Latham Group, a leading designer and manufacturer of in-ground residential swimming pools, is expected to see further growth through its direct-to-owner marketing strategy and international expansion.

I assumed that the new Latham Augmented Reality Pool Visualizer app will likely accelerate the demand for the products.

Further digital and marketing efforts could improve the company’s online presence and may bring further FCF growth.

I assumed that the stock repurchase program may bring significant demand for the stock as soon as the Board decides again to continue its stock buyback.

NicoElNino

Latham Group, Inc. (NASDAQ:SWIM) delivered beneficial guidancefor 2023, which is quite impressive considering the current macroeconomic environment. The expectations of market analysts are also beneficial. I believe that further efforts and implementation of the direct-to-owner marketing, which is working pretty well, will likely bring further FCF growth. Besides, international efforts and further manufacturing efficiency improvements recently announced could also represent beneficial FCF growth catalysts. I do see risks from lack of financing, but I believe that there is further upside potential in the stock price than downside risks.

Latham

Latham is the leading designer, manufacturer, and marketer of in-ground residential swimming pools in North America, Australia, and New Zealand.

With an operating history of more than 65 years, it offers the broadest portfolio of swimming pools and related products in the industry, including in-ground pools, pool liners, and pool covers. The company conducts business as one operating segment.

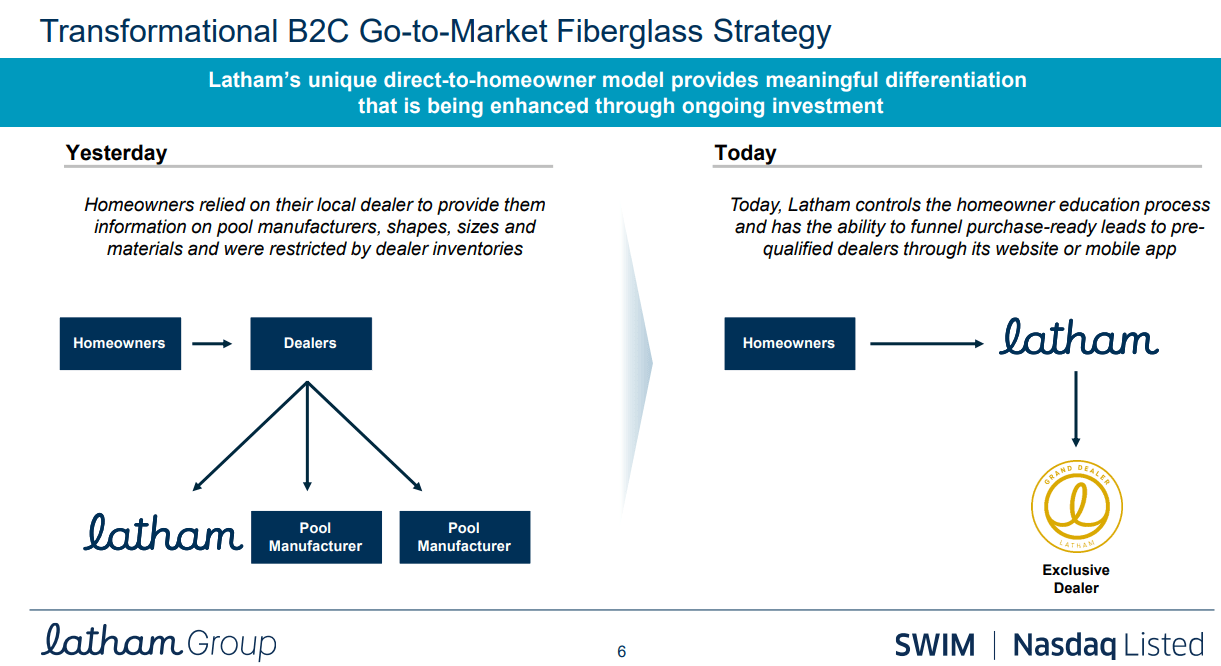

In my view, Latham offers an innovative direct-to-owner marketing approach that has transformed the pool buying process, generating demand and providing leads for its dealer partners. I believe that the long-standing dealer network and a focus on premium quality and aesthetics will likely continue to receive demand for its products.

