ZIM: The Value Trap Has Finally Been Exposed

Summary

- The author is bearish on container shipping stocks, particularly ZIM, due to the drop in rates and revenue.

- ZIM's shareholder base consists of many retail investors who were attracted by its low P/E and high dividend yield.

- The author believes that retail investors may not fully understand the risks involved in investing in companies like ZIM.

dbvirago

After writing about the lessors I thought I would write about the container shipping companies themselves. I've got opposite views on both, as the lessors locked in high rates while the container shipping companies on the other side locked in high costs from those lessors and now rates have dropped so revenue has crashed. This combined with many other factors has made me bearish on these stocks, and ZIM Integrated Shipping Services (NYSE:ZIM) seems to be the centre of this as that is where a majority of the retail frenzy is.

Terrible First Quarter Earnings

ZIM's first-quarter earnings report was well below the expectations of the market. It also came with an announcement of no dividends for this quarter and likely for the rest of the year.

I've linked the trailing P&L on a quarterly basis. Last quarter we saw $1.3743bn of revenue, $434.6mm of gross profit and -59.5 of net income.

What makes this worse is that rates have since gone down and future earnings reports will likely be far worse:

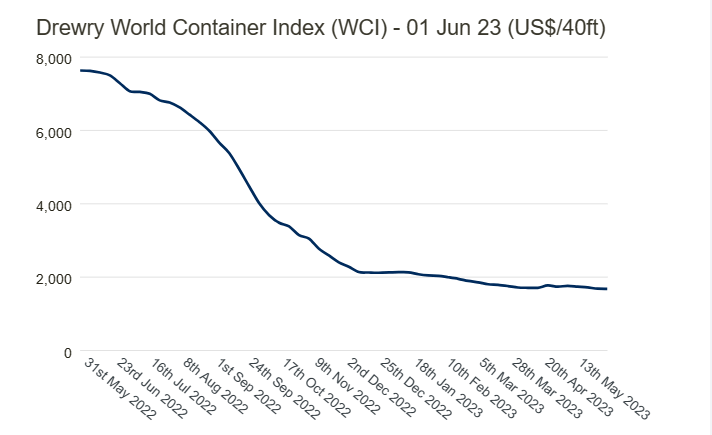

Freight Rates (Drewry)

As can be seen on the above chart in just the last few months rates have gone down further. Rates were around $2000 in the first quarter, but have since declined to $1600, which is a 20% cut in rates. We can adjust last quarter's earnings report to this:

Revenue down 20%: $1.09944bn

Gross Profit at the same COGS would be $159.74mm

EBIT with the same operating expense would be -$288.36mm

Add interest expenses onto the EBIT and you are well above $300mm in losses. I decided to use the same COGS and operating expenses as both tend to be stable from quarter to quarter.

If this wasn't already bad enough, rates pre-covid were normally around $1500 and dipped as low as $700-$1000 when demand was low.

Another key to keep in mind is the volume of freight being shipped; the volume has dropped. I look at this negatively as now the company is fighting a war on two fronts, one against rates and another against volumes going down. This also goes to show that the position of the consumer and consumer demand is starting to quickly weaken.

Because my macro view is that we have a deep, prolonged recession, in this situation, ZIM could be underwater for years on end.

Book Value Is Pointless In This Situation

An argument I've seen from bulls is that ZIM is trading for ≈68% below book value, hence they believe that even if the company currently has cash burn it will be able to withstand it with the high book value and a large amount of cash.

First off the cash burn is $300mm+ per quarter, which if continued for the next two years will remove $2.4bn of cash. This brings the book value from $5bn to $2.6bn, and this assumes other assets stay stable in value.

This also brings up another even bigger point which is that book value doesn't matter if there is no way to extract that book value. To provide an analogy, if I were to gift you your pick of two investments: $1mm all in super liquid and low-risk t-bills or an investment of $5mm worth of very specialized equipment, which would you pick? While $5mm is better than $1mm, in a scenario where you can't liquidate the $5mm of equipment if there are no buyers for the highly specialized equipment, then what's the utility of the $5mm value? Hence the $1mm in t-bills would be a better pick over $5mm in illiquid equipment. That's basically how I see book value, in that unless a company is profitable with a high ROE or unless a company will liquidate its assets and distribute the process to shareholders, book value becomes meaningless. In other words, unless you as a shareholder see any cash in your hands from the low book value, it might as well not matter. In this case, ZIM is unprofitable and is generating a negative ROE as of the last quarter's earnings report, so it can't use its book value to generate a lot of FCF and although ZIM has a lot of cash on its balance sheet it isn't going to pay any dividends, so that's out. All in all, in this situation, I don't see a discount to book value being meaningful as shareholders derive no direct benefit from it.

What Can Management Do?

I biggest issue I see here is that there isn't much management can do to change the P&L. Management of course can't control the revenue and COGS. So the gross profit is essentially at the mercy of the market. All they can control is the operating expenses, which last quarter was $448mm. In this situation, they could try to cut expenses, but I feel as though it's like putting a bandage over a tumour, as it might slow the cash bleed by a bit, but it doesn't turn things around. Otherwise, on the balance sheet all the management could do is invest the cash elsewhere such as leasing more ships at a cheaper rate or stock buybacks if the price of the stock goes low enough, but this wouldn't help as it means taking on more risk. Diluting the stock here to get more cash after the price has gone down a lot also wouldn't be wise. So I really feel as though the management is in a situation where even if they have a crystal ball and can tell the future, they can't change the direction that the company is headed in. At the end of the day, I believe that ZIM has just become a levered play on where container freight rates are headed and management can't do much about it.

Who Bought This?

