ON Semiconductor: Leading Provider Of Intelligent Power And Sensing Solutions

Summary

- ON Semiconductor Corporation is a leading provider of intelligent power and sensing solutions with a focus on automotive electrification and charging systems.

- Recent performance in the automotive segment has been lackluster, with flat sequential growth in revenue, leading to concerns about the company's outlook.

- Despite the challenges, ON Semiconductor is well-positioned to benefit from tailwinds in the automotive and industrial markets, and its relatively low debt strengthens its financial position.

- I do much more than just articles at Deep Value Returns: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

metamorworks/iStock via Getty Images

Investment Thesis

ON Semiconductor Corporation (NASDAQ:ON) is yet another semiconductor company that is having a very strong 12-month performance, with its stock up 30% in the past twelve months.

However, despite being positioned in a very hot sector, the stock is not expensive at very approximately 18x this year's EPS.

All in all, I believe that there's a lot to like from this investment.

Why ON Semiconductor? Why Now?

ON Semiconductor is a leading provider of intelligent power and sensing solutions. On Semiconductor specializes in developing technologies that enable automotive electrification and efficient charging systems for industries like automotive and industrial infrastructure sectors.

The company has undergone a transformation in the past 2 years, streamlining its product portfolio and focusing on silicon carbide technology. This has allowed ON Semiconductor to go after the rapidly growing market of electric vehicles and ADAS (Advanced Driver Assistance Systems).

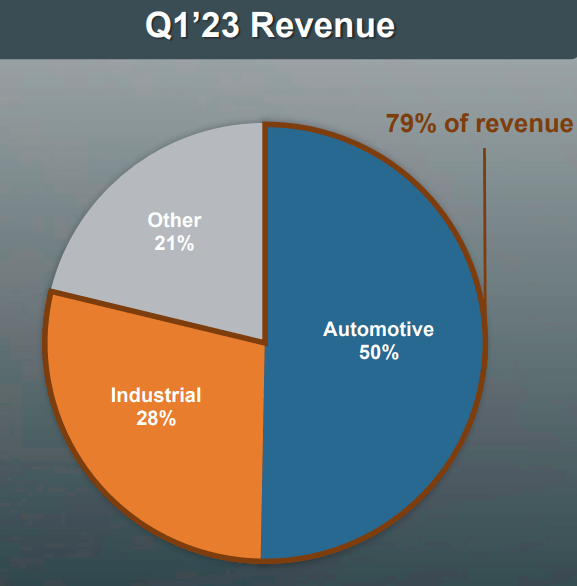

As a consequence of this streamlining, asides from losing some of its revenues, presently 50% of its business is derived from its automotive exposure.

ON Q1 2023

However, as a consequence of all this focus on its automotive exposure, any lackluster performance and investors would rapidly be left unimpressed. And that's what happened in this quarter, with its automotive revenue reporting flat sequential growth.

Essentially, investors are looking beyond its recent past. Investors are zeroing in on its outlook ahead. And the outlook for ON Semiconductor isn't all that impressive, something we'll discuss in more detail next.