Source: Investor Presentation

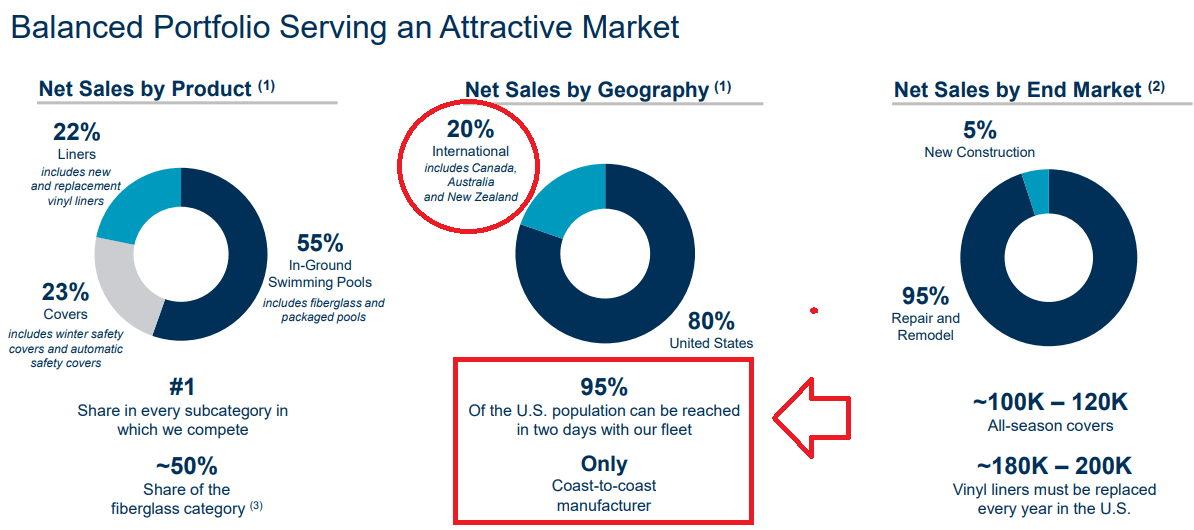

I also believe that the fact that 95% of the total amount of net sales comes from repair and remodel is attractive. Owners of swimming pools, who already know the market, contact the company for repairing and remodeling.

Source: Investor Presentation

I am quite optimistic about the international figures reported by Latham. The company reports that close to 20% of its total net sales comes from Canada, Australia, And New Zealand. With a proven business model in the United States, I believe that further expansion in Europe or Asia could represent a significant revenue catalyst for the company.

Expectations Include Net Sales Growth, Operating Margin Growth, and Positive 2025 FCF

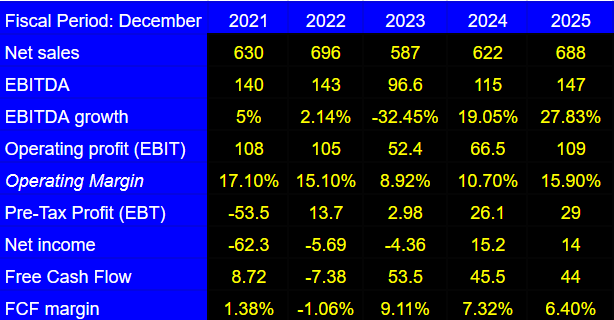

I believe that the expectations of other analysts are optimistic, and they are worth considering. Analysts expect net sales growth in 2024 and 2025 as well as operating margin growth. 2025 net sales would be close to $688 million with 2025 EBITDA of $147 million, 2025 net income of $14 million, and 2025 free cash flow close to $44 million.

Source: Marketscreener.com

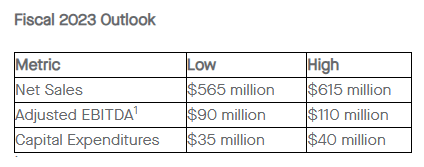

I also believe that the guidance given for the year 2023 is overall optimistic. The company expects 2023 net sales close to $565-$615 million, a maximum adjusted 2023 EBITDA of $110 million, and capex close to $35-$40 million.

