracts are lying around, not to mention for foreign investment.

After the deep-dive into the market opportunity, it appears RDY is well positioned within this sub-sector, and this adds to the buy thesis in my view. You're looking at a leading player in a high-growth market, with fairly unique fundamentals.

Valuation and conclusion

The company is priced at 20x forward earnings and this is a slight premium to the sector's 19.7x. You could say the two are trading in-line. Does RDY deserve the sector multiple? In my view, a firm yes. Given the differentiating factors on fundamentals and sentiment discussed here, the market is correct in pricing it at the sector number.

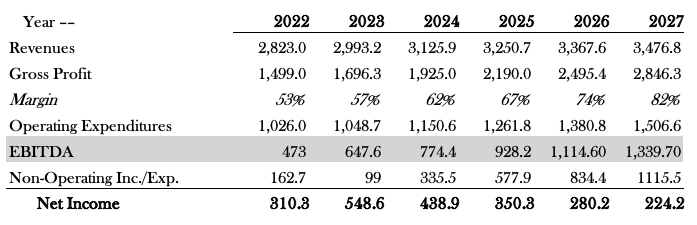

I also believe RDY is an absolute steal at 13x forward EBIT, how the market has priced it 18% below the sector there is beyond me, precisely why I believe it is overlooking the Indian opportunity. Looking to my numbers, I have the company to do $774mm in FY'24 pre-tax earnings [see: Appendix 1], and that calls for $60/share at the sector multiple (774x13/166 = $60). This supports a buy rating, and I am looking to $60 for the next objective.

In short, the investment case remains a firm buy for RYD in my view. There is strong data showing it creating value for shareholders, along with several critical facts. I'd call these:

- Consistent launch of new products;

- High returns on incremental capital;

- Differentiated market exposure (Indian market).

Collectively, these have generated strong returns for investors over the periods to date, and my estimates have these trends to continue, adding bullish weight to the risk/reward symmetry. Net-net, I am reiterating RDY a buy

Appendix 1. FY'24-'27 forecasts

Data: Author Estimates

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of RDY either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.