What stands out to me is the shareholder base. I often like to look at the shareholders that own a company to find out what kind of hype is behind it and where the flows will go. For example, the shareholder base of a company like Berkshire Hathaway (BRK.A) is buy-and-hold, so even in a downturn I wouldn't expect the drawdowns of its stock to be larger than the benchmark (SPX). On the other hand, there are companies that have shareholders that are only holding on for a certain thesis; an example would be most oil and gas companies where shareholders are often only holding on to the stock as a levered oil and gas price play, and if prices were to drop even if the company was growing and fundamentally sound, the stock would go down. In the case of ZIM, it seems many retail investors bought in as it was going for a low P/E and had an insanely high dividend yield.

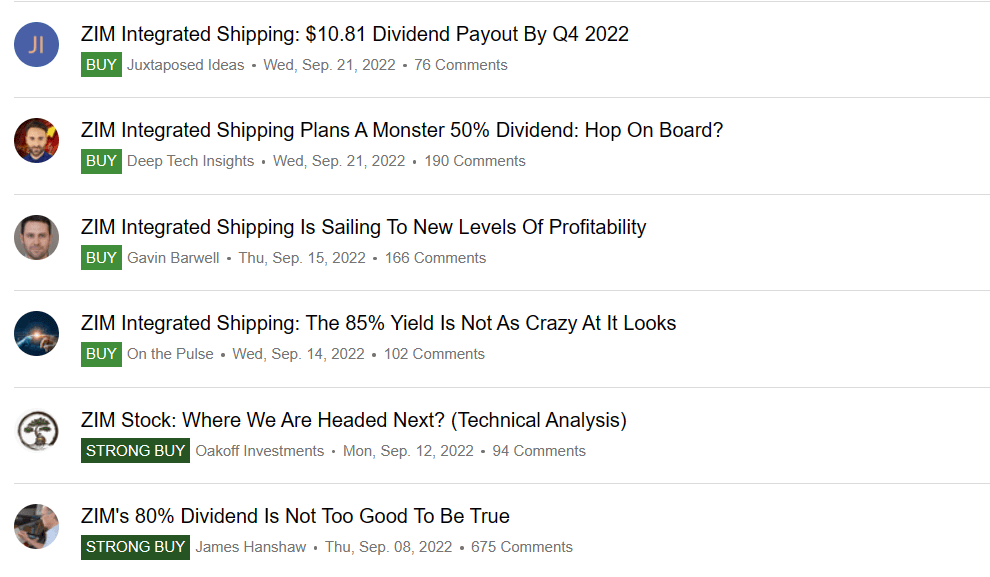

Seeking Alpha

Just as an example, I took a screenshot of articles from September 2022 that came out on this stock. As can be seen, most of the articles mention the insanely high dividend and how the company was so profitable. In fact, when I looked through the articles on Seeking Alpha from 2022 it was rare to find a bearish article. I also saw this when I went to sites like Yahoo Finance which have a forum where retail investors will provide their thoughts on a stock and almost everyone was bullish on the stock in 2022. To put it in a blunt and brutely honest way many retail investors know enough about stock picking to think they are right, but not enough to know when they are wrong. In other words, many retail investors know just enough to be dangerous when picking stocks. ZIM is the perfect example. Most retail investors know they should buy into companies that go for a low valuation and return capital to shareholders(this is knowing enough to be right), but what they don't understand is that ZIM's business model is very cyclical thus the revenue is very volatile, meaning that the stock could easily be a value trap as the earnings could go negative as they did in the last quarter; on top of this, the dividend isn't stable as it changes from quarter to quarter unlike dividends from large-cap companies that are dividend aristocrats; this is the part where retail investors don't know enough to know when they are wrong. Hence I say that retail investors investing in stocks like this are playing with fire without realizing it.

Going back to the comment about the shareholder base, I suspect that over time the trailing P/E ratio of this stock will go up and eventually negative(keep in mind most sites won't show a negative P/E ratio as they remove it entirely when a company is unprofitable) as it goes through an earnings recession; on top of this, the trailing dividend yield will go down and eventually to zero. As this happens the hyped retail investors that originally brought this stock from $11 to $88(plus likely reinvested dividends along the way) and now sold it down to $14 will likely sell all they own as they realize this doesn't serve the original purpose of high dividends. Because of all of this, I feel as though there is still more selling coming from retail investors who were simply looking for an easy high-yield play.

What's The Trade Then?

Once I came to my conclusion I did have to ask myself what the trade then is. The issue at this time is that the stock price is down so much that I find it hard to put a short on it as the upside risk is so big compared to the downside.

So in this situation, if I were an investor I would sit on my hands and wait till the stock price goes significantly lower and the other side of the downturn, which could potentially take another 2 years to play out I would look to get long.

I would also look at a long position in the lessors like Danaos (DAC) which I'm bullish on and have written a write-up about prior. They are essentially in the opposite situation as they have already locked in their revenues.

If I were a trader/speculator that was interested in trading this on a shorter-term basis I would look for the price to get back to where it was pre-earnings, which is around $17.50. If it does it provides an enticing short there with a tight stop loss at around $18.50. This would be more akin to speculating than investing, but an enticing one at that. I reason I believe it would be enticing with that setup is that you would get to short at pre-earnings release prices when the market didn't know about the horrendous earnings report that was about to be released, yet we do know about the earnings report, so it's as if we have an edge by shorting there.

The Bottom Line

The bottom line here is pretty simple: I expect ZIM to burn through over $300mm of cash per quarter. This completely changes the retail investor narrative of using this stock as a cheap yield play and a deep value play. This stock has gone from a deep value play to a value trap very quickly, and my belief is that a lot of retail investors who bought in just because of the low P/E and high yield have yet to sell out. On top of this management has little ability to manoeuvre in this situation as the revenue of the company is at the mercy of the market, so all they can do is cut costs to try to slow the bleeding.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.