Source: Quarterly Press Release

Solid Balance Sheet With Some Debt

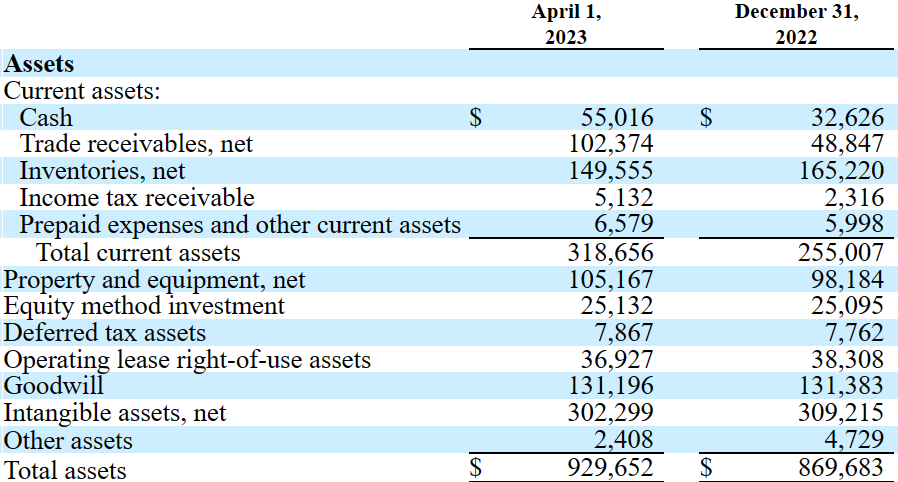

In the last quarter, I did see major changes in the balance sheet. It is quite beneficial that the total amount of cash increased along with increases in trade receivables as well as property, plant and equipment.

Total assets increased along with the total amount of liabilities driven by increases in the total amount of long-term debt. Considering the EBITDA expectations for 2025 of close to $147 million, the total amount of long term debt of $375 million does not seem worrying. At the end of the day, we are talking about a solid business with somewhat stable EBITDA margins and many years in the market.

More in particular, as of April 1, 2023, Latham reported cash close to $55 million, 2023 trade receivables of about $102 million, inventories worth $149 million, and total current assets worth $318 million.

Property and equipment would be close to $105 million with operating lease right-of-use assets of about $36 million, goodwill close to $131 million, and total assets worth $929 million. The asset/liability ratio stands at close to 2x, so I would say that the balance sheet appears stable.

Source: 10-Q

With regards to the list of current liabilities, the company reported accounts payable of $48 million, current maturities of long-term debt close to $3 million, current operating lease liabilities of about $7 million, and total current liabilities of about $106 million.

Also, with long-term debt close to $357 million, deferred income tax liabilities of $50 million, and non-current operating lease liabilities worth $30 million, total liabilities were equal to $554 million.

Source: 10-Q

Under My Optimistic Case Scenario, The Company Is Worth $5 Per Share

Latham appears to be increasing its investment in digital strategies and marketing to generate a greater number of leads for homeowners. Its digital platform offers educational and engagement tools that help homeowners in their pool buying process, including a unique viewing experience, informative videos, budget calculators, and a community of pool experts. I expect that this strategy will likely result in better search engine performance.

I also assumed that new strategic partnerships with priority dealers and training new dealer partners could bring new opportunities and more visibility. In particular, under this case scenario, I assumed that new opportunities outside the United States would be successful.

Under my optimistic case scenario, I assumed that the new Latham Augmented Reality Pool Visualizer app will likely accelerate the demand for the products offered by Latham. In my view, further information to dealer partners about fiberglass pools will likely strengthen the opportunities in different regions. Management noted that further education about the ease and speed of installation of fiberglass pools could be quite useful.