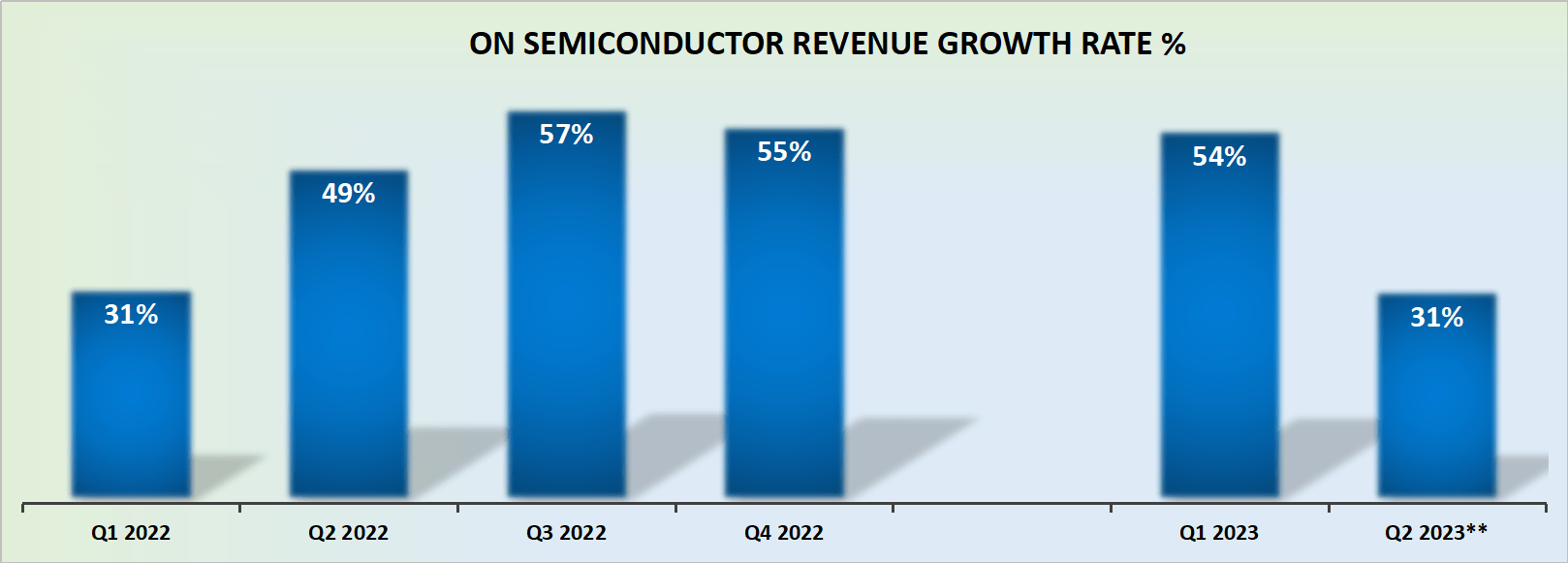

Revenue Growth Rates Moderate

ON revenue growth rates

Highlighted above, we get to the crux of the problem. Investors were more than willing to embrace exposure to the sluggish auto market when ON Semiconductor was printing 50% CAGR figures.

But now that its outlook has suddenly moderated down to approximately 30% CAGR, investors are being slightly more timid before aggressively backing this stock.

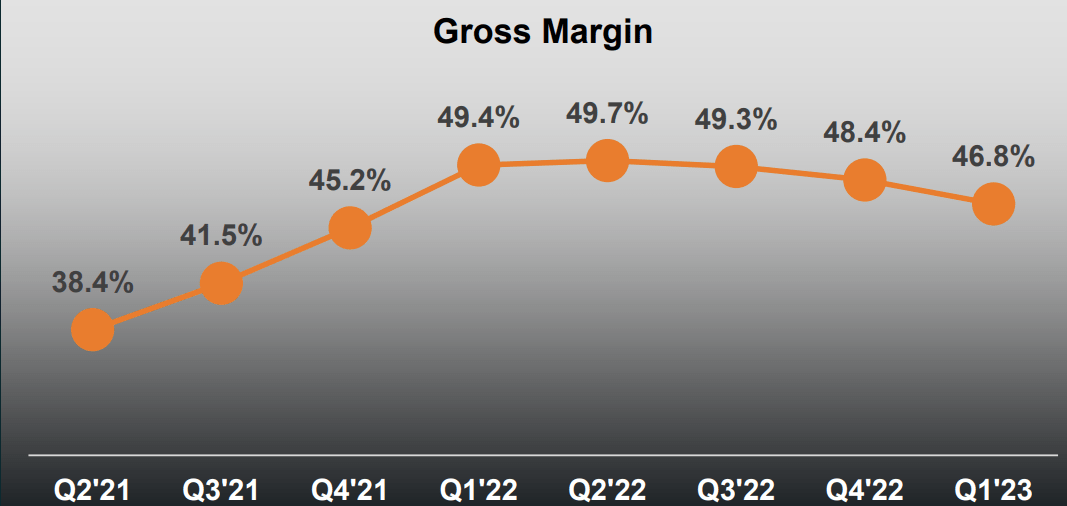

Profitability Profile Could Improve in 2024

On Semiconductor's gross margin profile is expected to compress around 200% basis y/y as it heads to Q2 2023 to around 47.5%. That being said, it is expected to be a slight upturn sequentially, which investors see as a positive turn of events.

ON Semiconductor Q1 2023

Indeed, as you can see above, ON Semiconductor saw its gross margin profile compress for four consecutive quarters.

Consequently, the fact that Q2 2023 is guided to an approximately 100 basis points improvement sequentially from Q1 2023, inspires hope that the trough could be in for ON Semiconductors.

On the other hand, investors are now naturally questioning, how much of this gross margin improvement is in fact down to the underlying business improving? And how much of this gross margin improvement is a one-off outcome of the businesses that were sold off in the past year?

Perhaps this is not the real question as it pertains to its profitability prospects near-term. Perhaps a better question could be how long until ON Semiconductor's utilization rate moves back to mid-70s%?

This question was discussed on the earnings call and this is what ON Semicondutor's CFO Thad Trent stated,

So the utilization dropped in the quarter from about 74% to 71%. We expect, kind of, what we're seeing right now is utilization to stay in that range plus or minus for the remainder of the year.

Meaning that for now, the business is being run as optimally as possible and that investors will need to be patient as ON Semiconductor rebuilds its gross margin profile higher, probably in 2024.

The Bottom Line

ON Semiconductor has undergone a transformation, streamlining its product portfolio and targeting the electric vehicle and ADAS markets.

However, its recent performance in the automotive segment has been lackluster, leading to concerns about its outlook. Investors are cautious due to a moderation in revenue growth rates and a compression in gross margin.

I believe that its profitability profile is expected to improve in 2024, but questions remain about the underlying business improvement.

Nonetheless, ON Semiconductor Corporation is well-placed to benefit from tailwinds in the automotive and industrial markets. Furthermore, the business doesn't hold a substantial amount of debt, as its $2.7 billion of cash nearly fully offsets its total debt outstanding.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.

This article was written by

DEEP VALUE RETURNS: The only Marketplace with real performance. No gimmicks. I provide a hand-holding service. Plus regular stock updates.

We are all working together to compound returns.

WARNING: Any stocks that you feel like buying after discussions with me are your responsibility.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.