The Latham Augmented Reality Pool Visualizer app allows homeowners to browse fiberglass models and to select from a variety of options from their mobile device. At "Latham University," our dealer partners discover firsthand the benefits of fiberglass pools, including the ease and speed of installation. Dealers also learn both basic and advanced fiberglass pool installation techniques. Source: 10-k

It is evident from the last quarterly report that the company continues to report an increase in property and equipment. Hence, I would expect that further investments in capacity will likely lead to improvement in margins. Besides, the company expects to report further investments in new equipment and manufacturing productivity, which would most likely lead to FCF margin improvements.

We expect that our investments in people, processes, and equipment aimed at enhancing our manufacturing productivity will further expand our margins. Source: 10-k

Finally, I assumed that the stock repurchase program may bring significant demand for the stock as soon as the Board decides again to continue its stock buyback. In this regard, let's note that close to $77 million are available for share repurchases.

As of April 1, 2023, approximately $77.0 million remained available for share repurchases pursuant to the Repurchase Program. Source: 10-Q

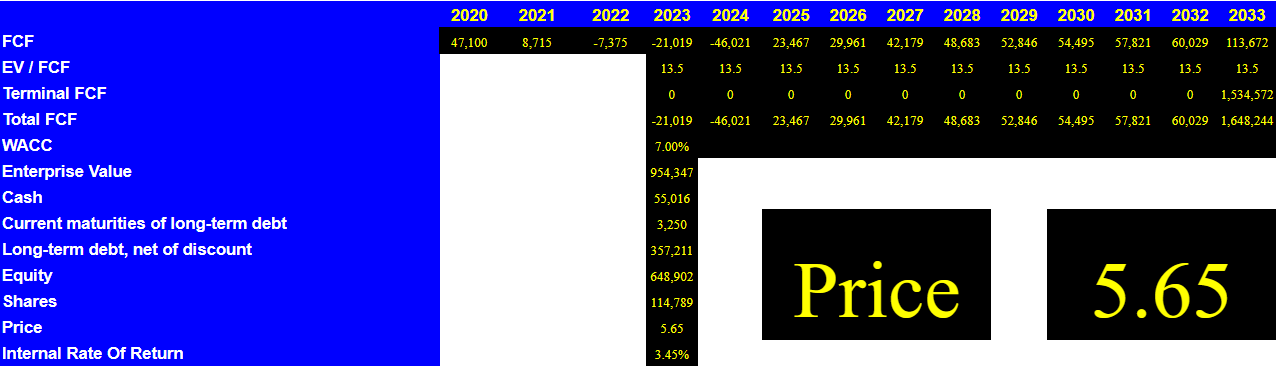

Under this scenario, I included 2033 net income of $150 million, 2033 depreciation and amortization of about $107 million, amortization of deferred financing costs close to -$11 million, and stock-based compensation expense worth $126 million.

Also, with distributions received from equity method investment of close to $10 million and provision on liability for uncertain tax positions worth $8 million, I also included changes in trade receivables of about $72 million.

Source: My Cash Flow Model

If we also assume 2033 inventories of -$27 million, prepaid expenses and other current assets close to $35 million, and changes due to accounts payable of -$135 million, 2033 CFO would be close to $63 million. Finally, with a 2033 capex of -$1 million, 2033 FCF would be close to $113.5 million.

Source: My Cash Flow Model

With other analysts expecting 2025 EV/FCF close to 13x and EV/EBITDA of 3.8x, I believe that we could assume 2033 EV/FCF of 13.5x.

Source: marketscreener.com

Thus, my results would include 2033 terminal FCF of $1.5 billion and an enterprise value of close to $955 million. If we also add cash of $55 million, and subtract current maturities of long-term debt close to $3 million and long-term debt of $357 million, the implied equity valuation would be around $650 million. Finally, the implied fair price would be close to $5 per share with an IRR close to 3.45%.

Source: My Cash Flow Model

Risks And My Bearish Case Scenario

Latham competes with regional and local manufacturers based on factors such as brand recognition and loyalty, quality, performance, and product features. In my view, Latham stands out for its differentiated value proposition, broad product portfolio, domestic manufacturing in the United States, and a leading sales force. However, I believe that failed introduction in new markets outside the United States could lower future net income growth. In my view, growing marketing expenditures could be quite detrimental when net revenue growth does not grow as expected.

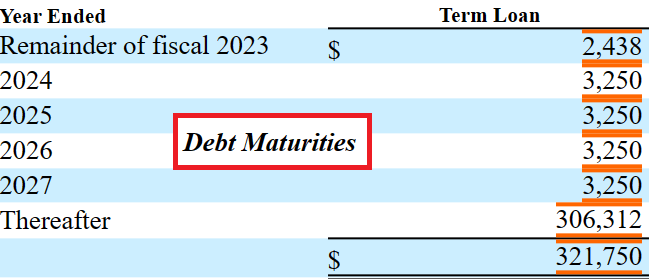

I am not really concerned about the total amount of debt because the debt maturities are supposed to be around 2027. However, I believe that a deterioration of the credit markets and increases in the interest rates overall could affect the FCF margin reported by Latham. Besides, if investors believe that management will not be able to receive beneficial debt terms, they may sell shares even before 2027. As a result, I believe that we may see a decline in the stock price.

The Term Loan matures on February 23, 2029. Loans outstanding under the Term Loan bear interest, at the borrower's option, at a rate per annum based on Term SOFR, plus a margin ranging from 3.75% to 4.00%, depending on the First Lien Net Leverage Ratio, or based on the Base Rate, plus a margin ranging from 2.75% to 3.00%, depending on the First Lien Net Leverage Ratio. Source: 10-Q

Source: 10-k

Consumer changes and tightening consumer credit may also affect the business model of Latham. Consumers may acquire less pools because they do not find cheap financing to make purchases. In this regard, I believe that noting the following information about the expectations for 2023 appears quite relevant.

In economic downturns such as many economists and industry leaders are forecasting for 2023, the demand for swimming pools and related products has declined and we expect that such demand would decline in the future. Source: 10-k

I also believe that shareholders may suffer risks from lack of adequate level of cash. Latham expects to use its CFO, but also a revolving credit facility in the coming months. Besides, the company did not confirm that future debt or equity financing would not be dilutive to stockholders.

We believe that our existing cash, cash generated from operations and availability under our Revolving Credit Facility, will be adequate to fund our operating expenses and capital expenditure requirements over the next 12 months, as well as our longer-term liquidity needs. Source: 10-Q

There can be no assurance equity or debt financing will be available to us when we need it or, if available, the terms will be satisfactory to us and not dilutive to our then-current stockholders. Source: 10-Q

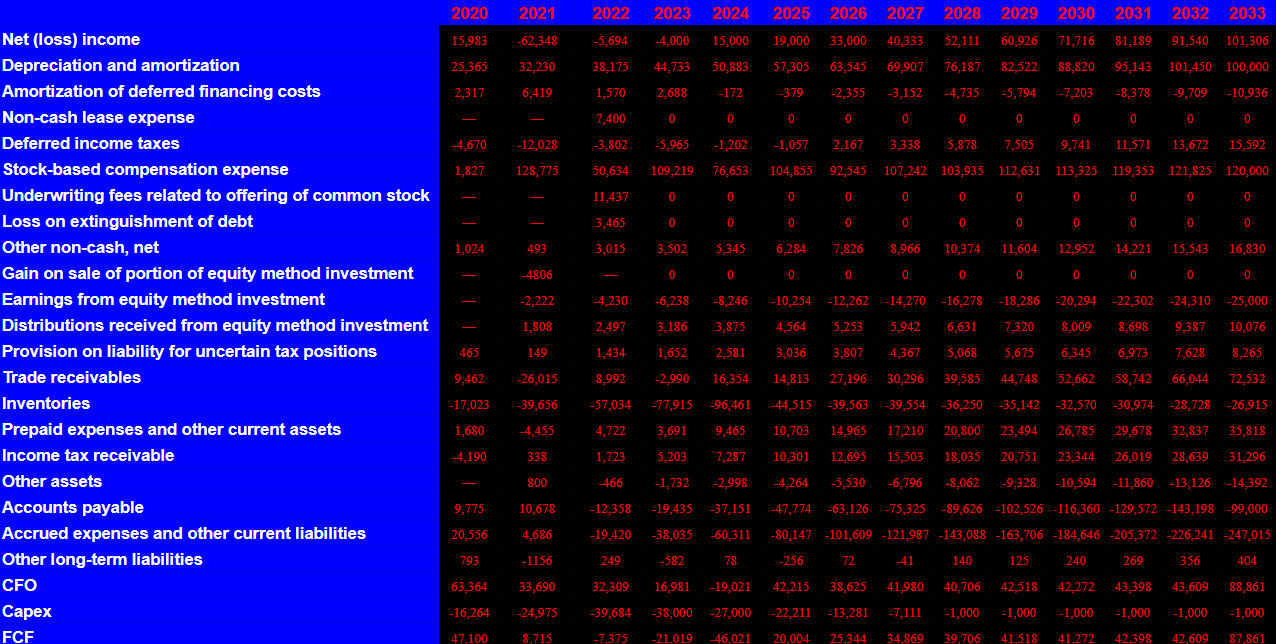

Under the previous conditions, I assumed 2033 net income of $101 million, 2033 depreciation and amortization close to $100 million, 2033 amortization of deferred financing costs of -$11 million, 2033 distributions received from equity method investment close to $10 million, and changes in inventories worth -$27 million. Finally, I would expect 2033 FCF close to $87 million.

Source: My Cash Flow Model

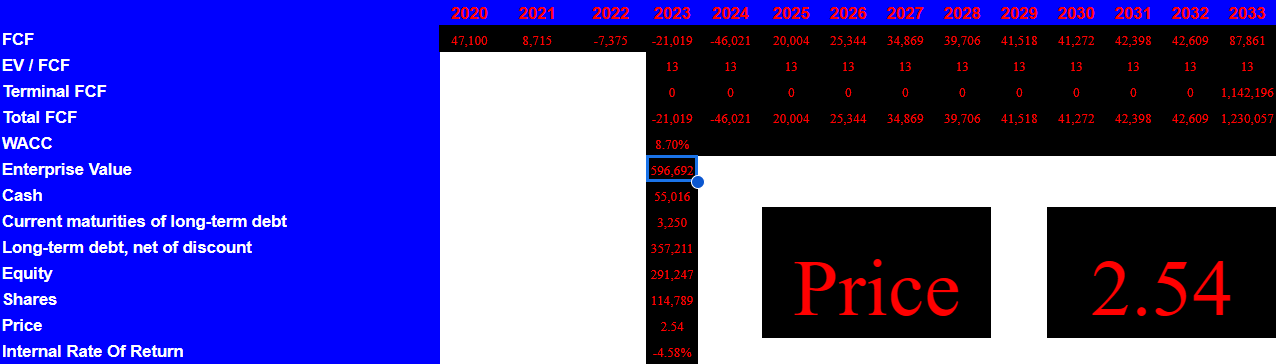

Finally, if we assume WACC of 8.7% and EV/FCF of 13x, the implied enterprise value would be $596 million. If we add cash of $55 million, and subtract current maturities of long-term debt close to $3 million and long-term debt of $357 million, the implied fair price would be $2.54 per share.

Source: My Cash Flow Model

Conclusion

In my opinion, Latham has achieved a strong position by offering a wide range of high quality products and a differentiated value proposition. Its focus on innovation, premium aesthetics, and direct-to-owner marketing will likely continue to generate demand and provide leads for its dealers. Under my best case scenario, further digital and marketing efforts could improve the company's online presence, and may bring further FCF growth. Besides, international expansion, manufacturing efficiency improvement, and more contracts with dealers could represent interesting revenue catalysts. With that, I assumed a bearish case scenario, in which lack of adequate supply of cash, competition, and failed expansion into new markets lead to a lower stock price. I see more upside potential in the stock valuation, but there are many risks to keep in mind.

I am an M&A investment advisor with 10+ years of experience. I used to work for a big institution. I like M&A deals, value investing, and emerging markets. If you see an error please contact: wangluxem@financier.comQuingshan Capital Management provides articles for informational purposes only. I only give my opinion. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on my articles constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of SWIM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.